Debt collectors in South Carolina sometimes cross the line, using aggressive tactics that violate your rights. The Fair Credit Reporting Act (FCRA) provides strong protections against harassment, but many consumers don’t know what those protections actually are.

At Hays Cauley, P.C., we help South Carolina residents understand their rights and fight back against illegal collection practices. This guide walks you through what constitutes harassment, how to document violations, and what steps you can take.

How Debt Collectors Violate Your Rights in South Carolina, Including Greenville, Columbia and Charleston

Illegal Contact Methods and Timing

Debt collectors in South Carolina routinely break the rules about when and how they contact you. Calls before 8 a.m. or after 9 p.m. violate federal law unless you’ve given written permission. Calls to your workplace violate the law if your employer objects, yet the Federal Trade Commission documents thousands of workplace-contact complaints annually. Collectors cannot use postcards, demand collect calls, or contact you by telegram or fax in ways that expose your debt to third parties. Many collectors ignore these restrictions because enforcement requires you to document violations and take action. The moment a collector calls at 7:45 a.m. or continues calling after you’ve told your employer you don’t want workplace contact, you have a documented violation worth recording with the date, time, caller name, and exact phone number used.

Threats and Abusive Conduct

Collectors cannot threaten arrest, jail, wage garnishment, or property seizure unless these actions are actually legal in your situation. In South Carolina, wage garnishment for consumer debts is illegal, making any threat to seize your wages an automatic violation. Profanity, threats of violence, repeated calls designed to harass, and publishing your name on debtor lists all violate federal law. Collectors also cannot conceal their identity or claim to represent a government agency when they don’t. A collector who calls repeatedly within hours, uses obscene language, or threatens actions they cannot legally take commits violations that result in statutory damages up to $1,000 per violation under the Fair Debt Collection Practices Act (separate from any actual damages you’ve suffered).

Misrepresentation and False Claims

Debt collectors frequently misstate debt amounts, falsely claim attorney involvement, or pretend documents are legal court papers when they’re not. A collector cannot tell you a debt is yours without verification, yet many demand payment based solely on bulk-purchased debt lists they cannot authenticate. If a collector claims you owe $5,000 when your records show $3,200, that constitutes misrepresentation. If they state they’re calling from an attorney’s office when they work for a collection agency, that violates the law. The Federal Trade Commission reports that false claims about debt amount and attorney involvement rank among the most common collector violations. These misrepresentations matter legally because they give you grounds to dispute the debt, request verification, and ultimately sue if the collector cannot prove their claims-which leads directly to understanding what rights you possess as a South Carolina consumer.

What You Can Actually Do About Debt Collection Violations, Serving South Carolina, Including Greenville, Columbia and Charleston

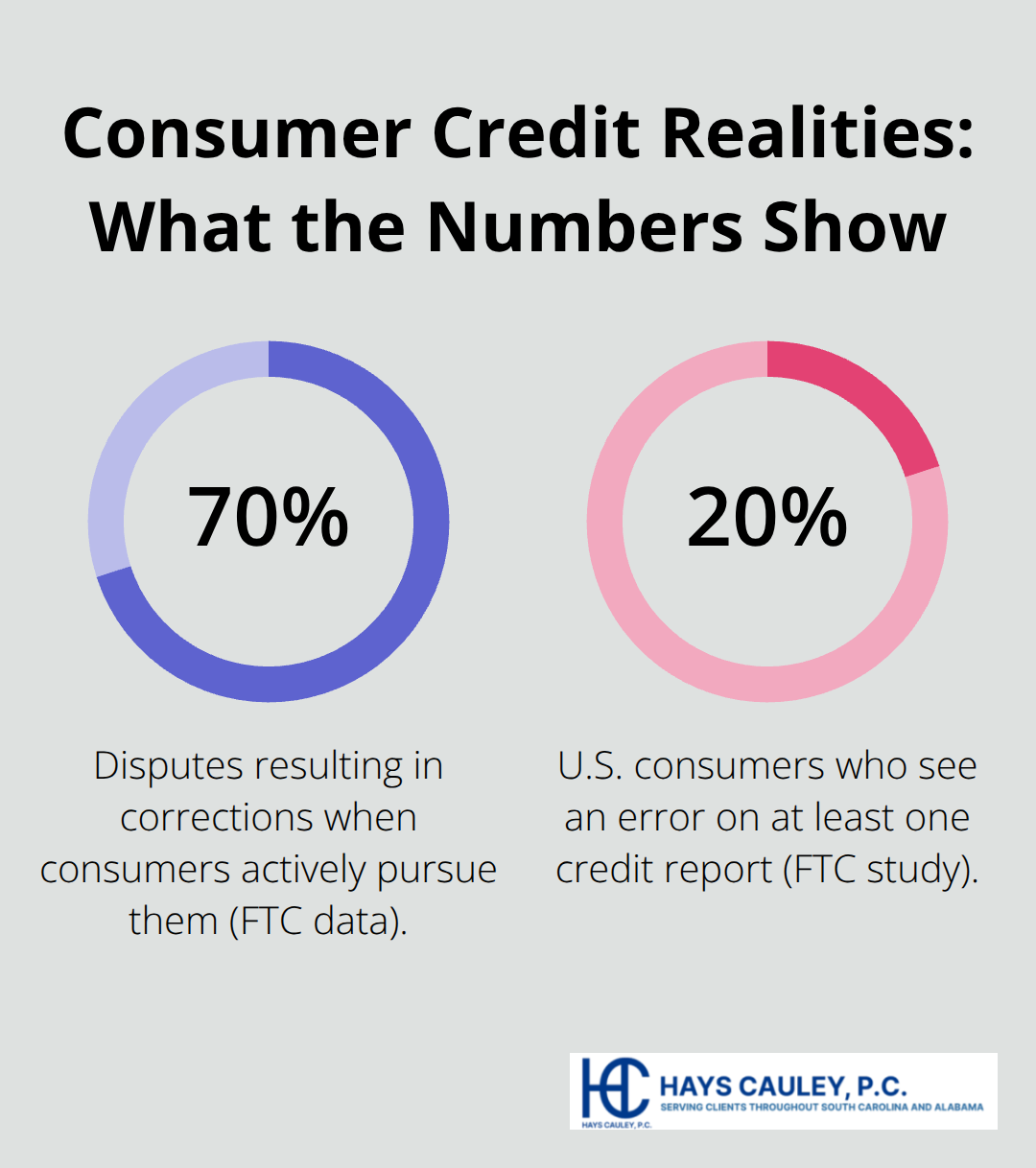

South Carolina law and the Fair Credit Reporting Act give you concrete tools to stop harassment and fight back. The moment a collector contacts you, you possess multiple legal rights that shift the balance of power in your favor. Federal Trade Commission data shows that approximately 70% of disputes result in some correction when consumers actively pursue them, yet most people never take action because they don’t understand what rights exist.

Request Written Debt Validation Immediately

The first actionable step is sending a written debt validation request within 30 days of initial contact. This written request forces the collector to stop collection activity entirely until they provide proof that the debt is actually yours and the amount is correct. Many collectors cannot verify old debts purchased in bulk, meaning they cannot legally continue collection efforts if they cannot produce documentation.

Send this request certified mail with return receipt requested to create a paper trail that proves the collector received your demand. The collector must respond with verification or cease collection, and if they cannot produce legitimate documentation, your leverage increases dramatically because they violate the law by continuing to collect an unverified debt.

Correct Credit Report Errors Before They Cost You

Your credit report directly affects your ability to borrow, rent housing, and in some cases secure employment. A Federal Trade Commission study found that approximately 20% of consumers see an error on at least one of the three major credit bureaus, and inaccurate debt information from collectors contributes significantly to this problem.

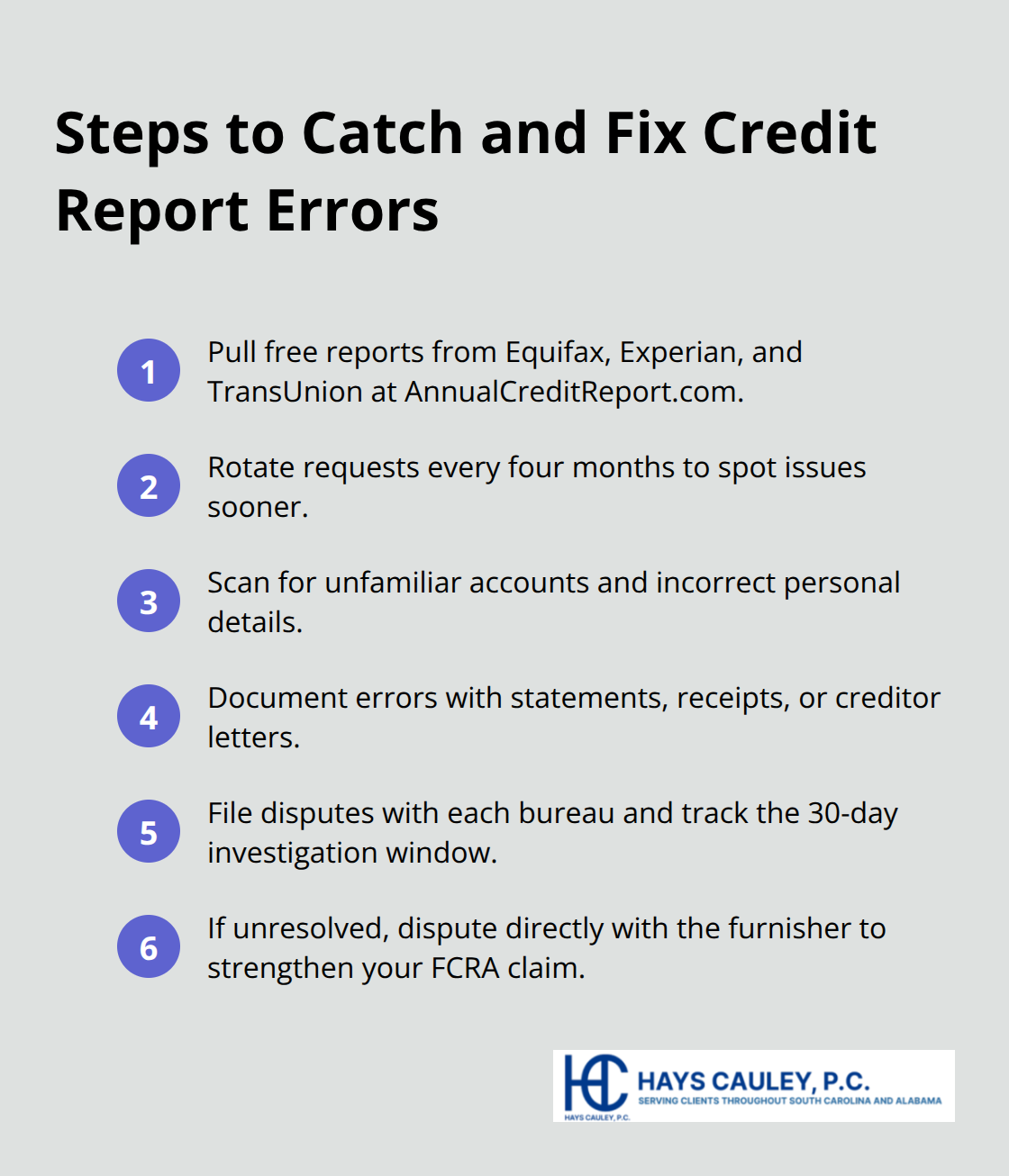

Pull free copies of your credit report from Equifax, Experian, and TransUnion at AnnualCreditReport.com every 12 months, rotating requests roughly every four months to catch errors faster. Look specifically for unfamiliar accounts, incorrect personal details, and negative items related to debts you’re disputing. Document any error immediately with bank statements, receipts, or creditor communications before details fade from memory.

File disputes with each bureau using certified mail and include your supporting documents; the Fair Credit Reporting Act requires bureaus to investigate within 30 days. If the error persists after investigation, dispute directly with the furnisher because the furnisher’s failure to correct strengthens your legal position under the FCRA. The Consumer Financial Protection Bureau received approximately 175,000 credit reporting complaints in 2020, showing how seriously these violations are monitored.

Stop Contact and Build Your Legal Case

Send a written cease-and-desist letter by certified mail if a collector continues contacting you after you’ve requested they stop. Under federal law, collectors must honor this request within five days and can only contact you thereafter to confirm receipt or inform you of specific legal action.

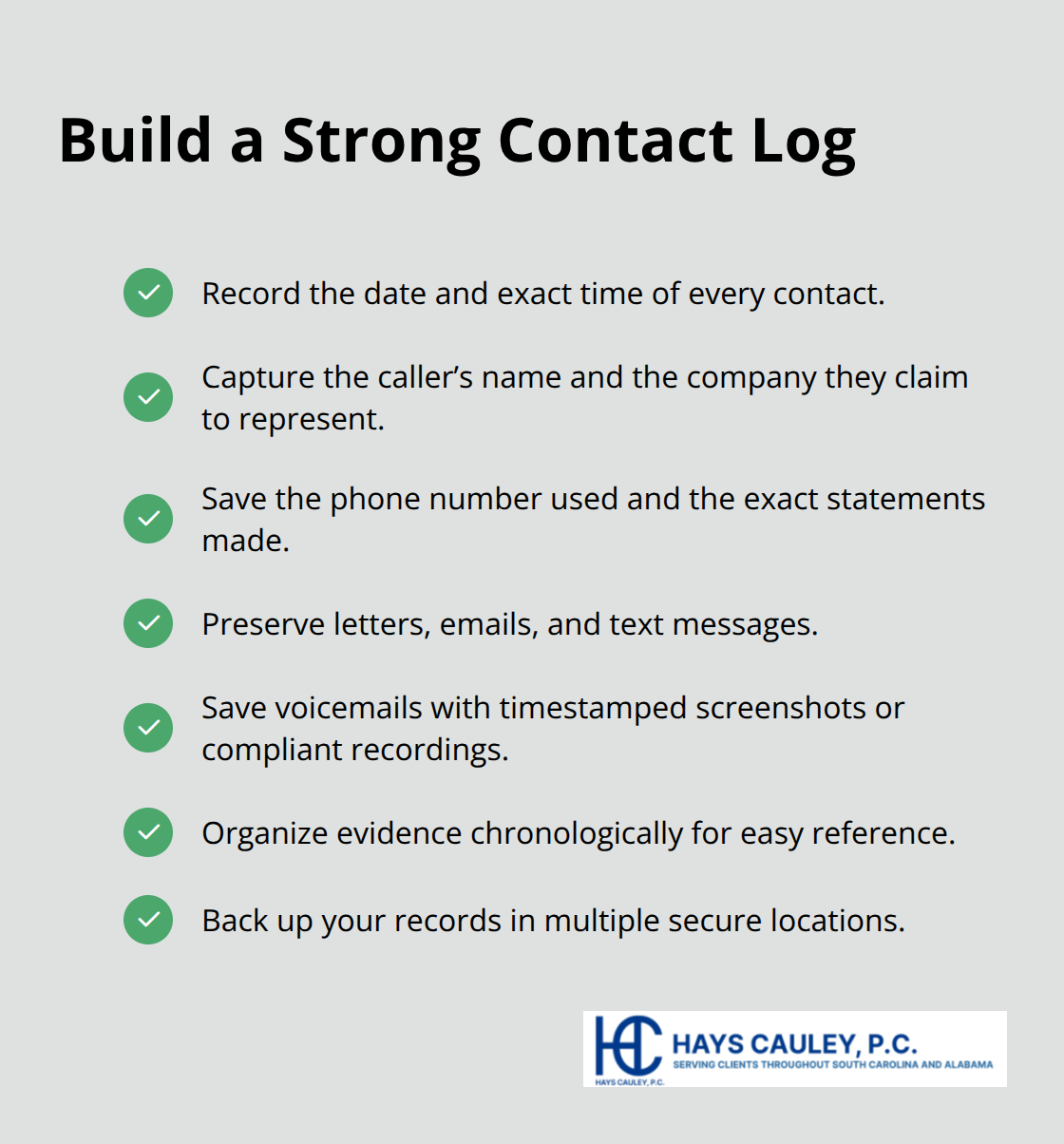

Simultaneously, document every single contact with the collector: record the date, time, caller name, company name, phone number used, and the exact statements made. Preserve all written communications including letters, emails, and text messages, and save voicemails by taking timestamped screenshots or recording them. This documentation becomes your evidence if you pursue legal action, and South Carolina courts require detailed records to prove violations.

Sue for Damages and File Complaints

If a collector violates the Fair Debt Collection Practices Act or South Carolina’s consumer protection laws, you can sue for actual damages plus statutory damages up to $1,000 per violation, and you recover attorney’s fees and court costs if you win. You have one year from the violation date to file suit in state or federal court.

File a complaint with the Consumer Financial Protection Bureau at ConsumerCompliance.gov, which typically takes 15 minutes and forces the collector to respond within a set timeframe. The CFPB publishes complaint data that supports enforcement action against repeat violators, meaning your complaint contributes to broader accountability. When violations mount and documentation proves a pattern of illegal conduct, the collector faces serious financial exposure that often motivates settlement or cessation of harassment.

Build Your Evidence and File Complaints, Serving South Carolina, Including Greenville, Columbia and Charleston

Document Every Contact with Precision

Documentation separates successful legal cases from failed attempts because courts require concrete proof of violations. Start recording the moment a collector first contacts you. Write down the exact date and time of every call, text, email, or letter received from a collector. Include the caller’s name, the company they claim to represent, the phone number they used, and word-for-word what they said. If a collector threatens wage garnishment, record that specific statement. If they call at 6:45 a.m., note the exact time. If they use profanity or make false claims about debt amount, capture those details immediately while they’re fresh.

This documentation becomes admissible evidence in court, and courts heavily weight detailed, contemporaneous records over vague recollections made months later. Many collectors count on consumers forgetting details or giving up before gathering sufficient proof, so your meticulous record-keeping directly undermines their strategy.

Preserve Written Communications Across Multiple Locations

Save every letter, email, and text message from collectors, and take timestamped screenshots to prevent deletion or modification claims later. Save voicemails by recording them on your phone or using a call recording app that complies with South Carolina’s two-party consent law. Store copies in multiple locations so a lost phone or computer doesn’t erase your evidence. When you’ve gathered enough documentation showing a pattern of violations, you possess the foundation for legal action.

File a Complaint with the Consumer Financial Protection Bureau

The Consumer Financial Protection Bureau received over 175,000 credit reporting complaints in 2020 according to the Bureau itself, demonstrating the scale of enforcement scrutiny these cases receive. File a complaint at ConsumerCompliance.gov, which takes approximately 15 minutes and triggers a mandatory response requirement from the collector. The CFPB publishes aggregated complaint data that regulators use to target enforcement actions against repeat violators. Your complaint contributes to broader accountability and creates an official record of the collector’s conduct.

Sue for Damages in State or Federal Court

After filing with the CFPB and documenting violations thoroughly, you can sue in state or federal court for actual damages plus statutory damages up to $1,000 per violation, with attorney’s fees and court costs awarded if you prevail. You have one year from each violation date to file suit, so don’t delay once violations occur. Many collectors settle cases before trial when faced with solid documentation and a clear legal violation, particularly when multiple violations stack up (a pattern of conduct strengthens your position significantly).

We at Hays Cauley, P.C. help South Carolina consumers in Greenville, Columbia, and Charleston stop debt collector harassment and hold collectors accountable.

Final Thoughts

Debt collection harassment in SC violates your rights under the Fair Credit Reporting Act and federal law, but you possess concrete tools to fight back. Start immediately by sending a written debt validation request within 30 days of first contact, then document every call, text, email, and letter with precise dates, times, and exact statements made by collectors. File a complaint with the Consumer Financial Protection Bureau to create an official record, pull your credit reports from all three bureaus to dispute inaccurate information, and send a cease-and-desist letter by certified mail if contact continues after you request it stop.

When violations mount and documentation proves a pattern of illegal conduct, you can sue for actual damages plus statutory damages up to $1,000 per violation, with attorney’s fees and court costs awarded if you win (you have one year from each violation to file suit). Many collectors settle cases before trial when faced with solid documentation and clear legal violations, so your meticulous record-keeping directly undermines their strategy and increases your leverage significantly. Approximately 70% of disputes result in corrections when consumers actively pursue them, yet most people never take action because they underestimate their own power.

We at Hays Cauley, P.C. help South Carolina consumers stop debt collection harassment and hold collectors accountable for violations. Contact us today to discuss your situation and learn how we can protect your rights.