Every day, consumers face threats to their financial security-from unauthorized charges to identity theft to aggressive debt collectors. Understanding your consumer rights is the first step toward protecting yourself.

We at Hays Cauley, P.C. know that many people don’t realize what protections federal law actually gives them. This guide walks you through the violations you might encounter, the legal safeguards available to you, and exactly how to fight back when something goes wrong.

Common Consumer Rights Violations: Serving South Carolina, including Greenville, Columbia and Charleston

Unauthorized Credit Inquiries and Reporting Errors

Unauthorized credit inquiries damage your financial standing without your knowledge or consent. When a creditor or debt collector pulls your credit report without permission, your credit score drops and problems multiply.

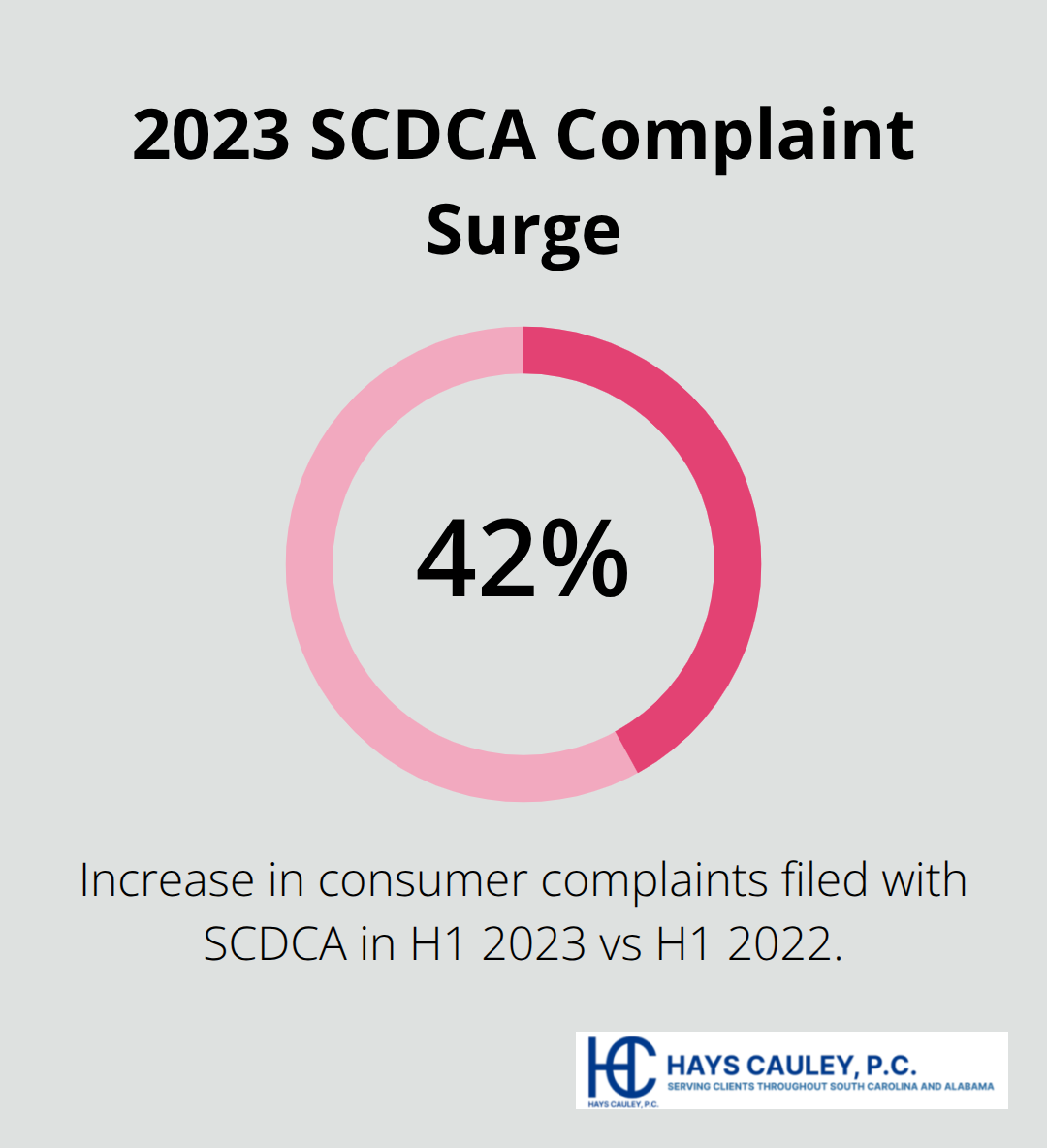

The Fair Credit Reporting Act sets strict rules about who can access your credit file and under what circumstances, yet violations occur regularly. In the first half of 2023, the South Carolina Department of Consumer Affairs logged 2,885 consumer complaints-a 42% increase compared to the same period in 2022-with credit and reporting issues representing a substantial portion of these complaints.

Reporting errors inflict equal damage to your finances. A single mistake on your credit report (a missed payment that wasn’t yours, an account opened fraudulently, or an incorrect balance) can tank your score and make lenders deny you credit at reasonable rates. Credit reporting agencies process millions of files with minimal human review, which is why errors persist. If you spot an inaccuracy, you have the legal right to dispute it directly with the credit bureau and demand correction within 30 days.

Identity Theft and Fraudulent Accounts

Identity theft ranks among the most destructive violations consumers face today. Thieves open credit cards, take out loans, or establish accounts in your name, leaving you responsible for the debt. The South Carolina Department of Consumer Affairs provides resources specifically for identity theft victims, recognizing how prevalent this crime has become. Fraudulent accounts appear on your credit report immediately, damaging your score before you even know the theft occurred.

The recovery process demands significant time and effort. You must contact each creditor, file police reports, place fraud alerts with credit bureaus, and monitor your accounts for months. Prevention matters far more than recovery. Check your credit reports from all three bureaus annually at no cost. Look for accounts you didn’t open, inquiries you didn’t authorize, and balances that don’t match your records. If you spot fraudulent activity, act fast-the faster you report it, the faster you can limit damage and recover funds.

Debt Collection Harassment and Illegal Practices

Debt collectors often cross legal lines to pressure consumers into paying. The Fair Debt Collection Practices Act prohibits calling before 8 a.m. or after 9 p.m., contacting you at work if your employer prohibits it, threatening arrest or wage garnishment they can’t legally pursue, and contacting third parties about your debt. Yet violations happen constantly. Some collectors call repeatedly within hours, use profanity, threaten violence, or misrepresent the debt amount.

South Carolina law provides additional protections through the Unconscionable Debt Collection Practices Act, which prohibits practices that are grossly unfair, oppressive, or unconscionable. Document every call, text, and letter from collectors. Write down the date, time, caller name, company name, and exactly what was said. Keep these records in a file you can access quickly. If a collector violates the law, you can file a complaint with the South Carolina Department of Consumer Affairs or call 800-922-1594. Many consumers tolerate harassment without realizing that violations give them legal remedies and potential damages-understanding these protections is the foundation for taking action when your rights are violated.

What Federal Law Actually Guarantees You

Federal consumer protection laws exist specifically because violations happen constantly and companies count on consumers not knowing their rights. Three major federal statutes form the backbone of your protections against credit reporting abuse, debt collection harassment, and identity theft.

The Fair Credit Reporting Act Protects Your Credit File

The Fair Credit Reporting Act gives you the power to challenge inaccurate information on your credit report, and creditors must verify disputes within 30 days or remove the item. This matters because credit bureaus often ignore consumer disputes the first time around. Send your dispute in writing, keep copies, and follow up if you don’t receive a response within the deadline.

Inaccuracies on your credit report can cost you thousands in higher interest rates or denied credit applications. The law requires credit bureaus to investigate your claim and respond to you in writing with the results. If the bureau cannot verify the information, it must delete it. You have the right to add a statement to your file if the bureau refuses to remove an error, which appears whenever someone pulls your report.

The Fair Debt Collection Practices Act Sets Hard Limits

The Fair Debt Collection Practices Act prohibits debt collectors from calling before 8 a.m. or after 9 p.m., contacting you at work, misrepresenting the debt amount, or threatening actions they cannot legally take. South Carolina adds another layer of protection through the Unconscionable Debt Collection Practices Act, which makes illegal any collection tactic that is grossly unfair or oppressive.

If a collector violates these rules, you can sue for actual damages, statutory damages up to $1,000 per violation, and attorney fees. This means a collector making five harassing calls in one day could owe you $5,000 plus your legal costs, which is why many collectors stop immediately when they know the law. Document every call, text, and letter from collectors with the date, time, caller name, company name, and exact words spoken.

Identity Theft Protections Give You Real Control

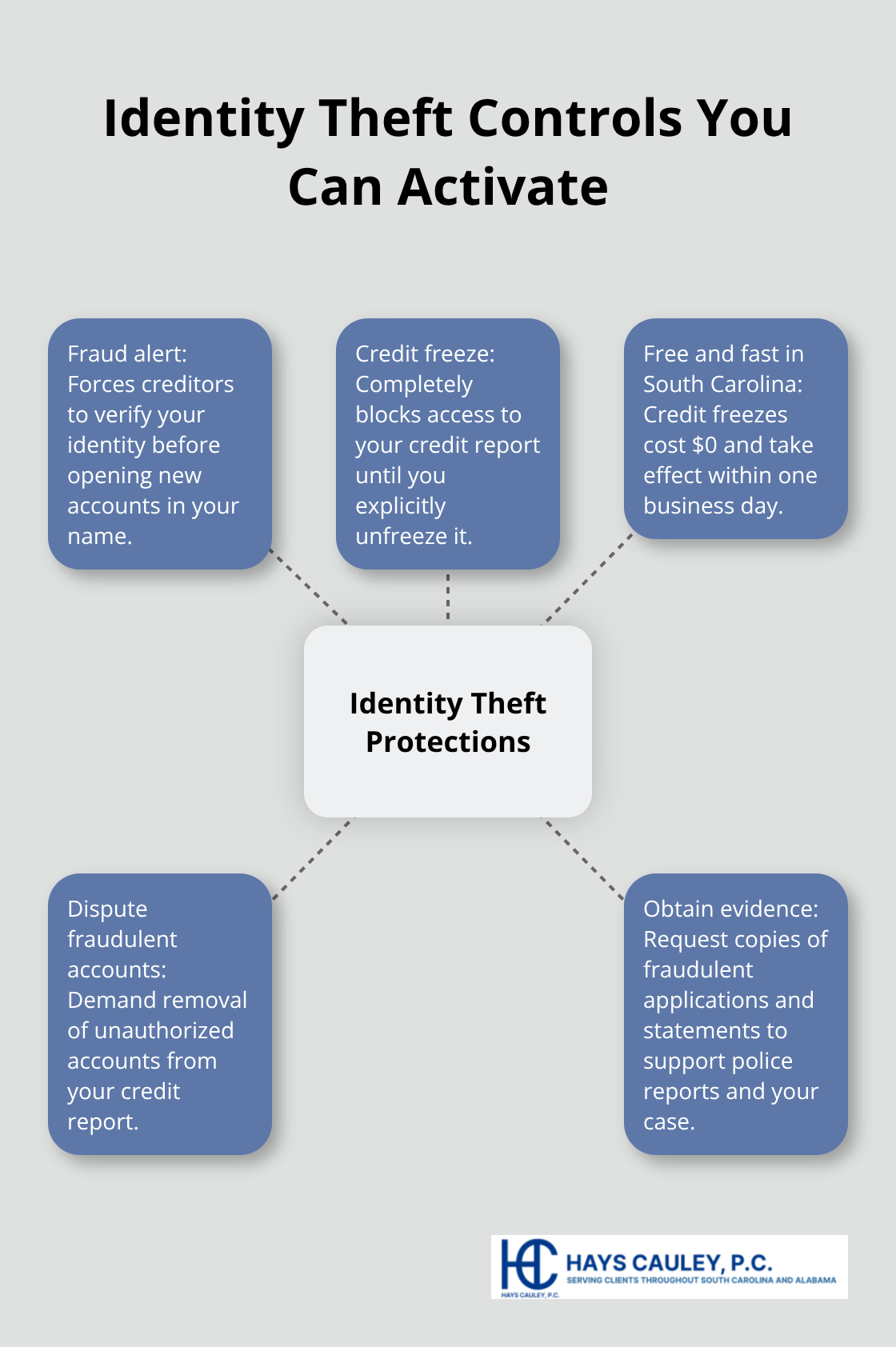

The Identity Theft Enforcement and Recovery Act gives you rights that most consumers never use. You can place a fraud alert on your credit file for free, which forces creditors to verify your identity before opening accounts in your name. Better yet, you can request a credit freeze, which completely blocks access to your credit report unless you explicitly unfreeze it. Credit freezes cost nothing in South Carolina and take effect within one business day.

If identity theft does occur, you have the right to dispute fraudulent accounts and demand removal from your credit report. The law also entitles you to obtain copies of fraudulent applications and account statements from creditors, giving you evidence to file police reports and support your case. Contact the South Carolina Department of Consumer Affairs at 800-922-1594 if a creditor refuses to provide these documents or if collectors continue contacting you about fraudulent debt.

These federal protections exist on paper, but they only work when you take action. The next section shows you exactly how to document violations and file complaints that force companies to respond.

How to Take Action When Your Rights Are Violated

Document Everything Immediately

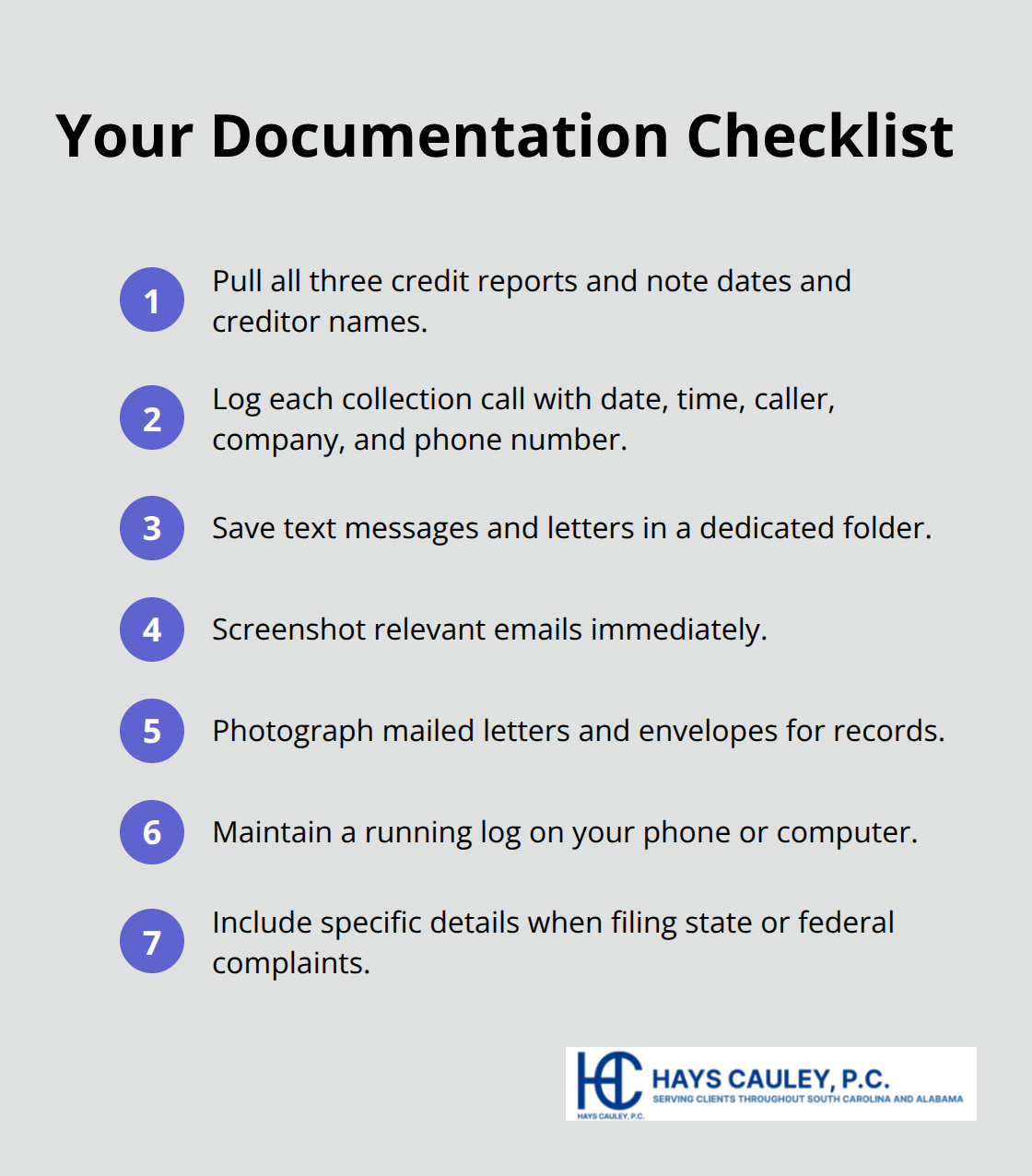

Documentation forms your foundation for winning. Start immediately after you discover a violation and do not wait. For unauthorized credit inquiries, pull your credit reports from all three bureaus at annualcreditreport.com and note the exact date each inquiry appears, the creditor name, and whether you authorized it. For debt collection harassment, write down the date, time, caller name, company name, phone number, and every word spoken during the call. Save text messages and letters in a folder you can access quickly.

Screenshot emails, photograph letters, and maintain a running log on your phone or computer. This documentation becomes your evidence when you file complaints or pursue legal action. In the first half of 2023, the South Carolina Department of Consumer Affairs recovered nearly $500,000 for consumers through the complaint process, and that recovery happened because people filed documented complaints with specific details.

File Complaints with State and Federal Agencies

Filing a complaint with the South Carolina Department of Consumer Affairs is free and often more effective than you realize. Visit consumer.sc.gov and click FILE A COMPLAINT to submit your case online through the portal available 24/7, or mail a paper complaint form to PO Box 5757, Columbia, SC 29250. The online portal proves superior because you can track progress and communicate directly with your assigned analyst, which speeds processing significantly.

Include your documentation with the complaint, describe the violation clearly, and state what remedy you seek (refund, account removal, or damages). SCDCA processes complaints and mediates between you and the business, and the agency tracks complaint patterns to identify widespread violations. When you file, you also help other consumers because complaint data guides enforcement action. For federal violations involving debt collection or credit reporting, you can file complaints with the Consumer Financial Protection Bureau at consumerfinance.gov, which investigates violations of federal law and publishes complaint trends publicly. Filing with both state and federal authorities strengthens your case.

Pursue Legal Action for Significant Violations

Legal action becomes necessary when complaints fail to produce results or when violations caused significant financial harm. Consumer protection laws allow you to recover actual damages, statutory damages up to $1,000 per violation, and attorney fees. A debt collector making five harassing calls in violation of the law could owe you $5,000 plus legal costs. This is why many collectors stop immediately once they learn you know the law.

Consult with a consumer protection attorney if a creditor refuses to correct errors after your dispute, if collectors continue contacting you about fraudulent debt, or if your credit score damage resulted from violations. Most attorneys handling consumer cases work on contingency, meaning you pay nothing upfront and the defendant pays your attorney fees if you win.

Final Thoughts

Your consumer rights exist to protect you, but only when you actively use them. Start monitoring your credit today by pulling your reports from all three bureaus at annualcreditreport.com and reviewing them carefully for unauthorized accounts, incorrect balances, or inquiries you didn’t authorize. Place a credit freeze with each bureau to block access to your file unless you explicitly unfreeze it-this single step costs nothing in South Carolina and prevents most identity theft before it starts.

Document everything from this moment forward when violations occur. Write down the date, time, caller name, and what was said during collector calls; screenshot credit report errors immediately; photograph fraudulent account statements. This documentation transforms complaints from vague accusations into compelling evidence that agencies and courts take seriously, and file complaints with the South Carolina Department of Consumer Affairs at consumer.sc.gov or call 800-922-1594 when violations happen.

Understanding your consumer rights means recognizing that federal laws give you real power to dispute credit errors, stop illegal debt collection, and recover damages from companies that violate your rights. If violations occur and complaints alone haven’t resolved the matter, contact Hays Cauley, P.C. for guidance navigating your rights and pursuing legal action. You deserve a fair marketplace, and the law stands behind you when you stand up for yourself.