Your credit report directly affects your ability to borrow money, rent an apartment, or even get hired for certain jobs. A single error on your report can cost you thousands in higher interest rates or denied applications.

We at Hays Cauley, P.C. help South Carolina residents fix SC credit report issues every day. This guide walks you through reviewing your report, disputing errors, and rebuilding your score with concrete steps you can take right now.

What’s Actually on Your Credit Report

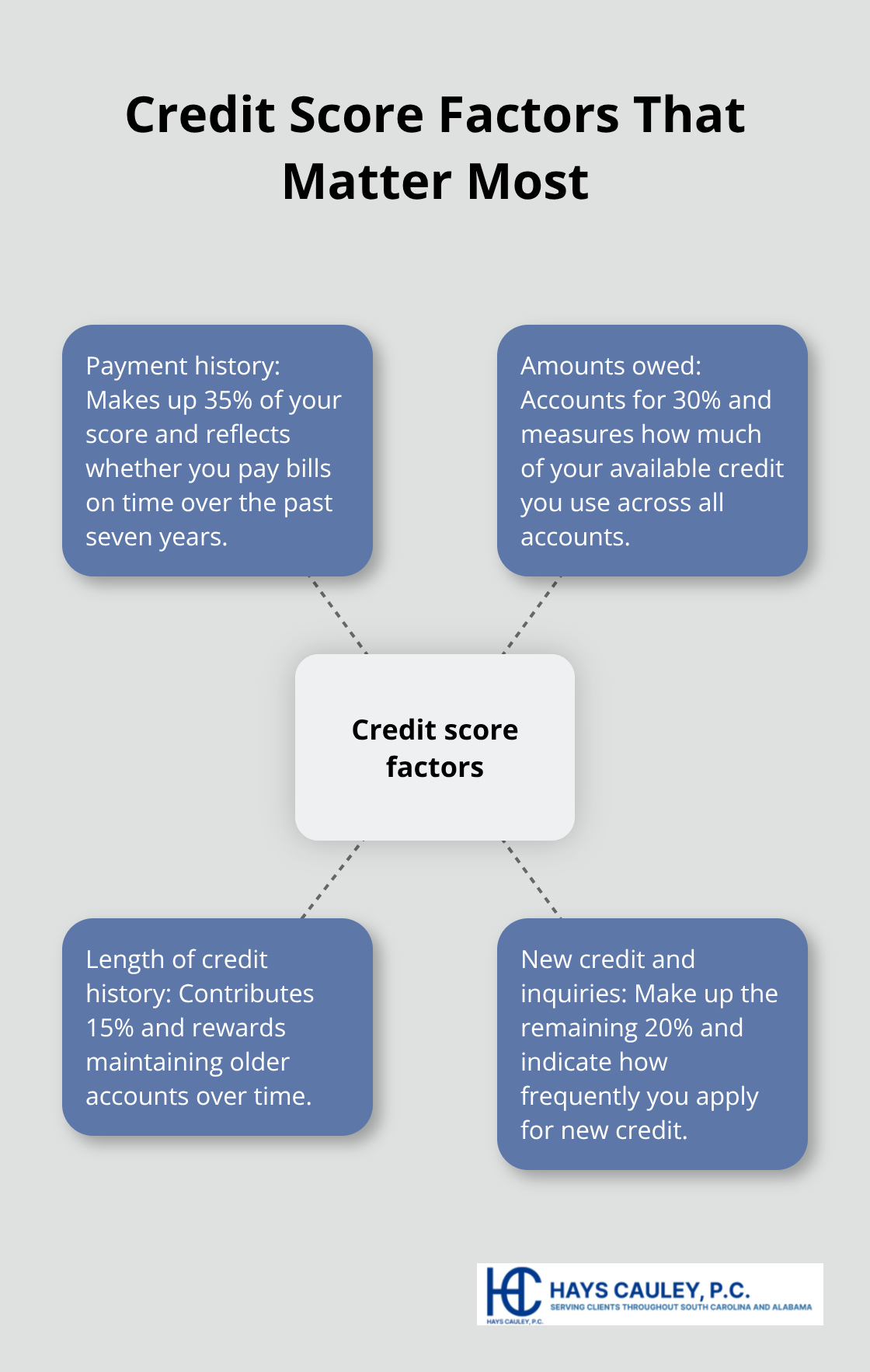

Your credit report contains four categories of information that lenders, landlords, and employers review. Payment history makes up 35 percent of your credit score and shows whether you paid bills on time over the past seven years. Amounts owed accounts for 30 percent and reflects how much of your available credit you use across all accounts. Length of credit history contributes 15 percent and rewards you for maintaining older accounts.

Recent inquiries and new credit account for the remaining 20 percent and show how often you apply for new credit recently.

The three major bureaus-Equifax, Experian, and TransUnion-collect this data from creditors, lenders, and public records, but they often receive conflicting or incomplete information from these sources. This is why your reports can differ significantly across the three agencies. In South Carolina, 79 percent of credit reports contain errors according to data cited by the South Carolina Department of Consumer Affairs, meaning the information lenders see about you is frequently wrong.

How Errors Slip Into Your Credit File

The bureaus don’t verify information before adding it to your report. A creditor reports a late payment, a collection agency lists a debt under your name, or a duplicate account appears-and the bureaus accept it without confirmation. You won’t see these errors unless you actively pull your reports and review them line by line. Most people check their credit only when applying for a loan, which means errors can persist for months or years before discovery.

The Real Cost of Inaccurate Information

A single error on your credit report can lower your score by 100 points or more, which translates directly into higher interest rates on mortgages, auto loans, and credit cards. Someone in South Carolina with a credit score below 700 (which describes 44.3 percent of the state’s population) already faces significantly higher borrowing costs and frequent loan denials. An inaccurate late payment, a duplicate account, or a debt that doesn’t belong to you compounds this problem and makes your financial situation appear worse than it actually is.

Lenders make split-second decisions based on your score and won’t dig deeper to verify accuracy. The damage extends beyond lending: landlords use credit reports to screen tenants, and some employers pull reports for hiring decisions. If your report contains false information, you won’t know it’s costing you opportunities unless you actively review your reports.

What Happens When You Take Action

Disputing errors removes inaccurate information and restores your true financial picture to lenders. The process is free, and both the credit bureaus and the companies that reported the information must correct inaccurate or incomplete data. Once errors are removed, your score can improve significantly within weeks or months, depending on how many items you dispute and how quickly the bureaus process your requests.

The first step is obtaining your actual credit reports from all three bureaus so you can identify what needs correction.

Review Your Credit Reports and File Disputes

Access Your Free Credit Reports

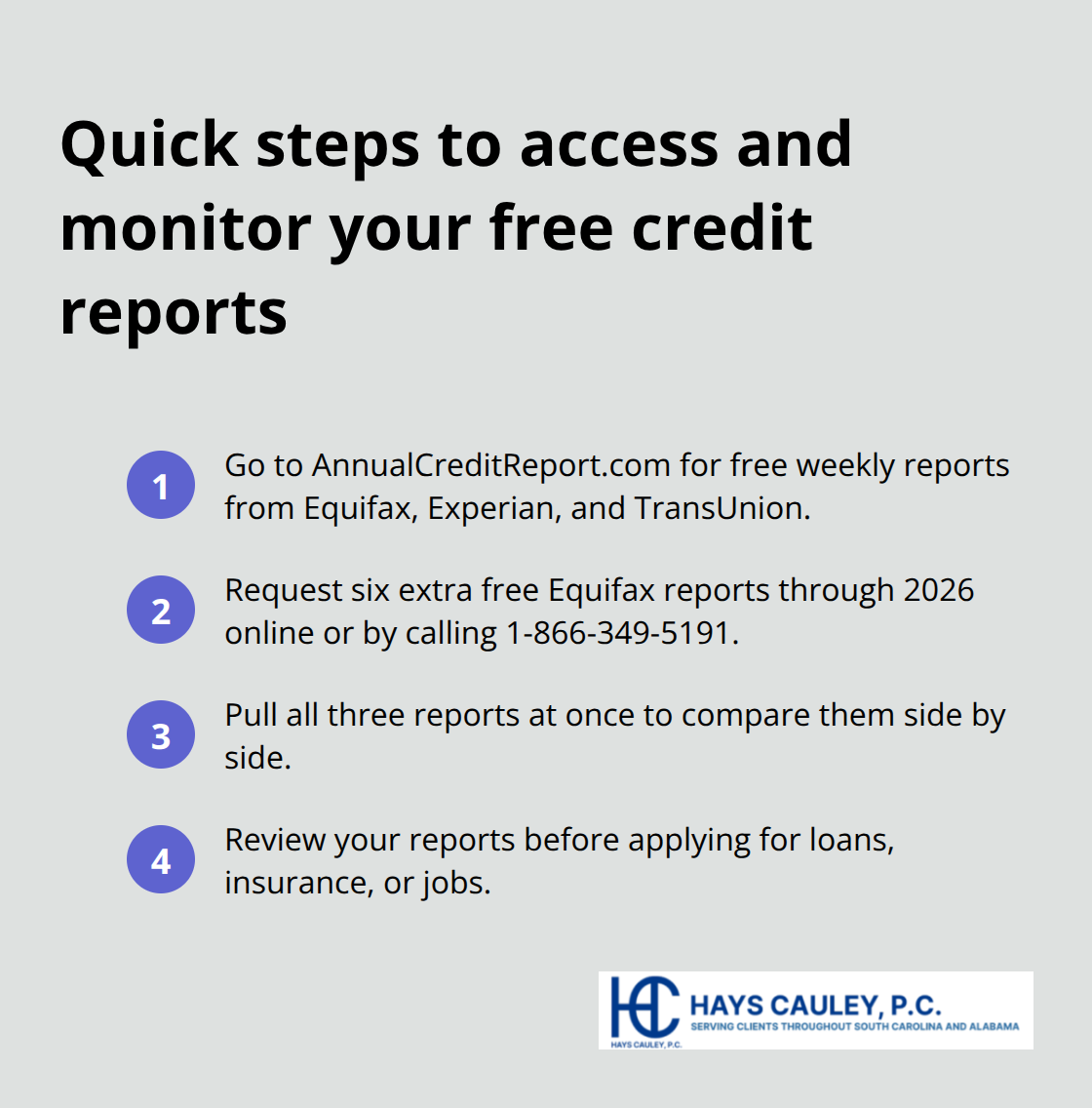

You have permanent access to free credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com, the only site authorized by federal law to provide them. The three major agencies now offer free weekly reports as part of a permanent program, giving you the ability to monitor your credit multiple times per year instead of waiting until a problem surfaces. Additionally, through 2026, Equifax provides six extra free reports annually if you visit their website or call 1-866-349-5191. This means you have no excuse to skip reviewing your reports regularly.

Pull all three reports at once so you can compare them side by side, since each bureau may contain different information pulled from different data sources. The South Carolina Department of Consumer Affairs urges residents to review their reports at least once annually before applying for loans, insurance, or jobs.

Identify Errors on Your Report

Start your review by checking for unfamiliar accounts, incorrect personal information, duplicate entries, and late payments you know you didn’t make. Circle or highlight each error directly on the printed or saved report so you have visual documentation of what needs correction. Most people check their credit only when applying for a loan, which means errors can persist for months or years before discovery.

A single error on your credit report can lower your score by 100 points or more. Someone in South Carolina with a credit score below 700 (which describes 44.3 percent of the state’s population) already faces significantly higher borrowing costs and frequent loan denials. An inaccurate late payment, a duplicate account, or a debt that doesn’t belong to you compounds this problem and makes your financial situation appear worse than it actually is.

Send Written Disputes to Bureaus and Furnishers

Once you identify errors, send written disputes to each affected credit bureau and to the company that reported the inaccurate information. Address your dispute letter to the bureau with your full contact information, the account number of the disputed item, a clear explanation of why the information is wrong, and copies of supporting documents. The Fair Credit Reporting Act requires credit bureaus to investigate disputes within 30 days and furnishers (creditors, collection agencies, etc.) to respond within about 30 days as well.

Send disputes by certified mail with return receipt so you have proof of delivery. Keep copies of every letter, document, and mailing receipt in a personal dispute file. If a bureau declares your dispute frivolous, they must notify you within five business days with their reasoning.

Track Corrections and Enforce Your Rights

If the furnisher corrects information after your dispute, they must notify the bureaus so your reports update automatically. After resolution, inaccurate information must be removed from your report, and if harmful information isn’t corrected within ten days after judgment, South Carolina law allows damages up to one thousand dollars per day until removal occurs. The process is free and you can manage it yourself.

However, complex disputes or situations where bureaus or furnishers fail to correct errors may require legal assistance. We at Hays Cauley, P.C. help South Carolina residents navigate these situations and enforce their rights when the standard dispute process stalls. Once your errors are removed and your score begins to improve, the next step involves taking active measures to rebuild your credit through consistent payment behavior and strategic debt reduction.

Rebuild Your Credit Score Faster Than You Think

Errors removed from your report restore accuracy, but your score won’t climb significantly until you change the behaviors that damaged it. Payment history accounts for 35 percent of your credit score, and this is where you gain the most control. Missing even one payment tanks your score, while 30 consecutive on-time payments can lift it substantially. The Federal Trade Commission notes that improving your credit takes time, but the timeline depends entirely on your actions starting today.

Reduce Credit Card Balances Immediately

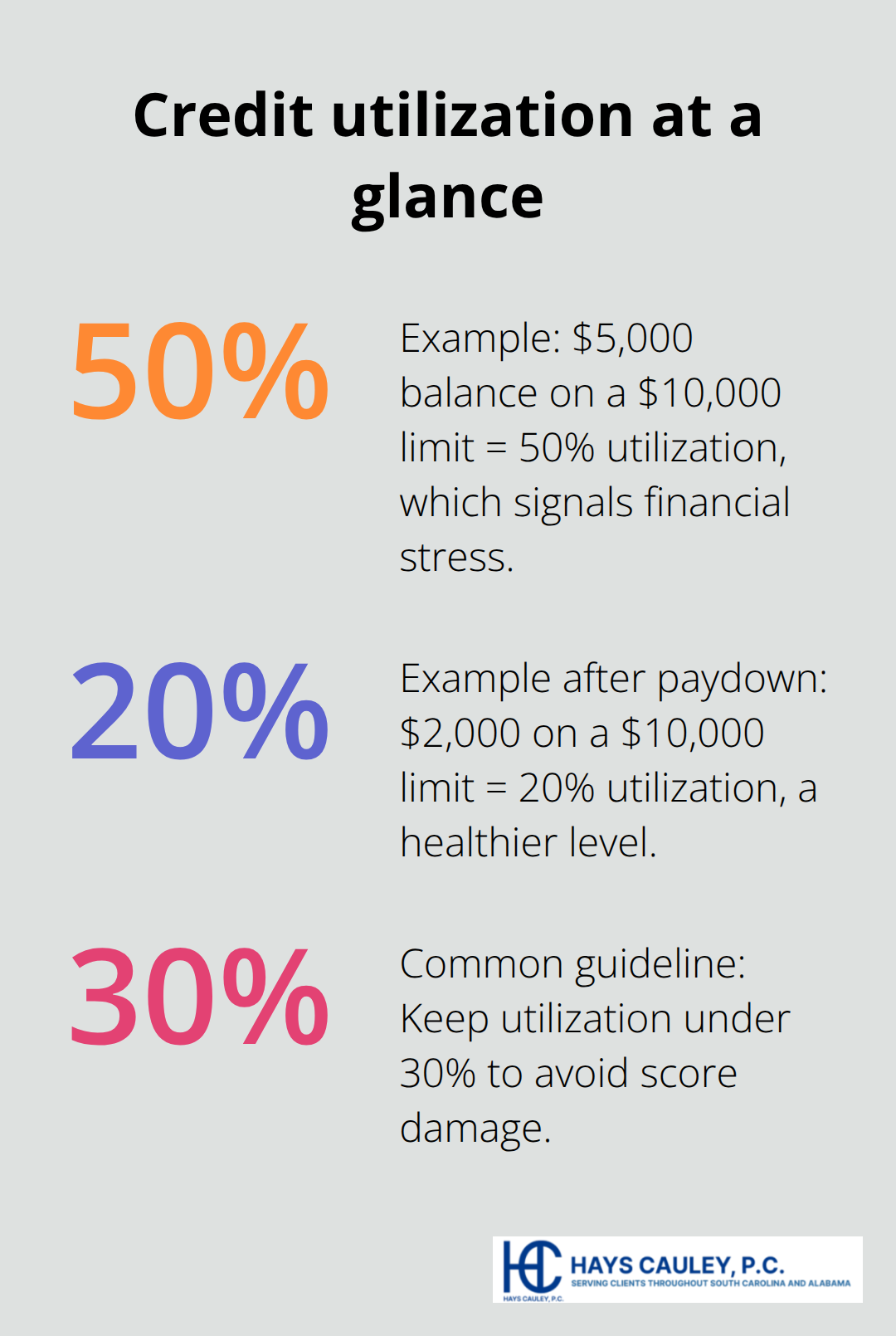

If you currently carry balances on credit cards, reduce them now because amounts owed accounts for 30 percent of your score. Someone with a credit card balance of $5,000 on a $10,000 limit has a 50 percent utilization ratio, which signals financial stress to lenders and damages your score significantly. Dropping that same balance to $2,000 cuts utilization to 20 percent and can improve your score by dozens of points within weeks once the credit bureaus receive the updated information from your card issuer.

This works because credit utilization has an immediate impact, unlike payment history which requires months of perfect behavior to show meaningful gains. Focus on paying down high-balance cards first, especially those with utilization above 30 percent. Even small reductions in your balances produce measurable score improvements.

Handle Collections and Charged-Off Debts Strategically

Collections accounts and charged-off debts represent the most serious damage on any credit report, yet most South Carolina residents don’t understand how to handle them strategically. A collection account stays on your report for seven years from the original delinquency date, not from when the collection agency purchased the debt, which means you cannot erase it early through payment alone. However, paying a collection account in full stops the collection agency from pursuing further action and removes a major barrier to future lending.

The Federal Trade Commission warns against paying collections without first getting a written agreement because some creditors will report the account as paid but leave the negative mark intact. Negotiate with the collection agency in writing before sending payment, requesting that they remove the account entirely or report it as paid in full. Late payments older than two years carry far less weight than recent delinquencies, so if you have multiple negative items, focus your immediate effort on preventing new late payments rather than obsessing over aged accounts that will naturally age off your report within a few years.

Establish On-Time Payment Patterns

Payment history requires consistent action over months to show meaningful improvement. Set up automatic payments for all bills so you never miss a due date, even if the amount is small. One missed payment can lower your score by 100 points or more, while one on-time payment begins rebuilding trust with lenders. The impact compounds: after six months of perfect payments, lenders view you as lower risk, and after 12 months, the improvement becomes substantial.

If you struggle with multiple bills, consider consolidating debt or working with a credit counselor to create a manageable payment plan. The key is consistency-lenders reward those who pay reliably over time.

Final Thoughts

Fixing your SC credit report requires three concrete actions: obtain your reports from all three bureaus, dispute inaccurate information in writing, and establish consistent on-time payment behavior. The process costs nothing and remains entirely within your control. Errors disappear once you challenge them, your score improves as you reduce debt and pay bills on time, and your financial opportunities expand as your creditworthiness increases.

Some situations demand legal assistance when credit bureaus or furnishers ignore your disputes, continue reporting inaccurate information after you provide documentation, or refuse to correct errors that violate South Carolina law. Willful violations of state credit protections carry damages up to three times your actual losses or $3,000 per incident, plus attorney fees. If inaccurate information harms your creditworthiness and isn’t corrected within ten days after judgment, South Carolina law allows additional damages of up to $1,000 per day until removal.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, enforce their credit reporting rights when the standard dispute process fails. Pull your free reports from AnnualCreditReport.com today, identify errors, and send your first dispute letters this week.