Best credit report attorney: How to Choose the Right Lawyer

Your credit report shapes your financial life. Errors, fraud, or disputes on your report can cost you thousands in higher interest rates or denied loans.

We at Hays Cauley, P.C. help South Carolina residents fix these problems. Finding the best credit report attorney means knowing what to look for-and this guide walks you through exactly that.

What Separates Good Credit Report Attorneys from the Rest

Track Record Against Major Credit Bureaus

The difference between a mediocre credit report attorney and one who actually wins cases comes down to three concrete factors. First, look for an attorney with a documented track record against the major credit bureaus-Experian, Equifax, and TransUnion. Ask directly about cases involving mixed-file errors or identity theft claims, since these are among the most damaging violations under the Fair Credit Reporting Act. Mixed-file errors alone can drop your credit score by 100 points or more, so you need someone who understands how to pursue these aggressively.

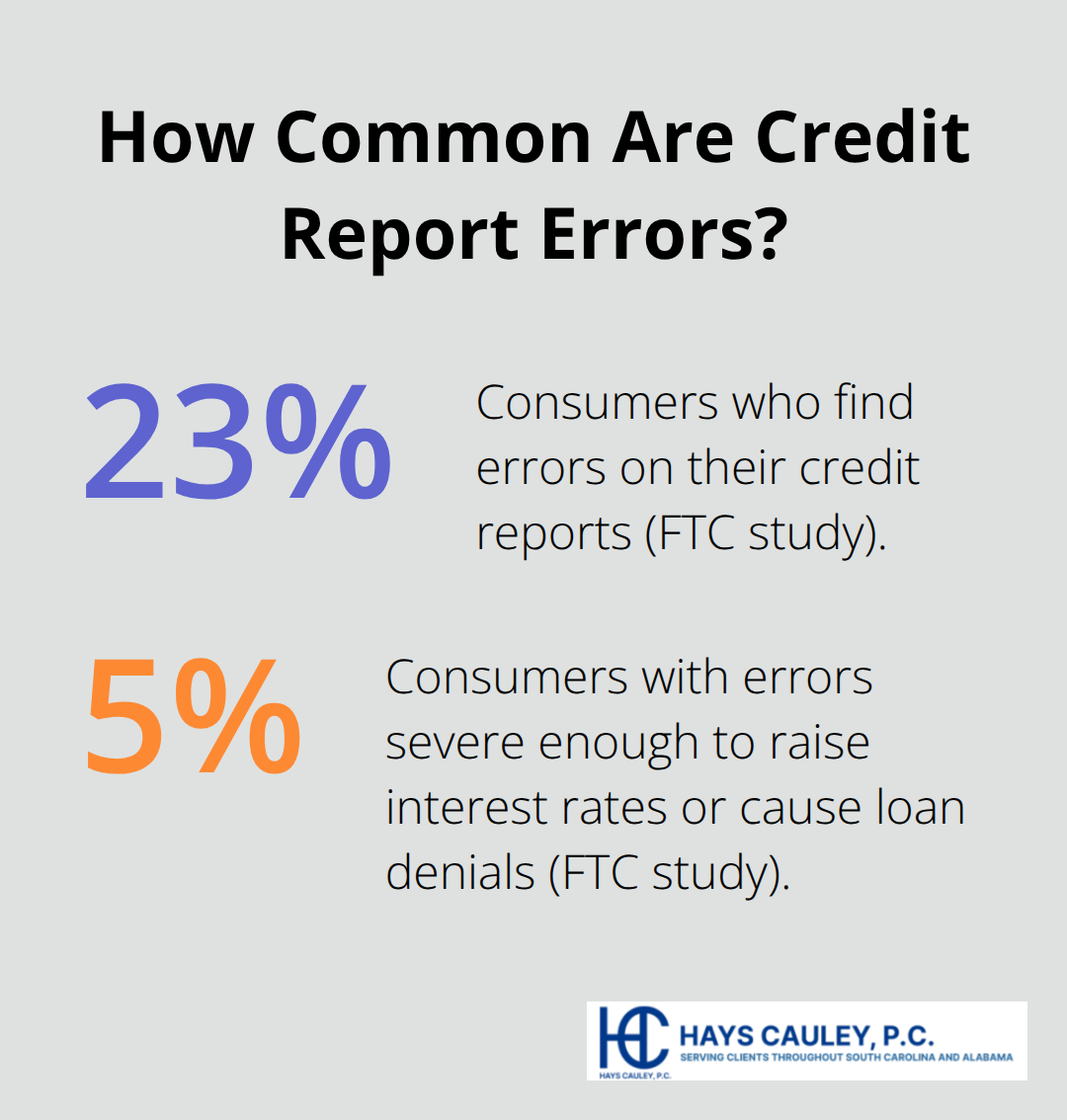

The FTC study shows that 23% of consumers find errors on their credit reports, and 5% have errors severe enough to raise interest rates or cause loan denials. An attorney worth hiring should cite specific settlements they’ve achieved, not vague promises about what might happen. When you ask about their experience, they should explain the difference between negligent violations (which carry $100 to $1,000 per violation) and willful violations (which can trigger six-figure punitive damages). The Ramirez v. TransUnion case resulted in a $60 million verdict, demonstrating the scale of recoveries possible when bureaus act with willful disregard.

Deep Knowledge of Fair Credit Reporting Act and State Law

Second, demand evidence of their understanding of the Fair Credit Reporting Act and South Carolina state laws. An attorney should walk you through exactly how disputes work: the bureau has 30 days to investigate, the furnisher must report back, and if the bureau ignores a valid dispute or reinstates deleted information without notice, that’s grounds for legal action. Many attorneys focus on unrelated practice areas and lack true Fair Credit Reporting Act depth-avoid them. Effective identity theft lawyers distinguish themselves by asking about case volume and credit bureau experience during your consultation.

Proven Results Through Client Examples

Third, request actual client testimonials or case examples showing reinsertion of deleted information or disputes the bureau initially deemed frivolous. Reviews matter less than concrete examples of what the attorney accomplished. During your initial consultation, ask whether the attorney will personally handle your case or delegate to associates. Ask about their typical timeline for settlements-most Fair Credit Reporting Act lawsuits resolve in 8 to 18 months-and what their fee structure is.

Fee Arrangements and Red Flags

Contingency arrangements are common in these cases, typically running 33 to 40% of recovery, which means you pay nothing upfront. Red flags include attorneys who promise specific settlement amounts before reviewing your case, those who lack genuine Fair Credit Reporting Act litigation experience, or those who won’t discuss the strengths and weaknesses of your claim honestly. When you’ve identified attorneys who meet these standards, the next step involves evaluating how they communicate and whether their approach aligns with your needs.

Problems an Attorney Can Fix on Your Credit Report

Inaccurate Information That Costs You Money

Inaccurate information on your credit report is expensive. The FTC found that 5% of consumers have errors severe enough to raise interest rates or cause loan denials, costing thousands in higher borrowing costs and lost opportunities. Late payment errors on accounts you actually paid on time can drop your credit score by 60 to 110 points per incident. Mixed-file errors-where another person’s information appears on your report-rank among the most damaging violations, often causing score drops exceeding 100 points.

An attorney becomes necessary when the credit bureau ignores your dispute or when you’ve already sent letters to Experian, Equifax, or TransUnion without resolution. The bureaus have 30 days to investigate disputes, and if they give you a form-letter response, reinstate deleted information without notice, or determine your dispute is frivolous when it clearly isn’t, that’s grounds for legal action. You can fix credit report errors on your own first, but persistent inaction from bureaus requires legal intervention.

Identity Theft and Fraudulent Accounts

Identity theft demands immediate legal intervention because fraudulent accounts can tank your score and open you to liability. If someone opens credit cards or loans in your name, the bureaus must remove those accounts once you provide proper documentation of the fraud, but many fail to do so. An identity theft attorney can force the bureaus to comply and pursue damages if they’ve been negligent or willful in their violations.

Stalled Disputes and Bureau Inaction

Disputes with credit bureaus stall when you’re dealing with them alone. The bureaus must forward your dispute to the furnisher, which must investigate and report back within 30 days, but many furnishers ignore disputes or send back vague responses that don’t actually address your claim. If the furnisher continues reporting inaccurate information after your dispute, you can request the bureau add a dispute notice to your file, but this doesn’t remove the error-it just flags it.

An attorney knows how to identify when bureaus break the law, such as when they fail to investigate adequately or reinstate information you’ve already disputed. Under the Fair Credit Reporting Act, negligent violations carry statutory damages of $100 to $1,000 per violation, while willful violations can trigger punitive damages reaching six figures. Most lawsuits settle within 8 to 18 months, with typical settlements for mixed-file and identity theft claims ranging from $25,000 to $100,000.

Acting Within Legal Deadlines

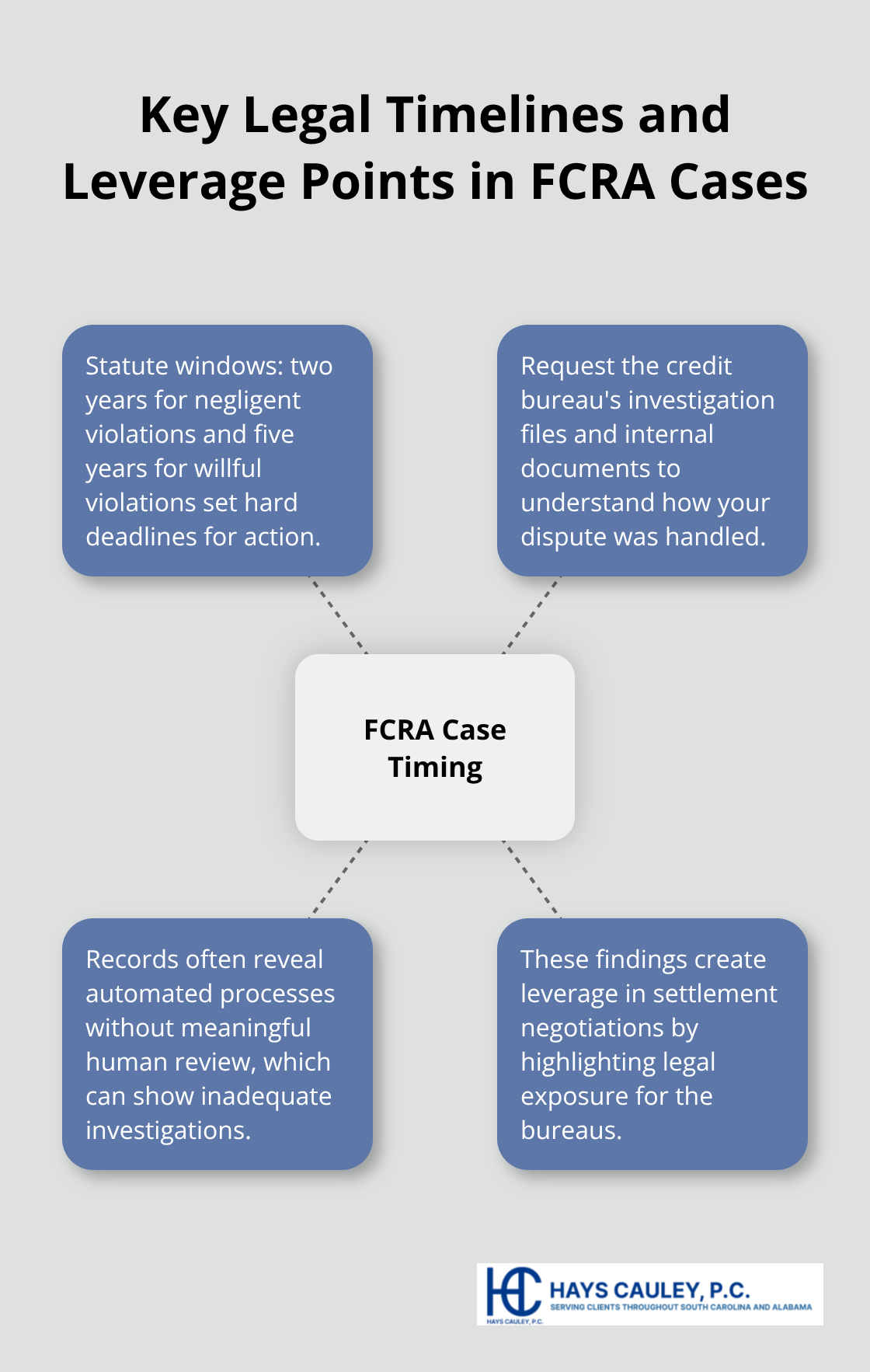

The key is acting within the statute of limitations-two years for negligent violations and five years for willful violations-and having an attorney who can request the credit bureau’s investigation files and internal documents. These documents often reveal automated processes without meaningful human review, giving you leverage in settlement negotiations. Understanding what an attorney can accomplish sets the stage for evaluating which lawyer fits your situation best.

How to Evaluate and Compare Credit Report Attorneys: Serving South Carolina, Including Greenville, Columbia and Charleston

What to Ask During Your Initial Consultation

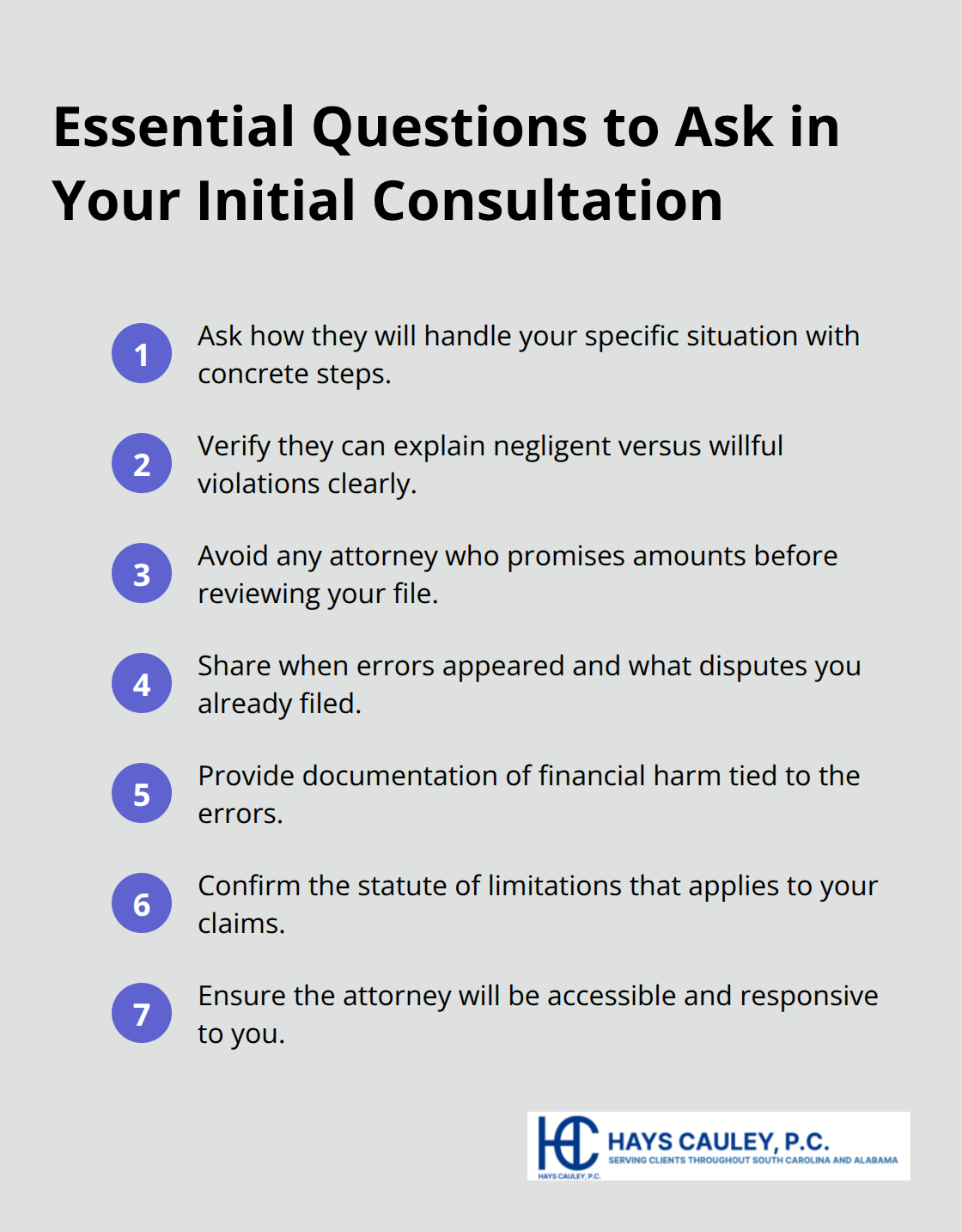

The initial consultation reveals everything you need to know about an attorney’s capability and fit for your case. During this meeting, ask the attorney to explain how they would handle your specific situation-not in vague terms, but with concrete steps. If they cannot articulate the difference between a negligent violation and a willful violation, or if they start promising specific settlement amounts before reviewing your credit reports and dispute history, walk away. A competent attorney should ask you detailed questions about when errors first appeared, what disputes you have already filed, and whether you have documented the financial harm those errors caused. They should also discuss the statute of limitations for your claim: two years for negligent violations and five years for willful violations. This matters because if your error occurred more than five years ago, your legal options narrow significantly.

Pay attention to whether the attorney personally answers your calls or whether you reach an answering service each time. The attorney who handles your case should be accessible, not hidden behind layers of staff.

Understanding Fee Structures and Cost Responsibility

Fee structure determines whether you can afford representation without financial strain. Most credit report attorneys in South Carolina work on contingency, meaning they take 33 to 40 percent of any settlement or judgment you win, and you pay nothing upfront. This arrangement aligns the attorney’s incentive with yours: they only profit if they recover money for you. However, you may still owe case costs-filing fees, court costs, and expenses for obtaining documents from credit bureaus-which typically range from five hundred to two thousand dollars depending on case complexity.

Ask whether the attorney advances these costs or expects you to pay them as you go. Attorneys who demand large retainers upfront or who require payment before reviewing your case are less common in this practice area and should raise suspicion. During your consultation, request a written fee agreement that spells out the percentage, what costs you are responsible for, and whether costs are deducted before or after the attorney’s fee.

Timeline Expectations and Deadline Management

Ask about their typical timeline: most Fair Credit Reporting Act cases settle within 8 to 18 months, though identity theft claims sometimes take longer if fraud is extensive. An attorney who will not commit to any timeline or who suggests immediate resolution is either inexperienced or overselling their capabilities. Availability matters because credit bureau disputes operate on strict deadlines-30 days for the bureau to investigate, 60 days in some cases-and missed deadlines can eliminate your claims. Before hiring, confirm the attorney can meet these deadlines and that they will keep you informed of progress without requiring constant follow-up calls from you.

Final Thoughts

Selecting the best credit report attorney comes down to three factors: proven results against major credit bureaus, genuine understanding of the Fair Credit Reporting Act, and transparent communication about fees and timelines. An attorney who cites specific settlements, explains negligent versus willful violations, and walks you through your case step-by-step is worth hiring. An attorney who makes vague promises or avoids discussing weaknesses in your claim is not.

The right attorney shifts the dynamic in your favor. Credit bureaus count on consumers abandoning disputes after initial rejections, but legal representation changes that calculation. Bureaus recognize that willful violations trigger six-figure damages, that discovery exposes their automated processes, and that most cases settle within 8 to 18 months (giving you leverage in negotiations). An attorney who understands this reality can force compliance and secure compensation you would never recover alone.

Gather your credit reports, dispute letters, and documentation of financial harm, then contact two or three attorneys for initial consultations. Pay attention to how they answer, whether they listen to your specific situation, and whether they explain your options honestly. We at Hays Cauley, P.C. help South Carolina residents with credit reporting, identity theft, and debt-related issues-reach out for a consultation and let us review your case.