Your credit score affects everything from loan approvals to interest rates. A South Carolina credit fix starts with understanding what’s actually on your report and why it matters.

We at Hays Cauley, P.C. have helped many people rebuild their credit by taking concrete steps and avoiding common pitfalls. This guide walks you through the process.

What’s Actually on Your Credit Report

The Information Lenders See

Your credit report is a financial record that lenders use to decide whether to approve you for loans and at what interest rate. It contains payment history, outstanding debts, credit inquiries, and public records like judgments or bankruptcies. The three major credit bureaus-Equifax, Experian, and TransUnion-compile this information from creditors, collection agencies, and court records. Each bureau may have slightly different data, which is why checking all three reports matters.

How Common Errors Damage Your Score

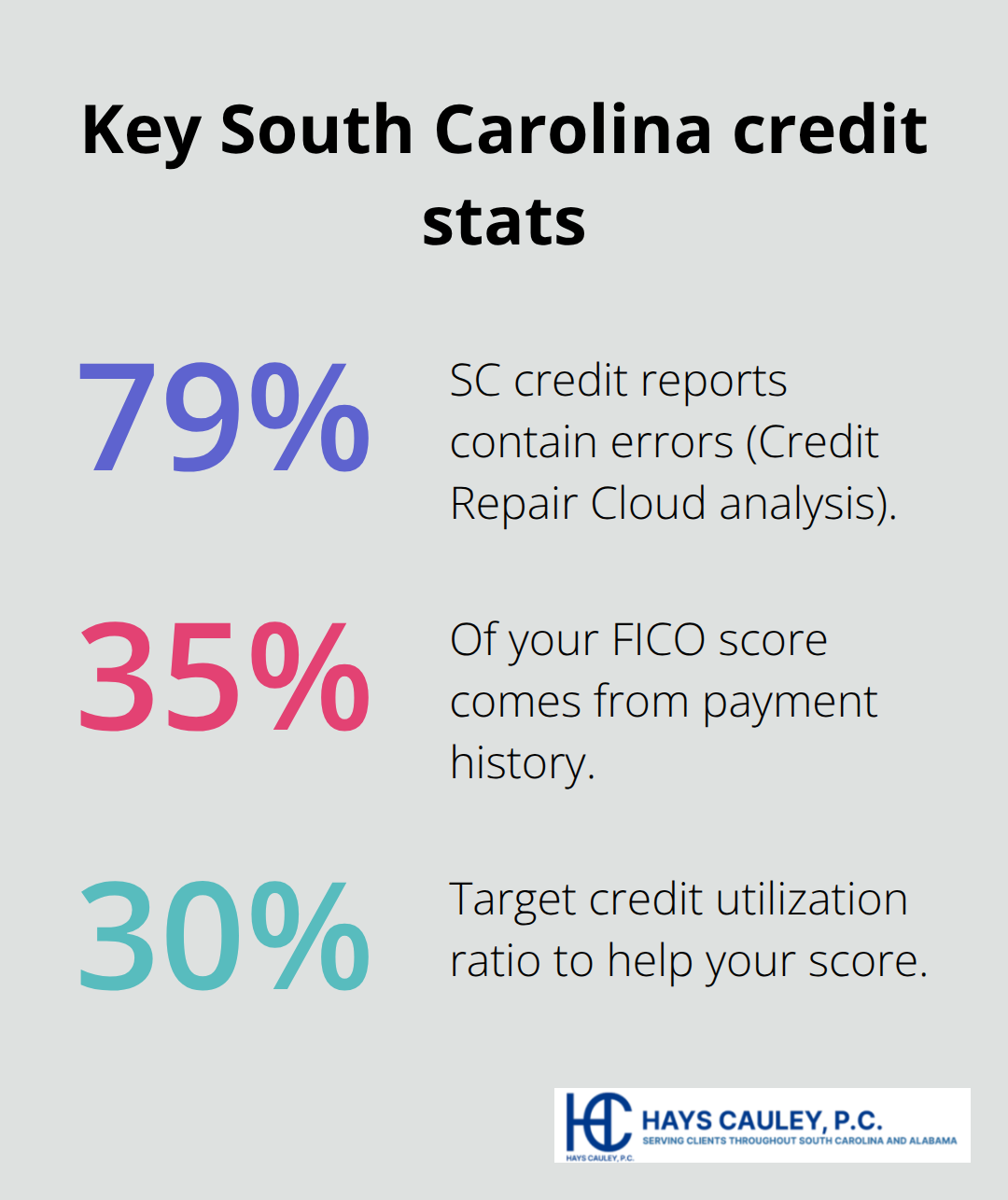

According to Credit Repair Cloud’s analysis, 79% of South Carolina credit reports contain errors, ranging from duplicate accounts and incorrect balances to late payments that weren’t actually late and closed accounts still showing as open. A single inaccuracy can drop your score by 50 to 100 points depending on the error type and your overall profile. The Fair Credit Reporting Act requires bureaus to investigate disputes within 30 days and correct inaccurate information at no cost to you.

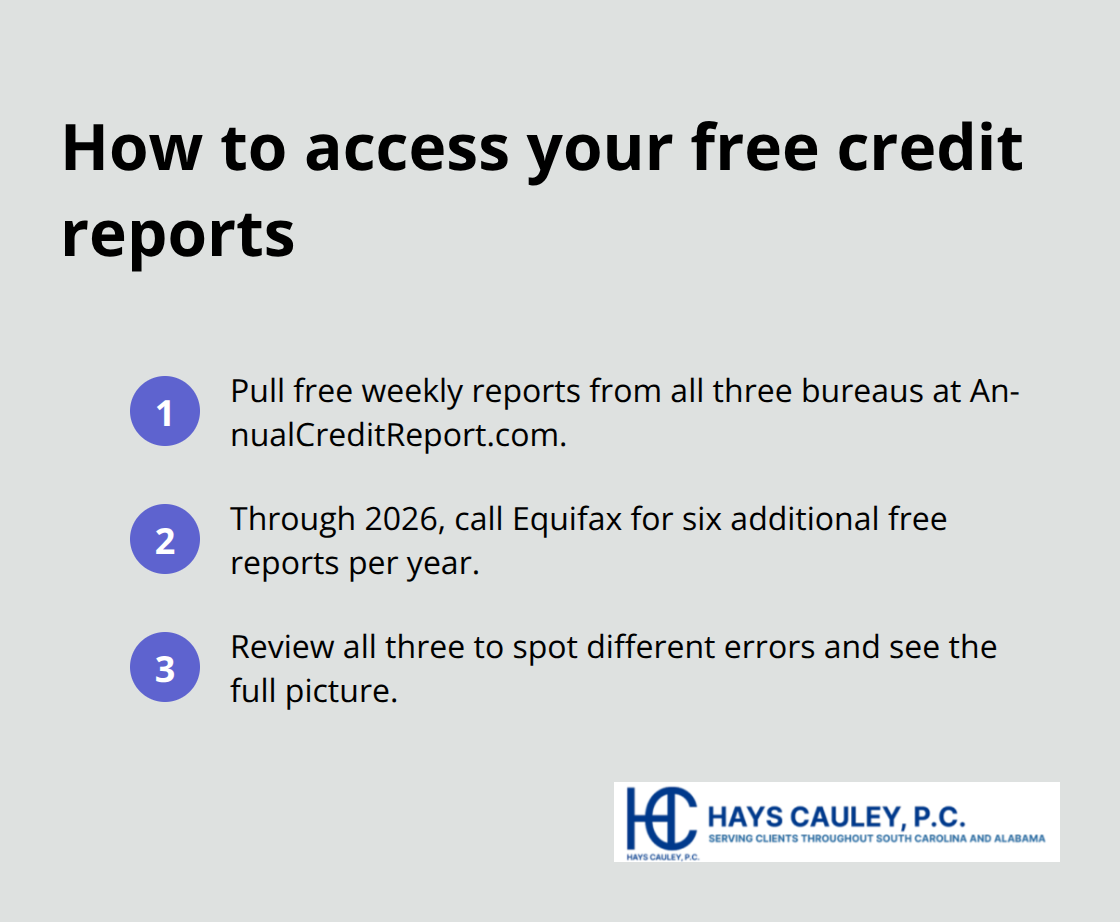

How to Access Your Reports

Start by pulling your free credit reports from all three bureaus at AnnualCreditReport.com, where you can check each report once per week for free. Through 2026, Equifax also offers six additional free reports per year by calling 1-866-349-5191. Each report may reveal different errors, so reviewing all three gives you the complete picture lenders see.

Understanding Your Credit Score

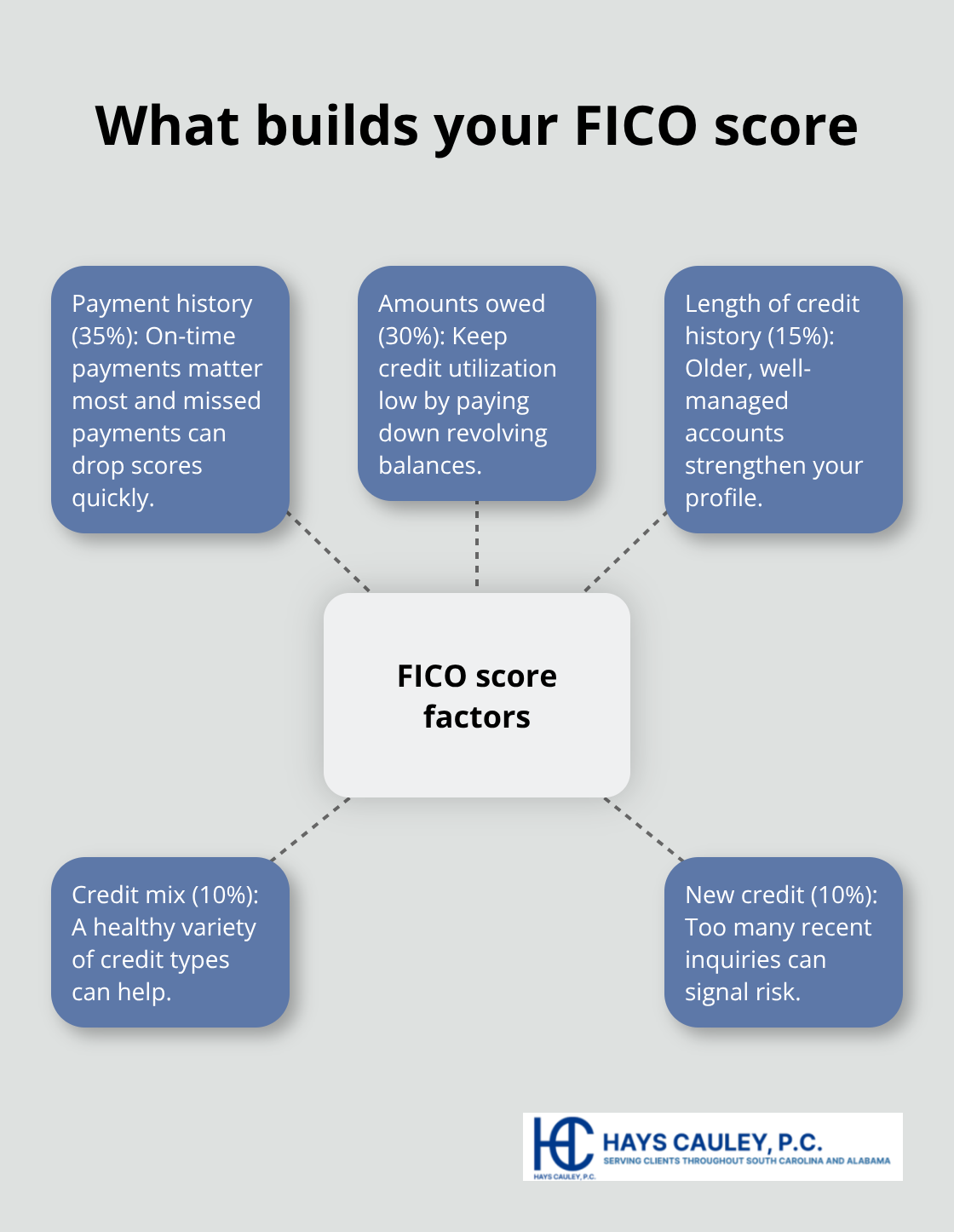

Your credit score ranges from 300 to 850 and is built from five factors: payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%). Lenders use this three-digit number to assess risk, and a lower score means higher interest rates or loan denials. About 44.3% of South Carolinians have scores below 700, indicating substantial room for improvement through error correction and intentional rebuilding.

Spotting and Documenting Errors

When you review your reports, look for accounts you don’t recognize, payment statuses that don’t match your records, duplicate listings, and inflated balances. Write down each error with specific details: the creditor name, account number, what’s wrong, and why. Under the Fair Credit Reporting Act, you can dispute inaccuracies with the credit bureau in writing or by phone-Experian at 888-397-3742, TransUnion at 800-916-8800, and Equifax at 866-349-5191. Send written disputes by certified mail with return receipt to create a paper trail. Include copies of supporting documents (bank statements, payment receipts) that prove the error. The bureau must investigate within 30 days and provide written results. If the investigation finds the information inaccurate, the furnisher must notify all three bureaus to correct the file. Check your reports again three months after filing disputes to confirm removals took effect. Once you identify and challenge these errors, you’ll move toward the next critical phase: taking active steps to rebuild your credit through strategic debt reduction and consistent on-time payments.

How to Fix Errors, Reduce Debt, and Handle Collections Serving South Carolina, including Greenville, Columbia and Charleston

File Disputes the Right Way

Disputing errors on your credit report is the fastest way to improve your score, but it only works if you follow the process correctly. Send your dispute by certified mail with return receipt requested, and include copies of supporting documents that prove the error-bank statements, payment receipts, or correspondence with the creditor. The FTC provides sample dispute letters on its website to guide your writing. After you file a dispute with a credit bureau, the agency has 30 days to investigate and respond in writing. If the bureau finds the information inaccurate, the furnisher must notify all three bureaus to correct it.

Contact the creditor or collection agency directly in writing and dispute the item there as well. Under the Fair Credit Reporting Act, if the furnisher continues reporting disputed information after receiving notice of your dispute, they must tell the bureaus, which then must investigate again. This dual approach increases pressure on both parties to correct errors. After the investigation closes, pull your reports again within 60 days to confirm the inaccurate information was removed.

Escalate When Bureaus Resist

If a bureau ignores your dispute or refuses to correct clear errors, South Carolina law allows you to pursue damages up to $1,000 per day plus attorney fees through civil action. Documentation matters here-keep copies of all dispute letters, certified mail receipts, and bureau responses to build your case. When bureaus resist correction despite clear evidence, professional guidance can help navigate the process and pressure both the bureaus and creditors to act.

Lower Your Debt and Build Payment History

Your credit utilization ratio-the amount you owe divided by your total credit limits-makes up 30% of your score, so paying down balances produces immediate results. Focus first on high-balance credit cards to lower your reported utilization to around 30% or below. The average South Carolina resident carries about $5,700 in debt on their credit report, and inflated balances from errors make this worse.

Set up automatic payments for all accounts to eliminate the risk of late payments, which damage your score far more than any other factor. Payment history accounts for 35% of your score, so even one missed payment can drop it by 50 to 100 points depending on how recent it is.

Negotiate Collections and Charge-Offs

If you have collection accounts or charge-offs, negotiate a settlement in writing if possible. Demand that the creditor or collector agree in writing to remove the item from your report upon payment, though many will only agree to mark it as paid in full rather than removed. A paid collection still hurts less than an unpaid one, and the age of the item matters-negative information stays on your report for seven years, so older items have less weight.

If a collector refuses reasonable settlement terms or continues illegal practices, file a complaint with the Consumer Financial Protection Bureau or the South Carolina Department of Consumer Affairs. Once you’ve addressed errors and begun rebuilding through consistent payments and debt reduction, you’ll see measurable score improvement within three to six months. The next step involves avoiding the traps that derail many people’s credit repair efforts.

What Derails Credit Repair Efforts Serving South Carolina, including Greenville, Columbia and Charleston

Credit Repair Scams Cost Real Money

Credit repair scams cost Americans millions annually, and South Carolina residents are frequent targets. The FTC reported more than $7.9 billion in losses to investment and credit-related scams in 2025, with a median individual loss exceeding $10,000. These operations promise rapid score increases or guaranteed removal of negative items, then demand upfront fees before delivering anything. Under the Credit Repair Organizations Act, credit repair companies cannot legally charge fees before delivering results, yet many ignore this rule entirely.

If a service demands payment upfront or guarantees item removal regardless of accuracy, it’s a scam. Legitimate credit repair involves disputing errors yourself at no cost through the bureaus or working with a consumer protection law firm that operates on contingency or reasonable fees tied to actual results.

Keeping Old Accounts Open Protects Your Score

Many people close old credit accounts after paying them down, which is a costly mistake. Your credit history length accounts for 15% of your score, and closing accounts shortens that history and reduces your total available credit, which raises your utilization ratio instantly. If you paid off a card, keep it open with zero balance and occasional small purchases to maintain active status.

The only exception is if the account carries annual fees that outweigh the benefit. Even then, request a downgrade to a no-fee version first before closing the account. Older accounts with positive payment history carry significant weight in your score calculation, so preserve them whenever possible.

Monitor Your Reports Regularly to Catch Errors

Ignoring your credit report entirely guarantees that errors persist and damage your score indefinitely. Many South Carolinians assume their reports are accurate or believe checking them will hurt their score, which is false. Soft inquiries from checking your own reports cause no damage whatsoever.

The reality is that 79% of South Carolina credit reports contain errors according to Credit Repair Cloud’s analysis, meaning odds are high that your report contains mistakes costing you points. You must pull reports at least annually from all three bureaus at AnnualCreditReport.com and review them line by line. Set a calendar reminder to check every three months during active repair so you catch new fraudulent accounts or reporting errors before they age and become harder to remove.

Passive monitoring catches identity theft early, prevents score damage, and gives you documentation for disputes.

Final Thoughts

Credit repair takes time, but the process is straightforward once you understand what to do. Your South Carolina credit fix begins with pulling your reports, identifying errors, and filing disputes-all steps you can take yourself at no cost. Most people see measurable score improvement within three to six months of consistent effort, especially when they combine dispute work with strategic debt reduction and flawless payment history.

Create a realistic timeline based on your situation. If you have multiple errors to dispute, expect the investigation process to take 30 days per bureau, plus additional time if you need to escalate resistant bureaus. If you’re rebuilding after collections or charge-offs, plan for 12 to 24 months of on-time payments to demonstrate reliability to lenders. Track your progress by pulling updated reports every three months and noting score changes.

Many South Carolinians benefit from professional guidance when disputes stall, bureaus resist correction, or the process feels overwhelming. We at Hays Cauley, P.C. help consumers with credit reporting, identity theft, and debt-related issues across South Carolina, including Greenville, Columbia and Charleston. If you’ve filed disputes and encountered resistance, or if errors are costing you real money on loans and interest rates, reaching out for support makes sense.