FCRA Guidance SC Understanding Your Rights

Your credit report affects major life decisions-from getting a mortgage to landing a job. Errors on that report can derail your financial future, and credit reporting agencies don’t always get it right.

We at Hays Cauley, P.C. created this FCRA guidance for South Carolina residents to help you understand what protections federal law gives you. This guide walks you through your rights, how to spot violations, and what steps to take if your information has been mishandled.

Understanding the FCRA: What It Protects and Your Rights, Serving South Carolina, Including Greenville, Columbia and Charleston

What the FCRA Actually Covers

The Fair Credit Reporting Act protects information that consumer reporting agencies collect-credit bureaus like Equifax, Experian, and TransUnion, plus medical information companies and tenant screening services. The FTC enforces the FCRA alongside the Consumer Financial Protection Bureau, which took over rulemaking responsibilities after the Dodd-Frank Act transferred authority in 2010. What matters most to you is that the FCRA controls what information agencies can collect, who can access your reports, and how errors get fixed. The law covers credit decisions, insurance underwriting, employment screening, and rental applications. South Carolina residents receive specific protections under state law: credit bureaus must reinvestigate disputes within 30 days at no cost, and willful violations trigger treble damages or up to $1,000 per incident plus attorney fees. If an inaccuracy damages your creditworthiness and a judgment exists, damages can reach $1,000 per day until removal.

Your Rights to Access and Monitor Your File

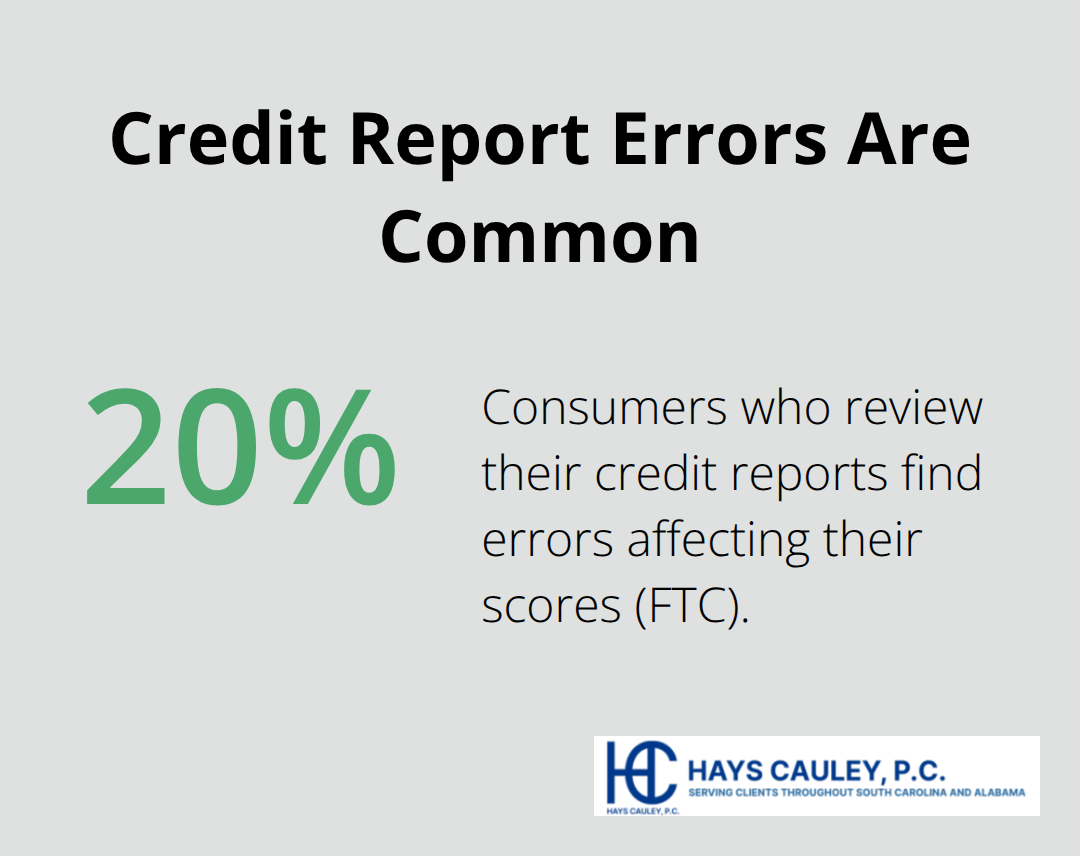

You can obtain one free credit report annually from each of the three major bureaus through annualcreditreport.com or by calling 1-877-322-8228-avoid other sites that charge fees. The FTC reports roughly 20% of consumers who review their reports find errors affecting their scores. A practical approach spreads your requests: pull one report every four months to monitor continuously without cost.

You also have the right to know which entities accessed your report in the past year (two years for employment purposes) and to receive a free copy if you are denied credit. Additional free reports apply if you lack employment and plan to seek work within 60 days, receive public assistance, or suspect fraud. If correcting errors improves your score, the savings compound significantly-moving from 650 to 750 could reduce interest costs on a $200,000 thirty-year mortgage by roughly $68,000 over the loan’s life.

How Disputes and Corrections Work

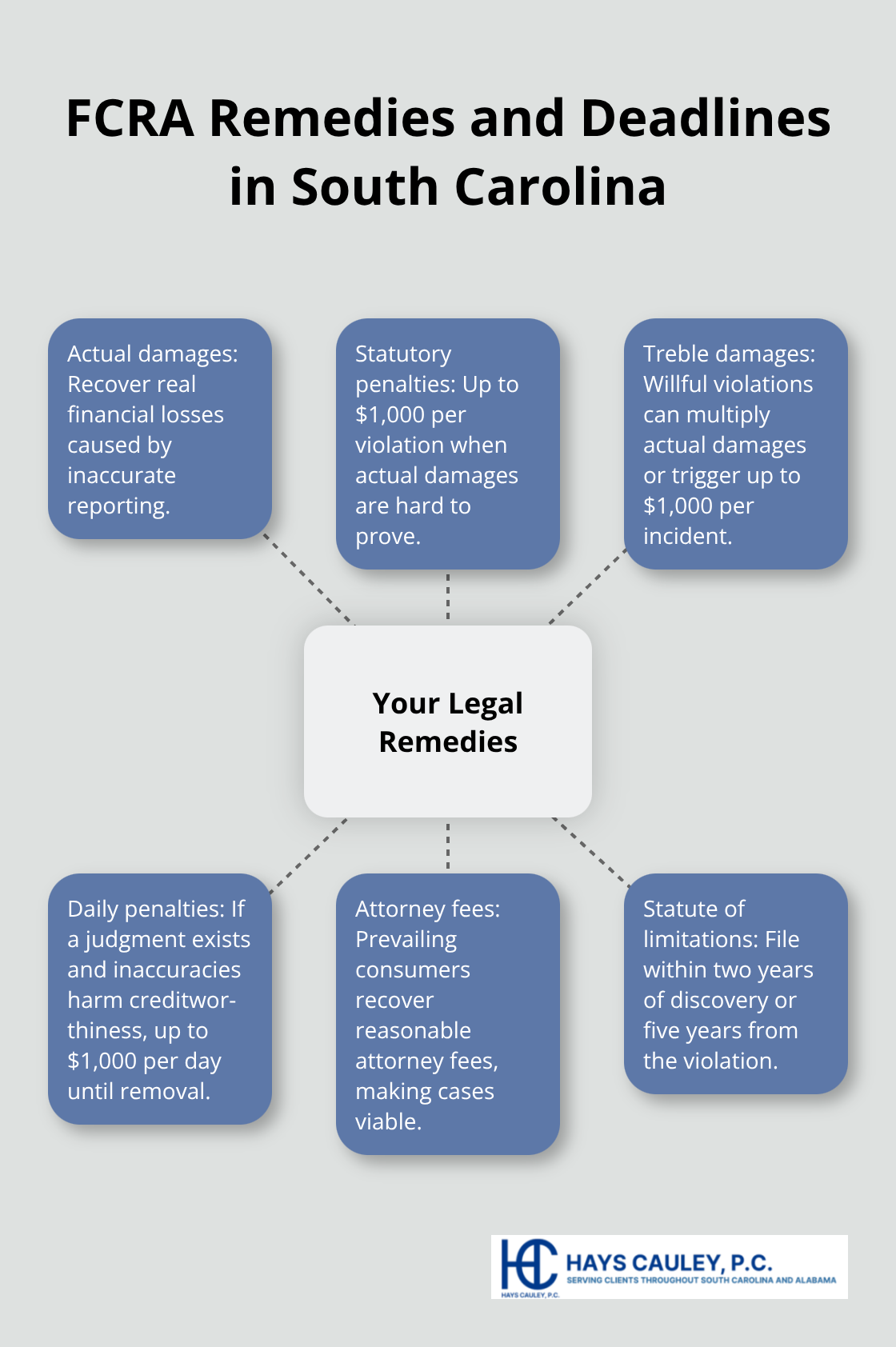

When you spot an error, submit a dispute directly to the bureau via certified mail and keep proof of delivery for your records. The agency must investigate and respond within 30 days; if they find the information inaccurate, they correct it and notify anyone who received your report in the last six months. Furnishers, creditors, lenders, and debt collectors who report to bureaus-have their own duty to investigate disputed items timely. Common issues include unverified tradelines, incorrect account balances, unauthorized hard inquiries, and obsolete public records that should no longer appear. You strengthen your case when you gather supporting documents before disputing: payment statements, court records, proof of account closures, and identity verification. If errors persist after investigation, South Carolina residents can pursue litigation under the FCRA to recover actual damages, statutory penalties up to $1,000 per violation, and attorney fees. The statute of limitations runs two years from discovery or five years from the violation’s occurrence, so acting quickly protects your rights.

What Happens When Violations Occur

Violations of the FCRA carry real consequences for agencies and furnishers. Willful noncompliance can result in treble actual damages or statutory penalties up to $1,000 per incident, while negligent violations trigger actual damages or up to $1,000 per incident. You also recover attorney fees when you prevail, which makes litigation financially viable even for individual cases. The law empowers you to control your credit narrative by accessing reports, disputing inaccuracies, and tracking who has accessed your file. Regular, accurate credit information supports better financial planning for major purchases (home, car) and helps you negotiate more favorable terms with lenders. Consistent credit report reviews can lead to lower loan interest rates, better insurance premiums, and improved job prospects tied to trustworthy credit history.

Understanding these protections sets the foundation for recognizing when violations occur and what remedies you can pursue. The next section identifies the specific violations that harm South Carolina consumers most often and shows you how to spot them in your own credit file.

Common FCRA Violations and How to Identify Them

Inaccurate Information Damages Your Credit Score

Credit reporting agencies and furnishers make mistakes regularly, and some violations cause far more damage than others. Inaccurate account information tops the list of problems that harm South Carolina credit files. Unverified tradelines appear on reports when a furnisher fails to validate whether an account actually belongs to you before reporting it-yet bureaus include these accounts anyway. Incorrect account balances inflate your reported debt and tank your credit score even when you’ve paid down the actual balance. The FTC found that roughly 20 percent of consumers who reviewed their reports discovered errors, and many of those errors directly affected their credit scores. Accounts that should have aged off your report-like paid-off judgments, satisfied liens, or resolved collection accounts-linger for years past their seven-year window. When a bureau receives your dispute, federal law requires them to investigate within 30 days and correct verified inaccuracies, but negligent agencies skip this step or conduct sloppy investigations that miss obvious errors.

Unauthorized Inquiries and Improper Access

Unauthorized hard inquiries from lenders pull your report without consent, and each inquiry can drop your score by a few points. Furnishers also violate the law by ignoring dispute notices from bureaus or responding too late to meet the reinvestigation deadline. South Carolina law amplifies these violations: willful noncompliance by a bureau or furnisher triggers treble damages or up to $1,000 per violation, plus your attorney fees. If an inaccuracy harms your creditworthiness and a judgment exists, damages can reach $1,000 per day until the error is removed. This means violations compound quickly and create substantial liability for agencies and creditors who ignore their legal duties.

How to Spot Violations in Your Own File

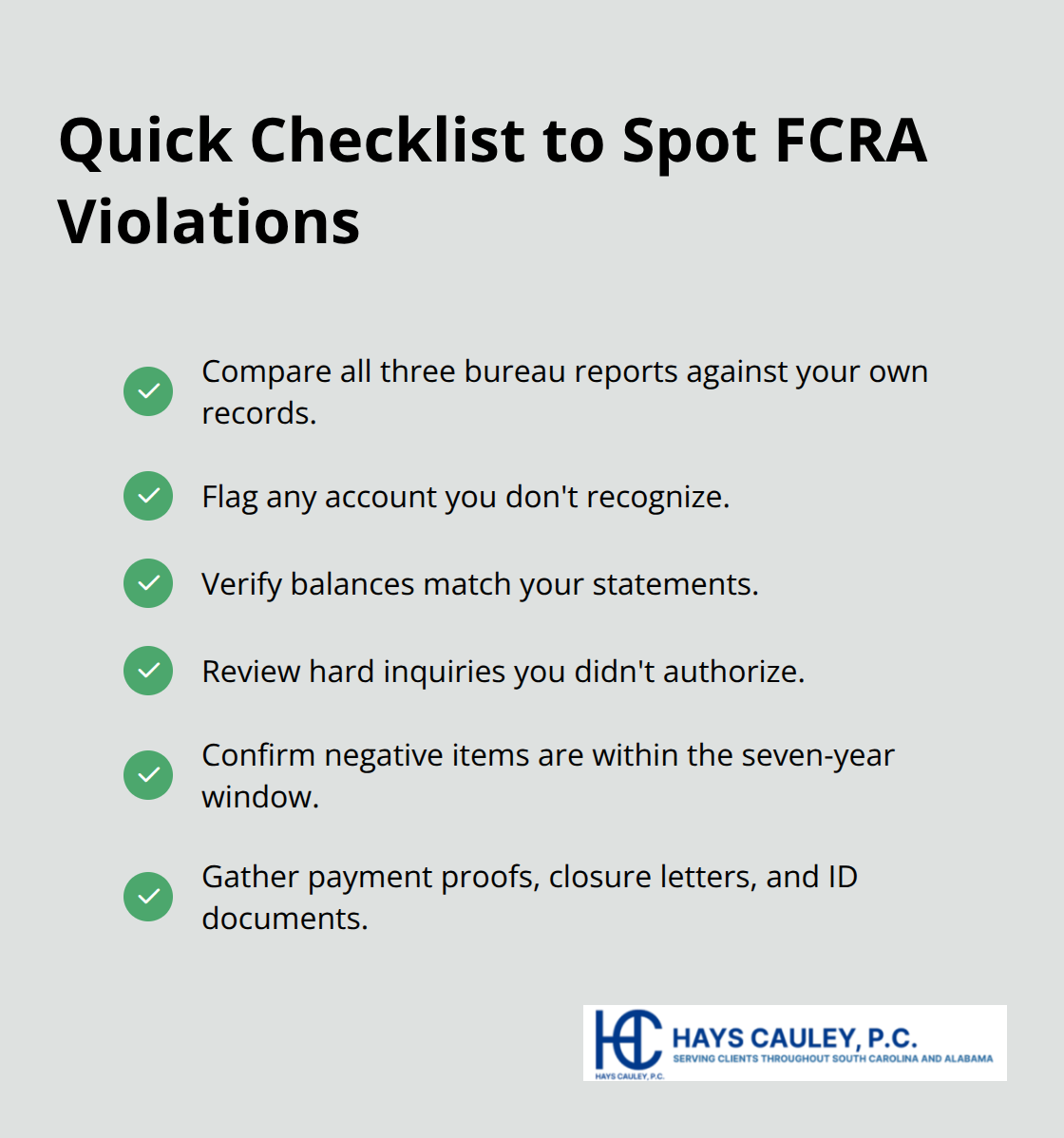

Pull your reports from Equifax, Experian, and TransUnion through annualcreditreport.com and compare them line-by-line against your own payment records and account statements. Flag any account you do not recognize, any balance that does not match your records, and any inquiry from a company you never contacted. Check the dates on negative items-accounts should age off seven years from the first date of delinquency, and paid tax liens or satisfied judgments should disappear after their reporting period ends.

Gather proof of payments, account closure letters, and identity verification documents before you dispute anything, because bureaus and furnishers investigate faster when you provide evidence upfront.

Documentation Strengthens Your Dispute

Submit your dispute via certified mail to create a verifiable record that the bureau received your claim, and keep the delivery confirmation. When the bureau responds, review their findings carefully-if they claim the information is verified but your documents prove otherwise, that investigation failure itself constitutes a violation. Violations that persist after the reinvestigation period ends or those involving suspected willful misconduct warrant legal action. South Carolina residents can recover actual damages, statutory penalties, and attorney fees through federal court, making legal action financially viable even for individual cases.

When to Pursue Legal Action

If errors persist after reinvestigation or if you suspect willful misconduct, litigation becomes necessary to protect your financial interests. Understanding your FCRA dispute rights when creditors refuse your claims helps you take the right steps to challenge violations and recover damages through the legal system.

What to Do When Your Credit Report Has Errors

Obtain and Review Your Credit Reports

Start with certified copies of your credit reports from all three bureaus through annualcreditreport.com, then compare each report against your payment records, bank statements, and account documentation. The FTC found that roughly 20 percent of consumers who reviewed their reports discovered errors, so take this step seriously. Document every discrepancy: unverified accounts, wrong balances, accounts past their seven-year reporting window, and unauthorized inquiries. Create a dispute file containing proof of payments, account closure letters, identity verification documents, and a detailed description of each error you found.

Prepare Strong Documentation for Your Dispute

Solid documentation strengthens your case significantly. Agencies respond faster to disputes backed by proof, so gather your evidence before you submit anything. Include copies of supporting documents but retain originals for your records. Submit your dispute via certified mail to each bureau that reports the error, and keep the delivery confirmation as proof they received your claim. This documentation becomes your evidence when the bureau investigates.

Understand the 30-Day Investigation Timeline

The bureau must investigate and respond within 30 days under South Carolina law. If they find information inaccurate, they correct it and notify any entity that received your report in the last six months. Furnishers, creditors, lenders, and debt collectors-have their own obligation to investigate disputed items timely, so consider sending dispute notices directly to them as well using certified mail. This dual approach (sending notices to both bureaus and furnishers) increases pressure for accurate corrections.

Take Legal Action if Errors Persist

If errors persist after the 30-day reinvestigation period or if the bureau conducts a sloppy investigation that ignores your evidence, litigation becomes your next step. South Carolina residents can recover actual damages, statutory penalties up to $1,000 per violation, and attorney fees through federal court. Willful violations by bureaus or furnishers trigger treble damages or up to $1,000 per incident, and if inaccurate information damages your creditworthiness and a judgment exists, damages can reach $1,000 per day until removal.

The statute of limitations runs two years from discovery or five years from the violation’s occurrence, so act quickly to preserve your rights. We at Hays Cauley, P.C. handle FCRA litigation for South Carolina consumers and can review your dispute history, credit reports, and bureau responses to identify violations and build your case. Contact us for a confidential consultation to understand whether your situation warrants legal action and what damages you may recover.

Final Thoughts

Your FCRA rights protect you from inaccurate reporting, unauthorized access, and agency negligence that damages your financial life. South Carolina amplifies these protections with state-level requirements: 30-day reinvestigation periods, treble damages for willful violations, and daily penalties up to $1,000 when inaccuracies harm your creditworthiness. This FCRA guidance SC empowers you to act decisively when errors appear on your file.

Start by pulling your free annual credit reports from Equifax, Experian, and TransUnion through annualcreditreport.com and review them carefully against your payment records. If errors persist after 30 days or if you suspect willful misconduct, litigation becomes your path to recovery (the statute of limitations runs two years from discovery or five years from the violation). South Carolina residents can file complaints with the FTC at ReportFraud.ftc.gov if agencies ignore your rights, and you can place a security freeze on your credit file within five business days at no cost.

We at Hays Cauley, P.C. help South Carolina consumers enforce their FCRA rights through dispute resolution and litigation. If you believe your credit file contains errors harming your finances, contact us for a confidential consultation to understand your options and protect your credit future.