FCRA Dispute Rights What You Can Do If A Lender Refuses

A lender’s refusal to acknowledge your dispute doesn’t mean your FCRA dispute rights end there. The Fair Credit Reporting Act gives you specific tools to challenge inaccurate information, and we at Hays Cauley, P.C. want you to know exactly how to use them.

This guide walks you through your legal options when a lender pushes back, from documenting everything to filing formal complaints with credit bureaus. You have more power than you think.

Your Rights Under the Fair Credit Reporting Act: Serving South Carolina, Including Greenville, Columbia and Charleston

The Fair Credit Reporting Act protects you against false information that damages your financial future, but only if you know how to fight back. The FCRA requires lenders and credit bureaus to report accurate information, and when they don’t, you have the legal right to demand corrections. Lenders must provide specific reasons for denying credit, including the exact credit score used and the key factors that hurt your score. If denial stems from your credit report, the lender must disclose the name, address, and phone number of the credit bureau that supplied it. You also have the right to a free copy of your credit report within 60 days of the denial notice-this window gives you time to spot errors before they damage your finances further.

Common Lender Violations You Should Know

Common FCRA violations by mortgage lenders and loan servicers include reporting late or delinquent status when your payments are current, failing to correct errors after you dispute them, continuing to report data after a loan modification has been approved, and not conducting a thorough investigation into your dispute. These aren’t minor paperwork mistakes-they’re violations that can cost you higher interest rates or outright credit denial. Year-to-date through October 2025, FCRA filings reached 919 cases in October alone, up 36.4 percent compared to 2024, showing how widespread these disputes have become.

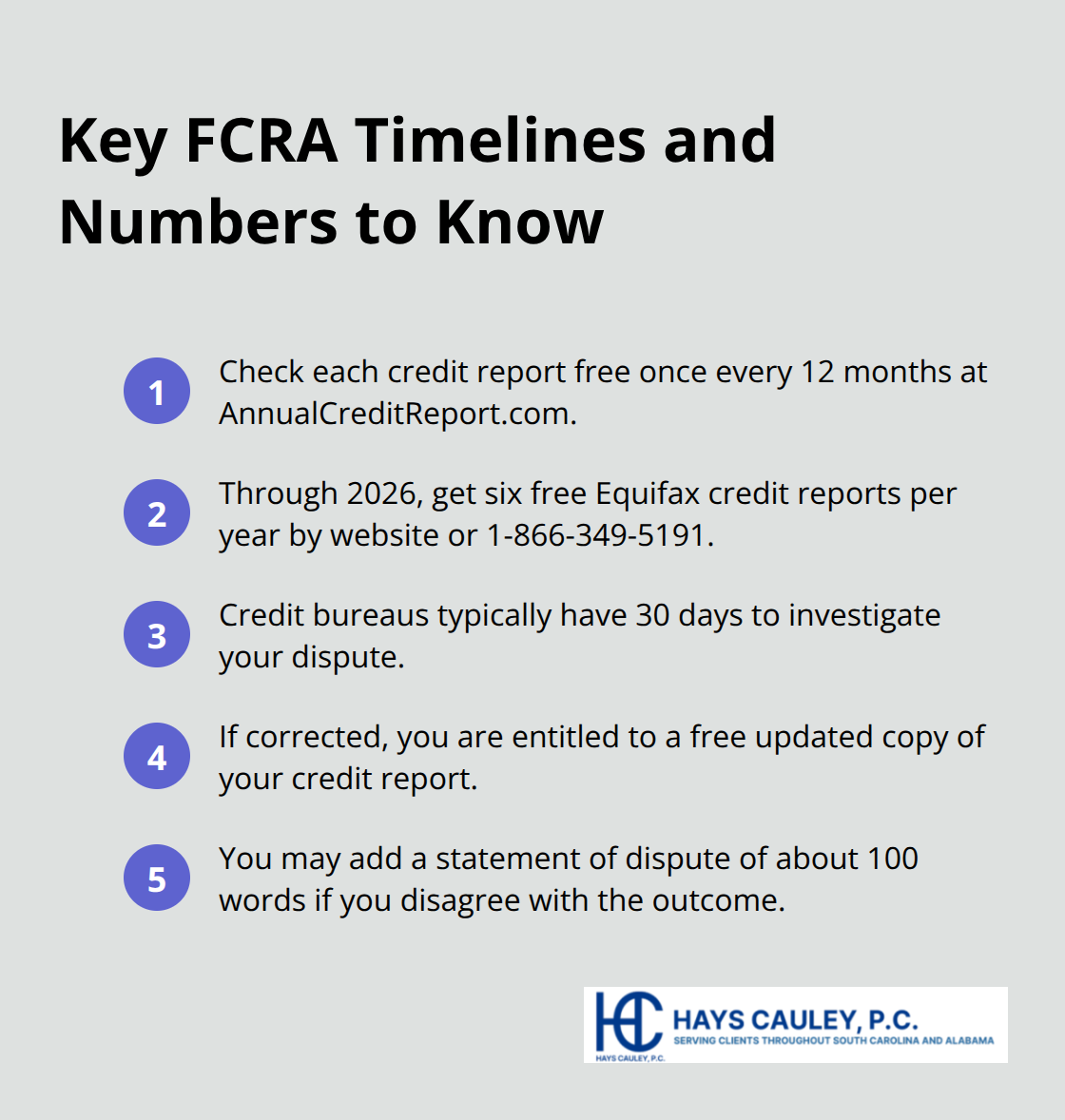

Getting Your Free Credit Reports

Start by obtaining your free credit reports from Equifax, Experian, and TransUnion at annualcreditreport.com, where you can check each report once every 12 months at no cost. Through 2026, you can access six free credit reports per year by visiting the Equifax website or calling 1-866-349-5191, giving you multiple opportunities to catch problems early.

When you review your reports, look for accounts you don’t recognize, late payments you know you made on time, duplicate entries, and loans marked delinquent after modification.

Filing Your Dispute with Credit Bureaus

If you find errors, file disputes with every credit bureau that lists the problem. The credit bureau typically has 30 days to investigate, though they will stop investigating if they deem your dispute frivolous. When disputing, write a clear explanation of what’s wrong, include copies of supporting documents, and circle the errors on your report. Send disputes via certified mail with return receipt to protect yourself: Equifax Information Services LLC, P.O. Box 740256, Atlanta, GA 30348; Experian, P.O. Box 4500, Allen, TX 75013; TransUnion Consumer Dispute Center, P.O. Box 2000, Chester, PA 19016. If the investigation results in a correction, the bureau must provide you with a free updated copy of your report.

Now that you understand your FCRA protections and how to identify errors, the next step involves taking action when lenders refuse to acknowledge your rights.

What to Do When a Lender Ignores Your Dispute

A lender’s silence or refusal to acknowledge your dispute violates the FCRA. The moment you send a written dispute, the lender becomes legally obligated to investigate your claim and report back within a reasonable timeframe. If they ignore you, that negligence strengthens your position.

Document Everything in Writing

Keep meticulous records of every communication you initiate. Send all disputes in writing using certified mail with return receipt requested-never rely on phone calls or emails alone, as you need proof of delivery. Write a clear, factual letter stating exactly what is wrong: for example, if your account shows a late payment from March 2024 but your bank statements prove you paid on time, include those statements as copies (do not send originals). Your letter should reference the specific account number, the disputed item, why it is inaccurate, and what correction you demand.

Understand the Lender’s Legal Obligation

The lender has a legal duty to conduct a thorough investigation, not a rushed or superficial one. If they fail to investigate properly or continue reporting false information after your dispute, that constitutes a willful FCRA violation. Willful violations can result in statutory damages of $100 to $1,000 per violation, plus actual damages for any financial harm you suffered (lost credit opportunities, higher interest rates, or emotional distress).

Send a Separate Dispute Letter to the Lender

After sending your formal dispute to the credit bureau, follow up directly with the lender or loan servicer that reported the false information. Send this letter separately from your bureau dispute because the lender may not respond to the bureau’s inquiry without additional pressure from you. Include the same documentation and be explicit about what you expect: removal of the inaccurate item or correction to reflect your true payment history. Many lenders bank on consumers giving up after one attempt. Your persistence and paper trail demonstrate you are serious.

What Happens When the Lender Continues Reporting Errors

If the lender continues reporting the inaccurate information to the bureaus after your dispute, the bureau must note in your file that you are disputing the item as inaccurate or incomplete. This notation does not remove the error, but it signals to future creditors that the information is contested. If you find that the lender conducted an investigation but refused to correct legitimate errors, or if they continue violating your rights, you have grounds to pursue legal action. When a lender’s refusal to correct errors persists despite your documented efforts, the next step involves understanding what legal remedies you can actually pursue.

What Happens After You File Your Dispute

The credit bureau has 30 days from receipt of your dispute to investigate, though most complete their work within two to three weeks. During this window, the bureau forwards your dispute and supporting documents to the lender or loan servicer that reported the information. The lender must then conduct its own investigation and respond to the bureau with findings. This is where many lenders fail. A rushed or superficial investigation violates the FCRA just as much as ignoring your dispute entirely. The lender cannot simply rubber-stamp the original report; it must actually review your documentation, check its records, and determine whether the disputed item is accurate.

What Happens When Errors Are Confirmed

If the lender finds the information incorrect, it must notify all three credit bureaus to update your file. You should receive a free updated copy of your credit report once corrections are made, giving you concrete proof that the dispute succeeded. The inaccurate item disappears from your report entirely, and future creditors see clean information. This correction can immediately improve your credit score, potentially lowering interest rates on future loans or enabling approvals you were previously denied.

Track the investigation timeline carefully. If 30 days pass without hearing from the bureau, send a follow-up letter asking for the investigation status and requesting written confirmation of their findings. Request a new credit report from each bureau that made corrections to verify the changes appear correctly.

The Risk of Re-Reporting After Removal

Many consumers stop monitoring their reports after corrections are made, but you should watch for the next several months because some lenders illegally re-report the same false information after it was removed. If that happens, you have grounds for an additional FCRA violation claim, and the lender’s pattern of misconduct strengthens your legal position significantly. Each instance of re-reporting after removal constitutes a separate violation, which multiplies your potential damages.

When the Bureau Disagrees with Your Dispute

Not every dispute results in removal. The bureau may conclude the information is accurate based on the lender’s response, or it may deem your dispute frivolous and stop investigating entirely. If you disagree with the outcome, you have the right to add a statement of dispute directly to your credit file. This statement, typically 100 words or less, explains your position and appears alongside the disputed item on future credit reports.

While a dispute statement does not remove the negative information, it signals to creditors that you contest the accuracy and have formally challenged it. Some creditors weigh dispute statements heavily when making lending decisions because they indicate potential FCRA violations by the lender. You may be charged a fee to send your dispute statement to past recipients of your report, though the initial statement in your file costs nothing.

When Investigation Failures Become Violations

If you believe the lender’s investigation was inadequate or deliberately misleading, that failure itself constitutes a willful FCRA violation. A lender cannot conduct a cursory review and claim compliance; the law requires a thorough, reasonable investigation that actually examines your evidence. When lenders fail to meet this standard (and many do), you have the right to pursue legal action for damages. Actual damages include out-of-pocket losses, missed credit opportunities, and emotional distress caused by inaccurate reporting. Willful violations can result in statutory damages of $100 to $1,000 per violation, and if you prevail, you may recover attorneys’ fees and court costs. We at Hays Cauley, P.C. help consumers pursue these claims when lenders refuse to conduct proper investigations or correct errors after disputes are filed.

Final Thoughts

Your FCRA dispute rights are real and enforceable, but they only work if you take action. You have the legal authority to demand accurate information on your credit report, challenge lenders who refuse to investigate properly, and pursue damages when they violate your rights. The data shows this matters: FCRA filings jumped 36.4 percent year-to-date through October 2025 compared to 2024, meaning thousands of consumers are fighting back against inaccurate reporting.

When a lender ignores your dispute or conducts a superficial investigation, that negligence becomes a violation you can act on. Willful violations carry statutory damages of $100 to $1,000 per violation, plus actual damages for financial harm and emotional distress. If you prevail, the lender pays your attorneys’ fees and court costs, which means pursuing your rights does not require money upfront if you work with the right attorney.

Contact us at Hays Cauley, P.C. when a lender continues reporting false information after your dispute, when the credit bureau investigation fails to resolve the error, or when you suspect the lender deliberately ignored your evidence. We help consumers throughout South Carolina fight back against credit reporting violations and hold lenders accountable for the damages you deserve.