Disputing credit report errors: What You Need to Know

Your credit report shapes your financial life, yet errors on it are surprisingly common. Inaccurate information can tank your credit score and cost you thousands in higher interest rates.

Disputing credit report errors is your legal right, and we at Hays Cauley, P.C. want you to understand exactly how to do it. This guide walks you through the process, your protections under federal law, and when to seek help.

What Errors Actually Appear on Credit Reports

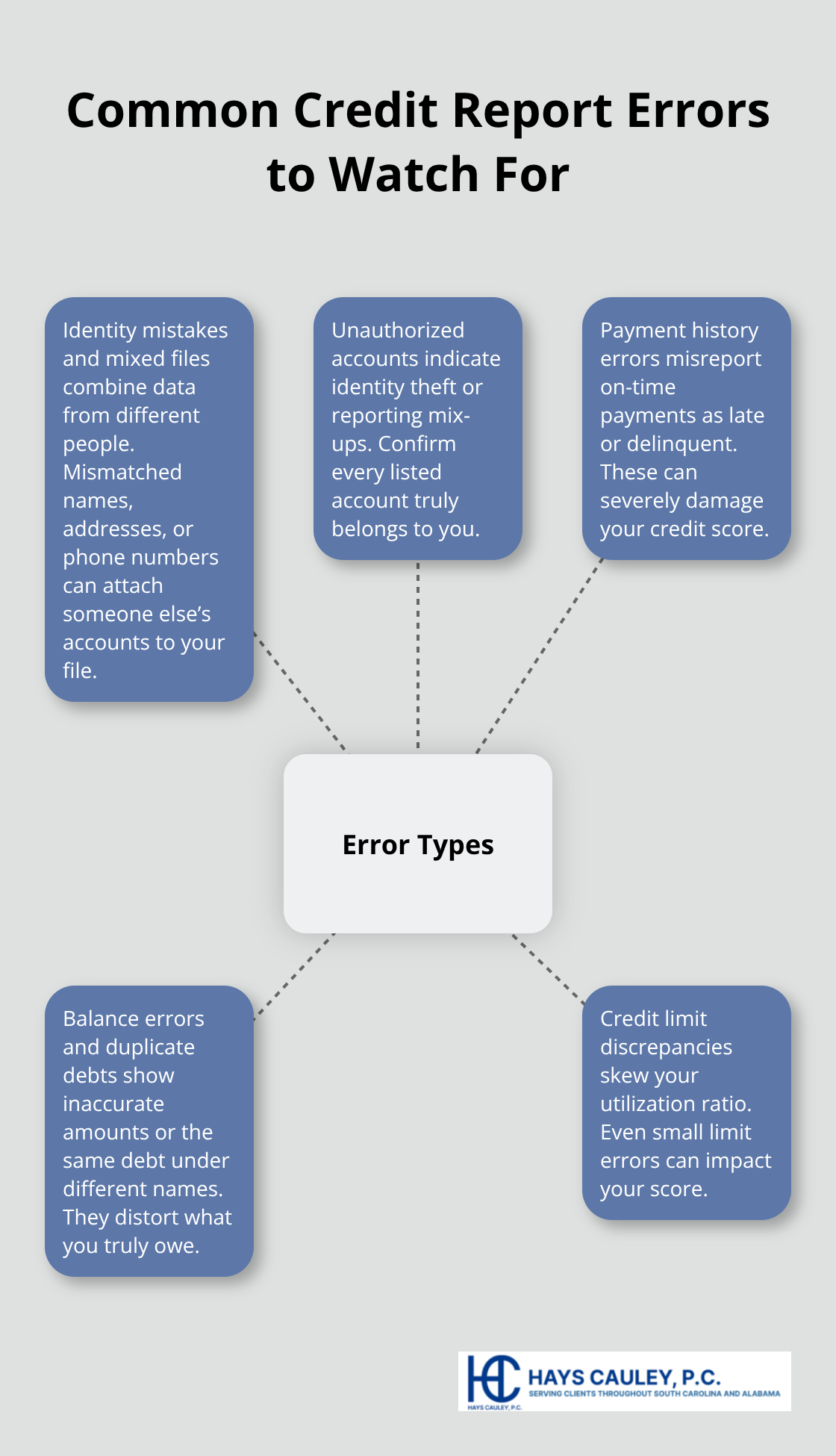

Identity Mistakes and Mixed Files

Identity mistakes top the list of credit report problems, and they’re often easier to spot than you’d think. Wrong names, phone numbers, or addresses get mixed into files regularly-sometimes because creditors mistype information, sometimes because two people share similar names. The Consumer Financial Protection Bureau found that mixed files occur when accounts from two consumers are combined in one file due to similar names, and this problem affects more people than most realize. Check your report carefully for any personal details that don’t match your records, especially if you’ve moved recently or share a common name.

Unauthorized accounts represent the second major error category, and these demand immediate action. If accounts appear on your report that you never opened, this signals either identity theft or a reporting mistake. Verify every account listed is actually yours-don’t assume anything. Look at the account holder status too, since being listed as an authorized user sometimes gets reported incorrectly as the primary account owner, which damages your credit unnecessarily.

Payment History and Account Status Errors

Payment history errors hit hardest because they directly tank your credit score. Accounts reported as late or delinquent when you paid on time happen more often than creditors admit, and they can lower your score by 100 points or more. Examine the dates carefully-when the account opened, when you made your last payment, and when any delinquency supposedly started. Check account status too; closed accounts sometimes get reported as open, which inflates your available credit and confuses lenders about your actual financial situation.

Balance and Credit Limit Discrepancies

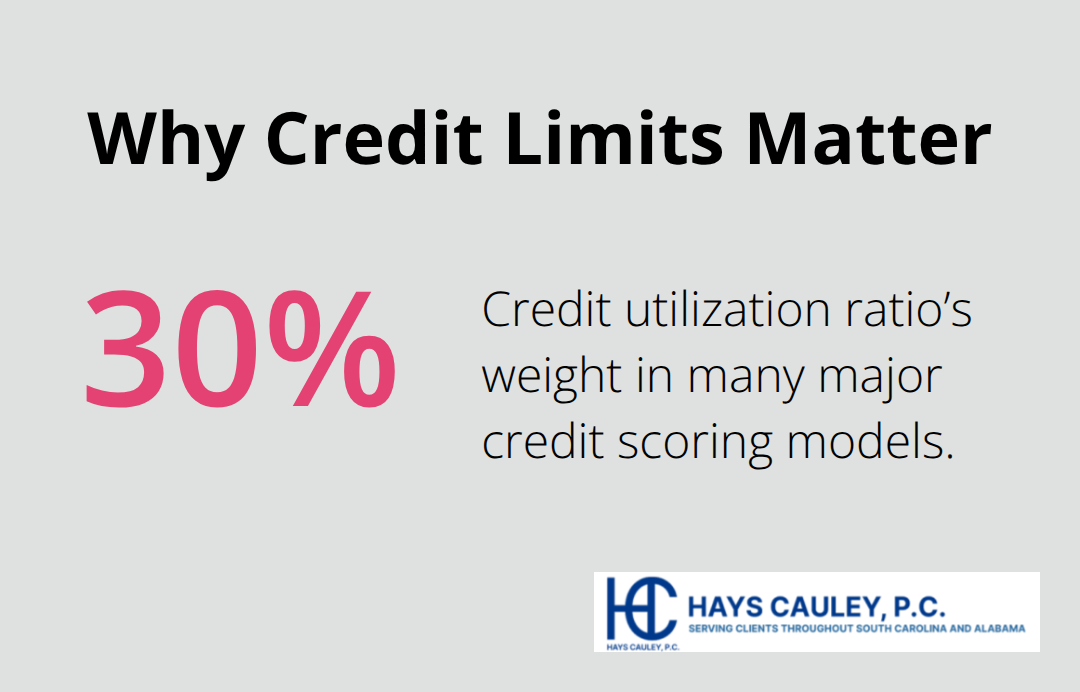

Balance errors also matter-your reported balance should match what you actually owe right now, not an old statement amount. The same debt appearing twice under different names or creditors is another red flag that requires investigation. Credit limit discrepancies might seem minor, but they affect your credit utilization ratio, which accounts for 30 percent of your credit score according to major scoring models.

Taking Action Against Errors

Once you spot an error, contact both the credit reporting company and the business that supplied the information to them. This dual approach works because each party has different responsibilities and timelines. The furnisher bank, creditor, or lender that reported the information-must investigate within 30 days and notify all three bureaus if they find the information wrong. Understanding these error types positions you to move forward with the dispute process, which we’ll cover in the next section.

How to Dispute Your Credit Report Errors: Serving South Carolina, Including Greenville, Columbia and Charleston

Gather Your Reports and Document the Errors

Visit annualcreditreport.com to obtain your free credit reports from Experian, Equifax, and TransUnion once every 12 months at no cost. Through 2026, Equifax offers six free reports per year if you visit their site or call 1-866-349-5191, which gives you more frequent monitoring windows. Print or save each report and circle or highlight the errors you identified in the previous section. Write down the account numbers, dates, and specific details about what’s wrong-vague disputes get ignored or rejected as frivolous. The Consumer Financial Protection Bureau allows credit reporting companies to dismiss disputes they reasonably determine are frivolous, but you won’t face this problem if you provide detailed, specific information about each error.

File Disputes with All Three Credit Reporting Companies

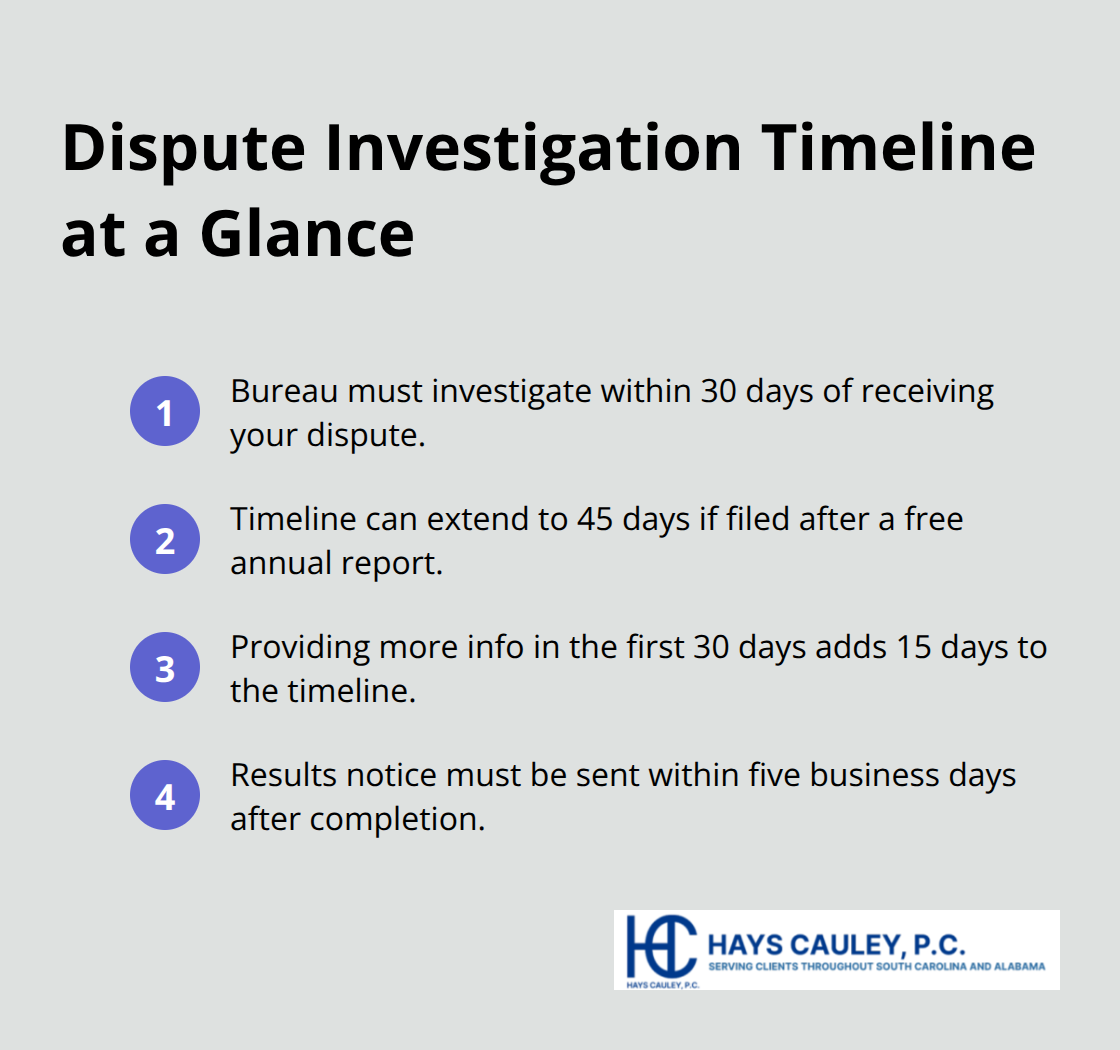

Send your dispute to all three bureaus that are reporting the error, not just one. Experian accepts disputes at 888-397-3742, TransUnion at 800-916-8800, and Equifax at 866-349-5191, but mailing by certified mail with return receipt proves you sent the dispute and when they received it. Include your full name, address, phone number, the confirmation number from your credit report (if available), each account number with the error, a clear explanation of why you’re disputing, copies of supporting documents, and a request to remove or correct the item. The credit reporting company must investigate within 30 days of receiving your dispute, though the timeline extends to 45 days if you file after obtaining your free annual report. If you submit additional relevant information during those initial 30 days, they get another 15 days to complete the investigation. They must notify you of the results within five business days after finishing, and the updated credit report they send you is free and doesn’t count toward your annual free report.

Contact the Furnisher Directly

Contact the furnisher bank, creditor, or lender that provided the information-at the same time you dispute with the bureaus. Send a certified letter to the furnisher’s address listed on your report or their dispute department address, explaining what information is wrong and why. Furnishers have 30 days to investigate and respond to your dispute, and if they find the information is inaccurate or can’t verify it, they must update or remove it and notify all three credit reporting companies. If the furnisher determines the information is accurate but you still disagree, you can request that the credit reporting companies include a disputed-item statement in your reports going forward.

Maintain Detailed Records Throughout the Process

Keep copies of every letter you send, every document you attach, and every response you receive-this paper trail protects you if the dispute stalls or if you need to escalate the matter. If a business continues reporting information you’ve disputed, it must inform the credit bureau, which must include a notice that you’re disputing the item on your reports. Monitor your credit reports after the investigation concludes to confirm the disputed information was removed or updated, and verify that the dispute notation appears on any reports still showing the item. The dispute process takes time, but persistence pays off when errors disappear from your file. If disputes with the bureaus and furnishers don’t resolve your situation, federal law provides additional protections and remedies that we’ll examine in the next section.

Your Rights Under the Fair Credit Reporting Act

Access Your Credit Reports for Free

The Fair Credit Reporting Act gives you concrete legal protections that transform how you handle errors on your credit report. Federal law entitles you to free access to your credit reports from all three bureaus once every 12 months through annualcreditreport.com, and through 2026, Equifax provides six additional free reports annually. Pull your reports every few months to catch errors early, since the longer inaccurate information sits on your file, the more damage it inflicts on your credit score and borrowing power.

Dispute Inaccurate Information at No Cost

You have the absolute right to dispute any information you believe is inaccurate or incomplete, and the credit reporting company must investigate your dispute within 30 days (or 45 days in certain circumstances) at no cost to you. The furnisher who provided the incorrect information must also investigate within 30 days, and if they find the information wrong or cannot verify it, they are legally required to notify all three credit bureaus so your file gets corrected everywhere simultaneously. If you suspect identity theft has caused errors on your report, visit IdentityTheft.gov immediately-this federal resource provides a personalized recovery plan and one-stop reporting that coordinates with law enforcement and credit bureaus.

Receive Notice of Adverse Actions

You have the right to receive notice whenever a creditor or lender takes adverse action against you based on information in your credit report. Companies must tell you why they denied your application, increased your interest rate, or reduced your credit limit. This notification requirement gives you the opportunity to dispute errors before they cost you money on a mortgage, car loan, or credit card.

File Complaints When Companies Violate Your Rights

If a dispute does not resolve your situation and you believe a credit reporting company or furnisher violated your rights, you can file a complaint with the Consumer Financial Protection Bureau, which investigates and forces companies to respond. The CFPB forwards your complaint to the company, provides you a tracking number, and keeps you updated throughout the process-this agency has real enforcement power and companies take complaints seriously. If errors persist despite your efforts or if you face ongoing problems with credit reporting accuracy, Hays Cauley, P.C. helps consumers navigate these situations and hold companies accountable when they violate your federal rights.

Final Thoughts

Credit report errors damage your financial future, but you now control the power to fight back. The most common mistakes-identity theft, mixed files, payment history errors, and balance discrepancies-follow predictable patterns that you can spot by reviewing your reports regularly. Disputing credit report errors works when you gather documentation, contact both the credit reporting companies and furnishers, and maintain detailed records throughout the process.

Monitoring your credit report every few months catches errors before they tank your score or cost you thousands in higher interest rates. Pull your free reports from annualcreditreport.com quarterly, and through 2026, grab those extra Equifax reports to stay ahead of problems. If you spot identity theft signals, act immediately through IdentityTheft.gov to minimize damage and coordinate recovery across all three bureaus.

Some disputes resolve quickly when furnishers acknowledge mistakes and update their records, while others drag on when companies resist correction or claim information is accurate despite your evidence. If you’ve disputed errors and faced resistance, or if identity theft has complicated your situation beyond standard dispute procedures, Hays Cauley, P.C. helps consumers navigate credit reporting violations and holds companies accountable when they ignore your federal rights. We serve South Carolina, including Greenville, Columbia, and Charleston, and we understand how frustrating these battles become when you fight alone.