What is FCRA rights: Your Guide to the Federal Credit Reporting Act

Your credit report affects everything from loan approvals to job opportunities. Yet many people in South Carolina don’t know what FCRA rights actually protect them or how to use those protections.

We at Hays Cauley, P.C. created this guide to show you exactly what the Federal Credit Reporting Act does for you and how to defend yourself when violations happen.

What the FCRA Actually Does

The Federal Credit Reporting Act became law in 1970 and governs how your personal financial information gets collected, stored, and shared. The law applies to credit bureaus like Equifax, Experian, and TransUnion, but it also covers medical information companies, tenant screening services, and any organization that compiles information about you for others to use in making decisions. Banks, employers, landlords, and insurance companies all rely on consumer reports, which is why the FCRA exists: to stop these organizations from misusing your data and to give you tools to fix errors that damage your financial life. The FTC enforces most FCRA violations, while the Consumer Financial Protection Bureau handles rulemaking. In South Carolina, the law protects your ability to access your own credit information, challenge inaccurate entries, and control who sees your data. The CFPB received more than 175,000 credit reporting complaints in 2020, and the FTC found that about one in five consumers discovers an error on at least one credit report. These numbers show how common reporting mistakes are and why understanding your FCRA rights matters.

How to Access Your Credit Report

You have the right to see what information credit bureaus hold about you. You can obtain a free copy of your credit report from Equifax, Experian, and TransUnion once every 12 months through annualcreditreport.com. Smart South Carolina residents rotate through the three bureaus so they review all reports roughly every four months rather than pulling all three at once. This approach gives you ongoing visibility into your file throughout the year. If an employer or lender takes adverse action based on your credit report, they must notify you and provide a copy of the report they used. Pull your reports regularly and look for unfamiliar accounts, incorrect payment histories, or accounts that don’t belong to you.

Fixing Errors Works If You Act Quickly

Credit reporting agencies must investigate disputes within 30 days and correct errors if the investigation finds them valid. This 30-day window is not a suggestion. When you find an error, gather supporting documents like bank statements, receipts, or creditor correspondence and file your dispute in writing using certified mail with return receipt requested. The CFPB provides templates to help structure your dispute letter. After you file, monitor for responses and request an updated copy of your credit report to confirm the changes were made. If the bureau doesn’t correct the error, you can add a brief personal statement to your file explaining your side. If disputes remain unresolved, escalate to the furnisher directly or seek legal assistance under the FCRA.

What Happens When Bureaus Ignore Your Dispute

Persistent errors that credit bureaus refuse to correct can damage your creditworthiness and cost you money in higher interest rates or denied applications. Hays Cauley, P.C. helps South Carolina residents challenge reporting errors when credit bureaus and furnishers refuse to correct inaccurate information. The FCRA gives you legal remedies when violations occur, including the ability to recover actual damages or at least $1,000 per incident, plus attorney’s fees and costs. Understanding these protections sets the stage for recognizing when violations happen and what steps you need to take next.

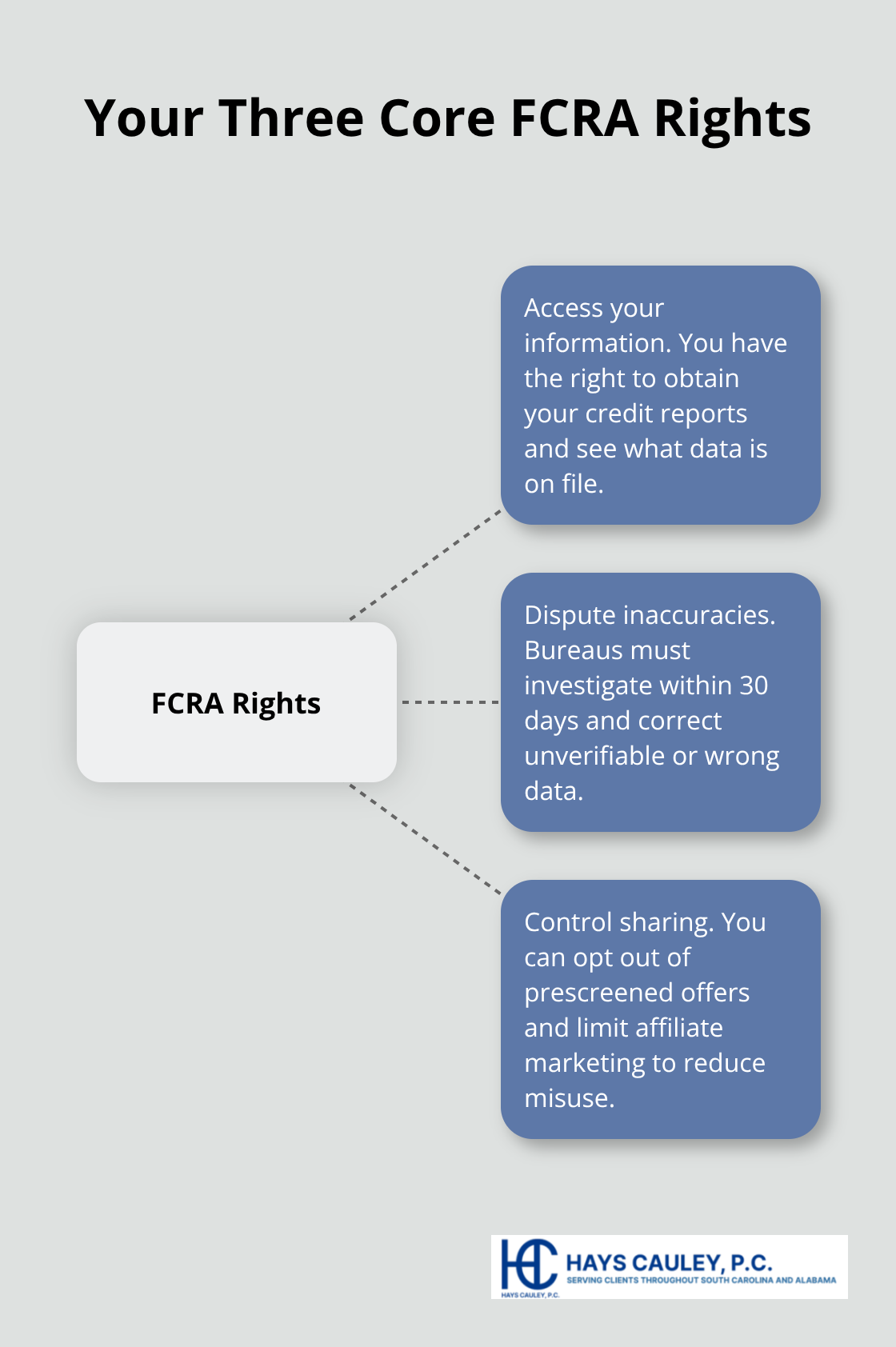

Your FCRA Rights and How to Use Them

The FCRA gives you three foundational rights that directly impact your ability to manage your financial reputation. First, you have the absolute right to know what information credit bureaus maintain about you. This isn’t passive knowledge-it’s actionable intelligence. When you pull your credit reports from Equifax, Experian, and TransUnion through annualcreditreport.com, you see the exact data that lenders, employers, and landlords use to make decisions about you. The FTC emphasizes that you should review these reports before any adverse action occurs, not after. Many South Carolina residents wait until they’re denied a loan or job to check their reports, which means they’ve already suffered the damage. Start pulling reports now and establish a rotation system.

Your Right to Access Your Credit Information

You can obtain a free copy of your credit report from each of the three major bureaus once every 12 months. Smart South Carolina residents rotate through the three bureaus so they review all reports roughly every four months rather than pulling all three at once. This approach gives you ongoing visibility into your file throughout the year.

If an employer or lender takes adverse action based on your credit report, they must notify you and provide a copy of the report they used. Pull your reports regularly and look for unfamiliar accounts, incorrect payment histories, or accounts that don’t belong to you.

Your Right to Challenge Inaccurate Information

Second, you hold the explicit right to dispute information you believe is inaccurate. This right has teeth. When you file a dispute in writing with a credit bureau, they must investigate within 30 days and respond with findings. If they find the information was wrong, they correct it and notify any creditor or organization that received your report in the previous six months. The law doesn’t require the error to be obvious or egregious-if you challenge it and the bureau can’t verify it, they must remove it. The CFPB handles over 100,000 consumer complaints weekly about financial products and services, and credit reporting complaints represent a significant portion of that volume.

Your Right to Control Information Sharing

Third, you can control how your information flows to third parties. You can opt out of prescreening, which stops credit card companies and other lenders from using your report to send unsolicited offers. Call 1-888-5OPTOUT to opt out of prescreened marketing. You can also stop banks and creditors from sharing your transactional information with affiliates for marketing purposes. These aren’t minor conveniences-they directly reduce your exposure to fraud and unwanted solicitations.

How to File a Dispute That Works

Understanding these rights in isolation means nothing without knowing how to exercise them. When you find an error on your report, gather supporting documentation before filing your dispute. Bank statements, receipts, correspondence with creditors, or payment confirmations give you ammunition when the bureau investigates. File your dispute in writing using certified mail with return receipt requested. The CFPB provides templates that structure your letter properly, which matters because poorly formatted disputes sometimes get rejected or delayed. After filing, expect a response within 30 days. Track the investigation actively. If the bureau corrects the error, request a fresh copy of your credit report to verify the change. If they refuse to correct it despite your evidence, add a brief personal statement to your file explaining your perspective.

When Bureaus Refuse to Correct Errors

If the error persists and continues damaging your creditworthiness, you have legal recourse. The FCRA allows you to recover actual damages or at least $1,000 per incident, plus attorney’s fees and costs. Negligent violations by bureaus or furnishers carry these penalties. Willful violations-where a bureau knowingly violates the law-can result in triple damages. In South Carolina, persistent reporting errors that bureaus refuse to fix often require professional help to enforce your legal rights when violations occur.

FCRA Violations That Damage Your Credit

The FCRA exists because credit bureaus, lenders, and employers frequently violate it. Inaccurate reporting happens constantly in South Carolina. When Equifax, Experian, or TransUnion fails to investigate your dispute within 30 days, that constitutes a violation. When a creditor pulls your credit report without permission, that constitutes a violation. When a bureau refuses to remove information you’ve successfully challenged, that violation carries teeth-the law lets you recover actual damages or at least $1,000 per incident, plus attorney’s fees and costs. The FTC found that about one in five consumers discovers an error on at least one credit report, and many of those errors stem from negligence or willful misconduct by the agencies handling your data.

How Inaccurate Information Damages Your Financial Life

South Carolina residents often discover that old accounts, paid-off debts, or accounts belonging to someone else appear on their reports. These errors don’t fix themselves, and waiting makes them worse. Inaccurate negative information stays on your report for seven years unless you actively force its removal. If a lender denies you a mortgage because of a false account, or an employer rejects your application due to fraudulent information, you’ve suffered real financial harm. The FCRA gives you the power to fight back, but only if you recognize when violations occur and act decisively.

Unauthorized Access to Your Credit Report

Unauthorized access to your credit report represents another serious violation that many South Carolina residents don’t catch until months after it happens. Your employer needs your written consent before pulling your report for employment purposes, yet some companies do it without permission. Credit card companies sometimes access your report to market new products without your authorization. Identity thieves may pull your report as part of a fraud scheme. The CFPB handles over 100,000 consumer complaints weekly, and credit reporting violations make up a substantial portion of that volume.

When you discover unauthorized access, file a dispute immediately with the credit bureau and request they document who accessed your file. The bureau maintains access logs and must provide this information upon request. If the access was truly unauthorized, you have legal grounds for compensation.

Bureaus That Refuse to Remove Disputed Information

Bureaus that fail to remove disputed information after investigation also violate the FCRA. If you’ve provided supporting documentation proving an account isn’t yours or a debt was paid, and the bureau still refuses to delete it, that constitutes a willful violation that can result in actual damages or at least $1,000 per violation. Document everything-keep copies of your dispute letters, the bureau’s responses, your supporting evidence, and any correspondence with creditors. This documentation becomes critical if you need to pursue legal action to enforce your rights.

Taking Action Against Violations in South Carolina

When violations persist despite your efforts to resolve them, you may need professional assistance. A consumer protection law firm can help South Carolina residents recover damages and force bureaus to correct records that continue harming your creditworthiness. The evidence you’ve collected (dispute letters, bureau responses, supporting documentation) strengthens your case significantly and demonstrates the bureau’s failure to comply with the 30-day investigation requirement or its refusal to remove inaccurate information.

Final Thoughts

Pull your credit reports from Equifax, Experian, and TransUnion on a rotating schedule every four months through annualcreditreport.com so you catch errors before they damage your financial life. Review each report carefully for unfamiliar accounts, incorrect payment histories, or fraudulent entries. The moment you spot something wrong, document it and prepare to act-don’t wait for a denied loan or job rejection to discover problems that have been sitting on your file for months.

File your dispute in writing using certified mail with return receipt requested when you find inaccurate information. Include copies of supporting documents like bank statements, receipts, or creditor correspondence that prove the information is wrong, and the credit bureau must investigate within 30 days and respond with findings. If they refuse to correct it despite your evidence, add a personal statement to your file and escalate the dispute to the furnisher directly.

Persistent violations that bureaus refuse to fix often require professional assistance, and understanding what FCRA rights protect you means nothing without taking action when violations occur. Contact Hays Cauley, P.C. if disputes remain unresolved after you’ve exhausted the bureau’s investigation process, and we can help South Carolina residents enforce their FCRA rights when credit bureaus and furnishers violate the law.