Identity Theft Remedies SC Strategies To Recover and Rebuild After a Breach

Identity theft can devastate your finances and credit in weeks. We at Hays Cauley, P.C. help South Carolina residents understand their identity theft remedies SC and take back control.

This guide walks you through immediate actions, credit recovery steps, and legal options available to you. You’ll learn concrete strategies to rebuild what was damaged and protect yourself going forward.

What to Do in the First 48 Hours After Identity Theft

Act Fast to Minimize Financial Damage

The first two days after discovering identity theft determine how much money you lose. Acting within 24 hours reduces your losses to about $1,200, according to the Federal Trade Commission, while delays push losses to around $4,800. Speed matters more than perfection at this stage. File an official identity theft report at IdentityTheft.gov within 24 to 48 hours to create a documented legal record recognized nationwide and signal to creditors that you are a victim. Save your Identity Theft Report number immediately-you will need it for every dispute with creditors and credit bureaus.

Contact Your Financial Institutions

Next, contact your banks and credit card companies directly using the phone numbers on your statements, not numbers from emails or texts that could be fraudulent. Report any unauthorized transactions and request that they freeze or close compromised accounts. Ask each institution to flag your account with a fraud alert so they verify your identity before processing future requests. This step stops additional unauthorized charges while you work through the recovery process.

Place Fraud Alerts and File a Police Report

Place a fraud alert with one of the three major credit bureaus-Equifax, Experian, or TransUnion. This takes under 10 minutes per bureau and prompts lenders to verify your identity before opening new credit in your name. The initial alert lasts one year; request a seven-year alert with written confirmation for extended protection. Processing happens the same day you contact them.

File a police report within 24 hours of discovering the theft. South Carolina law requires law enforcement to accept your report and provide you with a case number and copies for disputes. The South Carolina Law Enforcement Division maintains victim records, and having an official police report strengthens your credibility with creditors and credit bureaus. File a complaint with the Federal Trade Commission at FTC.gov or call 1-877-438-4338 to create an official record of the theft.

Document Everything From Day One

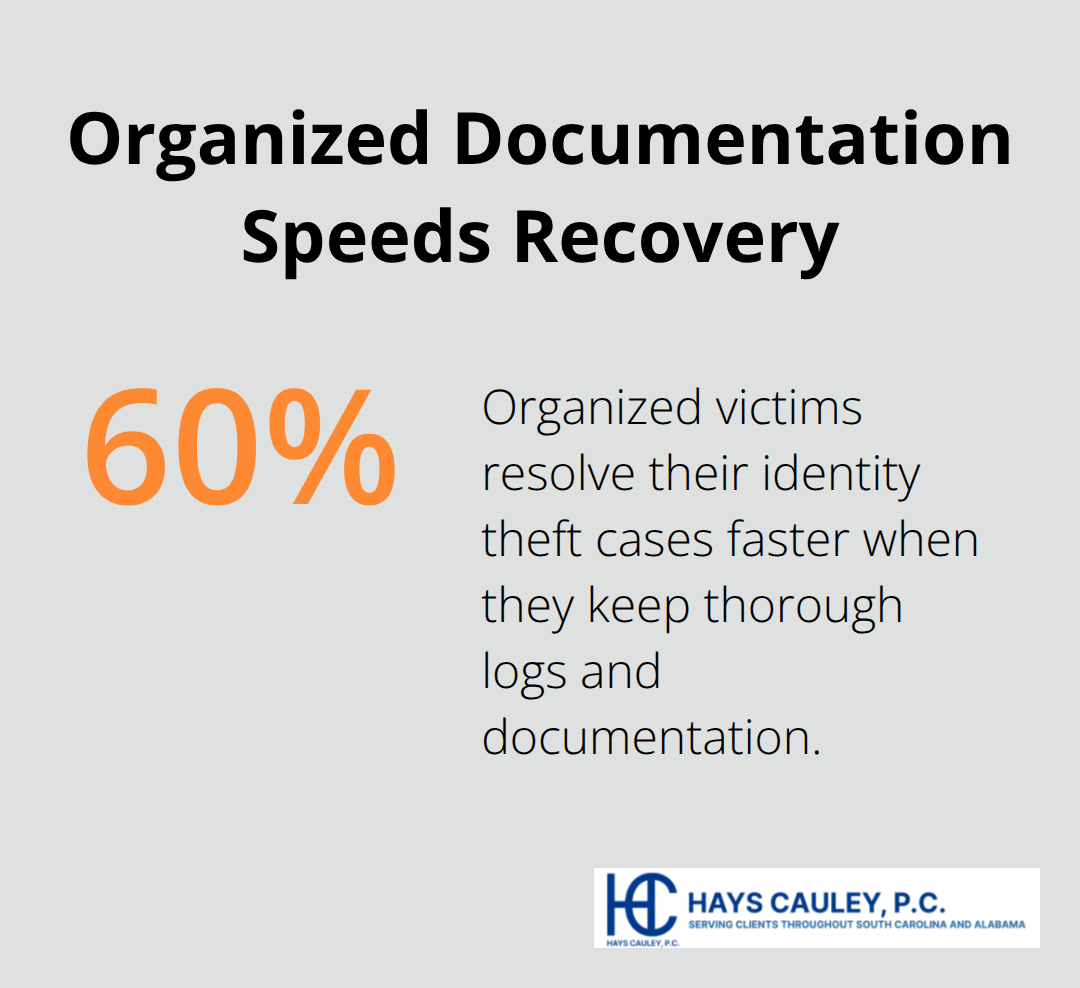

Contact the South Carolina Department of Consumer Affairs Identity Theft Unit at IDTheftHelp@scconsumer.gov or 1-800-922-1594 for free assistance and access to the Identity Theft Toolkit. Keep copies of your FTC report and police reports, all correspondence with banks and credit bureaus, screenshots of fraudulent activity, and a detailed log of dates, names, case numbers, and outcomes. Organized victims resolve cases about 60% faster than those who do not organize, according to the Identity Theft Resource Center. This documentation becomes essential for disputes with credit bureaus and potential legal action later.

With these immediate steps completed, you can now focus on reviewing your credit reports to identify all fraudulent accounts and begin the dispute process.

Rebuilding Your Credit After Identity Theft, Serving South Carolina, including Greenville, Columbia and Charleston

Pull and Review Your Credit Reports

Pull your free credit reports from annualcreditreport.com immediately-the only authorized source for all three bureaus. Review every account listed for unfamiliar entries, inquiries you didn’t authorize, and late payments you never made. About 1 in 5 credit reports contain inaccuracies according to the Federal Trade Commission, so errors may appear alongside actual fraud. Print and annotate each report, marking every suspicious item with dates and account numbers to create your dispute roadmap. You’re entitled to one free report per bureau annually, but identity theft victims can pull additional reports every 90 days at no cost during recovery.

Dispute Fraudulent Accounts Systematically

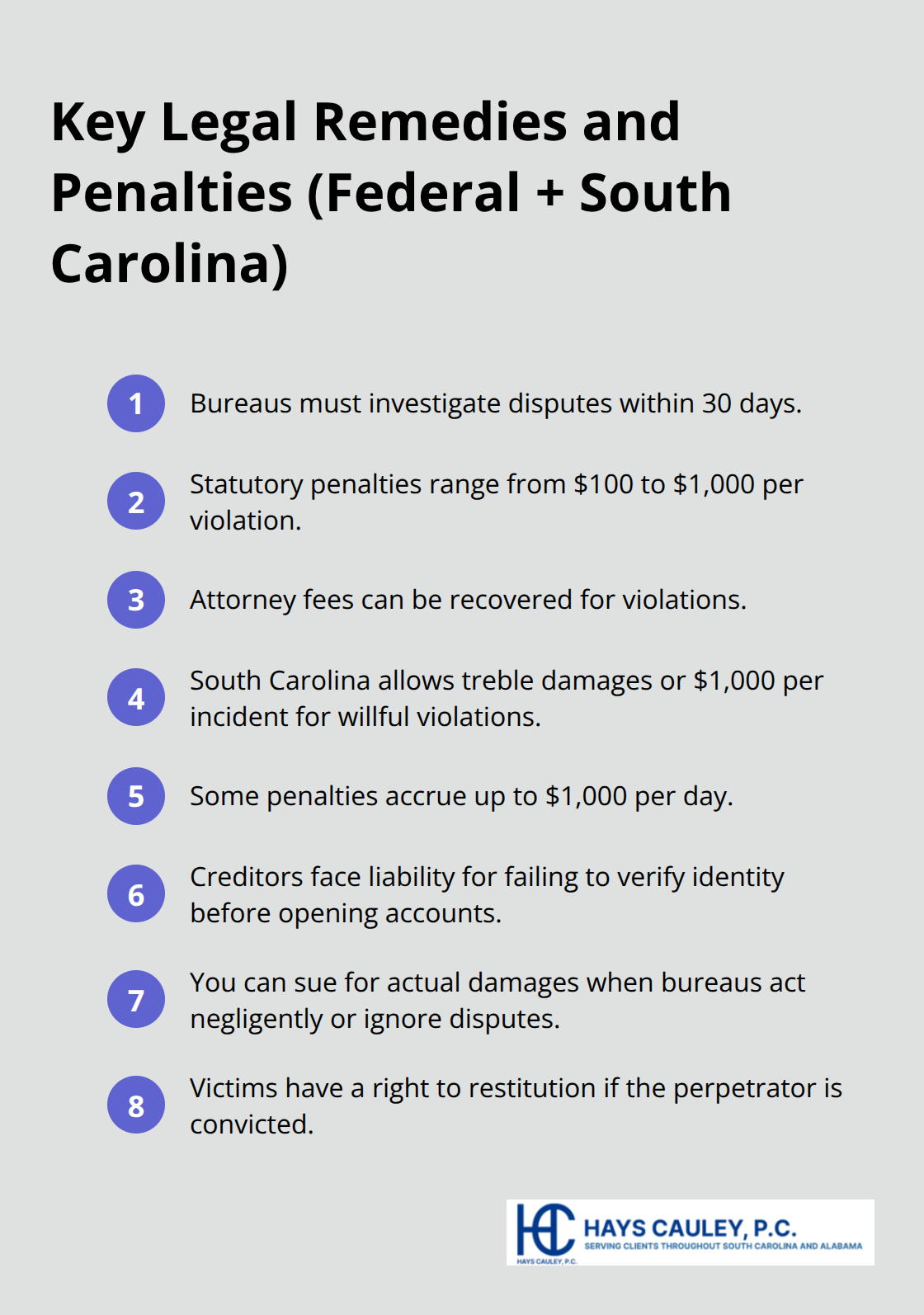

File written disputes with each credit bureau within 30 days of receiving your reports. Use certified mail with return receipt and include your FTC Identity Theft Report number on every communication. List each fraudulent account separately with the account number, creditor name, amount, and discovery date. The Fair Credit Reporting Act requires bureaus to investigate within 30 days and remove items confirmed as inaccurate. Contact each creditor in writing about fraudulent accounts using the same certified mail method simultaneously. Expect updates to appear on your credit reports within 30 to 90 days per account. If a creditor or bureau refuses to remove verified fraud, you have legal grounds to pursue civil claims under South Carolina law. Violations can result in actual damages, penalties up to $1,000 per incident, and attorney fees for willful misconduct.

Monitor Credit Activity During Recovery

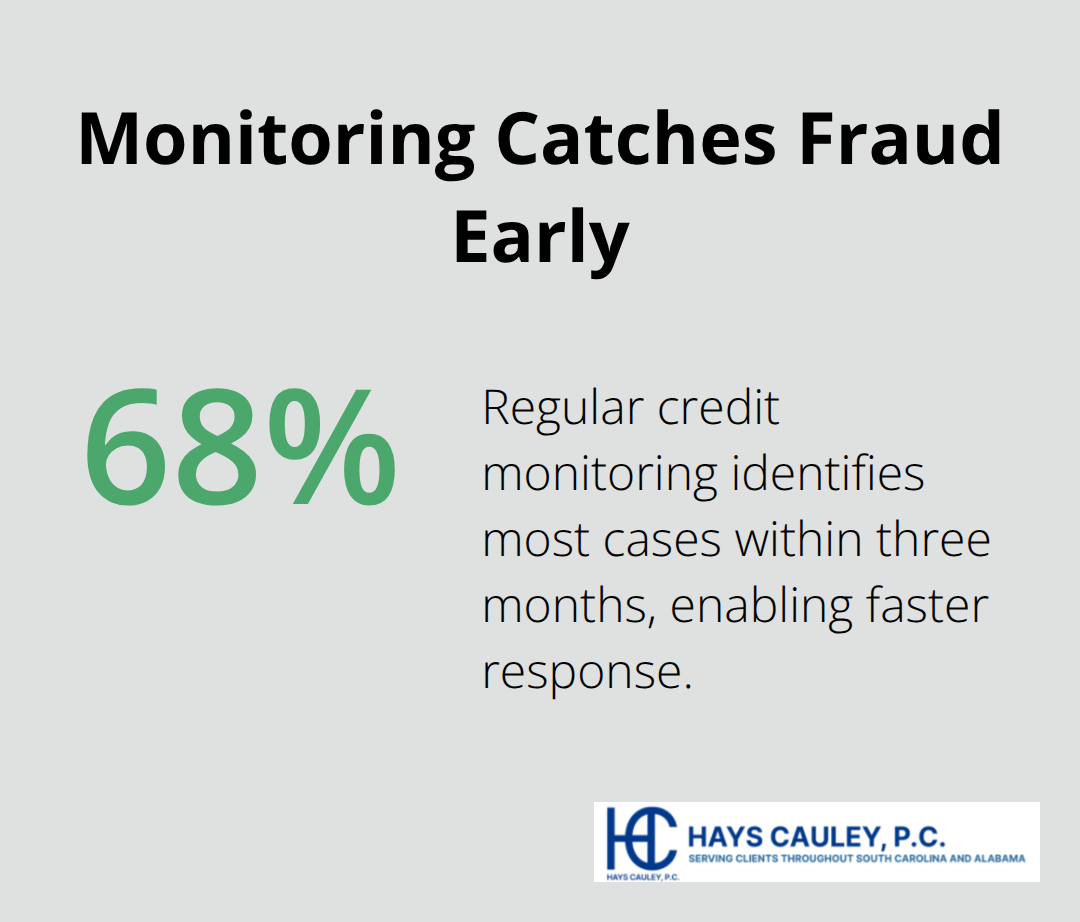

Set up ongoing credit monitoring and check your reports quarterly for the first two years, then annually afterward. Watch for credit score drops of 50 to 100 points paired with unfamiliar accounts or late payments as red flags of new fraudulent activity. Regular credit monitoring detects roughly 68% of identity theft cases within three months according to Federal Trade Commission data. Pull free reports from annualcreditreport.com on a rotating schedule so you review different bureaus every 30 days.

Track your credit score changes in a recovery log alongside every dispute, creditor contact, response, and reference number. Meaningful score recovery typically occurs within 12 to 18 months after you remove fraudulent accounts (if no new fraud occurs). South Carolina law allows you to request a judicial determination of factual innocence if your identity was used to commit crimes, creating a permanent record that clears your name and supports your recovery effort.

Understand Your Legal Protections

The Fair Credit Reporting Act protects you when credit bureaus fail to investigate disputes or remove inaccurate information. You can pursue civil claims for actual damages, statutory penalties, and attorney fees if a bureau acts negligently or willfully violates your rights. South Carolina law amplifies these protections-violations can result in damages up to three times your actual losses or $1,000 per incident, plus attorney fees for willful violations. Some penalties accrue daily up to $1,000 per day, making persistent violations costly for creditors and bureaus. If disputes stall or creditors resist removal of fraudulent accounts, a consumer protection attorney can navigate the legal process and hold negligent parties accountable. With your credit reports under review and disputes filed, you can now explore the broader legal remedies available to you under federal law.

What Federal Law Gives You Against Credit Bureaus and Creditors, Serving South Carolina, including Greenville, Columbia and Charleston

The Fair Credit Reporting Act Protects Your Right to Accurate Reports

The Fair Credit Reporting Act is your primary weapon against credit bureaus that refuse to fix fraud on your reports. Under this federal law, credit bureaus must investigate disputes within 30 days and remove items they cannot verify as accurate. If a bureau violates this requirement or acts negligently, you can sue for actual damages plus statutory penalties ranging from $100 to $1,000 per violation, plus attorney fees. South Carolina amplifies these protections significantly-state law allows damages up to three times your actual losses or $1,000 per incident for willful violations, with some penalties accruing daily up to $1,000. This means a creditor or bureau that knowingly ignores your dispute faces mounting liability.

Federal Crime Penalties and Your Right to Restitution

The Identity Theft Enforcement and Restitution Act makes identity theft a federal crime with penalties up to 15 years imprisonment for offenders. More importantly for your recovery, this law establishes your right to restitution from the perpetrator if caught and convicted. When you file written disputes with certified mail and a bureau ignores them, you have grounds for civil action. South Carolina courts recognize these federal protections and will award damages when bureaus fail their legal obligations.

Creditor Violations and the Fair Debt Collection Practices Act

If a creditor resists removing fraudulent accounts after you send written notice with your FTC Identity Theft Report number, that creditor violates the Fair Debt Collection Practices Act and state law. Document every refusal in writing and keep copies of all correspondence with dates and reference numbers. A creditor who opened fraudulent accounts without proper verification also bears liability, since the Fair Credit Reporting Act requires creditors to use reasonable procedures before extending credit. If a creditor failed to verify your identity before issuing a fraudulent credit card or loan, that creditor bears liability for damages.

Law Enforcement’s Role in Your Recovery

Law enforcement agencies in South Carolina take identity theft seriously, but they focus on criminal prosecution rather than your financial recovery. Your police report creates an official record that strengthens your credibility with creditors and credit bureaus, but getting law enforcement to pursue the perpetrator depends on case specifics and available resources. The South Carolina Law Enforcement Division maintains victim records, and filing a report within 24 hours of discovery gives you a case number for disputes. However, most victims recover their finances through civil remedies rather than criminal restitution.

How an Attorney Holds Negligent Parties Accountable

A consumer protection attorney becomes invaluable when disputes stall or creditors resist removal of fraudulent accounts. An attorney can identify which creditors and bureaus violated their legal obligations, calculate your actual damages under South Carolina law, and negotiate settlements or litigate if necessary. Your attorney can also pursue claims against creditors who opened fraudulent accounts without proper verification. The combination of federal law protections and South Carolina’s enhanced remedies creates a strong framework for recovery-but only if you act systematically and document everything from day one.

Final Thoughts

Identity theft recovery takes months, not weeks, but you now possess the tools to fight back effectively. File your FTC report and police report within 24 hours, place fraud alerts and freeze your credit with all three bureaus, pull your credit reports from annualcreditreport.com, and dispute every fraudulent account within 30 days using certified mail. Organized victims resolve cases 60% faster than those who skip documentation, so track every communication, reference number, and outcome in a recovery log from day one.

Long-term protection starts immediately through practical habits that prevent the next breach from becoming the next disaster. Use passwords of at least 16 characters with uppercase letters, numbers, and symbols, enable two-factor authentication on banking and email accounts (preferring authenticator apps over SMS codes), stop carrying your Social Security number, and shred pre-approved credit offers. Continue quarterly credit monitoring for two years after removing fraudulent accounts, then switch to annual checks to catch new fraud early.

South Carolina provides free resources through the Department of Consumer Affairs Identity Theft Unit at IDTheftHelp@scconsumer.gov or 1-800-922-1594, and Hays Cauley, P.C. helps consumers navigate identity theft remedies SC when disputes stall or creditors refuse to remove fraud. You don’t have to fight this alone, and recovery becomes possible when you act fast, document thoroughly, and pursue every legal remedy available to you.