Resolving credit report errors: A Step-By-Step Guide to Correcting Your Credit

A mistake on your credit report can tank your score and cost you thousands in higher interest rates. Yet most people never check their reports, so errors go unnoticed for years.

Resolving credit report errors is simpler than you think-and your legal rights are stronger than you realize. We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, fight back against inaccurate information that damages their financial future.

Why Credit Report Errors Happen More Often Than You’d Think

The Scale of the Problem

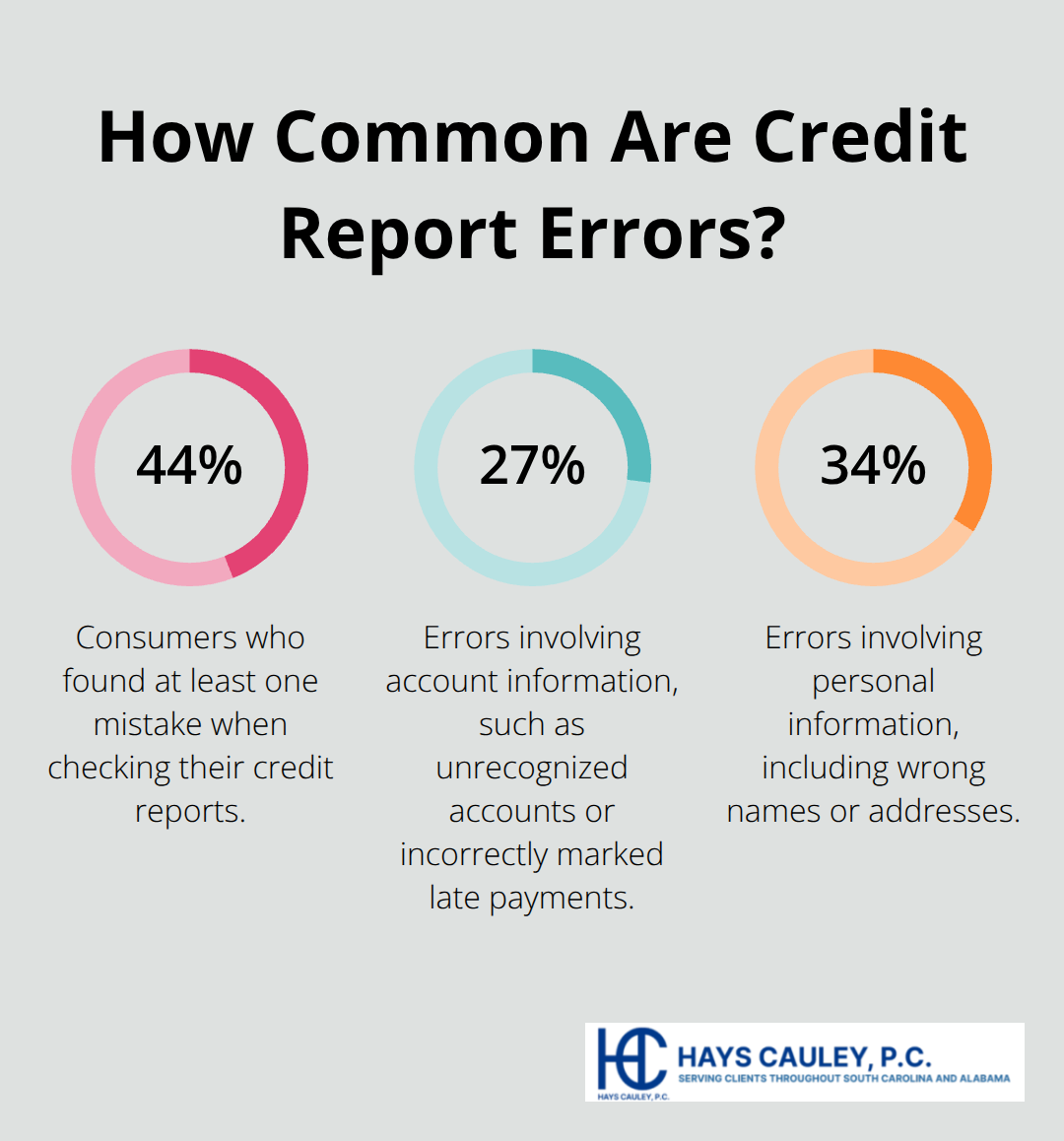

Credit report errors are far more common than most people realize, and they stem from surprisingly mundane sources. The CFPB reported that credit report errors became the top consumer complaint for three consecutive years, with complaints skyrocketing from 165,129 in 2021 to 430,600 in 2023. A Consumer Reports and WorkMoney study found that 44% of participants who checked their credit reports discovered at least one mistake. Among those errors, 27% involved account information problems like unrecognized accounts, late payments marked incorrectly, or debts that didn’t belong to them appearing in collections. Another 34% found personal information errors, including wrong names or addresses on file.

These aren’t rare edge cases-they’re happening to millions of South Carolina residents right now.

How Errors Enter the System

The mistakes happen because the credit reporting system relies on data flowing from hundreds of thousands of sources to three major bureaus: Equifax, Experian, and TransUnion. Banks, credit card companies, landlords, and debt collectors constantly feed information into this system, and the volume creates opportunity for human error and data mix-ups. Mixed files occur when information from someone with a similar name or Social Security number gets attached to your report. Paid-off accounts sometimes show as unpaid, duplicate loans appear, and collections debts get listed incorrectly.

The Financial Damage Errors Cause

The worst part is that these errors damage your financial health immediately. A single inaccuracy can lower your credit score by 50 to 100 points, which translates directly into higher interest rates on mortgages, auto loans, and credit cards. Over the life of a 30-year mortgage, a lower credit score can cost you tens of thousands of dollars. Beyond lending, inaccurate credit reports affect housing approvals, employment opportunities, and even insurance rates. The damage compounds because most people discover these errors only after applying for credit and getting denied-meaning the error has already been working against them for months or years without their knowledge. This is why identifying and correcting errors quickly matters so much, and why the next steps in the dispute process demand your immediate attention.

Finding and Documenting Every Error on Your Credit Report: Serving South Carolina, Including Greenville, Columbia, and Charleston

Access Your Reports From All Three Bureaus

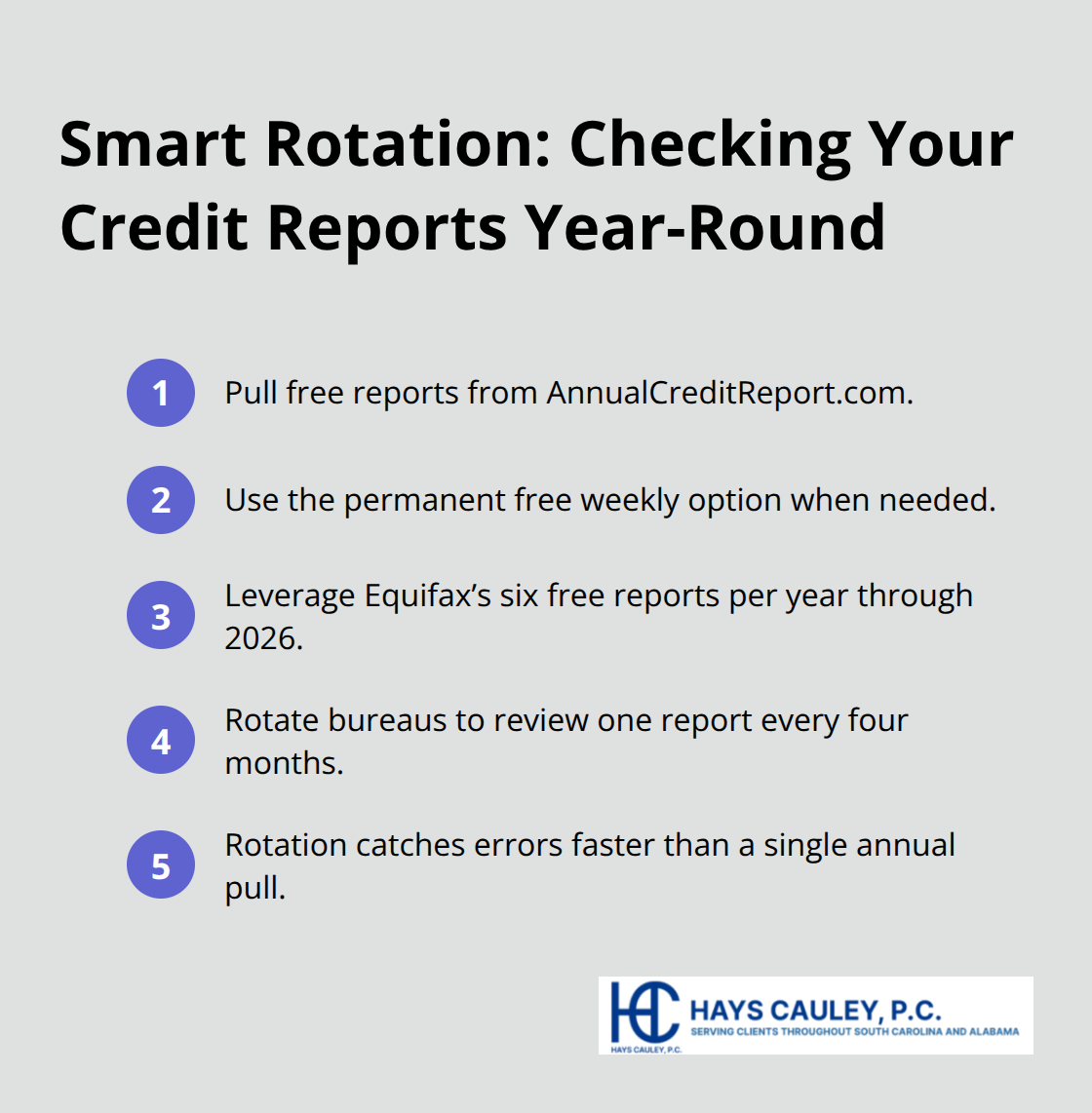

Start by pulling your credit reports from all three bureaus before you do anything else. You can access them free once every 12 months through annualcreditreport.com, or take advantage of the permanent weekly option available on the same site. Equifax offers up to six free reports per year through 2026 as well. Don’t pull all three at once and then wait months to check again. Instead, rotate them so you review one report every four months, which gives you ongoing visibility into your file throughout the year. This rotation strategy catches errors faster than waiting for your annual pull.

Navigate Identity Verification Challenges

When you log in, you’ll need to verify your identity by answering security questions about your credit history. If you can’t answer these questions because they reference old accounts or inaccurate information, the system may lock you out temporarily. This is frustrating but common, so stay patient and try again after a few hours or use an alternate verification method if available.

Scan for Three Categories of Errors

Once you have your reports in hand, read them line by line looking for three categories of problems. First, scan for account information errors: accounts you don’t recognize, late payments marked on accounts you paid on time, duplicate loans, or debts in collections that aren’t yours. The Consumer Reports and WorkMoney study found that 27% of people checking their reports found these types of mistakes. Second, look for personal information mistakes like incorrect names, addresses, phone numbers, or Social Security numbers, which 34% of study participants discovered. Third, watch for mixed files where someone else’s data appears on your report, which signals potential identity theft.

Gather and Organize Supporting Documentation

Once you spot an error, collect supporting documents immediately. Pull bank statements showing on-time payments, creditor letters, receipts, payment confirmations, or any correspondence proving the information on your report is wrong. Organize these documents by error so when you file your dispute, you have a clear paper trail. The stronger your documentation, the faster the investigation moves. Send copies only, never originals, and keep everything in a folder you can reference throughout the dispute process. With your evidence assembled and errors identified, you now have what you need to move forward with the formal dispute process-and understanding your rights under the Fair Credit Reporting Act will strengthen your position considerably.

How to File a Dispute and Protect Your Rights: Serving South Carolina, Including Greenville, Columbia, and Charleston

Send Your Dispute Letter by Certified Mail

Now that you’ve identified errors and gathered documentation, send a written dispute letter to each credit bureau reporting the error. Use certified mail with return receipt so you have proof of delivery. Your letter should include your full contact information, the confirmation number from your credit report if available, each disputed item with its account number, a clear explanation of why the information is wrong, and copies of your supporting documents with errors circled on your report. The CFPB provides a template dispute letter you can use to hit all required elements. Don’t rely on phone disputes or online portals alone-written certified mail creates the paper trail you’ll need if the bureau fails to investigate properly. Mail your dispute to the correct address for each bureau: Equifax at P.O. Box 740256, Atlanta, GA 30348; Experian at P.O. Box 4500, Allen, TX 75013; or TransUnion at P.O. Box 2000, Chester, PA 19016. Keep copies of everything you send.

What Happens During the 30-Day Investigation

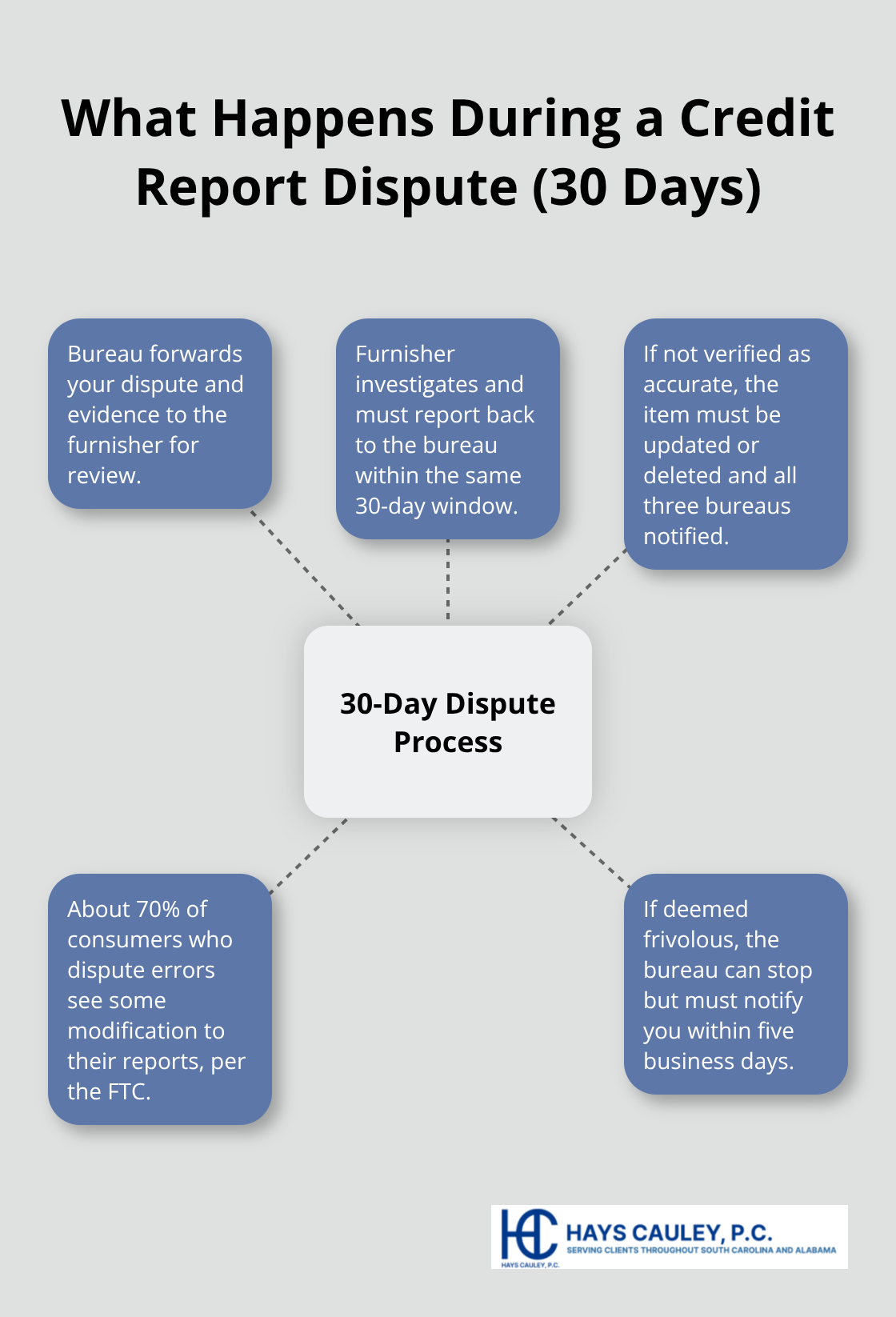

Once the bureau receives your dispute, it has 30 days to investigate. The bureau forwards your dispute and evidence to the furnisher (the bank, credit card company, landlord, or debt collector that reported the information). The furnisher must investigate and report back to the bureau within that same window. If the furnisher cannot verify the information is accurate, it must update or delete the item and notify all three bureaus so the correction appears across your entire credit file. The FTC found that about 70% of consumers who dispute errors see some modification to their reports, though many issues remain unresolved.

If the bureau deems your dispute frivolous or irrelevant, it can stop investigating but must notify you within five business days with an explanation (this rarely happens if your dispute is legitimate and supported by documentation).

Review Results and Request Correction Notices

The bureau must send you written results within 30 days of completing the investigation. If an item was corrected, request an updated copy of your report immediately to confirm the change appears correctly. The bureau must also send correction notices to anyone who received your report in the past six months, and to employers who received it for employment purposes in the past two years if you request it. If the investigation doesn’t resolve the dispute to your satisfaction, you can request a statement of dispute to be included in your file and sent to future report recipients.

Escalate Unresolved Errors to the CFPB

If errors persist and the bureau remains unresponsive, file a complaint with the CFPB, which received over 430,000 credit reporting complaints in 2023 alone. Persistent errors that damage your finances may warrant consulting an attorney who understands the Fair Credit Reporting Act, particularly when furnishers continue reporting disputed information despite your documentation.

Final Thoughts

Resolving credit report errors stops the financial damage immediately. Every month an error remains on your report, it tanks your credit score, inflates your borrowing costs, and blocks opportunities for housing, employment, and fair insurance rates. The dispute process takes 30 days, costs nothing, and follows a clear path you now understand completely.

After your report is corrected, stay vigilant by checking your credit reports quarterly using the free weekly option at annualcreditreport.com so new errors don’t accumulate undetected. Set a calendar reminder to rotate through the three bureaus every four months. If identity theft caused your errors, place fraud alerts on your file and monitor for suspicious activity going forward.

Some errors resist correction despite your best efforts-furnishers ignore disputes, bureaus claim information is accurate when it isn’t, or the same mistake reappears months later. When persistence fails, you need someone who understands the Fair Credit Reporting Act inside and out. We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, fight back against credit reporting violations and hold bureaus and furnishers accountable for inaccurate reporting.