South Carolina Credit Report Errors: Understand Your Rights

A mistake on your credit report can cost you thousands of dollars in higher interest rates and rejected loan applications. South Carolina credit report errors are more common than you’d think, affecting millions of consumers nationwide.

The good news is that federal law gives you powerful rights to challenge inaccuracies and hold credit bureaus accountable. We at Hays Cauley, P.C. help South Carolina residents protect themselves against these errors and recover damages when bureaus fail to correct them.

Common Types of Credit Report Errors Affecting South Carolina Residents, Including Greenville, Columbia and Charleston

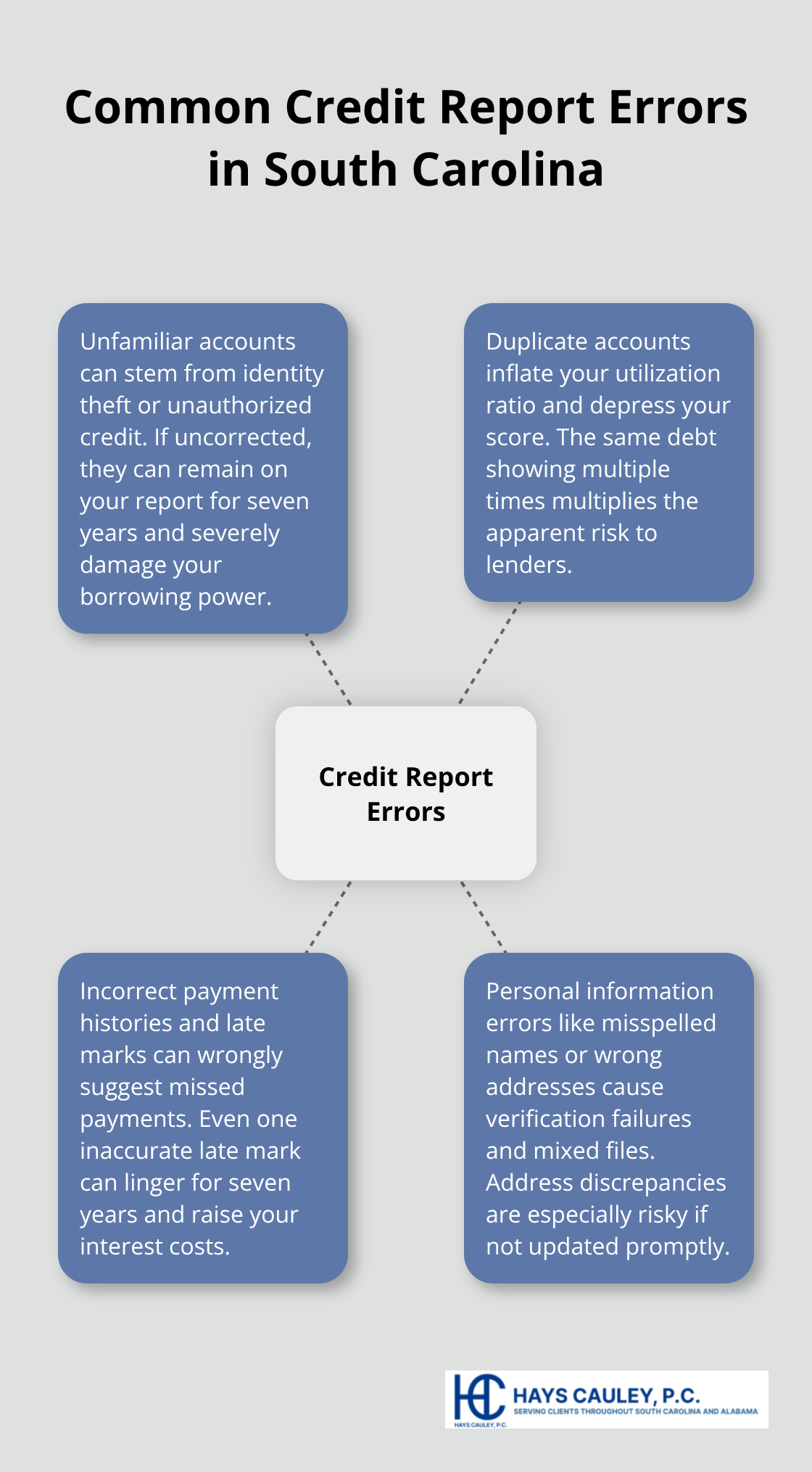

Unfamiliar Accounts and Unauthorized Credit

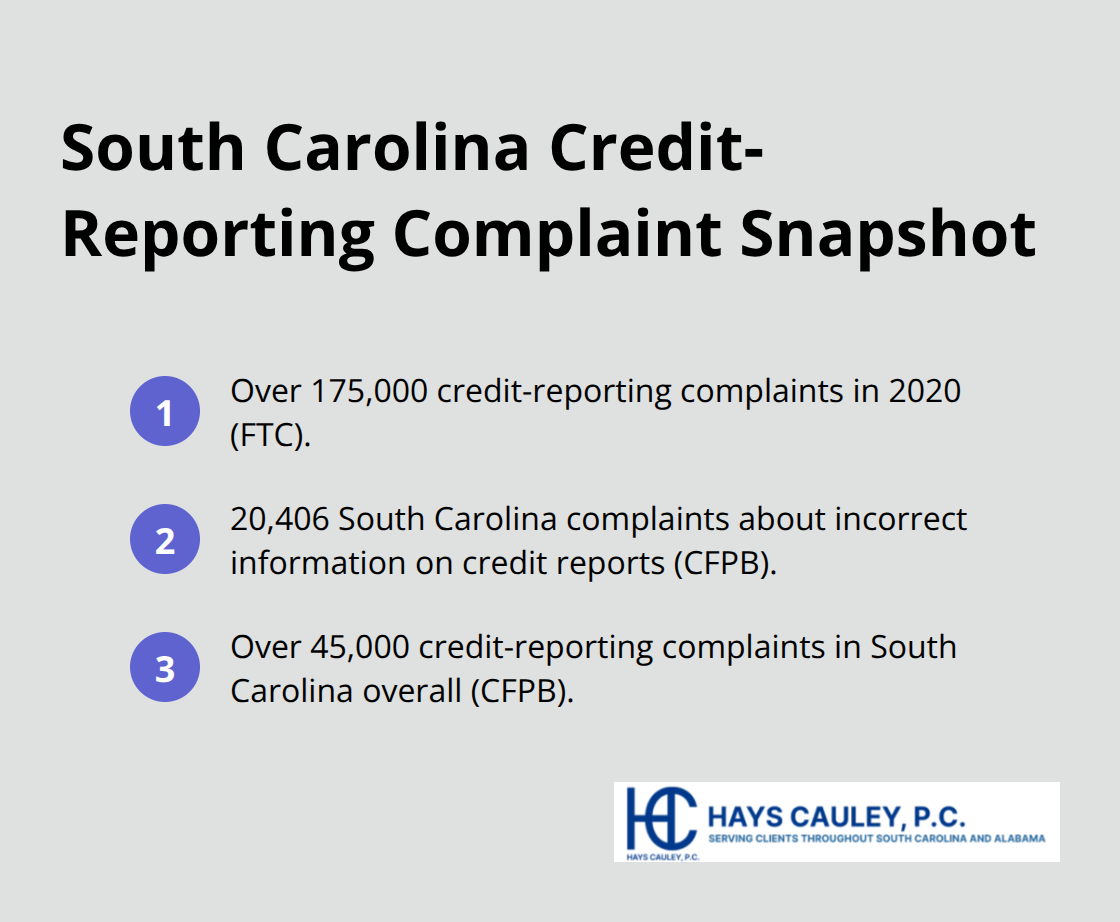

Unfamiliar accounts rank as the most damaging error on credit reports and they stay there for seven years if not corrected. These appear when someone opens credit in your name without permission or when a legitimate creditor lists an account you never authorized. The Federal Trade Commission reported over 175,000 credit-reporting complaints in 2020, and unfamiliar accounts trigger a significant portion of those disputes.

When you spot an account you don’t recognize, contact the furnisher in writing immediately and demand verification of ownership. If they cannot prove you authorized it, push for removal. Acting fast prevents the account from compounding damage to your credit score and borrowing power.

Duplicate Accounts Distorting Your Credit Profile

Duplicate accounts represent another common mistake that distorts your credit utilization ratio and tanks your score unnecessarily. The same debt appears multiple times under slightly different names or account numbers, multiplying the damage across your report. This error inflates how much credit you appear to be using, which lenders view as a red flag.

Gather documentation showing the accounts are identical and request removal of duplicates from the bureau. Provide clear evidence that links the accounts to the same original debt. The credit bureau must investigate your claim within 30 days and correct the error if your documentation proves the accounts are duplicates.

Incorrect Payment Histories and Late Marks

Incorrect payment histories and late marks plague roughly one in five South Carolina consumers according to Federal Trade Commission data. A single missed payment mark can stay on your report for seven years and raise your interest rates substantially. Even one inaccurate late payment can cost you thousands in higher borrowing costs over time.

Collect actual payment proof like bank statements and cancelled checks, then dispute both the bureau and the furnisher simultaneously to build a solid paper trail. Send your dispute by certified mail with return receipt to create documented evidence that the bureau received your claim. This dual approach increases the likelihood that the error gets corrected within the 30-day investigation window.

Personal Information Errors and Address Discrepancies

Personal information errors seem minor but they create real obstacles. Misspelled names, wrong addresses, or outdated employment details can lead to identity verification failures when you apply for credit. These errors also make you vulnerable to someone else’s negative information being mixed into your file.

Review your reports from Equifax, Experian, and TransUnion carefully and correct any discrepancies immediately. South Carolina ranks as the 13th highest state for identity theft reports per 100,000 residents according to the South Carolina Department of Revenue, making accuracy even more critical. Address discrepancies deserve special attention because creditors must verify a changed address before opening new accounts or issuing additional cards. If your address changed and the bureau hasn’t updated it, submit corrections in writing to prevent fraudsters from using old addresses to apply for credit in your name.

Once you understand what errors commonly appear on South Carolina credit reports, the next step involves pulling your actual reports and identifying which mistakes affect your file.

How to Access and Review Your Credit Reports, Serving South Carolina, Including Greenville, Columbia and Charleston

Obtain Your Free Annual Credit Reports

Start with annualcreditreport.com, the only official source for free annual credit reports from Equifax, Experian, and TransUnion. The Federal Trade Commission manages this site and it’s the only legitimate place to claim your guaranteed free reports. Pull all three reports at once rather than spacing them out, because errors often appear on one bureau’s file but not the others. This simultaneous approach gives you a complete picture of what creditors see about you.

South Carolina residents also benefit from an additional six free reports per year through Equifax until 2026, so take advantage of these extra checks beyond your annual allotment. The CFPB recorded 20,406 complaints in South Carolina specifically about incorrect information on consumer credit reports, demonstrating how widespread these errors are across the state.

Document and Organize Your Findings

When you pull your reports, print or save digital copies immediately and mark any accounts or details you don’t recognize. Create a separate file for each disputed item so you can track disputes individually and reference them later if bureaus claim they investigated and found nothing wrong.

Scan each report line by line for unfamiliar accounts, duplicate listings, wrong payment statuses, misspelled names, incorrect addresses, or accounts you closed that still show as open. Look for accounts from creditors you never contacted and verify every late payment mark against your actual payment records. Document everything you find by writing down the creditor name, account number, the error description, and the date you spotted it.

File Your Dispute With Supporting Evidence

Send your written dispute to the bureau by certified mail with return receipt requested, include a circled copy of the error on your report, and attach supporting documents like bank statements or payment receipts. South Carolina law requires credit bureaus to provide the basis for denial if they reject your dispute, a copy of your revised file, a description of their investigation procedure, and any evidence supporting their decision.

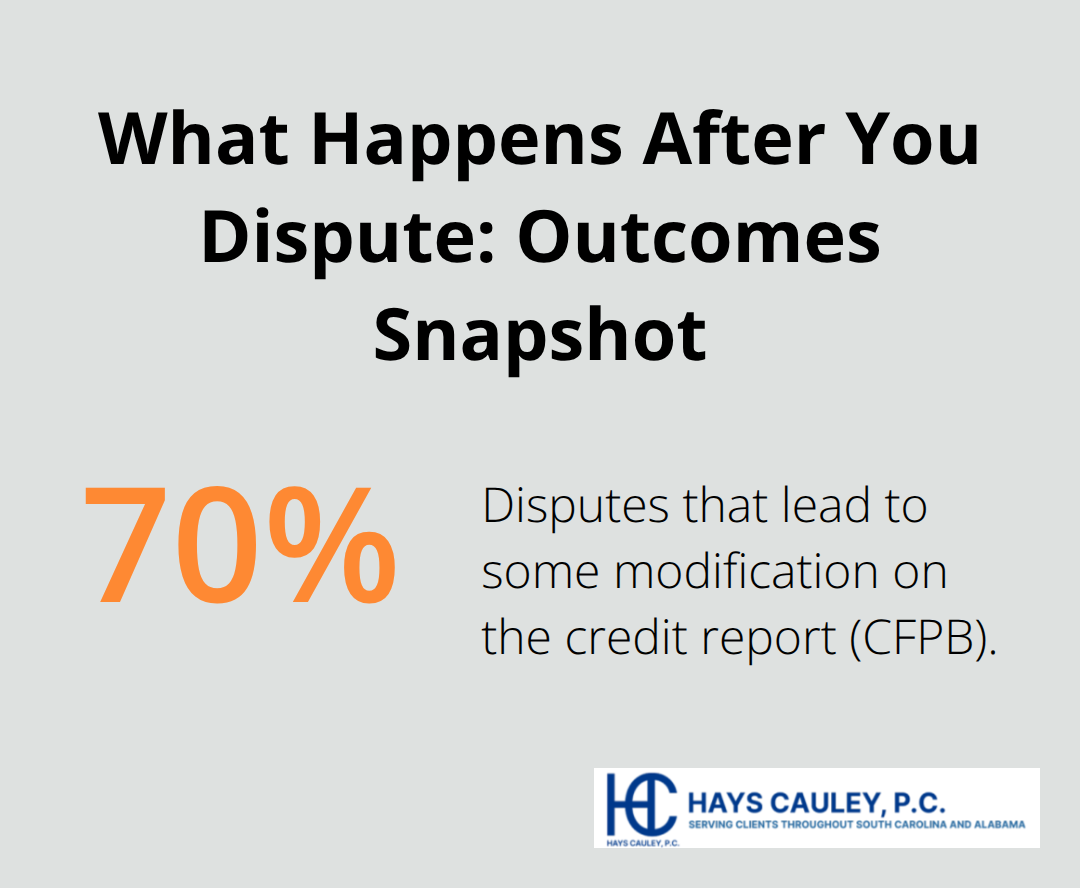

The CFPB noted that about 70 percent of disputes lead to some modification on the credit report, but persistence increases your chances of full correction. If the bureau dismisses your dispute as frivolous or ignores it entirely, file a second dispute with stronger documentation and reference your original dispute to show you’ve already raised this issue.

Once you file your dispute, the bureau must respond within 30 days and either correct the error or explain why they believe the information is accurate. Understanding what happens next in the dispute process and knowing your legal rights under federal law will help you navigate the investigation and hold the bureau accountable if they fail to act.

What the Fair Credit Reporting Act Actually Guarantees You

The 30-Day Investigation Window and Your Legal Leverage

The Fair Credit Reporting Act gives you the power to challenge inaccurate information on your credit report, and the statute includes teeth that punish bureaus for ignoring your rights. Credit bureaus and furnishers must investigate your dispute within 30 days and correct verified errors at no cost to you. If they fail to correct a legitimate error after proper investigation, you can sue for actual damages plus statutory damages up to $1,000 per violation, and the bureau must pay your attorney’s fees. South Carolina law layers additional protection on top of federal protections, requiring bureaus to provide the basis for denial if they reject your dispute, a copy of your revised file, and documentation of their investigation procedure. The CFPB returned $17.5 billion to wronged consumers across all 50 states, showing that legal action produces real results when bureaus violate these rules.

Willful and Negligent Violations: What You Can Recover

Your 30-day window after filing a dispute determines whether you can pursue damages. If the bureau ignores your dispute entirely or dismisses it as frivolous without proper investigation, you have grounds for a willful violation claim that can triple your actual damages or yield $3,000 per incident plus attorney fees. Negligent violations entitle you to at least $1,000 per incident plus attorney fees. If a judgment is entered against the bureau for inaccurate information and they fail to remove it within ten days, damages accumulate at $1,000 per day until correction occurs.

Building Your Paper Trail for Legal Action

Send your dispute by certified mail with return receipt to create documented proof of delivery, because this paper trail becomes essential if litigation becomes necessary. The CFPB complaint process offers a faster escalation path if the bureau’s investigation seems incomplete, and the agency typically responds within 15 business days. After filing a CFPB complaint, the bureau must respond and you can reference their inadequate response in future legal action.

Acting Promptly Protects Your Rights

South Carolina consumers have strong legal leverage here, but you must act promptly and document everything because your rights depend on proving the bureau received your dispute and failed to investigate properly.

Final Thoughts

South Carolina credit report errors demand swift action to protect your financial future. Pull all three reports from annualcreditreport.com, mark every discrepancy, and send written disputes by certified mail with supporting documentation to each bureau. The 30-day investigation window represents your critical deadline, so file your dispute promptly and retain copies of everything you submit.

The CFPB recorded over 45,000 credit-reporting complaints in South Carolina, with incorrect information on consumer reports accounting for the largest share of those complaints. You hold powerful federal protections under the Fair Credit Reporting Act, including the right to sue for actual damages plus statutory damages up to $1,000 per violation when bureaus willfully ignore your dispute. South Carolina law adds additional safeguards that require bureaus to provide detailed explanations if they deny your dispute.

If you’ve filed disputes and the bureaus still refuse to correct South Carolina credit report errors, contact Hays Cauley, P.C. to discuss your options and protect your rights. We help South Carolina residents challenge inaccuracies, hold credit bureaus accountable, and recover damages when bureaus fail to correct verified errors.