How to Recover from Identity Theft: A Complete Guide

Identity theft affects millions of Americans each year, and the financial and emotional toll can be devastating. The good news is that you can recover from identity theft with the right steps and support.

At Hays Cauley, P.C., we’ve helped countless South Carolina residents navigate this process. This guide walks you through immediate actions, credit repair, and legal protections you need to know.

Act Fast When Identity Theft Strikes: Serving South Carolina, including Greenville, Columbia and Charleston

The first 24 hours after discovering identity theft matter far more than most people realize. Your immediate actions directly determine how much financial damage you’ll face and how quickly you can regain control.

Contact Your Bank and Credit Card Companies Immediately

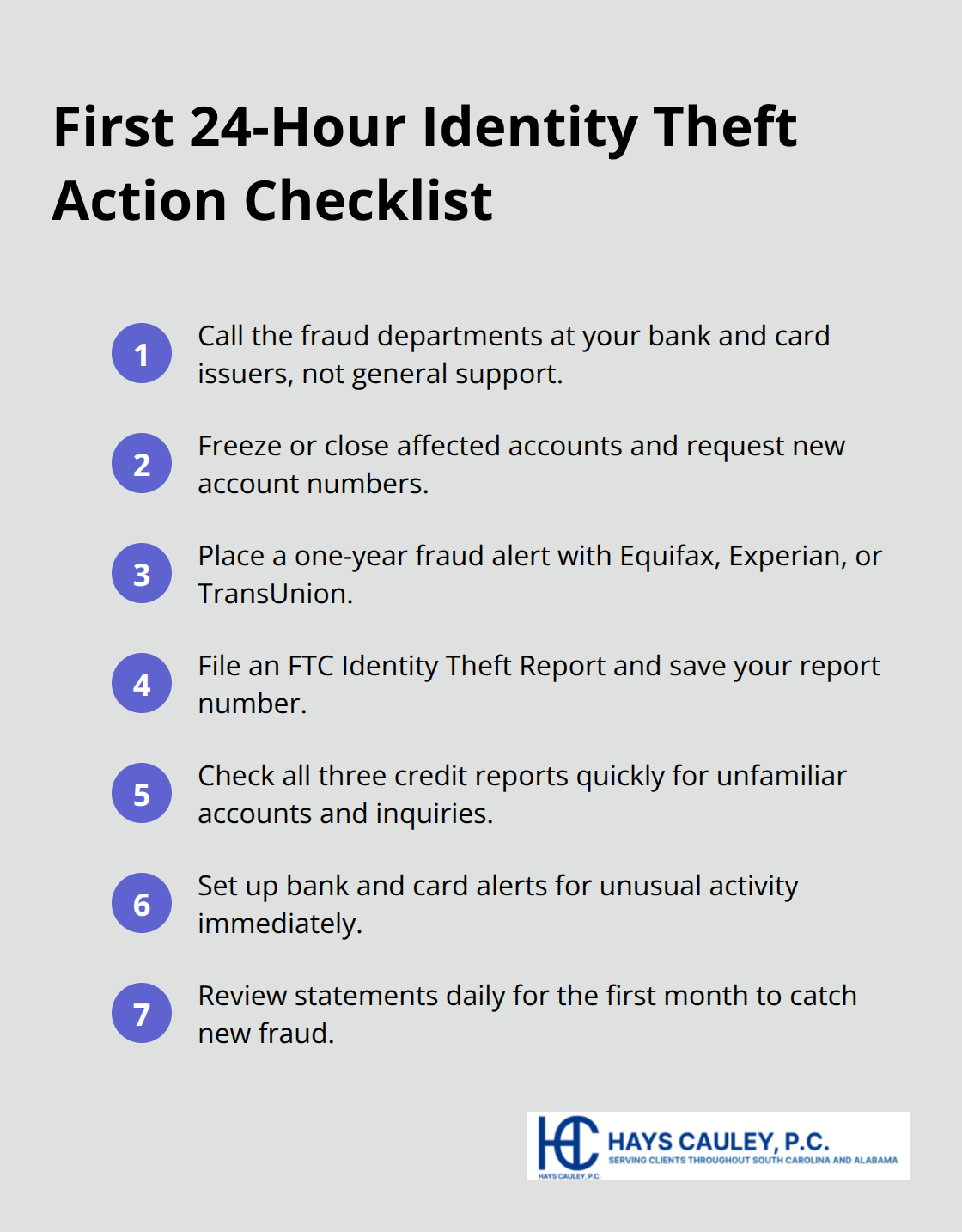

Call the fraud department at your bank and credit card companies before doing anything else-not the general customer service line. Report the theft verbally, then follow up with written confirmation via email or certified mail. The Federal Trade Commission reports that victims who act within one day of discovery experience significantly lower unauthorized charges than those who wait.

Request that your accounts be frozen or closed immediately. Ask for new account numbers and demand that the issuer flag your file to prevent additional fraudulent activity. Speaking directly with a fraud representative ensures your case receives priority attention and creates a documented record of your report. Do not rely on online chat or email alone for this critical step.

Report to Credit Bureaus and the FTC Without Delay

Place a fraud alert with all three major credit bureaus-Equifax, Experian, and TransUnion-on the same day you discover the theft. A one-year fraud alert costs nothing and alerts lenders that you may be a victim, requiring them to verify your identity before opening new accounts in your name. You only need to contact one bureau; that bureau must notify the other two by law.

File your Identity Theft Report with the Federal Trade Commission, which generates a personalized recovery plan tailored to your specific situation and provides legal documentation that creditors must accept when disputing fraudulent accounts. The FTC processes these reports free of charge and provides step-by-step guidance for each type of fraud. Keep your FTC report number handy-you’ll reference it repeatedly when contacting creditors and credit bureaus.

If the theft involves tax-related fraud, file Form 14039 with the IRS immediately to protect your tax records and request an Identity Protection PIN for future returns.

Monitor for New Fraud While Taking Action

Check your credit reports from all three bureaus at annualcreditreport.com within days of reporting the theft. During a fraud alert, you’re entitled to additional free reports beyond the standard annual report. Look specifically for accounts you did not open, hard inquiries from lenders you never contacted, and address changes you did not authorize.

Contact affected banks and creditors directly with your FTC report and Identity Theft Report to dispute fraudulent accounts. Under the Fair Credit Reporting Act, lenders have 30 days to investigate your dispute. Request written confirmation that fraudulent accounts have been closed and ask each company to send you updated statements showing zero balances on disputed charges.

Many victims overlook government benefits and Social Security records-contact the Social Security Administration to verify your earnings record and check for unauthorized benefits claims. Set up account alerts with your banks and credit card companies to receive notifications of unusual activity. Plan to review statements daily for at least the first month after discovery (and continue monitoring for 12–24 months to catch delayed fraud).

Your credit repair efforts begin in parallel with these immediate steps, and the documentation you gather now will support every dispute you file moving forward.

Rebuild Your Credit After Identity Theft: Serving South Carolina, including Greenville, Columbia and Charleston

Your credit reports are now your battlefield. These three documents from Equifax, Experian, and TransUnion determine whether lenders will approve you for mortgages, car loans, credit cards, and even rental agreements. After identity theft, fraudulent accounts and inquiries will damage your scores, sometimes by 100 points or more depending on the severity. The FTC reports that the average identity theft victim spends 100 to 200 hours resolving the damage. You cannot afford to move slowly here.

Pull Your Credit Reports and Document Every Fraudulent Item

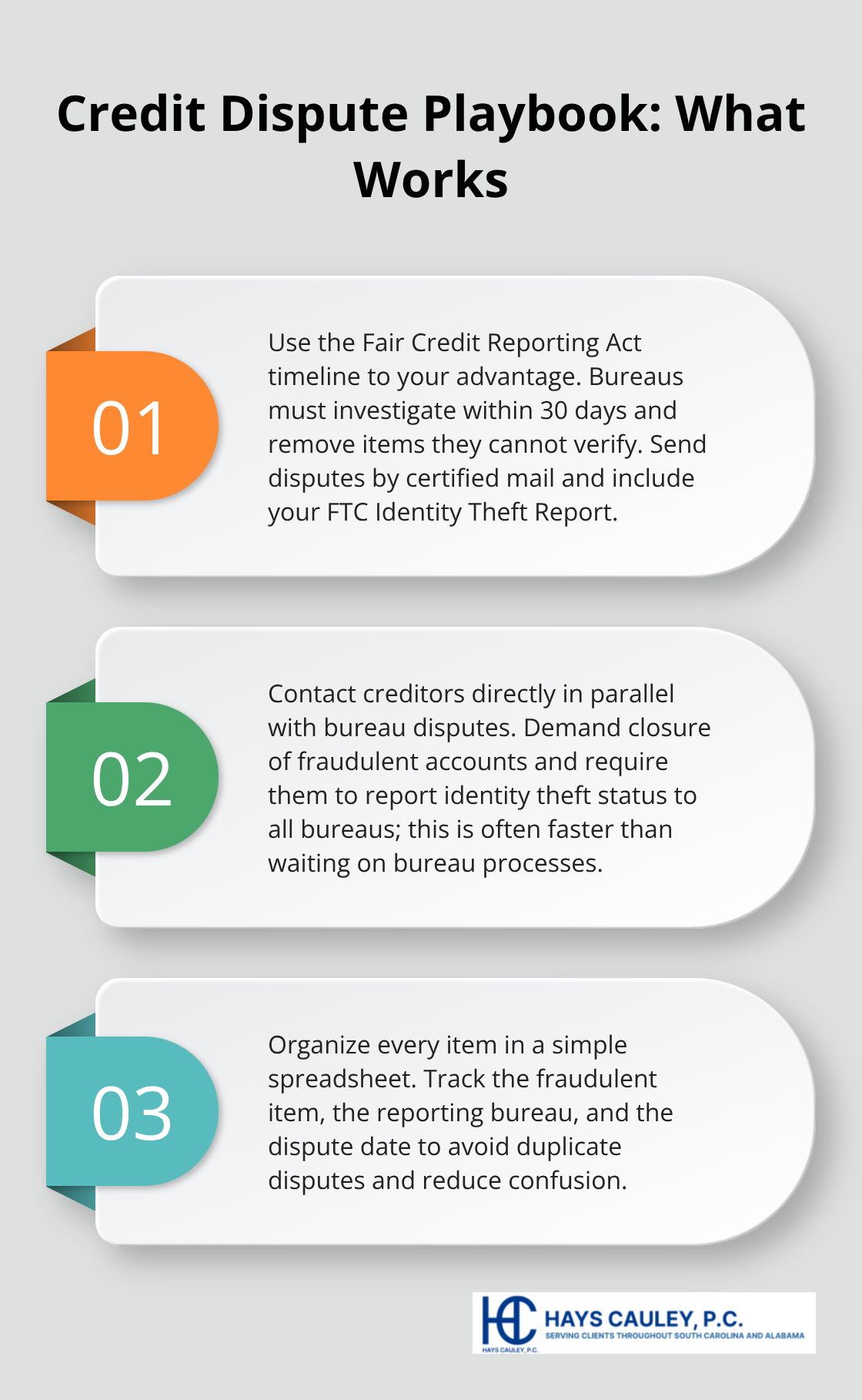

Pull your free credit reports from annualcreditreport.com immediately and print physical copies. Look for every account you do not recognize, every hard inquiry from lenders you never contacted, and every address change that is not yours. Mark these items directly on your printed reports because you will reference them constantly over the next weeks. Create a spreadsheet with three columns: the fraudulent item, the bureau reporting it, and the date you disputed it.

This document becomes your recovery roadmap and protects you from disputing the same item twice, which wastes time and confuses creditors.

Send Written Disputes to Credit Bureaus and Creditors

Send written disputes to each credit bureau within 30 days of obtaining your report, including a copy of your FTC Identity Theft Report and a clear explanation of why each item is fraudulent. The Fair Credit Reporting Act requires bureaus to investigate your dispute within 30 days and remove items that cannot be verified. Send your disputes via certified mail with return receipt requested so you have proof of delivery (do not rely on online dispute forms alone). Contact the creditor that issued each fraudulent account directly and send the same documentation. Demand that they close the account and report it to the bureaus as a result of identity theft. Many creditors will comply faster when contacted directly than when the bureau contacts them on your behalf.

Monitor Your Reports Obsessively for 12 to 24 Months

Monitor your credit reports obsessively for the next 12 to 24 months. Identity thieves sometimes open accounts months after the initial theft, and fraudulent items occasionally reappear after removal. Set up free credit monitoring through the FTC or your credit card issuer, and configure alerts for any new inquiries or account openings. Check your three reports every three months on a rotating schedule so you catch problems quickly.

Understand Your Legal Protections in South Carolina

South Carolina law defines identity fraud as a felony with penalties up to 10 years imprisonment, which means law enforcement takes these cases seriously if you file a police report and provide documentation. If you face persistent fraud or significant financial losses, a consumer protection attorney can help you document fraud patterns and pursue restitution from perpetrators when prosecution occurs. Your next step involves understanding the legal options available to you and how to protect yourself from future identity theft.

Protect Yourself Legally and Prevent Future Identity Theft: Serving South Carolina, including Greenville, Columbia and Charleston

Know Your Rights Under the Fair Credit Reporting Act

The Fair Credit Reporting Act grants you powerful protections that most identity theft victims never fully use. Credit bureaus must investigate disputed items within 30 days and remove anything they cannot verify as accurate. You can sue credit bureaus and creditors for violations that cause financial or emotional harm-courts have awarded damages ranging from hundreds to thousands of dollars in successful cases. If a credit bureau ignores your dispute or a creditor fails to investigate, document everything and consider consulting a consumer protection attorney. These violations happen more often than you’d expect, and creditors count on victims not knowing their rights.

Freeze Your Credit to Block New Accounts

A credit freeze represents your strongest defense against future identity theft because it prevents anyone from opening new accounts in your name without your explicit permission. Unlike a fraud alert (which simply requires lenders to verify your identity), a freeze blocks account creation entirely. You maintain PIN-protected access to unfreeze your credit when you need to apply for legitimate credit. Freezes cost nothing in South Carolina and remain in place until you remove them.

The Federal Trade Commission recommends freezes for all identity theft victims because they eliminate the most common form of post-theft fraud. An extended fraud alert lasts seven years instead of one year, but a freeze offers superior protection.

Pursue Legal Action When Losses Mount

If you face ongoing fraud or significant losses exceeding $1,000, a consumer protection attorney becomes essential. These attorneys identify patterns of fraudulent activity that individual disputes might miss, file police reports that strengthen your legal position, and pursue restitution from perpetrators when law enforcement makes arrests. Many attorneys work on contingency or charge modest flat fees for identity theft cases. South Carolina law treats identity fraud as a felony with sentences up to 10 years, which means prosecutors take documented cases seriously and can order perpetrators to repay victims. An attorney also protects you from liability if creditors attempt to hold you responsible for fraudulent accounts after you’ve provided proper documentation.

Sustain Your Recovery Effort Over Months

Your recovery requires sustained effort over months, not days, and these legal protections ensure you’re not fighting this battle alone. Stay organized, follow up with creditors consistently, and maintain records of all disputes and communications. The process tests your patience, but the legal framework exists to support your claims and hold wrongdoers accountable.

Conclusion

Identity theft recovery spans weeks to months, not days. Your immediate actions in the first 24 hours-contacting banks, placing fraud alerts, and filing your FTC report-stop the bleeding and create the legal documentation you need. The next phase involves disputing fraudulent accounts with credit bureaus and creditors, a process that typically takes 30 to 90 days per dispute. Finally, monitoring your credit reports for 12 to 24 months catches delayed fraud that thieves sometimes introduce months after the initial theft.

Ongoing vigilance separates victims who fully recover from identity theft from those who face repeated fraud. Set up account alerts with your banks and credit card companies, review statements monthly even after you believe the theft is resolved, and check your credit reports on a rotating schedule every three months. A credit freeze provides the strongest long-term protection because it blocks new account creation entirely, eliminating the most common form of post-theft fraud. Your Social Security number, driver’s license number, and financial account information remain valuable to criminals indefinitely, so protection must become a permanent habit rather than a temporary response.

South Carolina treats identity fraud as a felony with sentences up to 10 years, meaning law enforcement takes documented cases seriously and can order perpetrators to repay victims through restitution. If you face persistent fraud or losses exceeding $1,000, contact Hays Cauley, P.C. to discuss your situation and explore your legal options. You don’t have to navigate this process alone, and the right support makes recovery faster and more complete.