Credit bureaus reporting errors: How to Fix Mistakes Across Bureaus

Credit bureaus reporting errors can tank your credit score without warning. A single mistake-a missed payment that never happened, an account opened in your name, or a balance reported incorrectly-can cost you thousands in higher interest rates.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, fight back against these errors. This guide walks you through identifying mistakes, disputing them with the bureaus, and protecting your financial future.

Where Credit Report Errors Actually Come From

How Furnishers Contaminate Your Credit File

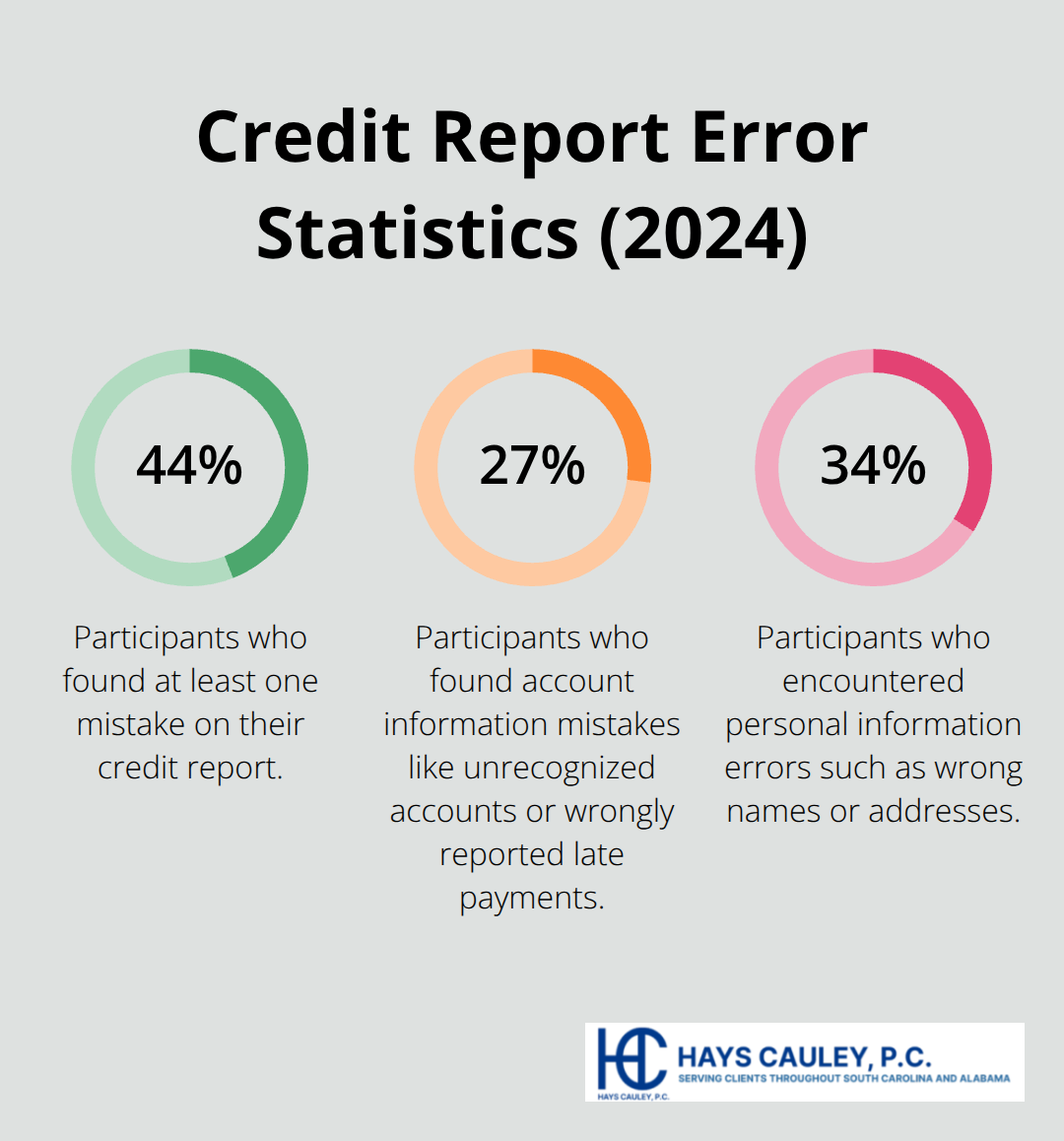

Credit bureaus don’t create errors out of thin air. They compile information from creditors, lenders, debt collectors, and landlords-what the industry calls furnishers. When any of these sources report incorrect data, the bureaus simply pass it along. A 2024 Consumer Reports and WorkMoney study of over 4,000 participants found that 44% of people checking their credit reports discovered at least one mistake. The most damaging errors were account information mistakes, with 27% of participants finding unrecognized accounts, incorrectly reported late payments, or debts that didn’t belong to them listed as collections.

Personal Information Errors Add to the Problem

Another 34% of study participants encountered personal information errors like wrong names or addresses. These aren’t rare glitches-they’re systemic problems that affect nearly half of all credit reports. The CFPB reported that credit reporting complaints jumped from 165,129 in 2021 to 430,600 in 2023, making credit reporting errors the top consumer complaint for three consecutive years. This explosion in complaints reflects a growing recognition that the system is broken and furnishers aren’t matching enough personal information before reporting accounts.

Why Errors Spread Across All Three Bureaus

The spread across all three bureaus happens because furnishers report the same incorrect information to Equifax, Experian, and TransUnion simultaneously. A single mistake from one creditor contaminates all three reports at once. Mixed files represent another critical failure point-when information from someone with a similar name or Social Security number gets blended into your file, or when fraudulent accounts appear due to identity theft.

The Real Cost of Inaccurate Reporting

When errors exist on your report, they directly suppress your credit score, making it harder to qualify for affordable credit and affecting your ability to secure housing, employment, or favorable insurance rates. The damage compounds because lenders, employers, and insurers all pull from these same contaminated reports. Understanding where these errors originate sets the stage for taking action-and that action starts with obtaining your actual reports to see what furnishers have reported about you.

Getting Your Reports and Finding What’s Wrong

Access Your Credit Reports from All Three Bureaus

Visit annualcreditreport.com, the only federally authorized source for free credit reports from Equifax, Experian, and TransUnion. You can pull one free report from each bureau every 12 months, though Equifax currently offers six free reports annually through 2026. Pull all three reports at the same time so you can compare them side by side. This matters because errors don’t always appear uniformly across all three bureaus-a missed payment reported to Equifax might not show up on Experian, or an unrecognized account could contaminate only TransUnion’s file.

Scan for Identity and Account Errors

Check for identity errors first: wrong name, phone number, or address. Then look for mixed files where accounts from someone with a similar name or Social Security number got blended into your report. Scan for accounts you don’t recognize that could signal identity theft. Verify that closed accounts aren’t still reported as open, and confirm you’re only listed as the owner of accounts you actually own rather than accounts where you’re merely an authorized user.

Verify Dates, Balances, and Payment Status

Check whether accounts are incorrectly marked as late or delinquent, and verify dates like the last payment date, account opening date, and first delinquency date. Watch for duplicate debts appearing under different names and confirm that current balances and credit limits are accurate. These details matter because even small inaccuracies can suppress your score and trigger denial of credit applications.

Gather Documentation Before You Dispute

Once you spot an error, collect supporting documentation before you dispute. Pull statements, payment confirmations, or correspondence from the creditor that proves the information on your report is wrong. If you’re contesting a late payment that never happened, obtain your bank statements showing on-time payments. If you’re challenging an account you didn’t open, collect written evidence that the account is fraudulent. Write down the exact date you discovered the error and which bureau reported it incorrectly.

File Your Dispute with Each Bureau

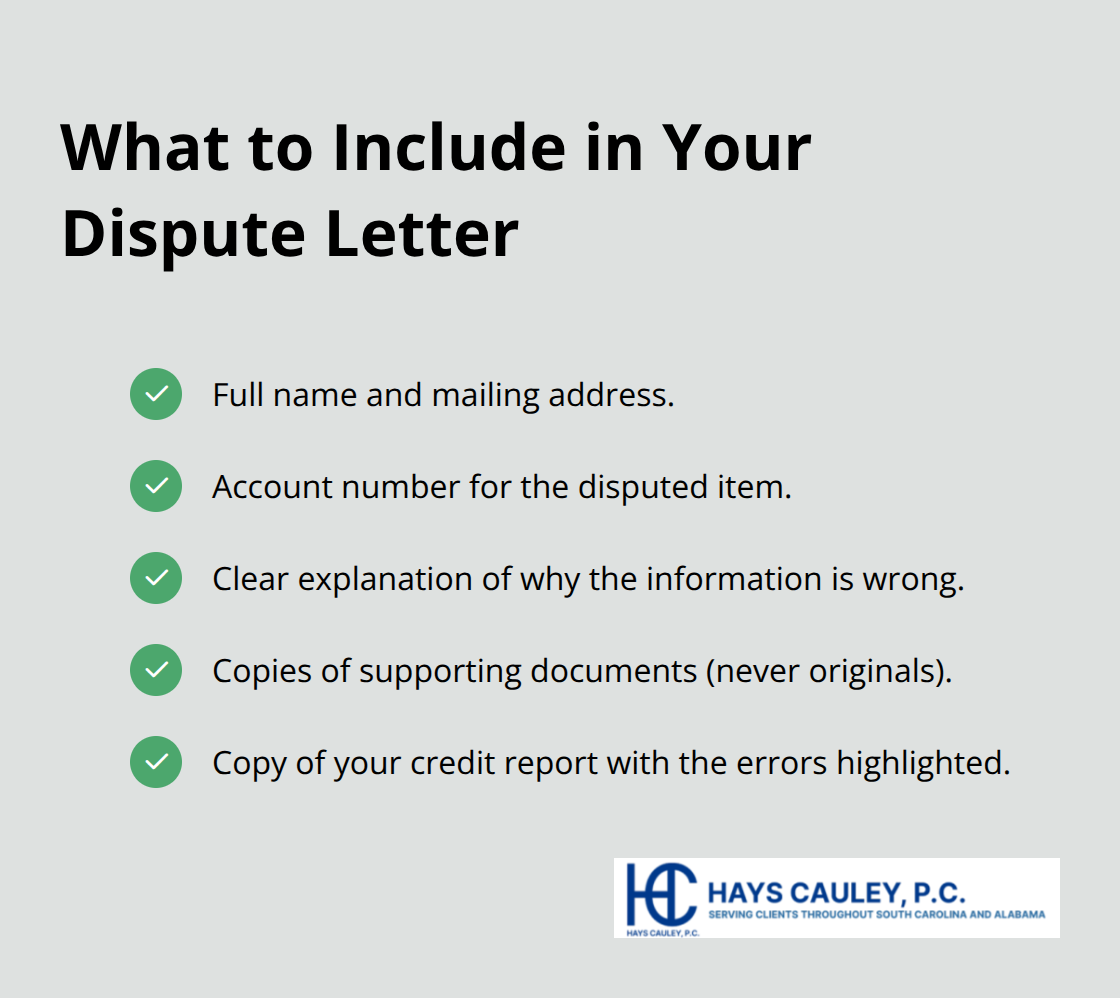

Send disputes to each bureau that shows the mistake using certified mail with return receipt. Address Equifax at P.O. Box 740256, Atlanta, GA 30348; Experian at P.O. Box 4500, Allen, TX 75013; and TransUnion at P.O. Box 2000, Chester, PA 19016. In your dispute letter, include your full name and address, the account number for the disputed item, a clear explanation of why the information is wrong, copies (not originals) of supporting documents, and a copy of your report with the errors circled or highlighted.

The bureaus have 30 days to investigate, though they can stop if they deem your dispute frivolous. After the investigation closes, monitor your reports to confirm corrections appeared across all three bureaus-and if they didn’t, you’ll need to escalate your complaint directly to the creditors who reported the false information.

How to Turn Disputes into Corrections

Understanding How the Dispute Process Works

The dispute process with credit bureaus differs fundamentally from disputing with creditors, and understanding this distinction saves time and increases your odds of success. When you file a dispute with Equifax, Experian, or TransUnion, the bureau investigates by forwarding your complaint to the furnisher that reported the information. The furnisher then has 30 days to respond and either confirm the data is accurate or correct it. This means the bureau acts as an intermediary rather than making the final call themselves.

If the furnisher confirms the information is accurate, the bureau closes the dispute in the furnisher’s favor, and your error remains on your report. This is why many disputes fail-furnishers often rubber-stamp their original reports without genuine investigation. The Fair Credit Reporting Act grants you the explicit right to dispute inaccurate information, and furnishers must investigate your claims, but the law doesn’t require them to investigate thoroughly or remove information simply because you disagree with it.

Filing Your Dispute with the Right Documentation

Send your dispute letter to the specific bureau address via certified mail with return receipt requested. This creates proof the bureau received your complaint on a specific date, which matters if you need to escalate later. Include a copy of your credit report with the error circled, your full contact information, the account number of the disputed item, a clear explanation of why the information is wrong, and copies of supporting documents. If the bureau deems your dispute frivolous or irrelevant, it must notify you within five business days and explain why it stops the investigation.

Monitoring Results and Following Up

After the 30-day investigation period closes, the bureau sends you written results and a free updated copy of your report if changes were made. Monitor that updated report carefully-corrections don’t always appear on the first try, and some furnishers reinsert incorrect information months later. If the same error persists after disputing with the bureau, contact the furnisher directly in writing using certified mail. Send your furnisher dispute to the address listed on your credit report or the company’s designated credit dispute address.

Escalating When Disputes Fail

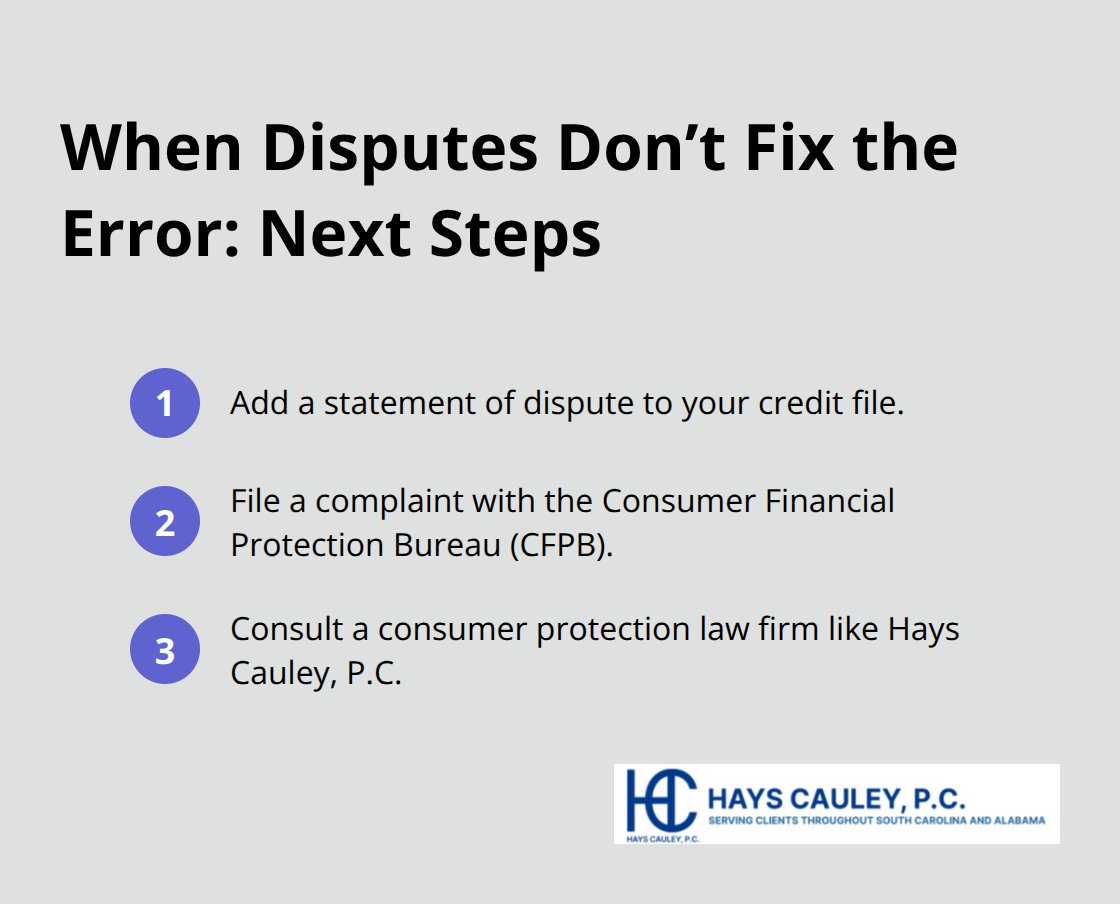

Furnishers typically respond within 30 days, and if they determine the information is inaccurate, they must notify all three bureaus to correct or delete it. If disputes still don’t resolve the problem, add a statement of dispute to your credit file that appears on all future reports (though this approach is weaker than actual removal because lenders still see the disputed item alongside your explanation). When standard disputes fail to produce results, you have additional options-filing a complaint with the Consumer Financial Protection Bureau or consulting with a consumer protection law firm like Hays Cauley, P.C. that handles credit reporting disputes can accelerate the correction process and hold furnishers accountable for their failures.

Final Thoughts

Fixing credit bureaus reporting errors requires persistence, but the process is straightforward once you understand how it works. You obtain your reports from all three bureaus, identify mistakes, gather supporting documentation, and file disputes with each bureau that shows the error. The bureaus forward your complaint to the furnisher, which has 30 days to investigate and respond. If the furnisher confirms the error, all three bureaus must update your report.

Long-term protection starts with monitoring your credit reports at least once annually through annualcreditreport.com, and consider pulling reports every few months if you’ve recently disputed errors. Watch for patterns-if the same furnisher repeatedly reports inaccurate information, that’s evidence of systemic negligence worth documenting. Set calendar reminders to verify that corrections actually appeared on your reports after disputes close, because some furnishers reinsert incorrect information months later.

When disputes stall or furnishers ignore your complaints, you need professional help. We at Hays Cauley, P.C. hold furnishers and bureaus accountable when they fail to correct errors, and we serve South Carolina, including Greenville, Columbia, and Charleston. Contact Hays Cauley, P.C. to discuss your situation if you’ve disputed errors without success or suspect systematic violations of the Fair Credit Reporting Act.