FCRA Violation Penalties How Violations Impact Your Credit and Rights

Your credit report shapes your financial future, yet many people don’t realize how easily violations of the Fair Credit Reporting Act can damage it. FCRA violation penalties can range from hundreds to thousands of dollars, but the real harm often goes deeper than the fines themselves.

At Hays Cauley, P.C., we help South Carolina residents understand their rights when credit reporting errors occur. This guide walks you through what violations mean for your credit, your wallet, and your legal options.

Understanding the FCRA and Its Real Impact, Serving South Carolina, including Greenville, Columbia and Charleston

The Fair Credit Reporting Act became law in 1970 to regulate how credit bureaus handle your financial information, and it remains the backbone of consumer credit protection today. The FCRA established strict rules that credit reporting agencies must follow when collecting, maintaining, and sharing your credit data. Equifax, Experian, and TransUnion-the three major credit reporting agencies-handle roughly 200 million consumer credit files in the United States. These agencies sell your information to lenders, employers, landlords, and insurers, which is why accuracy matters enormously. When violations occur, they distort your financial reality in ways that cost you thousands of dollars over time. The FTC enforces FCRA violations and has the authority to impose civil penalties up to $2,500 per violation for pattern or practice breaches.

How the FCRA Shields Your Credit Rights

The FCRA gives you concrete protections that many people don’t fully understand. You have the right to access your credit reports for free once every 12 months from each of the three major bureaus through annualcreditreport.com. You also have the right to dispute any inaccurate information on your reports, and when you do, the credit bureaus must investigate your dispute within 30 days and notify you of the results. The FCRA mandates that furnishers — the banks, credit card companies, and lenders that report data to credit bureaus-must conduct reasonable investigations when you dispute information. If they find the information is inaccurate, they must correct it across all three bureaus. The FCRA requires that companies only pull your credit report for permissible purposes, such as lending decisions, employment screening, or insurance underwriting. Unauthorized access to your credit report violates the law directly. The law also protects you from old negative information appearing on your report indefinitely. Chapter 7 bankruptcies must disappear after 10 years, lawsuits and judgments after 7 years, and most other negative items after 7 years as well.

What FCRA Violations Actually Look Like

Violations fall into several categories that harm consumers regularly. Furnishers report old information in violation of the FCRA-for example, reporting a Chapter 7 bankruptcy after 10 years have passed or a settled debt as still unpaid. Inaccurate reporting includes listing wrong balances, showing you as the primary debtor when you were only an authorized user, or reporting accounts that don’t belong to you. Mixed files occur when credit bureaus merge your information with someone else’s due to similar names or Social Security numbers, creating a tangled mess of false accounts and debts. Identity theft violations happen when bureaus fail to properly handle or correct information related to fraudulent accounts opened in your name. Failure to investigate disputes properly also violates the FCRA-when you dispute an item and the bureau ignores it or conducts only a cursory review instead of a reasonable investigation. Additionally, improper disclosure violations occur when credit bureaus or furnishers release your report to people without a permissible purpose (such as an employer pulling your credit before making a job offer without your consent or a debt collector accessing your report without authorization).

How Violations Damage Your Credit Score and Finances

Inaccurate negative items on your credit report tank your credit score immediately. A single late payment can drop your score by 100 points or more, depending on your current score and credit history. When furnishers report old information or inaccurate balances, lenders see a distorted picture of your financial responsibility. This distortion leads to higher interest rates on mortgages, auto loans, and credit cards-costs that compound over years. A borrower with a 620 credit score might pay 2% more in interest on a 30-year mortgage than someone with a 760 score, translating to tens of thousands of dollars in additional payments. Beyond credit costs, inaccurate reports affect employment and housing decisions. Landlords and employers pull credit reports to assess reliability, and false information can cost you a job or apartment. Identity theft violations create the worst scenario-fraudulent accounts appear on your report, damaging your score while you fight to prove the accounts aren’t yours.

Taking Action Against Violations

When you discover violations on your credit report, the dispute process is your first line of defense. Contact the credit bureau in writing and clearly explain what information is inaccurate, including copies of supporting documents. Send your dispute via certified mail with return receipt requested to create a paper trail. The bureau must investigate within 30 days and respond to you with results. If the bureau finds the information inaccurate, it must correct your report and notify all three major bureaus of the correction. If you believe a violation has caused you financial harm, you have the right to pursue legal remedies. Willful FCRA violations can result in statutory damages ranging from $100 to $1,000 per violation, plus actual damages, punitive damages, and attorney’s fees. Understanding these rights positions you to hold credit bureaus and furnishers accountable for their mistakes.

How FCRA Violations Tank Your Credit Score and Finances

The Immediate Impact on Your Credit Score

A single inaccurate negative item on your credit report can drop your score by 100 points or more, depending on your current score and credit history. When furnishers report old information or wrong balances, lenders see a distorted financial picture that costs you real money. A borrower with a 620 credit score pays approximately 2% more in interest on a 30-year mortgage than someone with a 760 score, translating to tens of thousands of dollars in additional payments over the loan’s life. This damage compounds across every form of credit you access.

Credit card companies charge higher interest rates to people with lower scores, auto lenders require larger down payments, and insurance companies sometimes deny coverage entirely based on credit reports. The financial bleeding doesn’t stop at lending decisions either. Landlords and employers pull credit reports to assess reliability, and inaccurate negative information can cost you an apartment or job opportunity.

Identity Theft and Mixed Files Create the Worst Damage

Identity theft violations inflict the most severe harm because fraudulent accounts appear on your report while you fight to prove they aren’t yours, destroying your score while someone else uses your stolen identity. Mixed files and duplicate accounts, where credit bureaus merge your information with someone else’s due to similar names or Social Security numbers, create a tangled mess that takes months to unravel through the dispute process.

During this period, you face denial of credit, higher rates on approved applications, and rejection for housing and employment. The cost of inaction is measurable and severe.

The Long-Term Financial and Emotional Toll

A late payment stays on your credit report for seven years, and during that time, lenders view you as higher-risk with every application you submit. Settled debts reported as unpaid or accounts showing wrong balances continue harming your creditworthiness indefinitely until you dispute and correct them. Someone fighting an FCRA violation spends dozens of hours writing dispute letters, gathering documentation, and following up with credit bureaus and furnishers. They spend money on certified mail, credit monitoring services, and potentially legal representation.

The financial and emotional toll of credit damage from violations makes holding violators accountable through legal action not just reasonable but necessary. When violations persist despite your efforts to correct them, understanding your legal remedies becomes the next critical step in protecting your financial future.

What You Can Actually Recover When FCRA Violations Happen

The dispute process gives you immediate power to correct inaccurate information, but understanding exactly what you can recover in damages separates those who accept violations from those who fight back. When you file a dispute with a credit bureau, that agency must conduct a reasonable investigation within 30 days and notify you of the results according to 15 U.S.C. § 1681i. The FTC defines reasonable investigation as more than a cursory check-the bureau must contact the furnisher, review your supporting documents, and verify the accuracy of the reported information. If the furnisher fails to respond or cannot verify the information, the credit bureau must remove it from your report. This happens thousands of times monthly, yet most consumers don’t realize they can demand this action simply by sending a certified letter with documentation.

How to Start Your Dispute and Create a Paper Trail

Start your dispute by obtaining your free credit reports from annualcreditreport.com and identifying every inaccuracy. Write to the credit bureau with specific details about what’s wrong, attach copies of supporting documents, and mail via certified mail with return receipt requested. The paper trail matters enormously if you later need to prove the violation occurred. Furnishers also receive the same 30-day investigation deadline, and when they discover information is inaccurate, they must notify all three major bureaus to correct your file. Many violations persist because consumers fail to pursue this documented process, allowing false information to remain unchallenged.

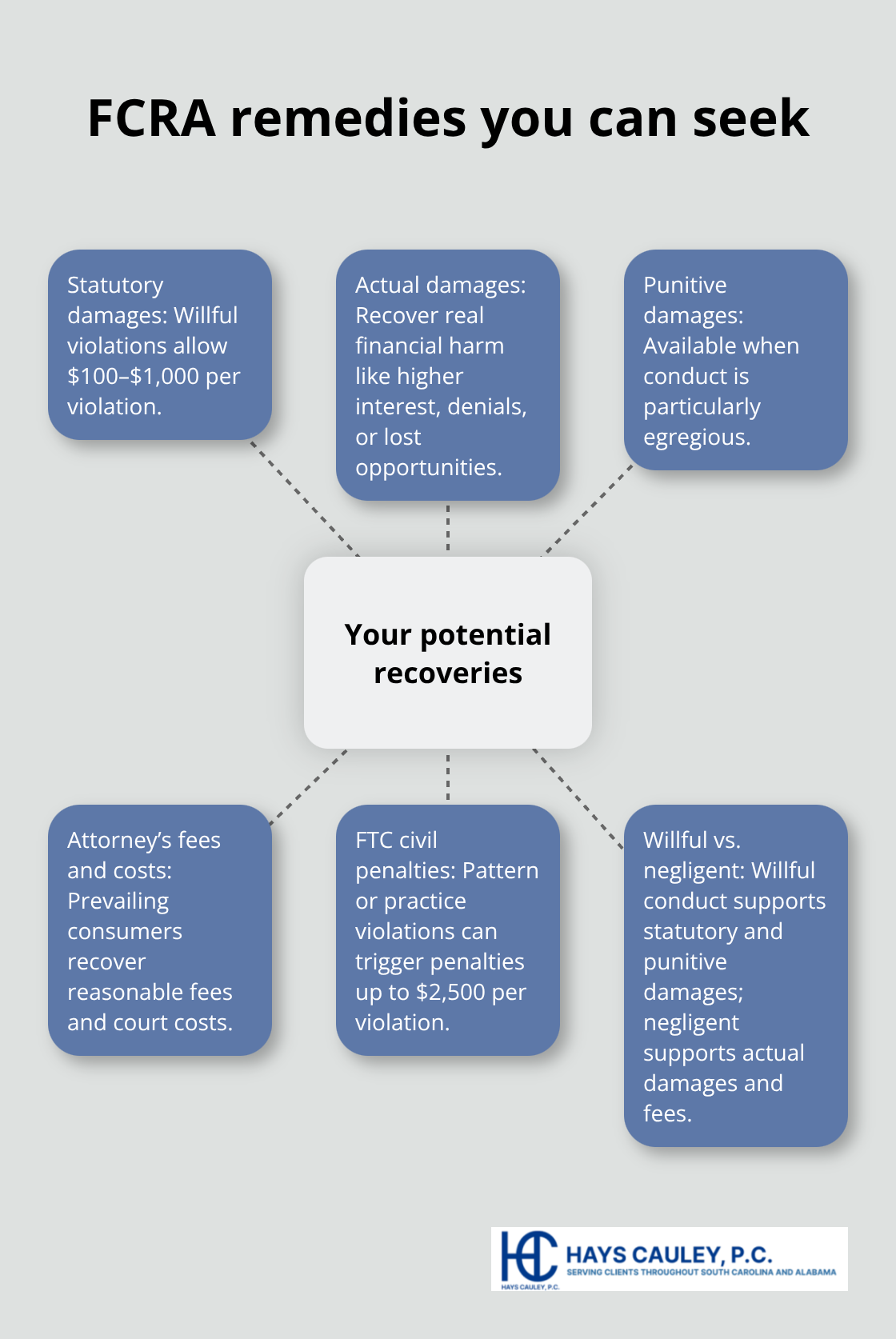

Statutory Damages: The $100-$1,000 Recovery You Deserve

Willful FCRA violations-meaning the violator knowingly or recklessly disregarded the law-entitle you to statutory damages ranging from $100 to $1,000 per violation under 15 U.S.C. § 1681n, plus actual damages reflecting your real financial harm. If a credit bureau illegally pulled your report without a permissible purpose or a furnisher knowingly reported false information, you can recover the greater of your actual damages or $1,000 per violation. Courts also award punitive damages in willful violation cases when the violator’s conduct was particularly egregious. The prevailing party recovers reasonable attorney’s fees and court costs, meaning you don’t shoulder the full financial burden of litigation.

Actual Damages and How to Document Them

Actual damages include costs you incurred from the violation: higher interest rates paid on loans, denied credit applications, job rejections, or housing denials directly caused by inaccurate reporting. Negligent violations under 15 U.S.C. § 1681o allow recovery of actual damages plus costs and attorney’s fees, though without the $100-$1,000 statutory minimum. Document every harm the violation caused-medical debt from denied insurance, higher mortgage payments from a reduced credit score, lost wages from a rejected job offer-because these damages strengthen your claim significantly and increase settlement value or jury awards.

Pattern or Practice Violations and FTC Enforcement

The FTC itself can bring enforcement actions against credit bureaus or furnishers for pattern or practice violations, imposing civil penalties up to $2,500 per violation. These penalties apply to any person or entity that violates the FCRA, including credit bureaus, furnishers, employers, and data brokers. The liability framework distinguishes between willful conduct and negligent mistakes, with different remedies for each. If you obtained a consumer report under false pretenses or without a permissible purpose, the violator owes you actual damages or $1,000, whichever is greater.

Final Thoughts

FCRA violation penalties range from $100 to $1,000 per willful violation, plus actual damages that reflect your real financial harm from inaccurate reporting. Start by obtaining your free credit reports from annualcreditreport.com, identify every error, and write to the credit bureau with specific details and supporting documents sent via certified mail with return receipt requested. The credit bureau must investigate within 30 days and correct inaccurate information or remove it entirely from your report.

If disputes fail to resolve the problem, you have the right to pursue legal remedies against the credit bureau, furnisher, or both for damages and attorney’s fees. Punitive damages and court costs apply in egregious cases, shifting the financial burden of litigation away from you and onto the violator. Document every harm the violation caused-higher interest rates, denied credit applications, job rejections, or housing denials-because these damages strengthen your claim significantly.

We at Hays Cauley, P.C. help South Carolina residents protect their credit rights when violations occur and hold violators accountable for the harm they cause. If you believe your FCRA rights were violated, contact Hays Cauley, P.C. to discuss your situation and explore your legal options. Your credit report shapes your financial future, and you deserve accuracy and protection under the law.