A mistake on your credit report can tank your score and cost you thousands in higher interest rates. At Hays Cauley, P.C., we help South Carolina residents, including those in Greenville, Columbia, and Charleston, correct credit report mistakes that shouldn’t be there.

The good news is that fixing these errors is faster than most people think. We’ll walk you through exactly how to identify problems, challenge them, and rebuild your credit.

Why Credit Report Errors Happen More Often Than You Think

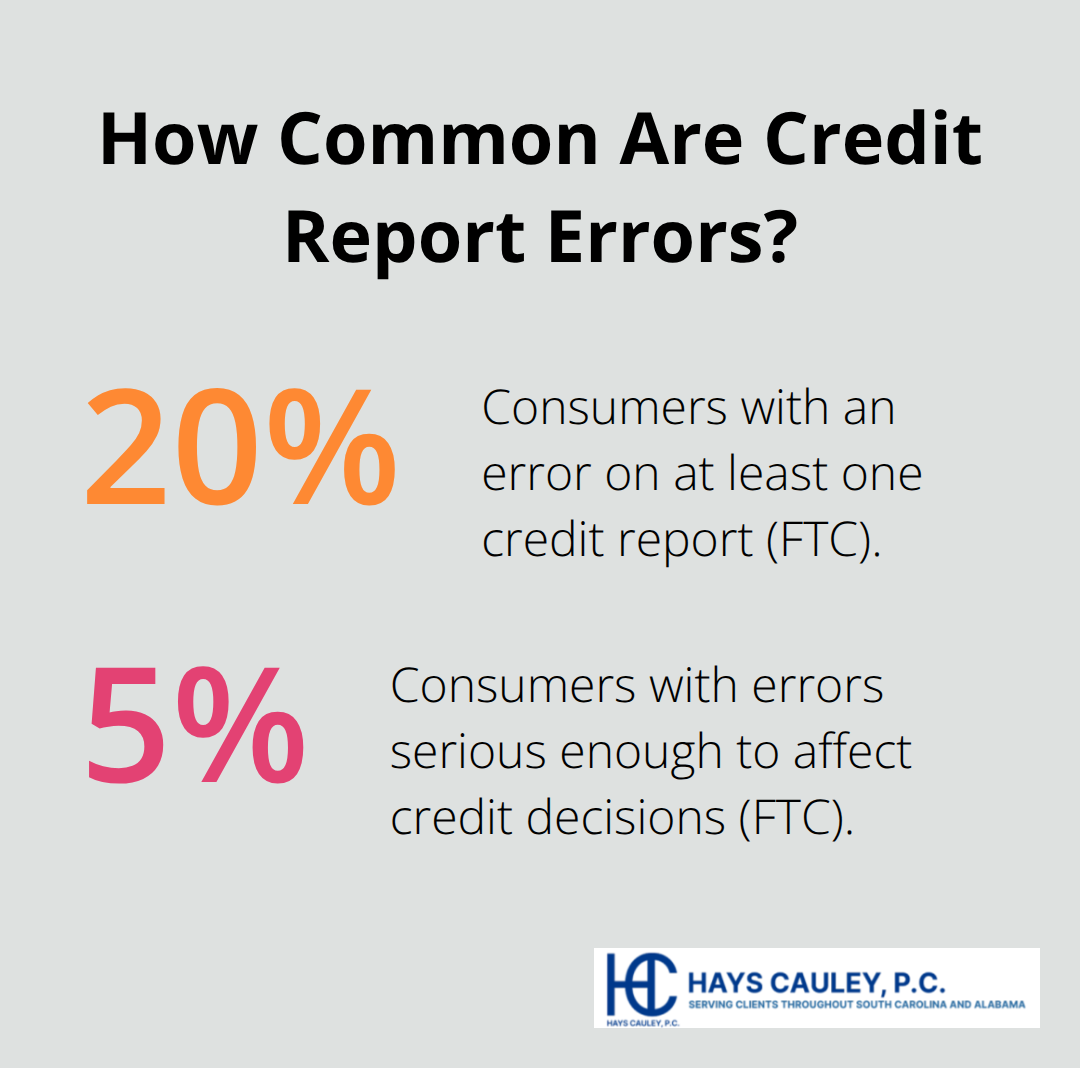

Credit report errors aren’t rare accidents. The Federal Trade Commission reports that one in five consumers has an error on at least one of their three credit reports, and roughly one in twenty has errors serious enough to affect their credit decisions. These mistakes fall into three main categories that you need to understand to protect yourself.

Personal Information Errors Create Confusion Across Systems

Personal information errors occur when bureaus mix up names, addresses, or Social Security numbers. Creditors report data inconsistently, and someone with a similar name can have their account attached to your file. Data flows through multiple systems with different formatting standards, and manual entry errors compound the problem. Creditors often use shorthand or abbreviations that don’t match what the bureaus expect, causing accounts to attach to the wrong file. The result is that you might see accounts you never opened, or your legitimate accounts get lost in someone else’s credit history. Checking your reports regularly is the only way to catch these before they tank your score.

Fraudulent Accounts and Identity Theft Damage Your Credit Instantly

If you spot accounts you don’t recognize, act immediately. Fraudulent accounts damage your credit instantly and can lead to collection calls for debts you never incurred. In 2023, the FTC received over 2.6 million identity theft reports, with credit card fraud and new account fraud leading the way. Report identity theft to receive a personalized recovery plan and dispute the fraudulent accounts directly with each bureau using their contact information and supporting documentation proving the account isn’t yours.

Creditor Reporting Errors Inflate Your Debt and Raise Interest Rates

Collection agencies and creditors frequently report inaccurate payment histories or fail to remove accounts after they’ve been paid off. Some report the same debt multiple times under different collection agencies, inflating your debt load on paper. Others report accounts as late when you paid on time, or they continue reporting accounts years after you settled them. These errors directly raise your interest rates on mortgages, auto loans, and credit cards, costing you hundreds or thousands over the life of a loan. What makes this worse is that negative information stays on your report for seven years, meaning one error can damage your finances for years if left uncorrected.

Now that you understand how these errors happen, the next step is learning exactly how to identify them in your own reports and challenge them effectively.

How to Find and Fix Errors on Your Credit Report, Serving South Carolina, Including Greenville, Columbia and Charleston

Pull Your Free Credit Reports from All Three Bureaus

Visit AnnualCreditReport.com or call 877-322-8228 to request reports from Equifax, Experian, and TransUnion. The program is permanently extended, meaning you can check each bureau’s report for free once per week. Most people only pull reports when applying for a loan, but that’s backwards-you should monitor them regularly to catch errors before they damage your finances. Stagger your requests across the three bureaus rather than pulling all at once. This gives you a rolling view of your credit file throughout the year and makes it easier to spot when new errors appear.

Review Your Reports Line by Line for Inaccurate Information

When your reports arrive, print them out and grab a highlighter. Don’t just skim them. Go line by line through every account, payment history entry, and personal detail. Look for accounts you don’t recognize, payment statuses that don’t match your records, duplicate listings of the same debt, incorrect balances, wrong personal information like addresses or phone numbers, and accounts that should have been closed years ago. Many people miss errors because they assume the bureaus got it right. They didn’t. According to the FTC, roughly one in twenty consumers has errors serious enough to affect their credit decisions, and most of those errors go undetected for months or years.

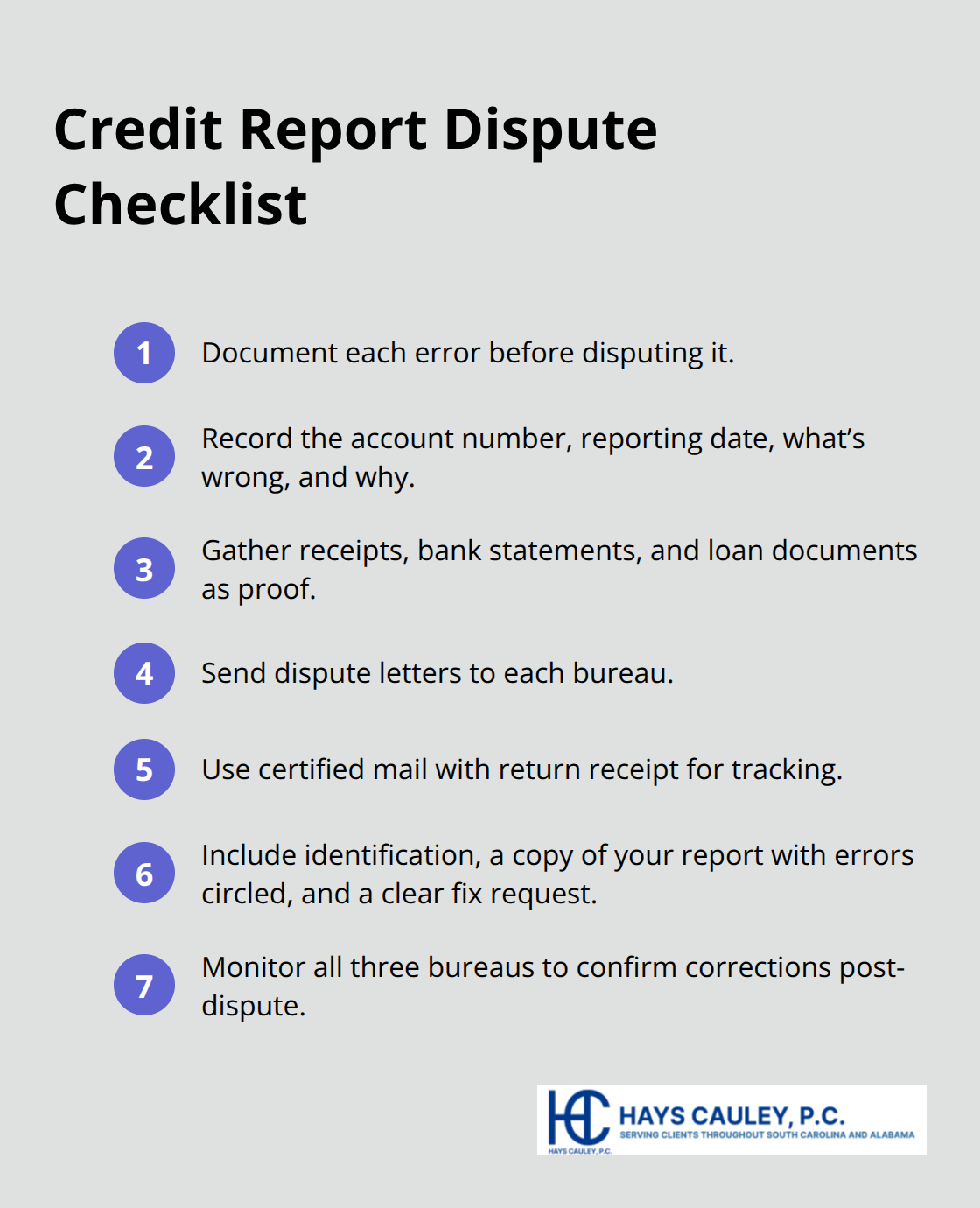

Document Your Errors and Gather Supporting Evidence

Once you find an error, document it thoroughly before you dispute it. Write down the account number, the reporting date, what’s wrong, and why it’s wrong. Collect supporting evidence-payment receipts, bank statements, loan documents, anything that proves the error.

Then send dispute letters to each bureau reporting the error. Use certified mail with return receipt so you have proof they received it. Include your full name and address, the specific item you’re disputing and why, copies of your supporting documents, a copy of your credit report with the error circled, and a clear explanation of what needs to be corrected.

File Disputes with Both the Bureau and the Creditor

Send the same documentation to the creditor or collection agency that reported the inaccurate information. The bureaus must investigate within 30 days and notify you of the results. If they find the information is inaccurate, both the bureau and the business that reported it must correct or delete it across all three bureaus. If the investigation doesn’t resolve your dispute, you can add a statement to your file explaining your position, and future reports will include that statement. After the dispute closes, monitor your reports again to confirm the error was actually removed and that any dispute notices appear correctly.

Once you’ve corrected the errors on your report, the real work begins-rebuilding your credit score and establishing the financial habits that prevent future damage.

Rebuild Your Credit After Errors Are Removed

Removing errors from your credit report is only half the battle. The real damage control happens in the months after corrections take effect, when you actively rebuild what those mistakes damaged. Your credit score does not instantly recover just because an error vanishes. According to the FTC, paying bills on time and reducing debt are the two most effective ways to improve your score, but the timing matters more than most people realize.

Start with On-Time Payments Immediately

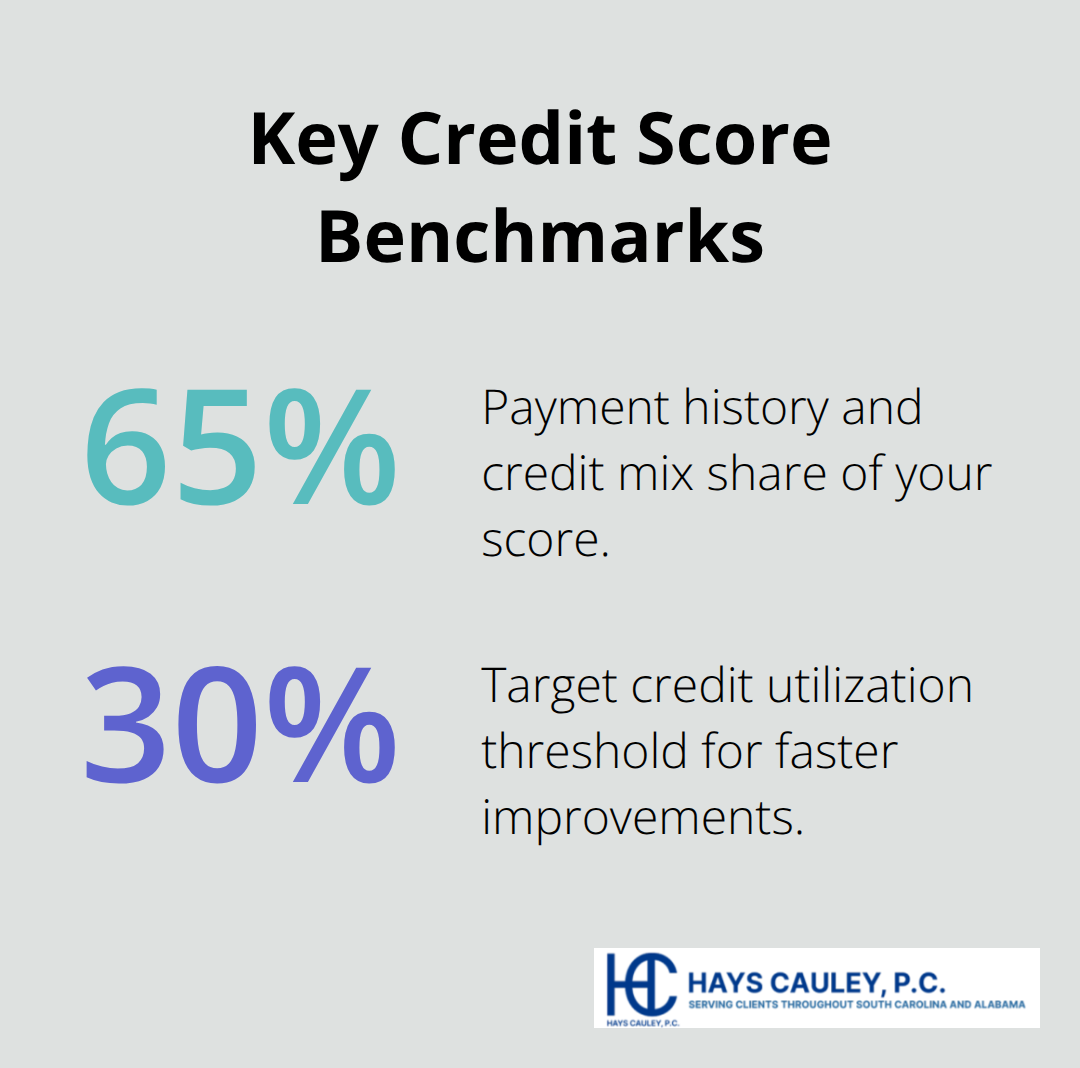

Start making on-time payments immediately, even while disputes are pending, because every month of clean payment history strengthens your file. Each on-time payment signals to lenders that you handle credit responsibly, and this matters far more than most people understand. Your credit mix and payment history make up 65 percent of your score, so having no active accounts is worse than having accounts you manage responsibly.

If you have been avoiding credit cards because of past errors, that approach actually hurts you now.

Use Secured Credit Cards to Rebuild Trust

Open a secured credit card if traditional cards will not approve you yet. Secured cards require a cash deposit that becomes your credit limit, typically ranging from $200 to $2,500. Capital One, Discover, and other major issuers offer secured cards with no annual fee, and they report to all three bureaus just like regular cards. Use the card for small purchases you would normally make anyway, then pay the full balance every month. This demonstrates you can handle credit responsibly without carrying balances that damage your score.

Monitor Your Score and Reduce Credit Utilization

Check your credit score monthly, not just when applying for loans. Free tools like Credit Karma and Experian’s free monitoring service show your score and flag changes so you catch problems before they worsen. Your score typically improves 20 to 50 points per month once you start paying on time, but jumps of 100 points happen within six months if you also reduce credit card balances below 30 percent of your limits. If a card has a $5,000 limit, try keeping your balance under $1,500. This single action often produces faster score improvements than anything else because credit utilization directly impacts your score calculation.

Avoid New Credit Applications and Negotiate Settlements

Stop applying for new credit while rebuilding. Each application generates a hard inquiry that temporarily lowers your score by a few points. Multiple inquiries within 45 days count as one for mortgage and auto loan purposes, but they still damage your score individually. Wait at least six months after corrections before applying for major loans. If you are currently carrying high-interest debt from collection accounts or old creditors, negotiate payoff amounts before they are removed from your report. Paying a collection account in full looks better than paying a settlement, but even settlements show better than unpaid debts. Once an account is paid and removed, your score jumps because the negative weight disappears entirely.

Final Thoughts

Correcting credit report mistakes directly affects your ability to borrow money, qualify for insurance, rent a home, and secure employment that requires credit checks. When errors vanish from your report, lenders view you as lower risk, which translates to lower interest rates on mortgages, auto loans, and credit cards. Over a 30-year mortgage, removing errors that cost you an extra 1 to 2 percent in interest can save you tens of thousands of dollars.

Most credit report errors resolve through the dispute process outlined in this guide, with bureaus investigating within 30 days and correcting inaccurate information. However, some situations demand stronger action-if a bureau ignores your dispute, continues reporting inaccurate information after you’ve provided evidence, or fails to investigate properly, you may have legal grounds under the Fair Credit Reporting Act. Damages can include compensation for lost credit opportunities, emotional distress, and attorney fees, with South Carolina law potentially providing additional remedies beyond federal protections.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, when credit reporting disputes stall or serious errors cost you money. Contact us for a confidential consultation about your options to correct credit report mistakes and protect your financial future.