Dispute Credit Report a Practical Guide To Correcting Your Credit Records

A mistake on your credit report can cost you thousands in higher interest rates and rejected loan applications. Inaccurate information stays on your record for years unless you take action to dispute it.

We at Hays Cauley, P.C. help South Carolina residents challenge these errors and reclaim their financial standing. This guide walks you through the entire process, from identifying problems to holding credit bureaus accountable.

Understanding Credit Report Errors and Their Impact

Types of Common Errors Found on Credit Reports

Credit reports contain far more than just your payment history. The three national bureaus-Equifax, Experian, and TransUnion-compile detailed records of your accounts, payment patterns, collections activity, and credit inquiries. The most damaging errors fall into specific categories that directly tank your creditworthiness.

Identity theft creates accounts in your name that you never opened. Mixed credit files happen when your information gets tangled with someone else’s, pulling their negative history into your report. Outdated account statuses remain marked as active or delinquent long after you’ve paid them off. Duplicate accounts appear when the same debt gets reported twice, artificially inflating how much you owe. Wrong personal details like misspelled names or old addresses seem minor but can trigger loan denials based on mismatched records. These errors are not rare occurrences-they’re systematic problems that affect millions of Americans annually.

How Errors Affect Your Credit Score and Financial Life

The financial consequences of inaccurate information are severe and measurable. A single error can cost you thousands in higher interest rates because lenders see inflated risk. Collections accounts that shouldn’t be there can block you from getting approved for mortgages, auto loans, or even rental housing.

Payment history accounts for 35 percent of your credit score, so a false late payment or charge-off tanks your number substantially. Insurance companies use credit reports too, and errors can result in higher premiums or outright denial of coverage. These consequences compound over time, affecting not just your immediate borrowing power but your long-term financial stability.

Your Legal Right to Dispute Inaccurate Information

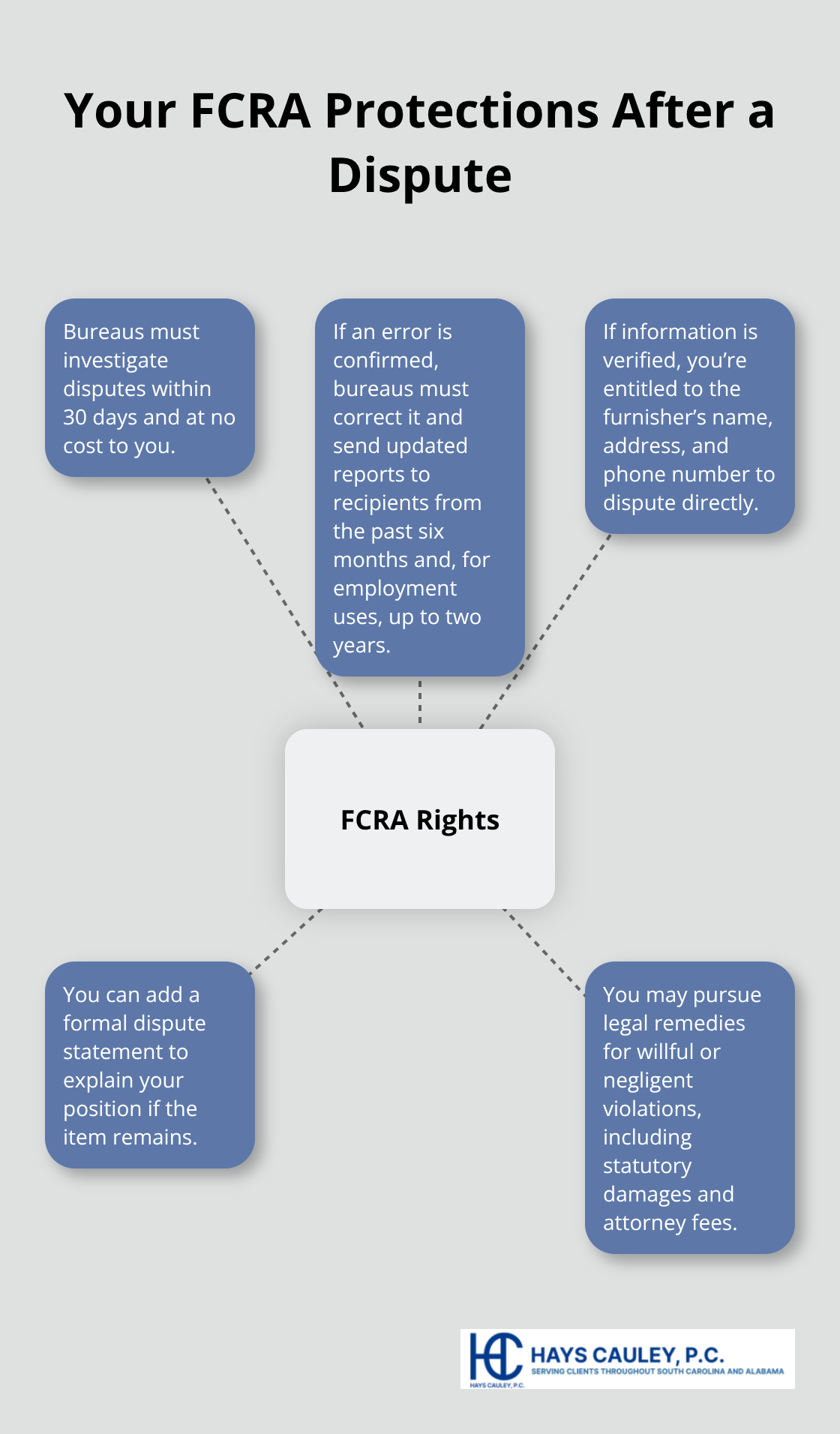

The Fair Credit Reporting Act gives you the explicit right to dispute any information you believe is wrong, and credit bureaus must investigate within 30 days at no cost to you. If they find an error, they must correct it and send updated reports to anyone who received your report in the past six months. This isn’t a favor-it’s your legal protection.

Many people don’t realize they have this power, and inaccurate information sits on their reports unchallenged for years, costing them real money and real opportunities. Understanding what errors look like and knowing your rights to challenge them sets the foundation for taking action. The next step involves obtaining your actual credit report and identifying which mistakes affect your specific situation.

Step-by-Step Process for Disputing Credit Report Errors

Obtain Your Credit Report and Identify Mistakes

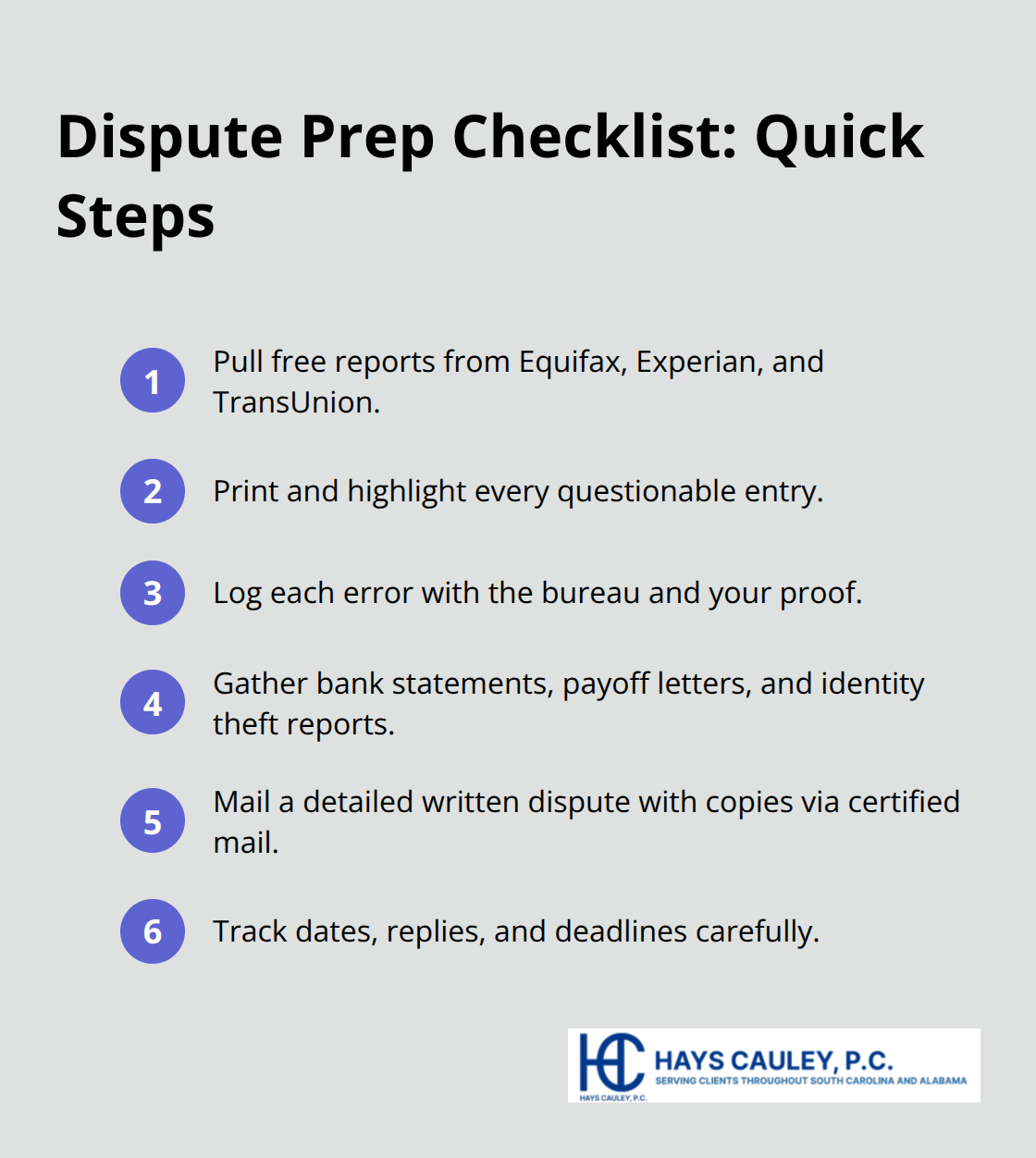

Your actual credit report is the only way to know what errors exist and what needs fixing. Head to annualcreditreport.com, the official source authorized by the Federal Trade Commission, and request free copies from all three bureaus: Equifax, Experian, and TransUnion. You receive one free report per bureau per year, and pulling all three gives you a complete picture since errors often appear on only one or two bureaus.

When your reports arrive, print them out and grab a highlighter. Go through each section methodically and mark anything that looks wrong: accounts you don’t recognize, late payments that weren’t late, collections that were already paid, duplicate entries, or personal information that’s outdated.

Circle every error on a printed copy and create a simple error log in a spreadsheet or document listing each problem, which bureau shows it, and what documents you have that prove it’s wrong. This organized approach prevents you from forgetting items and keeps you from missing filing deadlines.

Gather Evidence and Document Everything

Collect your evidence immediately. If a payment shows as late, pull bank statements showing the on-time deposit. If an account isn’t yours, grab any identity theft report you filed with police. If a collection was paid, locate the payoff letter. Store copies of everything because originals never go in the mail to credit bureaus-you need to keep your originals safe and send only duplicates.

File Your Dispute in Writing

Start your dispute directly with the credit bureau that’s reporting the error rather than using their online systems. The Federal Trade Commission confirms that written disputes create a paper trail and work better when you need proof later. Include a cover letter identifying each disputed item by account number, explain briefly why it’s wrong, and request reinvestigation. Attach copies of your supporting documents and keep duplicates for yourself. Send everything certified mail with return receipt requested so you have proof the bureau received it.

Track the Investigation and Follow Up

The credit bureaus typically respond within 30 days with their investigation results. If they find an error, they must correct it and send updated reports to anyone who received your report in the past six months. If they received your report for employment purposes within two years, request the corrected version go to those employers as well.

Don’t stop there if the bureau says the information was verified as accurate but you still believe it’s wrong. Contact the creditor or furnisher directly in writing and send the same evidence you sent the bureau. Sometimes creditors have outdated records on their end, and fixing the source forces the bureau to update it. Save every piece of correspondence, confirmation number, and result letter. Track dates and deadlines so nothing falls through the cracks. This methodical, documented approach gives you leverage if you need to escalate the dispute further or pursue legal remedies-which brings us to what happens next when the bureaus complete their investigation.

What Happens After You File a Dispute

The 30-day investigation window that credit bureaus must follow under the Fair Credit Reporting Act does not guarantee quick resolution. After you submit your dispute, the bureau contacts the furnisher entity that originally reported the information-and requests verification. The furnisher then has a limited time to respond, though the exact timeline varies. If the furnisher fails to respond within a reasonable timeframe, the bureau must remove the item from your report.

This is where patience meets leverage. Many disputes succeed not because the information is clearly wrong, but because furnishers cannot quickly locate their records or fail to respond at all.

Track Your Timeline Carefully

You must track your 30-day deadline with precision. Send your dispute certified mail and note the date it arrives. The bureau’s investigation clock starts when they receive your dispute, not when you mail it. If you do not receive a response within 35 days, follow up immediately with a second written request referencing your original dispute and demanding compliance with federal law. Some bureaus delay their responses hoping you will forget about it. You will not.

Understand Verification and Unverifiable Results

When the bureau completes its investigation, they will tell you whether the information was verified as accurate or removed as unverifiable. If the furnisher verified the information, the bureau must provide you with the furnisher’s name, address, and phone number in writing. This is your cue to dispute directly with the creditor. Many creditors maintain outdated records on their end, and a written dispute sent directly to them can force correction at the source faster than waiting for the bureau to reinvestigate.

Add a Dispute Statement if Needed

If the bureau says the item remains on your report after investigation and you still believe it is wrong, you have the right to add a formal dispute statement to your credit file. This statement appears on future reports and explains your version of events. However, a dispute statement does not remove the error itself.

Pursue Legal Remedies for Documented Harm

If the error causes measurable financial harm, you can pursue legal remedies under the Fair Credit Reporting Act. Willful violations by bureaus or furnishers carry damages of three times actual damages or up to $3,000 per incident, plus attorney fees. Negligent violations carry actual damages or at least $1,000 per incident. If an inaccuracy damages your creditworthiness and remains uncorrected after judgment, damages can escalate to $1,000 per day until removal. A consumer protection law firm can help South Carolina residents pursue these remedies when credit bureaus refuse to correct documented errors. Do not accept a bureau’s final answer if you have clear evidence the information is wrong.

Final Thoughts

Inaccurate information will not disappear on its own, so you must take action to dispute your credit report. Pull your free reports from annualcreditreport.com, identify every error, gather your evidence, and file written disputes with each bureau reporting the mistake. Keep copies of everything and follow up if you do not receive responses within 35 days, because credit bureaus often delay their responses hoping you will abandon the process.

If credit bureaus refuse to correct documented errors after investigation, you have legal remedies available under the Fair Credit Reporting Act (willful violations carry damages of three times actual damages or up to $3,000 per incident, plus attorney fees). We at Hays Cauley, P.C. help South Carolina residents challenge credit reporting violations and hold bureaus accountable when they fail to correct mistakes. Contact our consumer protection law firm serving South Carolina, including Greenville, Columbia and Charleston if you need guidance navigating the dispute process or if errors cause measurable financial harm.

Your credit report directly affects your financial future, and taking deliberate action now protects your borrowing power and prevents years of unnecessary damage. Start today by requesting your reports and identifying what needs fixing.