How to Investigate Credit Report Errors Before It Hurts Your Score

Your credit report directly impacts your ability to borrow money, rent an apartment, or even get hired for certain jobs. Errors on these reports happen more often than you’d think, and they can tank your score without you knowing why.

We at Hays Cauley, P.C. help people investigate credit report errors and fight back against inaccuracies that damage their financial health. This guide walks you through spotting mistakes, disputing them, and protecting yourself going forward.

Getting Your Free Credit Reports, Serving South Carolina, including Greenville, Columbia and Charleston

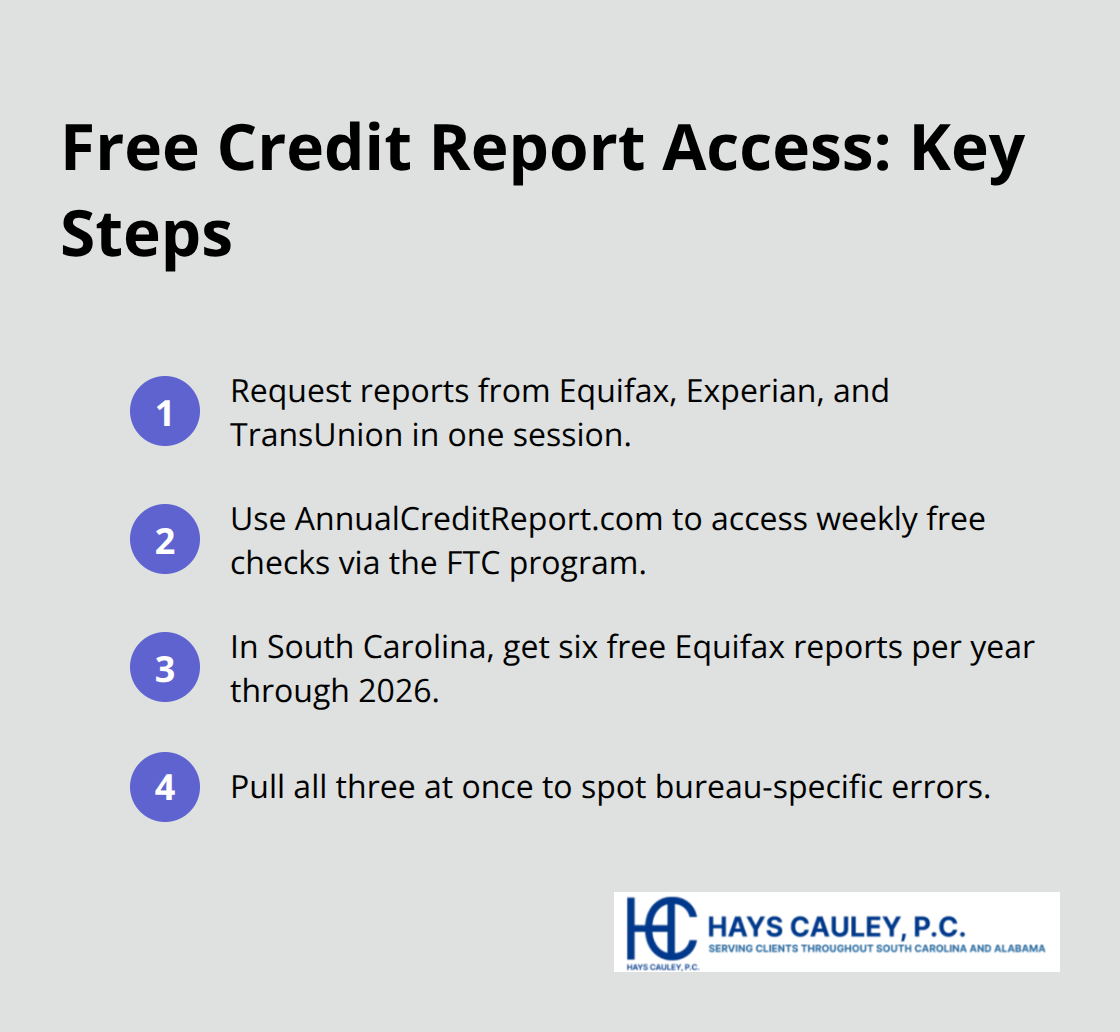

Request Reports from All Three Bureaus at Once

Start by pulling your credit reports from all three bureaus simultaneously rather than spacing them out over time. Visit annualcreditreport.com and request reports from Equifax, Experian, and TransUnion in one session. You receive one free report annually from each bureau, and the FTC also offers a program that lets you check each report for free once weekly through the same site. In South Carolina, you can obtain six free reports per year through 2026 by visiting Equifax directly or calling 1-866-349-5191. Getting all three at once matters because each bureau maintains separate records, and errors on one may not appear on another.

The FTC found that one in five consumers discovers errors on at least one credit report, so checking all three increases your odds of catching mistakes early.

Verify Your Personal Information First

Once you have your reports, examine your personal information before reviewing accounts. Verify that your name appears spelled correctly, your address matches where you actually live, and your phone number is accurate. Identity mix-ups occur frequently in South Carolina, particularly among residents with common surnames. These errors can cause accounts belonging to another person to land on your report, creating serious financial consequences. Catching these mistakes at the start prevents you from wasting time investigating account-level errors that stem from a fundamental identity problem.

Check Each Account Line by Line

Next, examine each account listed on your reports. Confirm you actually opened each account, verify the balance shown matches your records, and check that payment history reflects what you’ve actually paid. South Carolina residents commonly encounter accounts reported as open when they’re closed, delinquency status errors, and the same debt listed multiple times by different creditors. Medical debt errors are particularly prevalent in rural South Carolina areas where healthcare systems sometimes misreport or mishandle data. Fraudulent accounts you don’t recognize are red flags for identity theft and require immediate action.

Identify Outdated and Duplicate Items

Accounts that should have fallen off after seven years but remain on your report demand attention. Duplicate debts-the same debt listed multiple times by different creditors-also harm your score and require correction. These errors artificially inflate your debt load and lower your creditworthiness in lenders’ eyes. Spotting these items now positions you to move forward with targeted disputes that address the most damaging inaccuracies on your file.

Common Credit Report Errors in South Carolina, Serving Greenville, Columbia and Charleston

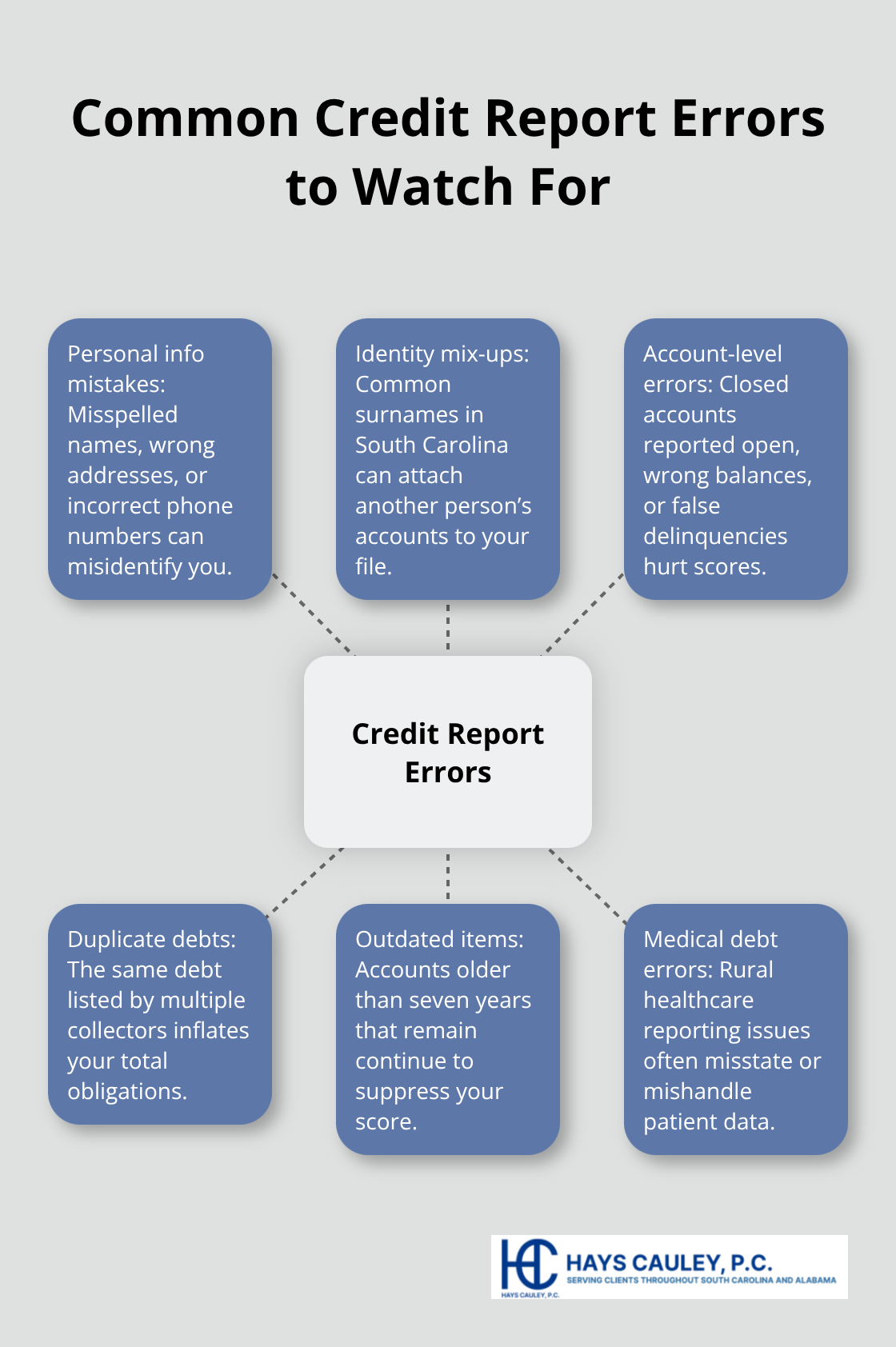

Personal Information Mistakes That Cascade Into Bigger Problems

Personal information errors form the foundation of many credit report problems. Misspelled names, incorrect phone numbers, and wrong addresses appear far more frequently than most people realize. In South Carolina, identity mix-ups happen regularly due to common surnames, and these errors cascade into larger problems when accounts belonging to another person land on your file.

You might see an address you’ve never lived at, a phone number you don’t recognize, or a middle initial that isn’t yours. These details matter because lenders use them to verify your identity, and mismatches can slow loan approvals or trigger fraud alerts. Check your Social Security number carefully as well-transposed digits or incorrect numbers on your report require immediate correction.

Account-Level Errors That Signal Fraud or Misreporting

Account-level errors prove equally damaging to your financial health. You may discover accounts you never opened, credit cards you don’t recognize, or loans attributed to you that belong to someone else. These fraudulent accounts signal identity theft and demand urgent action through IdentityTheft.gov, which provides a personalized recovery plan. Closed accounts still showing as open distort your available credit and lower your score artificially. Payment history errors-showing late payments you never made, incorrect delinquency dates, or wrong balances-damage your creditworthiness even when the underlying account belongs to you.

Duplicate Reporting and Outdated Items That Inflate Your Debt

Duplicate reporting and outdated items compound these problems significantly. The same debt appears multiple times under different creditors or collection agencies, inflating your total debt load and making your financial situation look worse than it actually is. Medical debt errors plague rural South Carolina areas especially, where healthcare systems sometimes misreport or mishandle patient data. Accounts that should have fallen off after seven years-the standard reporting period-continue appearing on your reports and suppressing your score. One in five consumers finds errors on at least one credit report according to the FTC, yet many people never investigate because they don’t know what to look for.

How to Document Errors Against Your Own Records

Start by creating a detailed list of every account on your reports: the creditor name, account number, reported balance, payment status, and the date the account opened. Compare this list against your own records-bank statements, payment confirmations, and loan documents. Discrepancies between what you see on the report and what your personal records show are the strongest evidence for disputes. Fraudulent accounts require different handling than simple errors. If you spot accounts you absolutely did not open, file a report with IdentityTheft.gov immediately and consider placing a security freeze on your credit file (which must be placed within five business days of your written request and costs nothing).

The errors you’ve identified now form the basis for your dispute strategy. Understanding which mistakes appear on your reports positions you to take targeted action that produces real results.

How to File a Dispute That Actually Gets Results, Serving South Carolina, including Greenville, Columbia and Charleston

Prepare Your Documentation Before Contacting Any Bureau

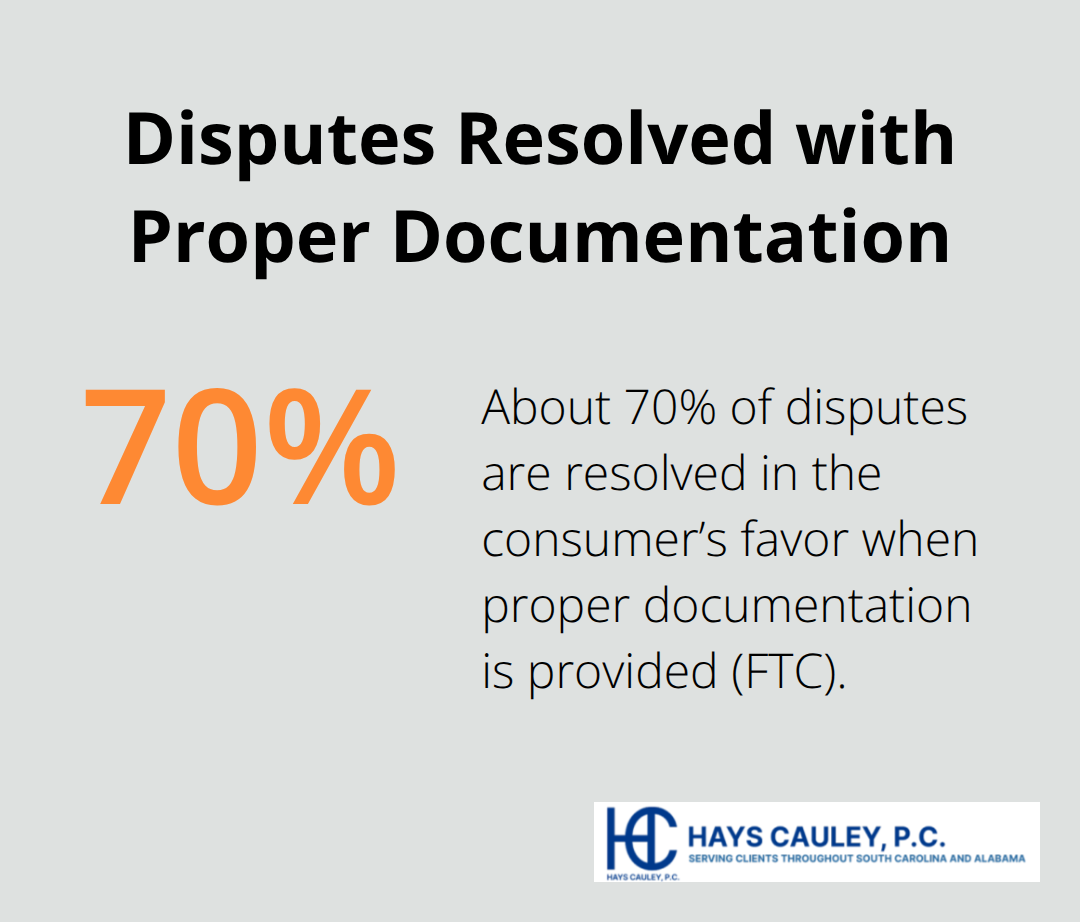

Pull together the specific account numbers, dates of first delinquency, reported balances, and any other details that appear on your credit report for each error you identified. Cross-reference these against your own records: bank statements, payment confirmations, loan documents, and any correspondence with creditors. Write down the exact discrepancies between what the bureau reports and what your records show. The FTC data reveal that disputes are resolved in the consumer’s favor about 70 percent of the time when proper documentation is provided, so this preparation stage directly impacts your success rate.

Send Your Dispute in Writing via Certified Mail

Send your dispute in writing via certified mail with return receipt requested-never rely on online-only submissions or phone calls. Your written dispute must include your full name, address, Social Security number, a detailed explanation of each error, the specific account numbers involved, and copies of supporting documents. The CFPB provides sample dispute letters that strengthen submissions, and attaching bank statements, payment receipts, court documents, and identity theft evidence makes your case substantially harder to dismiss. Mail your dispute to each credit bureau that reports the error; send the same documentation to the furnisher (the creditor or collection agency that originally reported the information). Contact Equifax at 1-888-378-4329, TransUnion at 1-800-916-8800, or Experian at 1-888-397-3742 to confirm mailing addresses, though you can initiate disputes online as well.

Track Progress Aggressively During the 30-Day Investigation

The 30-day investigation clock begins when the bureau receives your dispute, and many investigations are automated with minimal human review-which is precisely why aggressive follow-up matters. Call the bureau every 10 days to check progress and document every interaction with names, dates, and reference numbers. The bureau must notify you within five days if it deems your dispute frivolous or irrelevant; any such dismissal requires written explanation and gives you grounds to resubmit with strengthened evidence. After the investigation closes, the bureau must issue written results within five business days and provide the furnisher’s contact information if the item remains unchanged.

Handle Results and Escalate if Necessary

If the furnisher stands by the accuracy after 30 days, the item stays on your report unless you add a brief dispute statement explaining your position. If the investigation uncovers an error, the furnisher must notify all three bureaus to correct it, and you receive a free updated credit report. If the dispute drags past 35 days without resolution, escalate to the CFPB at consumerfinance.gov; the agency logged over 175,000 credit reporting complaints in 2020 alone, with investigation delays as a persistent problem. South Carolina law aligns with federal protections under the Fair Credit Reporting Act, providing you leverage if a bureau fails to conduct reasonable investigation or ignores clear evidence-violations can result in actual damages plus attorney fees.

Maintain Organized Records Throughout the Process

Keep every piece of correspondence in an organized file: dispute letters, certified mail receipts, bureau responses, furnisher replies, and your follow-up notes. This documentation becomes essential if you need to pursue legal action or file a complaint with the CFPB. We at Hays Cauley, P.C. help consumers navigate complex disputes and hold credit bureaus accountable when they fail to investigate properly.

Final Thoughts

Check your credit reports at least once every four months throughout the year rather than waiting for your annual free report. The FTC program allows you to access weekly free checks through annualcreditreport.com, which helps you spot fraudulent accounts or new errors before they damage your score significantly. South Carolina residents should stagger requests every four months to monitor changes across all three bureaus and catch identity theft early when you investigate credit report errors.

If you discover signs of identity theft, place a security freeze on your credit file immediately (it must be placed within five business days of your written request and costs nothing). A freeze blocks lenders from accessing your report without your authorization, preventing criminals from opening accounts in your name. You can lift a freeze temporarily for specific periods or lenders, with electronic lifts completing within about 15 minutes.

Serious disputes involving willful violations by credit bureaus demand professional guidance. If a bureau fails to conduct reasonable investigation or ignores clear evidence of errors, you may recover actual damages plus attorney fees. Contact Hays Cauley, P.C. if your dispute stalls or if you face barriers to credit, housing, or employment due to inaccurate reporting.