Support for Credit Errors: Getting Help to Correct Your Report

A mistake on your credit report can cost you thousands of dollars in higher interest rates or denied loans. Yet most people don’t know they have the right to challenge these errors.

We at Hays Cauley, P.C. help South Carolina consumers, including those in Greenville, Columbia, and Charleston, get support for credit errors and fix their reports. This guide walks you through your options-from handling disputes yourself to knowing when to call in legal help.

How Credit Errors Wreck Your Financial Life

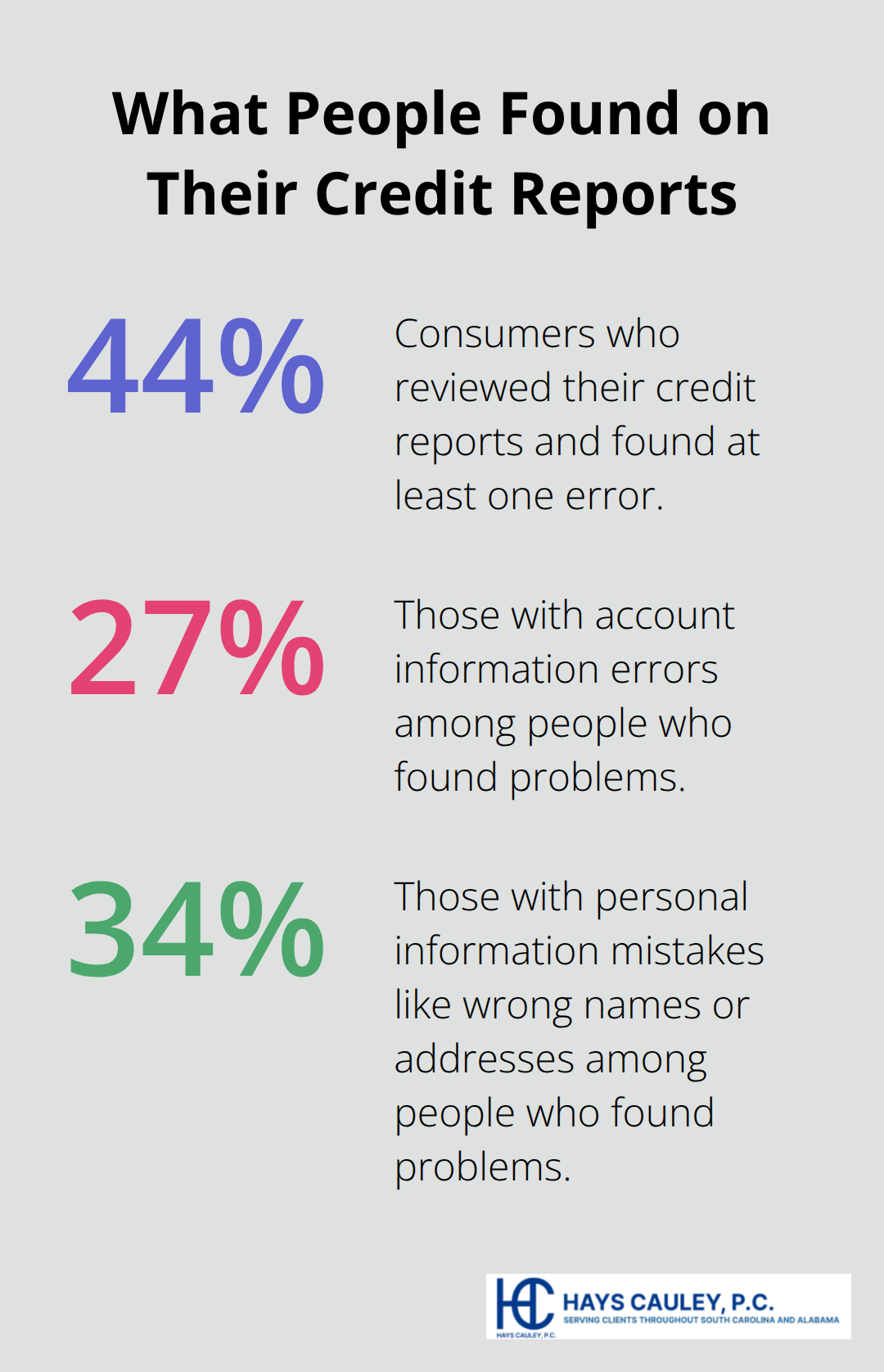

A Consumer Reports and WorkMoney study conducted in February 2024 found that 44 percent of people who reviewed their credit reports discovered at least one error. That’s nearly half of all consumers. The mistakes ranged from account information errors (27 percent of those who found problems) to personal information mistakes like incorrect addresses or names (34 percent).

These aren’t harmless typos. Account errors included unrecognized accounts opened in your name, late payments reported when you paid on time, and collections attributed to you that belong to someone else. When wrong information sits on your report, lenders see a riskier version of you than actually exists. A single error can cost you hundreds or thousands in higher interest rates. If a lender denies you credit entirely based on bad data, you lose access to loans, mortgages, or credit cards you should qualify for. The CFPB reported a dramatic surge in complaints about credit reporting errors, jumping from 165,129 complaints in 2021 to 430,600 in 2023. That threefold increase reflects how inaccurate data damages people’s financial lives.

Where Errors Come From

Data furnishers — the businesses that report information to credit bureaus-originate most errors. When a bank reports your payment history, a collection agency reports a debt, or a lender reports account details, mistakes happen at that source. Furnishers sometimes confuse accounts, misrecord payment dates, or fail to update information after you’ve resolved a problem. Mixed files represent the most serious category of error, where data from someone with a similar name or Social Security number gets tangled with your report. Identity theft creates another source of errors when fraudsters open accounts in your name. The three nationwide bureaus-Equifax, Experian, and TransUnion-compile and distribute this information without always catching errors before they damage your credit. You likely won’t catch these mistakes unless you actively review your reports, yet 25 percent of participants in the Consumer Reports study couldn’t even access their reports online, and 11 percent found the process extremely difficult due to security questions or system failures.

The Real Cost of Inaccurate Data

Your credit score directly determines whether lenders approve you and what interest rate you pay. A score difference of just 50 points means tens of thousands of dollars in additional interest over the life of a mortgage. Beyond lending, credit reports now affect hiring decisions at some employers, rental approvals from landlords, and insurance rates. An error that tanks your score doesn’t just cost you money on loans-it can cost you a job opportunity or force you into a worse apartment at higher rent. The damage compounds because corrections take time, and your credit remains damaged during the investigation period. Lenders, landlords, and employers all rely on these reports to make decisions about you, which means a single mistake can ripple across multiple areas of your life.

Why Access and Correction Matter

The path to fixing errors starts with access. You can’t correct what you don’t see, yet the system makes it harder than it should be for many people to even view their own reports. Once you spot an error, the correction process involves multiple parties-the credit bureau, the furnisher who reported the information, and potentially you. Each step takes time. The Fair Credit Reporting Act gives you the right to dispute inaccurate information, but knowing your rights and taking action separates those who fix their reports from those who suffer the consequences. Understanding what went wrong and how to challenge it puts you in position to reclaim your financial standing.

Your Rights Under Federal Law: Serving South Carolina, including Greenville, Columbia and Charleston

The Fair Credit Reporting Act Protects Your Financial Standing

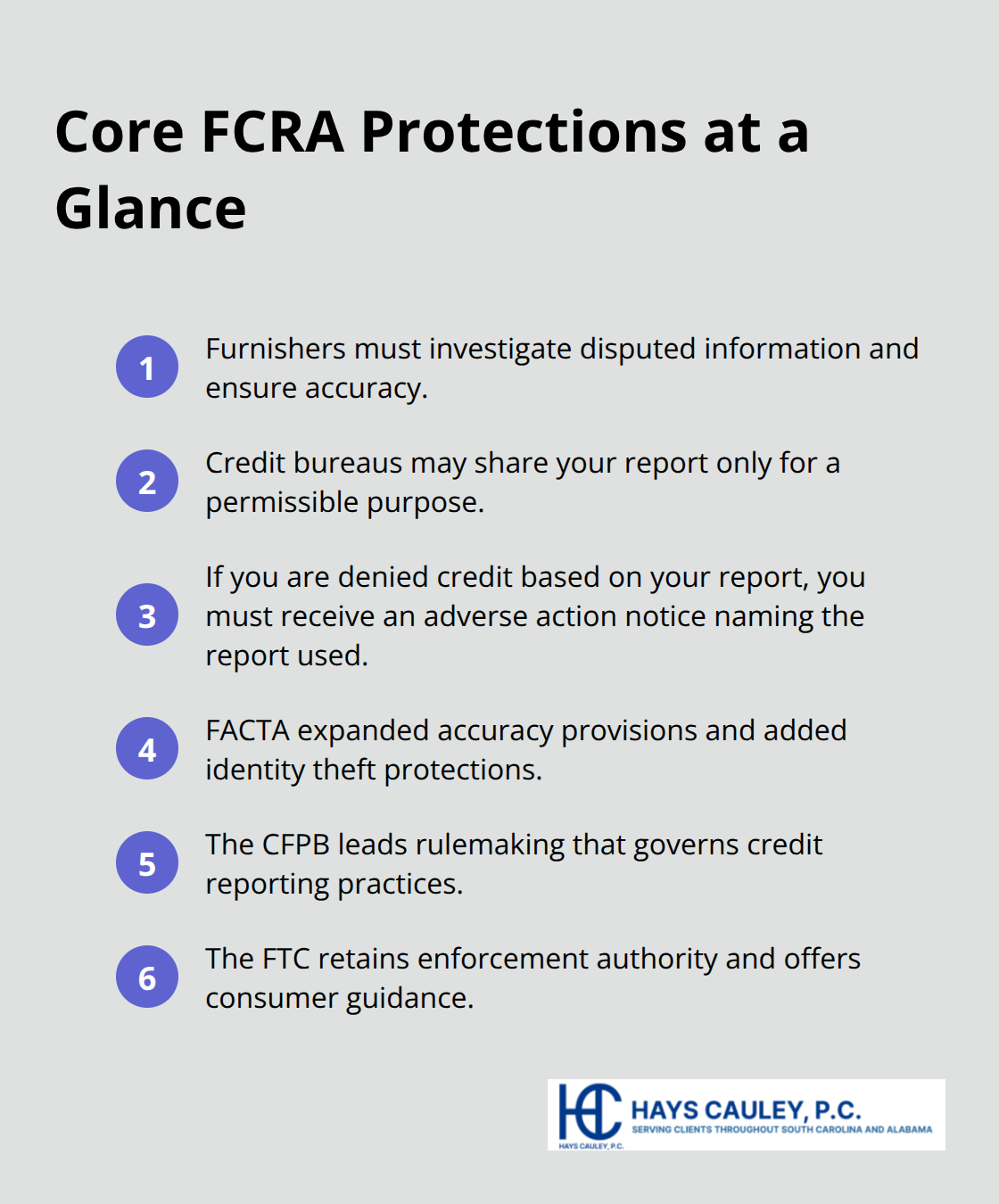

The Fair Credit Reporting Act, passed in 1970 as Title VI of the Consumer Credit Protection Act, gives you concrete legal rights to challenge inaccurate information on your credit report. Under this law, furnishers — the businesses that report your payment history and account details to credit bureaus-have a legal duty to investigate any disputed information to ensure accuracy. When you dispute an error, the furnisher cannot simply ignore you. The FCRA also requires that credit reporting agencies only provide your report to entities with a permissible purpose, protecting you from unauthorized access.

If a lender denies you credit based on information in your report, they must notify you and tell you which report they used.

The Fair and Accurate Credit Transactions Act expanded these protections by adding provisions to improve accuracy and address identity theft. This law shifted much of the rulemaking responsibility to the Consumer Financial Protection Bureau while the Federal Trade Commission retained enforcement authority. This dual oversight means multiple government agencies work to hold credit bureaus and furnishers accountable.

How You Challenge Inaccurate Information

Your right to dispute goes beyond simply asking for corrections. When you file a dispute with a credit bureau, that bureau must investigate within 30 days and forward your evidence to the furnisher reporting the information. If the furnisher determines the information is inaccurate, it must notify all three bureaus so they update your credit reports. The furnisher cannot drag its feet-it has 30 days to respond to your challenge.

If the furnisher verifies the information as accurate but you still believe it’s wrong, you can add a statement to your file explaining the dispute. This statement appears on all future reports and tells potential lenders that you contested the information. You can also request that the bureau send this dispute statement to past recipients of your report (though this may incur a fee).

Government Enforcement Backs Your Rights

The CFPB has enforcement power to penalize bureaus and furnishers that fail to investigate disputes thoroughly or respond within the required timeframe. The FTC provides templates, guidance, and a complaint portal at ReportFraud.ftc.gov to help you navigate the process. These agencies take violations seriously-when bureaus or furnishers ignore disputes or conduct sloppy investigations, they face real consequences.

The legal framework exists specifically because errors are common and their consequences severe. The law is on your side, but it requires you to take action and document everything carefully to make it work. Understanding what protections apply to you positions you to move forward with confidence as you begin the dispute process itself.

Steps to Correct Credit Errors on Your Own: Serving South Carolina, including Greenville, Columbia and Charleston

Obtain Your Free Credit Reports

Start at annualcreditreport.com, the only official source for free annual reports mandated by the FTC. Through 2026, you can access your reports six times per year from Equifax by calling 1-866-349-5191 or visiting their site. The bureaus have extended weekly free viewing access through annualcreditreport.com beyond the traditional annual allowance. Print or download each report and read through it carefully, looking for accounts you don’t recognize, payment statuses that contradict your records, personal information errors like wrong addresses or names, and collections or inquiries you didn’t authorize.

The Consumer Reports and WorkMoney study found that 27 percent of people who spotted errors had account information problems and 34 percent had personal details wrong. Scrutinize both categories thoroughly. Circle or highlight every error you find on your reports.

Gather Your Supporting Documents

Collect documentation immediately that proves the information on your report is inaccurate. Keep copies of bank statements, payment confirmations, letters from creditors, utility bills, or anything that supports your claim. This documentation becomes your evidence when you file your dispute. The stronger your evidence, the more likely the furnisher will correct the error during the investigation period.

File Your Dispute with the Credit Bureau

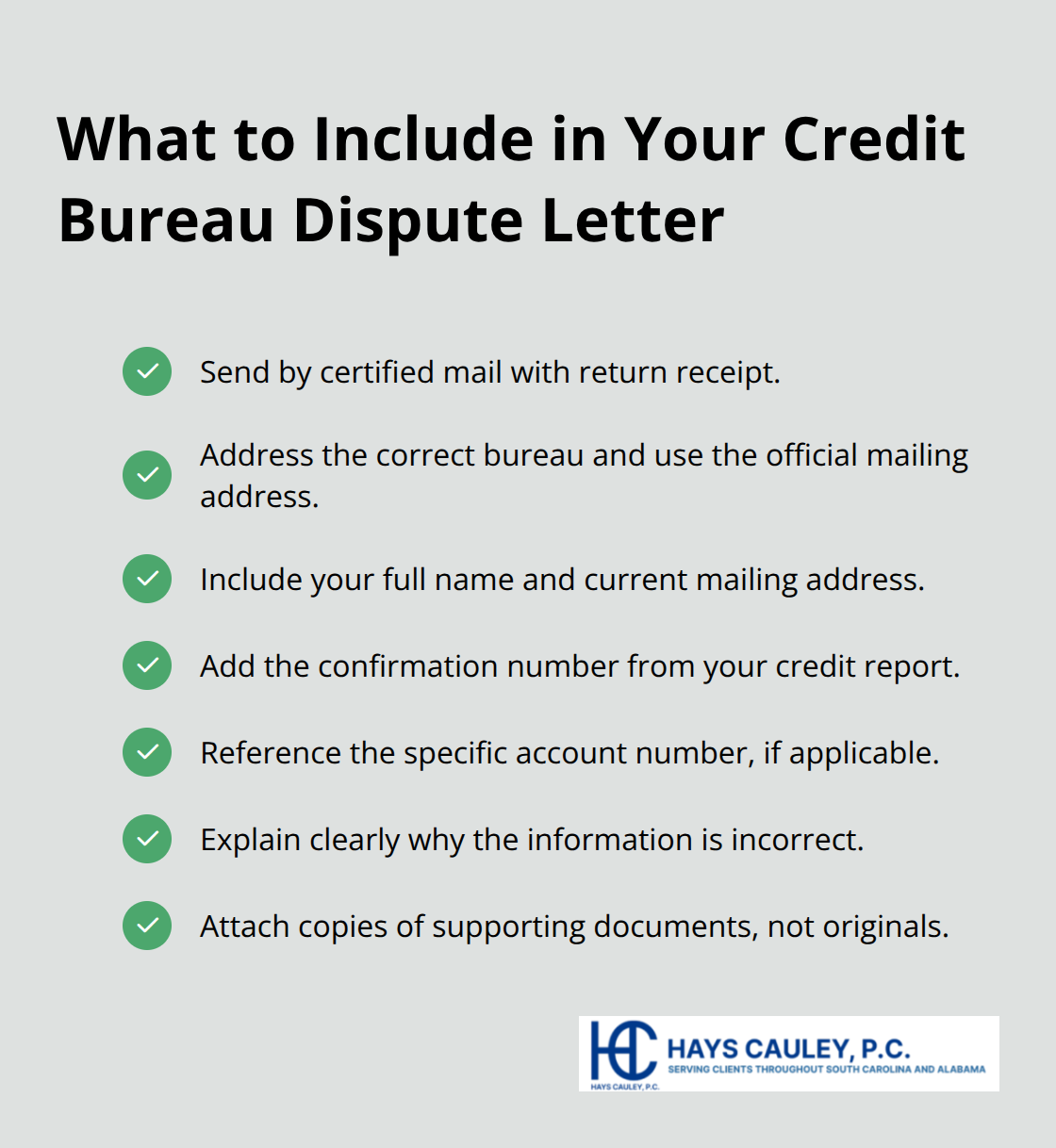

File your dispute directly with the credit bureau reporting the error. Certified mail with return receipt creates an undeniable record that they received your challenge. Address your letter to the correct bureau (Equifax Information Services LLC, P.O. Box 740256; Experian, P.O. Box 4500; or TransUnion Consumer Dispute Center, P.O. Box 2000) and include your name, address, the confirmation number from your credit report, the specific account number if applicable, a clear explanation of why the information is wrong, and copies of your supporting documents.

You can also file disputes online through each bureau’s website or by phone-Experian at 888-397-3742, TransUnion at 800-916-8800, and Equifax at 866-349-5191. Certified mail, however, gives you proof of delivery that protects you if the bureau claims they never received your dispute.

Understand the Investigation Timeline

The bureau has 30 days to investigate, forward your evidence to the furnisher who reported the information, and send you written results. If the furnisher finds an error, all three bureaus must update your reports. If the furnisher stands by the information, you can request that the bureau include a statement in your file explaining that you disputed it. This statement appears on all future credit reports you request.

Track Your Progress and Follow Up

Keep meticulous records of every letter, email, phone call, and document you send, tracking dates and confirmation numbers. Follow up if corrections don’t appear within 45 days of your dispute filing. Contact the bureau directly to confirm receipt of your dispute and ask about the investigation status. Request written confirmation once the investigation concludes, whether the information was corrected or the furnisher verified it as accurate.

When Professional Help Makes the Difference

You’ve filed disputes, gathered documents, and waited through investigations, but sometimes the system fails you. Credit bureaus ignore your dispute or refuse to investigate within 30 days, leaving your report damaged and your options limited. Furnishers stand by inaccurate information despite your evidence, and identity theft created accounts in your name that the bureaus won’t remove. These situations demand more than a template letter and certified mail-they demand legal action.

Support for credit errors becomes essential when disputes stall or when your situation exceeds what self-help can accomplish. Mixed files where another person’s data contaminates your report often require legal intervention to untangle. Systematic errors across multiple accounts suggest a pattern that demands investigation beyond a single dispute. If a lender denied you credit based on inaccurate information and you’ve exhausted the dispute process without results, you may have grounds for legal action under the Fair Credit Reporting Act.

We at Hays Cauley, P.C. help South Carolina consumers, including those in Greenville, Columbia, and Charleston, navigate credit reporting problems that won’t resolve through standard channels. When bureaus or furnishers have broken the law by ignoring disputes, conducting inadequate investigations, or failing to update information, we hold them accountable and help you understand whether you have a claim for damages. Contact us to discuss your situation and determine whether legal action can accelerate your path to a corrected credit report.