How to Dispute Errors Under the Fair Credit Reporting Act in South Carolina

Credit report errors affect millions of Americans and can damage your financial future. These mistakes can lower your credit score, increase loan costs, and even prevent you from getting approved for housing or employment.

The Fair Credit Reporting Act gives you powerful tools to fight back against inaccurate information. We at Hays Cauley, P.C. help South Carolina consumers navigate the Fair Credit Reporting Act dispute process and restore their credit standing.

What Does the FCRA Actually Protect

The FCRA Creates Real Financial Protection

The Fair Credit Reporting Act forces credit bureaus to maintain accurate records about your financial history. This federal law requires Equifax, Experian, and TransUnion to investigate disputes within 30 days and correct proven errors. The Federal Trade Commission found that one in five consumers discovers errors on at least one credit report (making these protections essential for South Carolina residents).

Credit bureaus process hundreds of millions of transactions daily, which creates countless opportunities for mistakes. The FCRA gives you legal weapons to fight back when these errors damage your credit score. You can access free credit reports from each bureau annually and dispute any inaccuracies without fear of retaliation.

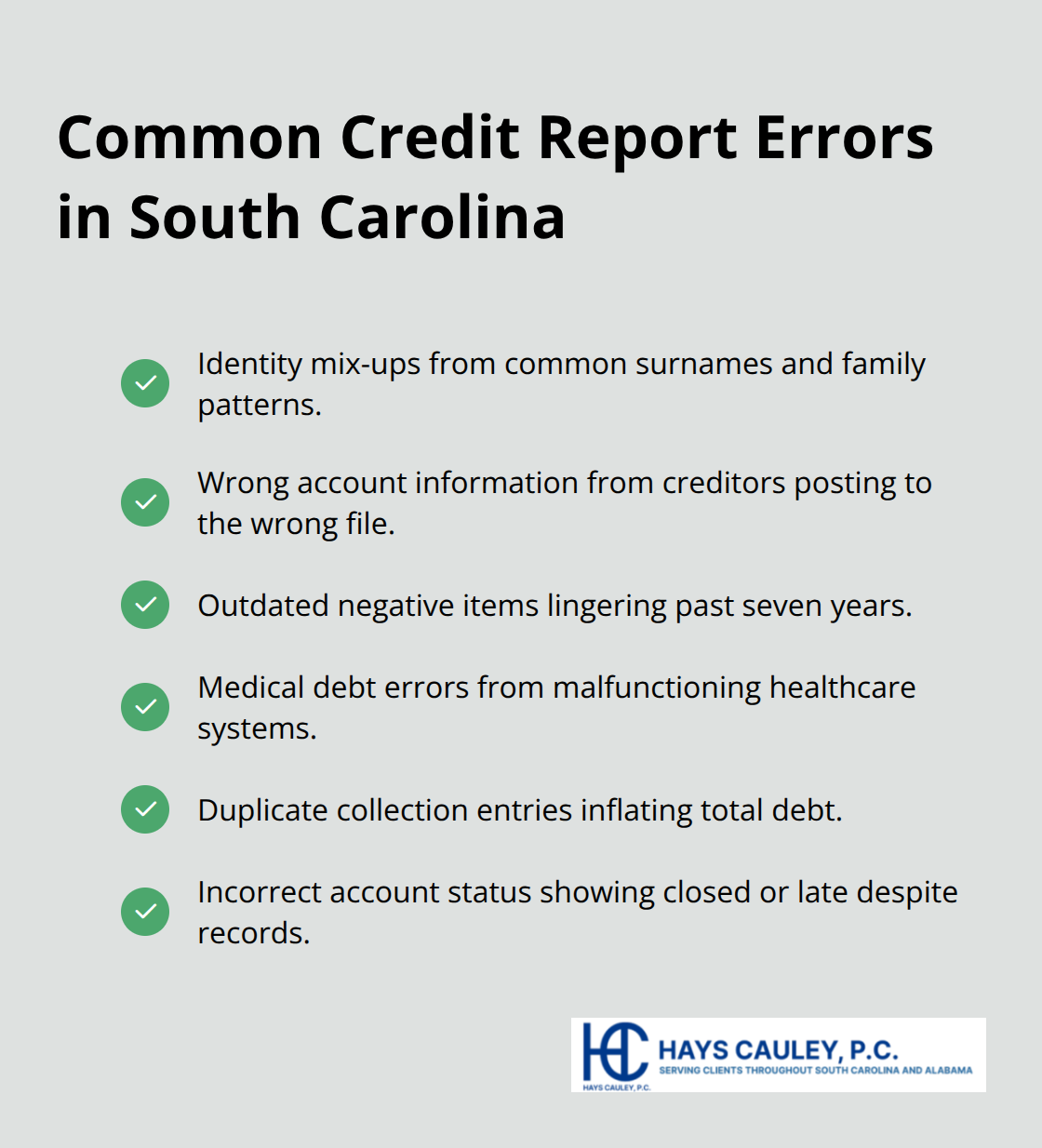

South Carolina Consumers Face These Specific Errors

Identity mix-ups plague South Carolina credit reports more than other states due to common surnames and family patterns. Wrong account information appears frequently when creditors report to the wrong person’s file. Outdated negative items that should have been removed after seven years continue to damage scores illegally.

Medical debt errors surge in rural South Carolina areas where healthcare systems often malfunction. Collection agencies frequently report the same debt multiple times, which artificially inflates your total debt load. Account status mistakes show current accounts as closed or payments as late when records prove otherwise.

Your Legal Rights Pack Real Power

The FCRA grants you the right to demand written proof of any negative item on your credit report. Credit bureaus must provide documentation that shows they verified disputed information with the original creditor. When they cannot produce this proof within 30 days, they must remove the disputed item completely.

You can recover actual damages plus attorney fees when credit bureaus willfully violate FCRA requirements. Negligent violations result in damages up to $1,000 per incident. The law also allows punitive damages up to $1,000 for each willful violation (creating real financial consequences for credit bureau misconduct).

Now that you understand your rights under the FCRA, the next step involves actually obtaining your credit reports and starting the dispute process.

How Do You Actually Start the Dispute Process

Get Your Reports From the Right Source

Visit annualcreditreport.com or call 1-877-322-8228 to obtain your free reports from all three bureaus. South Carolina consumers can access one free report from each bureau annually, but you should stagger these requests every four months to monitor changes continuously. The Consumer Financial Protection Bureau received over 175,000 credit reporting complaints in 2020 (which proves that regular monitoring catches problems before they escalate).

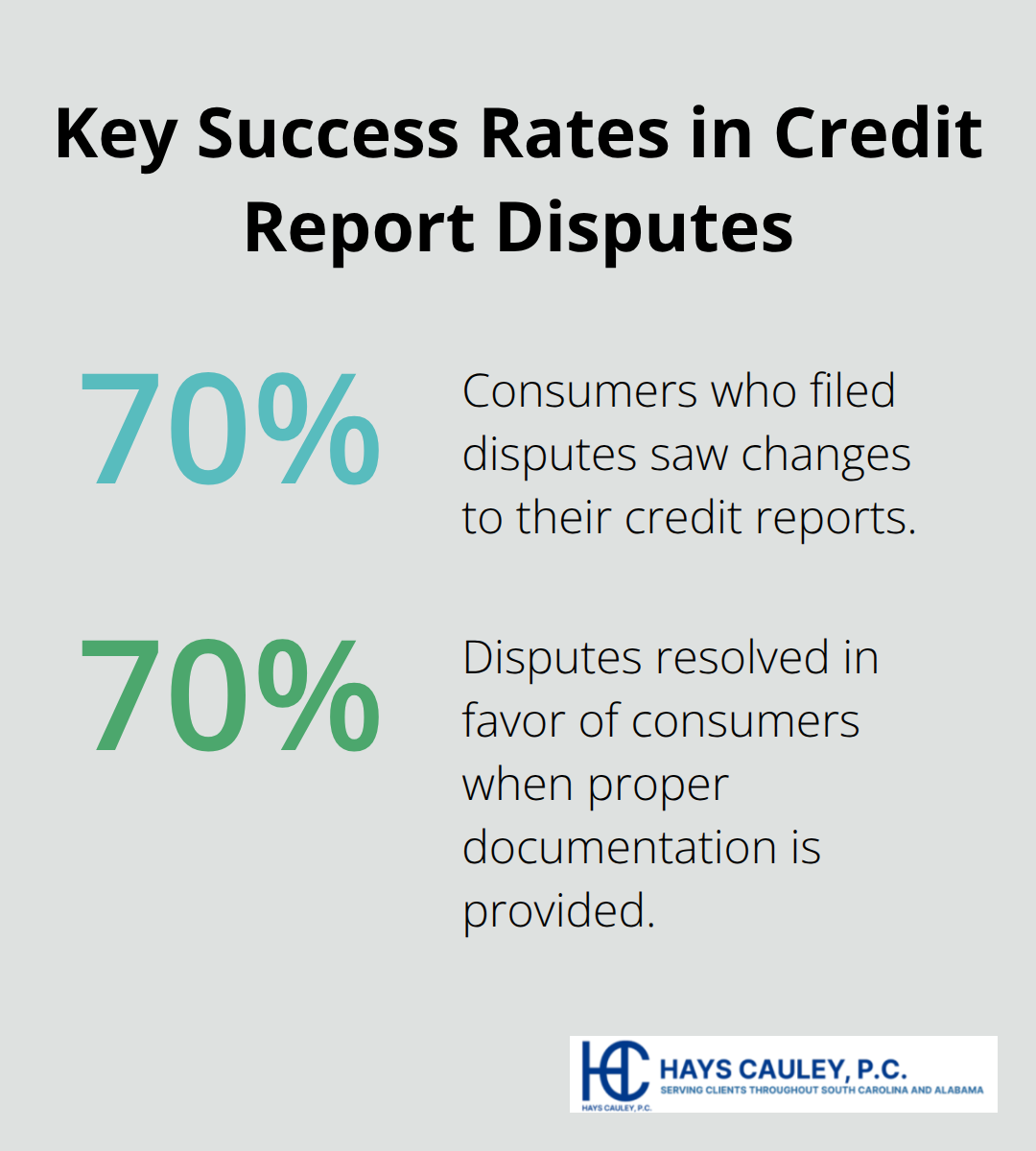

Skip third-party websites that charge fees or require credit card information. The Federal Trade Commission study showed that 70% of consumers who filed disputes experienced changes to their reports, which makes this free monitoring system your most valuable financial tool. Download and save PDF copies immediately since online access expires after a limited time.

File Your Dispute the Smart Way

Send disputes via certified mail with return receipt requested to create legal proof of delivery. Include your full name, address, Social Security number, and detailed explanation of each error with supporting documentation. Credit bureaus must investigate within 30 days, but they often ignore online disputes or claim they never received phone complaints.

Attach bank statements, payment receipts, court documents, or correspondence that proves the disputed information is wrong. The Consumer Financial Protection Bureau provides template letters that strengthen your dispute submissions significantly. Document every communication attempt because credit bureaus frequently violate the 30-day investigation requirement (and your records become evidence in potential legal action).

Build Your Evidence File Now

Collect proof before you file disputes because credit bureaus will demand verification of your claims. Payment histories from your bank, settlement letters from creditors, and identity theft reports from police create unshakeable evidence. Medical debt disputes require insurance explanation of benefits statements and provider billing records that show the actual responsible party.

Keep detailed logs of all dispute communications including dates, times, reference numbers, and representative names. Credit bureaus often claim they corrected errors when they actually ignored your dispute entirely. Your documentation proves their violations and strengthens any legal action needed to force compliance with FCRA requirements.

Once you submit your dispute with proper documentation, the credit bureaus must begin their investigation process within specific legal timeframes.

What Happens During the Credit Bureau Investigation

The 30-Day Investigation Clock Starts Now

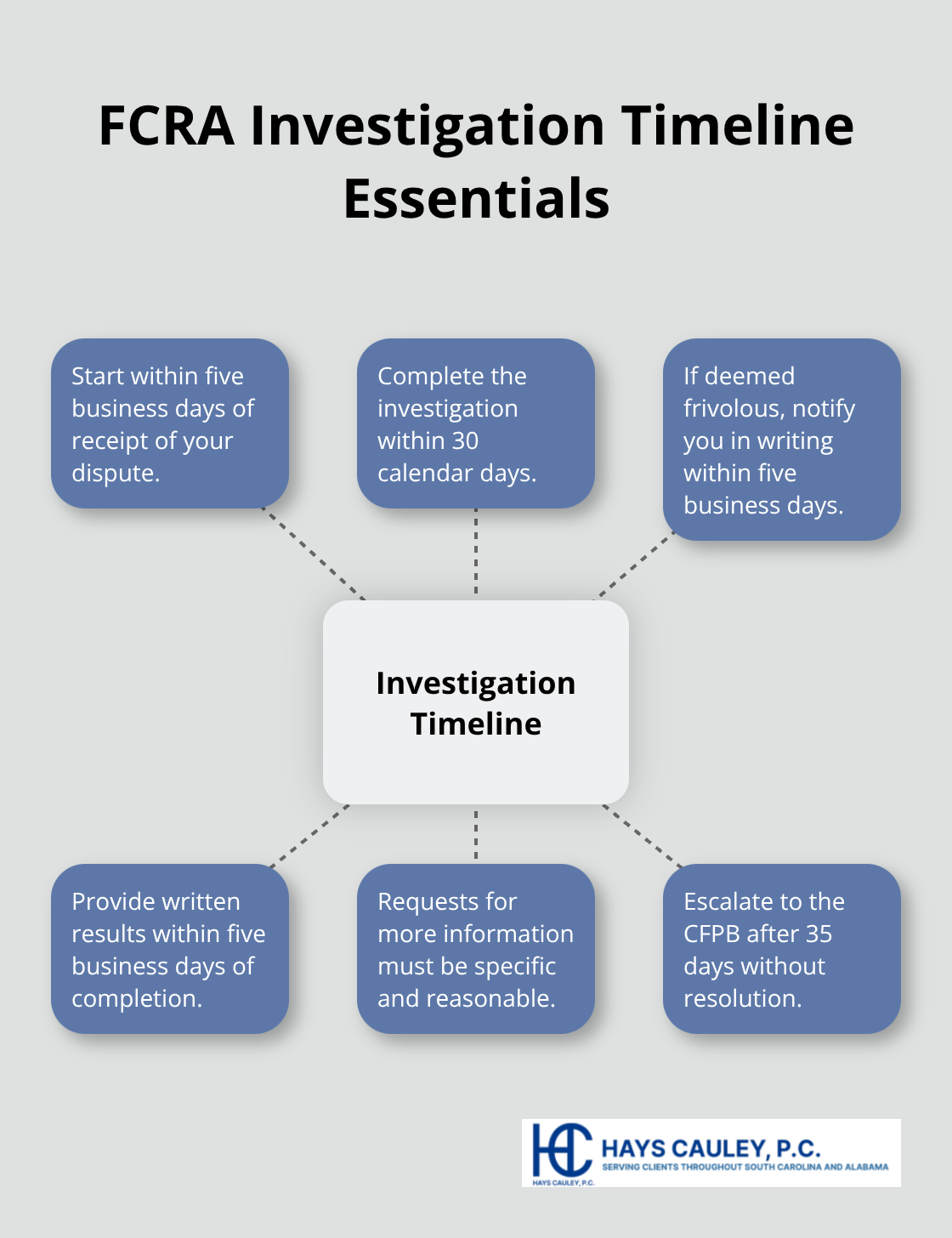

Credit bureaus must begin investigation of your dispute within five business days of receipt and complete the process within 30 calendar days. They contact the data furnisher (your creditor or collection agency) to verify the disputed information. The Federal Trade Commission found that credit bureaus resolve disputes in favor of consumers 70% of the time when proper documentation is provided. However, many investigations consist of nothing more than automated queries that rubber-stamp the original information without human review.

Credit bureaus often claim they need additional time or information to delay the investigation process illegally. They must notify you in writing if they determine your dispute is frivolous or irrelevant within five business days. Any request for more information must be specific and reasonable. The Consumer Financial Protection Bureau reports that credit bureaus frequently violate these timelines (especially during peak dispute periods between January and April when consumers receive tax refunds and focus on financial cleanup).

Track Your Dispute Progress Aggressively

Contact the credit bureau by phone every 10 days to check your dispute status and document each conversation with names, dates, and reference numbers. Credit bureaus must provide written results of their investigation within five business days of completion. Demand specific details about what steps they took to verify the disputed information and which documents they reviewed. Many credit bureaus provide vague responses that fail to explain their investigation methods or findings.

South Carolina consumers should immediately escalate unresolved disputes to the Consumer Financial Protection Bureau after 35 days without resolution. The CFPB received over 175,000 credit reporting complaints in 2020, with investigation delays representing the most common violation. File your complaint online at consumerfinance.gov and reference your original dispute documentation. Credit bureaus respond much faster to CFPB complaints because these violations can result in federal enforcement actions and substantial penalties.

Credit Bureau Investigation Failures Create Legal Opportunities

Credit bureaus violate FCRA requirements when they fail to conduct reasonable investigations or ignore clear evidence of errors. They cannot simply forward your dispute to the data furnisher and accept whatever response they receive. The law requires them to review all relevant information and make independent determinations about accuracy. When credit bureaus fail to remove obviously incorrect information after proper disputes, they face liability for actual damages plus attorney fees up to $1,000 per violation (making legal action a viable option for South Carolina consumers).

Final Thoughts

Credit bureaus that ignore valid disputes or conduct sham investigations face serious legal consequences under the Fair Credit Reporting Act. When they fail to remove obviously incorrect information after 30 days, you can recover actual damages plus attorney fees. South Carolina consumers who document credit bureau violations properly often receive settlements that exceed the financial harm the errors caused.

Consumer protection attorneys understand the complex requirements that credit bureaus must follow during Fair Credit Reporting Act dispute investigations. They know when credit bureaus violate federal law by conducting inadequate investigations or ignoring clear evidence of errors. Legal representation becomes necessary when credit bureaus repeatedly refuse to correct documented mistakes that damage your credit score and financial opportunities.

We at Hays Cauley, P.C. help South Carolina consumers hold credit bureaus accountable for FCRA violations and restore accurate credit reports. Our consumer protection law firm handles credit reports, identity theft, and debt-related issues that affect your financial future. Taking control of your credit report accuracy requires persistence, proper documentation, and legal action when credit bureaus fail to follow federal law (especially after multiple fair credit reporting act dispute attempts).