Dispute credit report quickly: Quick, Effective Steps to Challenge Errors

A credit report error can tank your score and cost you thousands in higher interest rates. The good news: you can dispute credit report errors quickly and effectively with the right steps.

At Hays Cauley, P.C., we’ve helped countless South Carolina residents challenge inaccuracies and reclaim their financial standing. This guide walks you through the entire process, from spotting mistakes to getting them removed.

Finding Errors on Your Credit Report

Start by obtaining your actual credit report from all three bureaus. The FTC has made free weekly checks available at annualcreditreport.com, and Equifax offers six free reports annually through 2026 by calling 1-866-349-5191. Don’t rely on credit score alone-your score tells you nothing about what’s actually written on your report. When you pull your report, print it out and read every single line. Look for accounts you don’t recognize, duplicate listings of the same debt, incorrect payment histories, wrong balances, outdated negative items, and personal information errors like misspelled names or old addresses.

Inaccurate negative information can legally remain on your report for seven years, while bankruptcy stays for ten years, so catching errors immediately matters. Common mistakes include payments marked late when you paid on time, accounts appearing multiple times under different creditor names or acronyms, balances that don’t match your actual debt, and accounts that belong to someone else entirely due to identity theft or data entry mistakes.

Spot Late Payments That Never Happened

Most people skip this step and miss obvious errors. Check if any late payments appear on accounts where you never missed a payment-this happens constantly when creditors misapply payments or when disputes weren’t properly recorded. Look at the account status and opening dates. If an account shows as open when you closed it years ago, or if it appears with multiple opening dates, that’s a data quality issue the bureau must fix.

Identify Duplicate Accounts and Name Variations

Examine creditor names carefully since TransUnion, Experian, or Equifax might list the same creditor under different names or abbreviations, making it harder to spot duplicates. If the same debt appears twice under slightly different names, that’s a major error affecting your score. Verify the current balance matches your last statement-errors here directly impact your credit utilization ratio and your score.

Catch Accounts You Never Opened

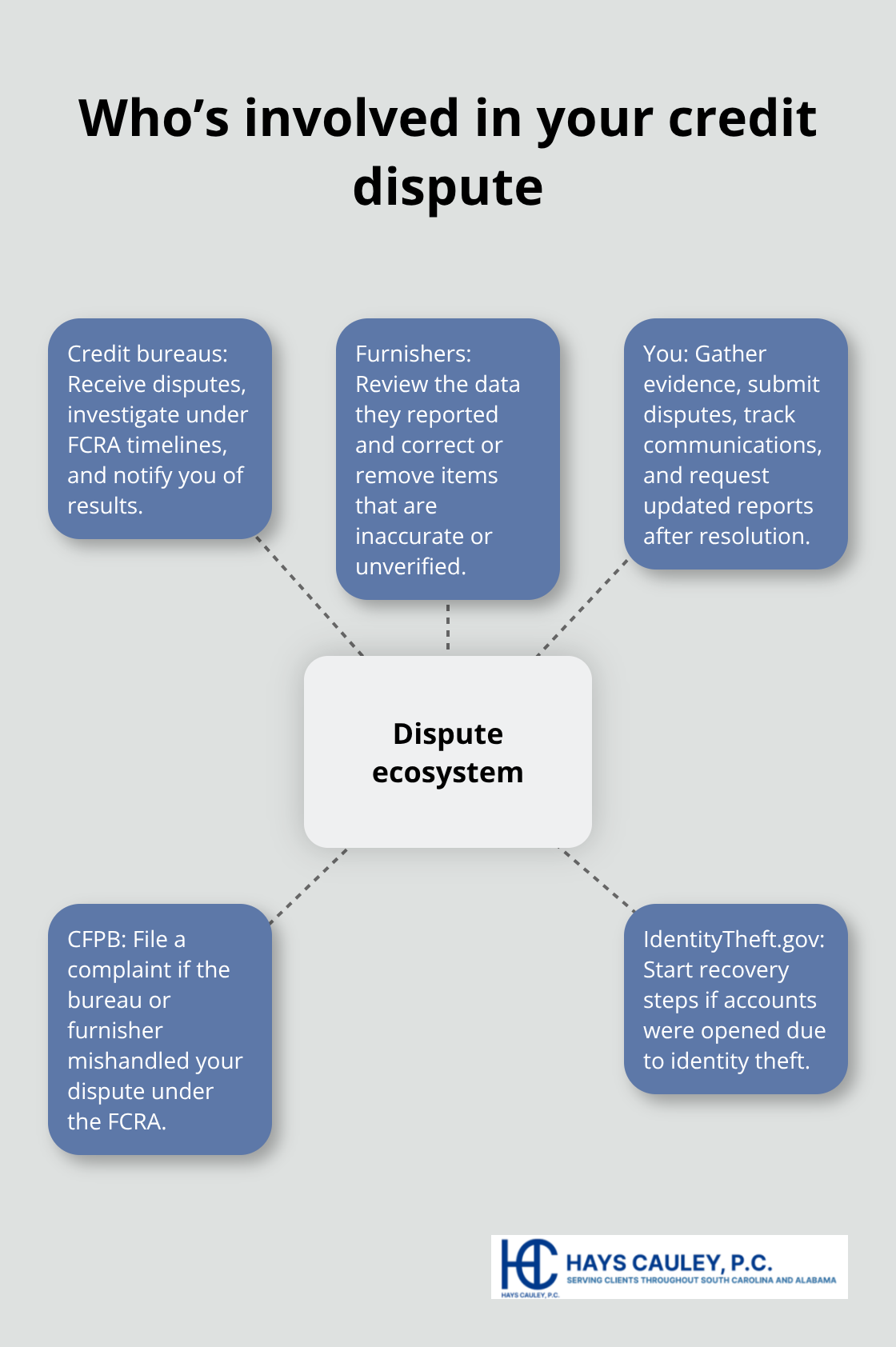

Check for accounts you genuinely didn’t open. Identity theft is real, and the FTC reports that theft victims should report it at IdentityTheft.gov to receive a personalized recovery plan. Gather copies of your statements, payment records, and any correspondence about disputed accounts (these documents become your evidence when you challenge inaccurate information with the credit bureaus). The sooner you spot unauthorized accounts, the faster you can stop the damage and move forward with your dispute.

How to File Your Dispute and Get Results: Serving South Carolina, including Greenville, Columbia and Charleston

Contact the Right Credit Bureau First

Start your dispute directly with the credit bureau that’s reporting the error, not with the creditor first. Contact Equifax at 1-866-349-5191, Experian at 1-888-397-3742, or TransUnion at 1-800-916-8800 to initiate your dispute online, by phone, or through certified mail. The Fair Credit Reporting Act gives these bureaus 30 days to investigate your claim, though submitting additional documents can extend this to 45 days.

Prepare Your Written Dispute with Supporting Documents

Send your dispute in writing using certified mail with return receipt requested-this creates proof the bureau received it, which matters if you need to escalate later. Include your full name, address, phone number, the account number you’re disputing, and a clear explanation of what’s wrong and why. Attach copies (never originals) of documents that support your position: statements, payment records, canceled checks, letters from creditors, or receipts. Circle or highlight the disputed items on your credit report copy so the bureau can’t miss what you’re challenging.

Understand the Investigation Timeline

The bureau must forward your dispute and all evidence to the furnisher (the creditor or company that reported the information) within five days of receiving it. The furnisher then has 30 days to investigate and respond. If they find the information is inaccurate or can’t verify it, they must notify all three bureaus to correct or remove it.

If the furnisher confirms the information is accurate, the bureau will notify you that your dispute was unsuccessful.

Simple identifying errors like a misspelled name or wrong address can appear corrected in about one week without requiring furnisher verification. Payment history disputes take closer to the full 30 days since the furnisher must verify the information.

Track Your Dispute and Handle Multiple Bureaus

Keep copies of every letter, email, and note from phone calls-this documentation becomes critical if you need to re-dispute or file a complaint with the Consumer Financial Protection Bureau. Don’t assume one dispute fixes everything across all three bureaus; if the same error appears on multiple reports, file separate disputes with each bureau. After the investigation concludes, request an updated credit report to confirm the correction was made.

Move Forward If Results Disappoint

If you’re not satisfied with the outcome, you can re-file with new evidence or add a statement of dispute to your file explaining your position to future creditors reviewing your report. This next step matters because some errors require additional pressure or documentation to resolve, and knowing your options helps you decide whether to pursue further action or seek additional support.

What Happens After You File a Dispute

Once your dispute lands with the credit bureau, a specific sequence unfolds over the next 30 to 45 days. The bureau must forward your dispute and supporting documents to the furnisher within five business days, and the furnisher then has 30 days to investigate your claim. If you submitted additional documents with your dispute, the investigation window extends to 45 days maximum. During this period, the furnisher checks whether the information on your report is accurate and verifiable. If they find the information is wrong or cannot verify it, they must notify all three bureaus immediately to update or remove it from your file. If they confirm the information is accurate, the bureau sends you a letter explaining why your dispute failed.

Timeline for Simple Errors vs. Complex Disputes

Simple errors like a misspelled name or incorrect address resolve in about one week without requiring furnisher verification. Payment history disputes almost always consume the full 30-day window since creditors must pull records and confirm dates and amounts. The furnisher’s response speed directly affects when you see results on your credit report.

Verify the Correction Actually Happened

After the investigation closes, pull your credit report again from the bureau that had the error to confirm the correction actually happened. Many people skip this step and assume the fix was applied, only to discover months later that nothing changed. If the disputed information was removed or corrected, the bureaus must send you a free updated copy of your report, separate from your annual free report.

What to Do If Your Dispute Failed

If you’re unhappy with the outcome, you have two realistic paths forward: re-dispute with additional documentation that strengthens your case, or file a complaint with the Consumer Financial Protection Bureau if you believe the bureau or furnisher mishandled your dispute. The CFPB takes these complaints seriously and investigates violations of the Fair Credit Reporting Act. If you discover during your monitoring that an inaccuracy still appears on your report after the investigation concluded, contact the furnisher directly and ask them to correct it again, then follow up with the bureau to confirm the update.

How Corrections Impact Your Credit Score

Corrected information can meaningfully improve your credit score within 30 to 45 days, potentially qualifying you for better loan terms and lower interest rates on future applications. The impact depends on what was removed-eliminating a late payment or duplicate account typically produces faster score recovery than removing a collection account. Your credit utilization ratio also improves if the correction involved an inflated balance (this change can boost your score significantly within weeks).

Final Thoughts

Disputing credit report errors quickly stops inaccuracies from damaging your financial future. The process itself is straightforward: pull your reports, identify the mistakes, file disputes with the bureaus, then monitor the results. Most corrections happen within 30 days, and simple errors like name or address mistakes resolve even faster.

Speed matters because credit bureaus must investigate within 30 days, furnishers must respond within that window, and corrections take another 30 days to appear on your updated report. That means you could see results in as little as 60 days if you file promptly and include solid documentation. Waiting weeks to gather documents or delaying your dispute extends the timeline unnecessarily, so act the moment you spot an error on your report.

We at Hays Cauley, P.C. understand how frustrating credit reporting errors can be, and we’re here to help South Carolina residents (including those in Greenville, Columbia, and Charleston) challenge inaccuracies and protect their financial rights. If you’ve filed disputes and hit roadblocks, or if you’re facing identity theft or complex credit issues, contact us to discuss your situation.