Your credit score affects everything from mortgage approval to interest rates on loans. At Hays Cauley, P.C., we’ve helped many Charleston residents understand that Charleston SC credit repair isn’t complicated-it starts with knowing what’s on your report.

This guide walks you through the practical steps to fix credit problems, access local resources, and rebuild your financial foundation.

What Your Credit Score Actually Means in Charleston, SC – Serving South Carolina, including Greenville, Columbia and Charleston

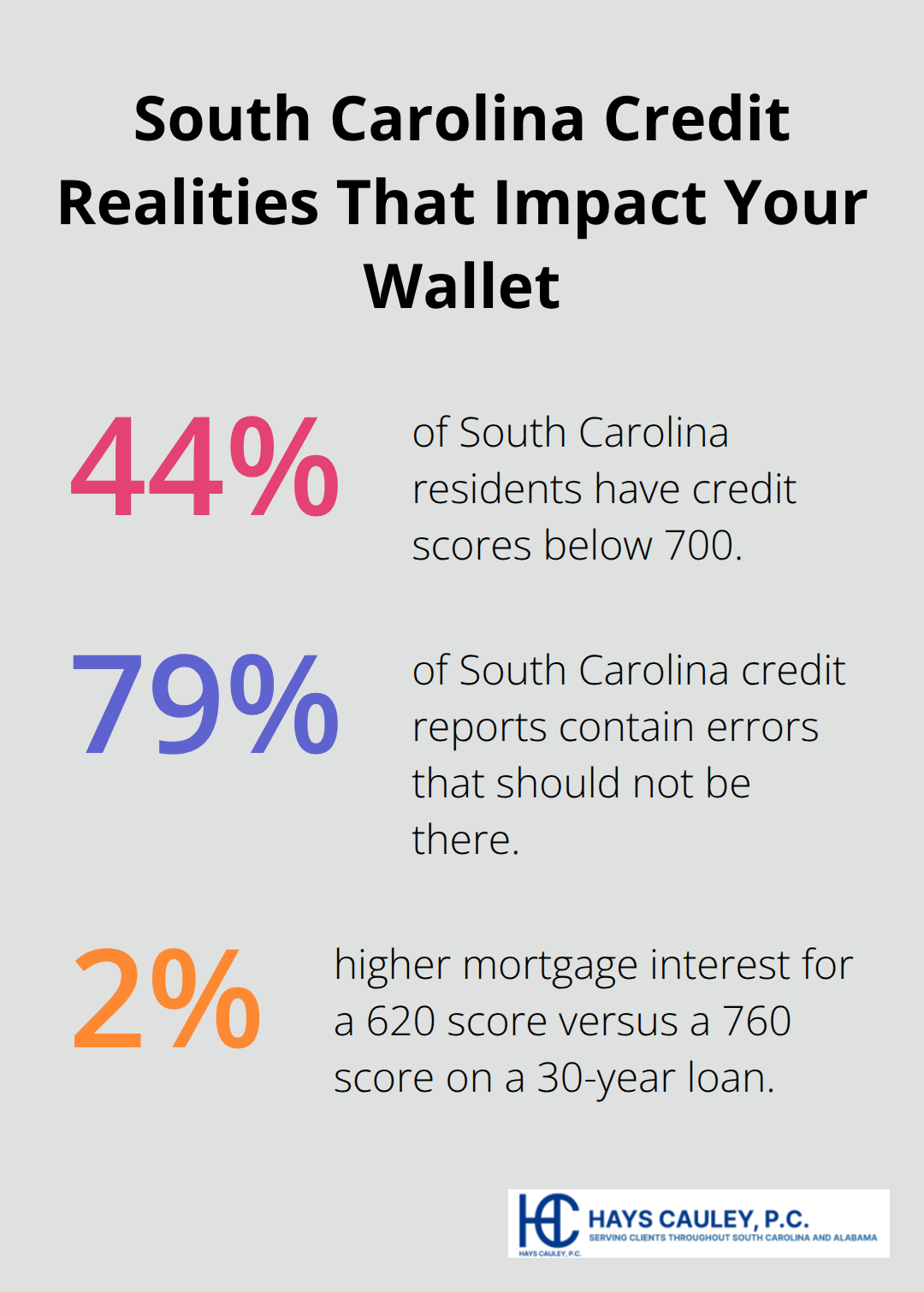

Your credit score is a three-digit number that lenders use to decide whether to loan you money and at what interest rate. The FICO scoring model, which most lenders rely on, ranges from 300 to 850, and payment history accounts for 35 percent of your score according to FICO. This single factor matters more than anything else, which means one late payment can damage your score for years. In South Carolina, 44.3 percent of residents have credit scores below 700, and 79 percent of South Carolina credit reports contain errors that shouldn’t be there at all. These errors cost you real money.

A borrower with a 620 credit score pays roughly 2 percent more in interest on a 30-year mortgage than someone with a 760 score, which translates to tens of thousands of dollars over the life of the loan.

How Lenders Evaluate Your Report

When you apply for a mortgage in Charleston, lenders pull your credit report from Experian, Equifax, and TransUnion to verify your creditworthiness. If errors exist on any of these reports, your score suffers unfairly, and you’ll face denial for better interest rates or rejection entirely. The average South Carolina resident carries roughly 5,700 dollars in debt, and most people have no plan to address it.

The Five Factors That Shape Your Score

Credit utilization makes up 30 percent of your FICO score, and FICO data shows that keeping balances under 30 percent of your credit limit significantly improves your standing. If you carry a 5,000 dollar balance on a 10,000 dollar card, you’re already damaging your score. The remaining factors include length of credit history (15 percent), credit mix (10 percent), and new inquiries (10 percent).

Why This Matters for Charleston Homebuyers

In Charleston, where 88 percent of home buyers obtain mortgages, your credit score directly determines whether you qualify for a loan and what you’ll pay monthly. Late payments stay on your report for seven years, collections for the same period, and a single missed payment can lower your score by 100 points or more. Each month you delay addressing errors on your file costs you money in higher interest rates and rejected applications.

Take Action on Errors Immediately

If you have a mistake on your credit file, disputing it with the bureaus should happen immediately. Errors that remain unchallenged continue to harm your financial standing and limit your options for loans and housing. The next section covers the local resources available to Charleston residents who want to challenge inaccuracies and start rebuilding their credit.

Where to Find Credit Repair Help in Charleston – Serving South Carolina, including Greenville, Columbia and Charleston

Local Debt Management Programs

Origin SC operates a debt management program specifically for Charleston residents struggling with credit card debt and unsecured loans. Their licensed credit counselors work with you to negotiate lower interest rates directly with creditors, then consolidate your payments into one monthly amount you send to Origin SC. The organization distributes your payment to creditors on your behalf, and most clients complete their debt payoff in five years or less.

Origin SC handles credit cards, store cards, and some unsecured bank loans from institutions like Capital One and Discover, but they cannot help with mortgages, car loans, taxes, payday loans, or student debt. You can start the process by calling 843-628-3000 option 5 or submitting a free online intake application through their North Charleston office at 8084 Rivers Avenue. They also offer free workshops on credit improvement, homebuyer education, and financial literacy, which provide actionable strategies without pushing you toward expensive solutions.

Verify Credentials and Avoid Scams

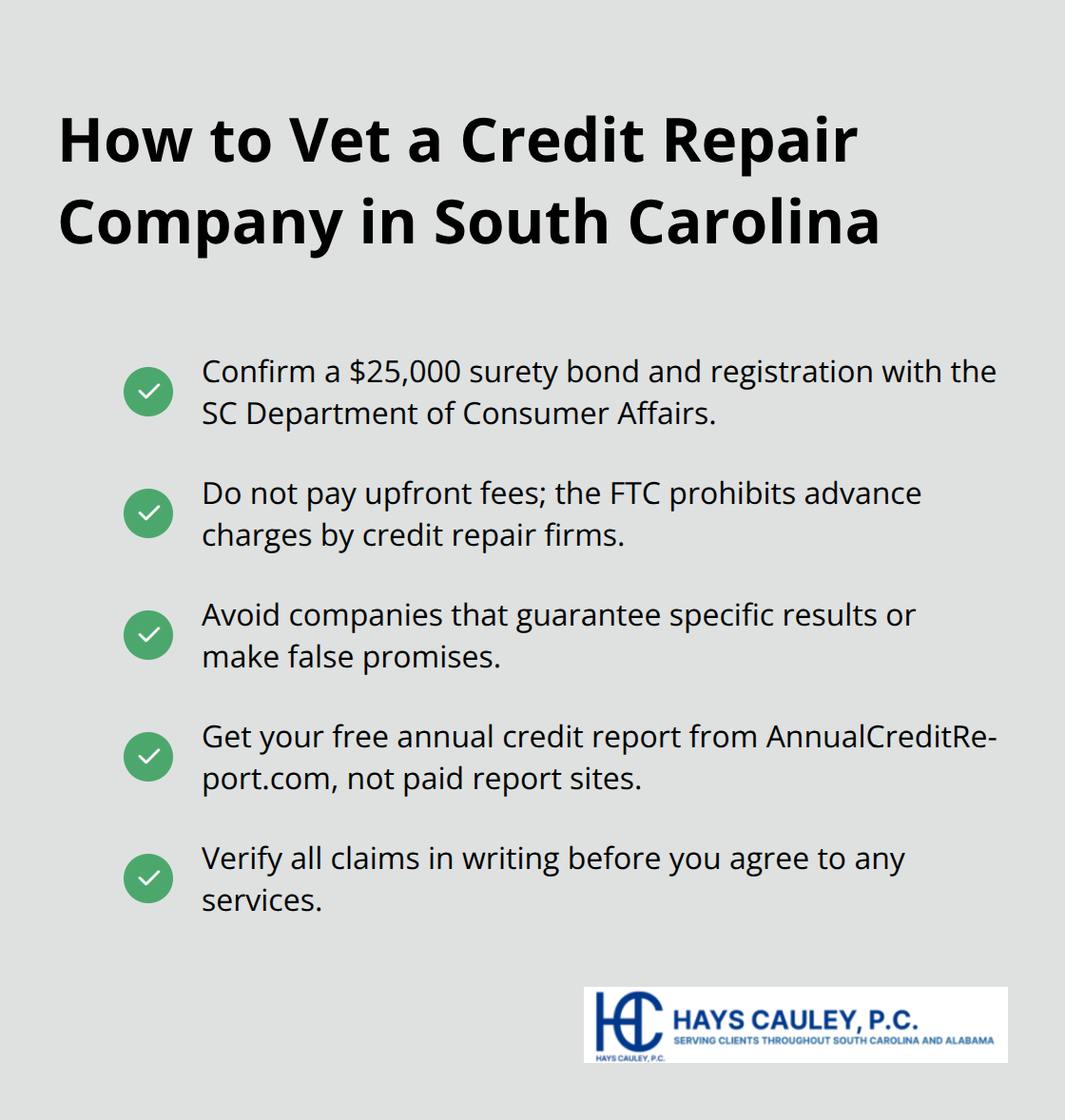

South Carolina law requires credit repair organizations to carry a minimum $25,000 surety bond and register with the Department of Consumer Affairs, so verify any company you work with holds these credentials before paying fees. The Federal Trade Commission prohibits credit repair firms from charging upfront payments, guaranteeing specific results, or making false promises about what they can accomplish. Your free annual credit report comes directly from AnnualCreditReport.com, the official source backed by the FTC and the three major bureaus (Experian, Equifax, and TransUnion), so avoid paid report services that charge unnecessary fees.

Know Your Legal Rights

South Carolina statutes cap credit repair contracts at five years and grant you a ten-day cancellation window after signing, meaning you can walk away if a company’s approach doesn’t fit your situation. When you dispute errors with the bureaus yourself, send written disputes with supporting documents and follow up until they respond. If disputes with the bureaus stall or you face resistance from creditors, a consumer protection law firm can challenge inaccuracies and protect your rights under federal law.

Next Steps for Your Credit Repair Journey

With local resources identified and your legal protections understood, you now have the foundation to take action. The practical steps you take next-disputing errors, creating a repayment plan, and building positive credit history-will determine how quickly your score recovers and what financial opportunities open up for you.

How to Fix Credit Errors and Build Better Payment Habits – Serving South Carolina, including Greenville, Columbia and Charleston

Challenge Inaccuracies With Written Disputes

Written disputes with supporting documents form your strongest tool for challenging inaccurate information on your credit file. The Federal Trade Commission requires credit bureaus to investigate disputes within 30 days, and if they cannot verify the information, they must remove it. Send your dispute letter to each bureau that shows the error-Experian, Equifax, and TransUnion all maintain separate dispute processes-and include copies of documents that prove the inaccuracy, such as payment receipts, account statements, or correspondence with creditors. Do not rely on phone calls or online dispute forms; written disputes create a paper trail that protects you if the bureau fails to act. After you submit your dispute, follow up in writing within 30 days if you haven’t received a response, and document every communication. If a bureau ignores your dispute or refuses to remove verified errors, a consumer protection law firm can file a lawsuit on your behalf to enforce your rights under the Fair Credit Reporting Act.

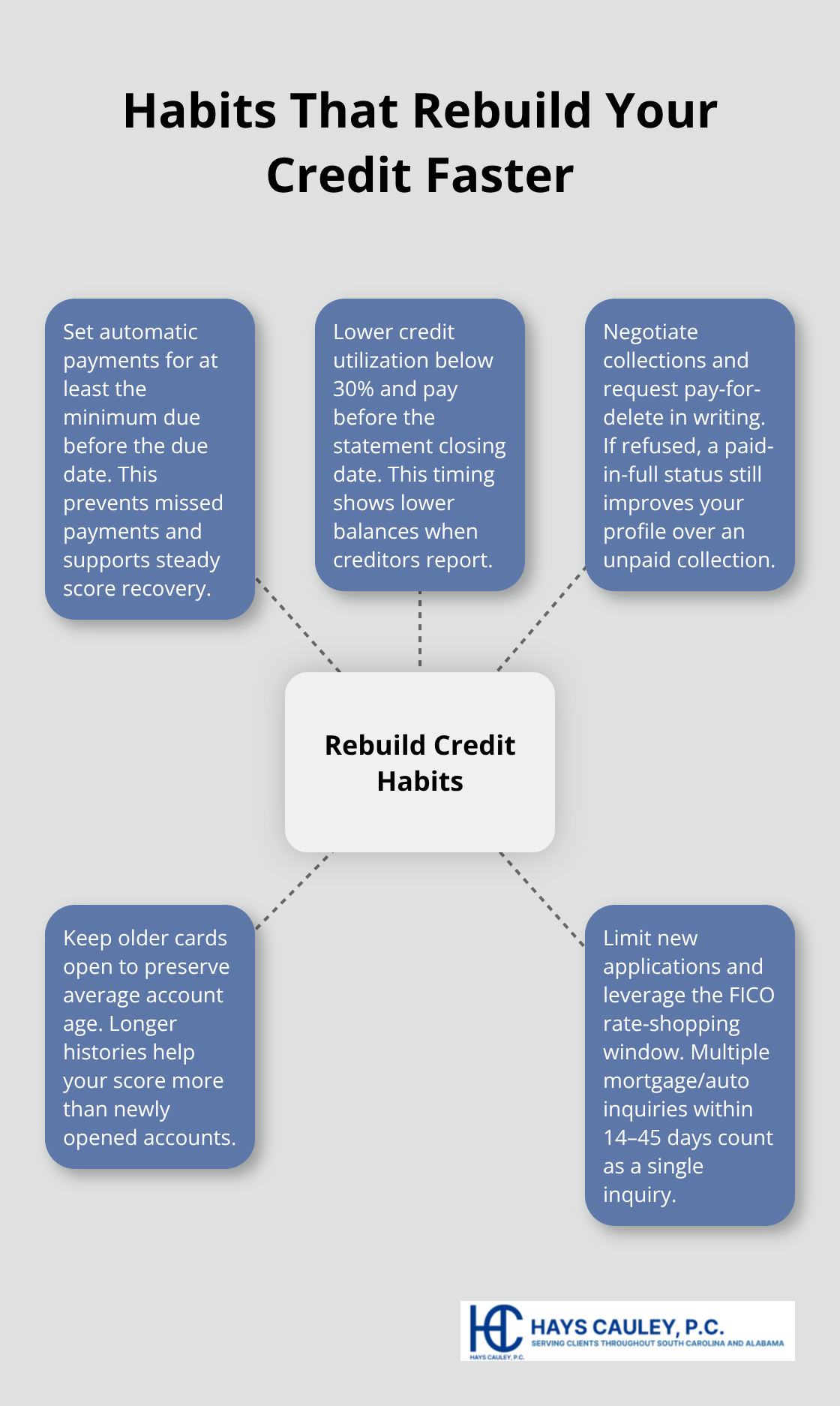

Establish Automatic Payments to Protect Your Score

Your payment history controls 35 percent of your FICO score, which means one missed payment can drop your score by 100 points, but consistent on-time payments rebuild it faster than any other action. Set up automatic payments for at least the minimum due on each account, scheduled to post before the due date, so you never miss a deadline regardless of your schedule. This single step eliminates the risk of accidental late payments and demonstrates reliability to lenders over time.

Reduce Credit Utilization Strategically

If you carry balances, pay down your largest debts first to reduce credit utilization-the second most important scoring factor at 30 percent of your FICO score-and try to get each card below 30 percent of its limit within the next 60 to 90 days. Creditors report your balance to the bureaus on a specific date each month, usually your statement closing date, so paying down balances just before that date shows lower utilization and improves your score faster than spreading payments throughout the month. This timing advantage costs nothing and accelerates your progress significantly.

Handle Collections and Preserve Account Age

If you have collections accounts, negotiate a settlement and request a pay-for-delete agreement in writing, where the collector removes the account from your report after you pay; if they refuse deletion, at least get them to mark the account as paid in full, which improves your score more than an unpaid collection. Keep older credit cards open even after paying them off, because closing them shortens your average account age and lowers your score. Accounts older than two years carry more weight than new accounts, so preserving your credit history length matters as much as current payment behavior.

Manage New Credit Applications Carefully

New credit inquiries temporarily reduce your score by a few points, so avoid applying for multiple loans or cards within 90 days unless you’re shopping for a mortgage or auto loan, where multiple inquiries within 14 to 45 days count as a single inquiry under FICO scoring rules. This protection allows you to compare rates without penalty when making major financial decisions.

Final Thoughts

Credit repair in Charleston takes time, but the steps you’ve learned here produce measurable results. Most people see score improvements within 30 to 60 days after disputing inaccuracies, since bureaus must investigate within 30 days and remove unverified items. Payment history changes take longer-consistent on-time payments rebuild your score gradually over three to six months, while collections and late payments fade in impact after two to three years of positive behavior.

If you’ve disputed errors and the bureaus refuse to remove them, or if creditors ignore your requests for corrections, contact a consumer protection law firm. We at Hays Cauley, P.C. help Charleston residents challenge inaccurate credit reporting and hold bureaus accountable when they violate your rights under federal law. Many people wait months hoping errors disappear on their own, but that strategy costs you thousands in higher interest rates and rejected loan applications.

Start with your free annual credit report from AnnualCreditReport.com, identify errors, and challenge them in writing. Set up automatic payments immediately and contact Origin SC if you need help negotiating with creditors. Your Charleston SC credit repair journey depends on taking action now rather than waiting for your score to improve on its own.