Understand credit reporting rights: A Practical Guide

Your credit report shapes your financial life, yet most people don’t understand their rights when it comes to this document. Errors on your report can cost you thousands in higher interest rates or denied loans.

We at Hays Cauley, P.C. created this guide to help you understand credit reporting rights and take control of your financial information. You’ll learn what protections the law gives you and how to use them.

What Your Credit Report Actually Shows

The Core Components of Your Credit Report

Your credit report is a detailed record of your borrowing history compiled by Equifax, Experian, and TransUnion. It includes your personal information like name, address, and Social Security number, alongside every credit account you’ve opened-credit cards, mortgages, auto loans, and personal lines of credit. Each account entry shows the creditor’s name, account number, credit limit or loan amount, current balance, and payment status. The report also lists every hard inquiry made when you applied for credit, which can temporarily lower your score by a few points.

How Payment History Dominates Your Score

Payment history accounts for 35% of your credit score calculation, so lenders scrutinize whether you paid on time, missed payments, or defaulted. Late payments stay on your report for seven years, even if you eventually paid them off, and a single 30-day late payment can drop your score by 100 points or more depending on your starting score. This means that one mistake can haunt your financial life for years, affecting your ability to qualify for favorable loan terms.

Negative Items That Wreck Your Creditworthiness

Your credit report flags negative items that seriously damage your creditworthiness. Charge-offs, collections accounts, foreclosures, and tax liens appear and remain for seven years, making it nearly impossible to qualify for favorable loan terms during that period. If you’ve experienced identity theft, fraudulent accounts opened in your name will appear on your report and wreck your score unless you dispute them immediately.

The Reality of Credit Report Errors

About 13 million people per year find inaccuracies on their credit reports according to industry data, including late payments labeled as late when they were actually on time, accounts you never opened, or duplicate entries of the same debt. These errors don’t just hurt your credit score-they can cost you thousands in higher interest rates, trigger loan denials, and even affect insurance premiums and job prospects. You’re responsible for catching and correcting these mistakes because credit bureaus have little incentive to fix them voluntarily, and errors compound over time if left unaddressed.

Understanding what appears on your report is the first step toward protecting yourself. The next section explains the specific rights the law grants you to access, review, and challenge the information that credit bureaus maintain about you.

What the Law Actually Guarantees You, Serving South Carolina, including Greenville, Columbia and Charleston

Your Three Core Rights Under Federal Law

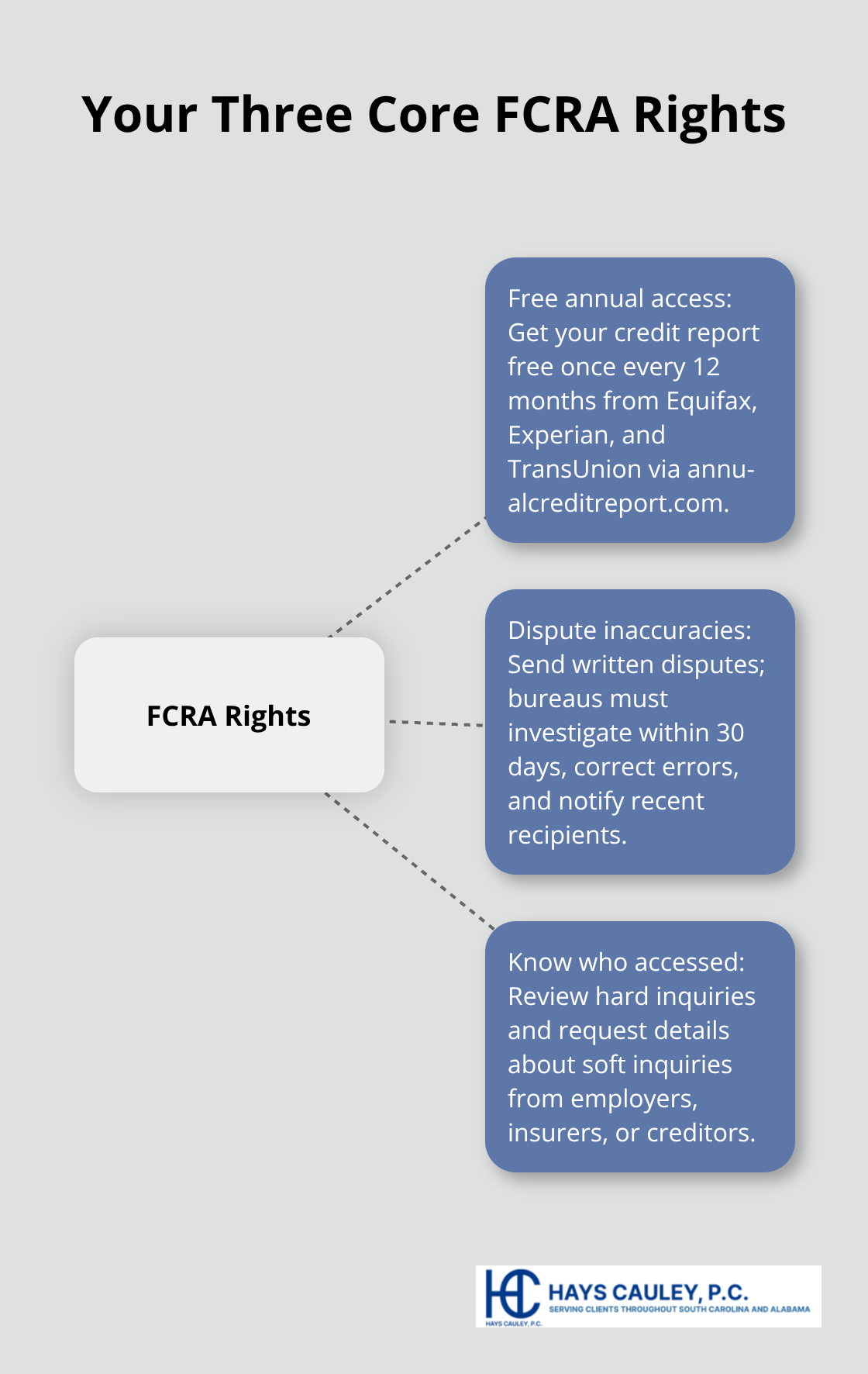

The Fair Credit Reporting Act grants you three fundamental protections that most people never use. First, you have the absolute right to access your credit report for free once every 12 months from each of the three major bureaus-Equifax, Experian, and TransUnion. You can request all three reports at once through annualcreditreport.com, or contact each bureau individually: Equifax at 1-800-685-1111, Experian at 1-888-397-3742, and TransUnion at 1-877-322-8228. You must obtain your reports because you bear responsibility for catching errors, and waiting until you apply for a loan to uncover a problem costs you time and money.

Second, when you find inaccurate information, you have the right to dispute it directly with the credit bureau in writing. The bureau must investigate within 30 days and inform you of the results. If they find the information is inaccurate, they must correct it and notify any entity that received your report in the last six months. Third, you have the right to know who accessed your report. Hard inquiries appear on your report when you apply for credit, and you can see them listed. Soft inquiries-from employers, insurance companies, or existing creditors reviewing your account-don’t appear, but you can request information about them.

How the Law Enforces Your Rights

The law backs these rights with real consequences for violations. Willful violations by credit bureaus expose them to triple your actual damages or at least $3,000 per incident, plus attorney’s fees. If a bureau refuses to remove inaccurate information after a judgment against them, damages accrue at up to $1,000 per day until the information is removed. This means action works. When you dispute an error in writing with clear documentation, you force the bureau to investigate rather than ignore you.

What Happens When Disputes Fail

If the dispute is denied, you can add a statement of dispute to your file that explains your position, and future lenders will see it. If the bureau still won’t fix a legitimate error, contact the creditor or furnisher directly and request they update their records-this often moves faster than the bureau dispute process. You should keep copies of everything: your dispute letters, the bureau’s responses, your proof documents, and all correspondence. Organized records protect you if the dispute stalls and you need to escalate to litigation.

Taking Action on Your Rights

The next section walks you through the specific steps to monitor your credit, identify errors, and dispute them effectively so you can reclaim control of your financial information.

How to Monitor Your Credit and Fix Errors, Serving South Carolina, including Greenville, Columbia and Charleston

Start With Your Three Credit Reports

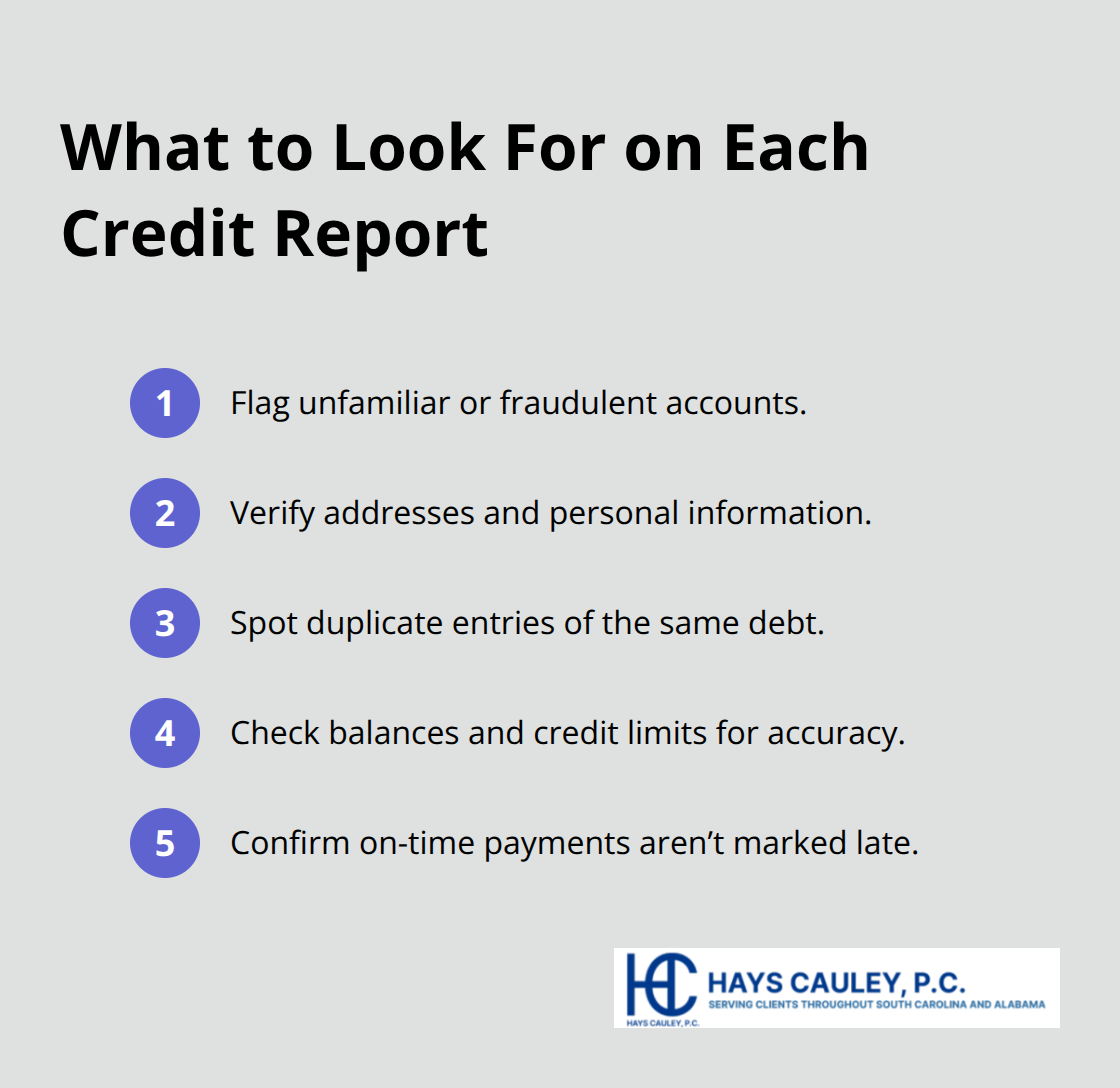

Checking your credit report once yearly protects you, but waiting twelve months between reviews leaves errors undetected and compounding. Obtain all three reports immediately from annualcreditreport.com, then review them side by side because errors often appear on one bureau’s file but not the others. Look for unfamiliar accounts, wrong addresses, duplicate entries, incorrect balances, and late payments marked as late when you paid on time. The three major bureaus-Equifax (1-800-685-1111), Experian (1-888-397-3742), and TransUnion (1-877-322-8228)-maintain separate files, so a mistake on one report may not appear on another.

Document Your Proof Before Disputing

Once you identify an error, gather supporting documents before disputing it. Collect bank statements, payment receipts, letters from creditors, or identity theft reports that prove the inaccuracy. Organize these materials by date and type so you can reference them quickly if the bureau requests clarification. This preparation strengthens your dispute and prevents delays when the bureau investigates.

File Written Disputes That Create a Trail

File your dispute in writing rather than by phone because written disputes create a documented trail that protects you if the matter escalates. Clearly explain the error, attach copies of your proof documents (never originals), and send everything to the bureau via certified mail with return receipt. The bureau must investigate within 30 days and inform you of the results. If they correct or remove the item, your report updates automatically. If they deny your dispute, contact the creditor or furnisher directly and request they fix their records with the bureau because creditors often respond faster than bureaus do. Add a statement of dispute to your file explaining your position if the bureau still refuses to correct a legitimate error. Keep copies of all correspondence, responses, and proof documents organized by date and type because these records protect you if you need to pursue litigation later.

Use a Security Freeze to Block Unauthorized Credit

A security freeze blocks new credit accounts from being opened in your name without your permission, which is the most powerful tool against identity theft. South Carolina law allows you to place a freeze for free within five business days of a written request with proper identification, and the bureau must send written confirmation with a unique PIN or password within ten business days. You can lift the freeze temporarily for a specific creditor or designated period, and online lifts occur within about fifteen minutes after identification.

Respond Immediately to Identity Theft

If you suspect identity theft has already occurred, contact the State Law Enforcement Division to initiate an investigation, then notify the three bureaus and place fraud alerts on your file immediately. File an identity theft report with the Federal Trade Commission at identitytheft.gov, which creates an official record you can use when disputing fraudulent accounts. Contact creditors whose accounts were opened fraudulently and request they close the accounts and remove them from your report. The process takes persistence, but organized records and written documentation force action. When bureaus and creditors resist corrections, litigation may become necessary to protect your rights under federal law.

Final Thoughts

Your credit report controls access to loans, insurance rates, housing opportunities, and even job prospects, yet most people never review it until something goes wrong. Understanding credit reporting rights puts you in control of your financial information instead of leaving it to chance. The Fair Credit Reporting Act gives you concrete protections: the right to access your report free once yearly, the right to dispute inaccurate information in writing, and the right to know who accessed your file.

About 13 million people per year find errors on their reports, and those errors cost real money in higher interest rates and denied applications. You must catch mistakes because credit bureaus won’t fix them voluntarily. Request your three reports from Equifax, Experian, and TransUnion immediately through annualcreditreport.com, then review them carefully for unfamiliar accounts, wrong addresses, and incorrect payment statuses. Document your proof before disputing any error, file disputes in writing with certified mail, and keep organized records of everything.

If a bureau denies your dispute, contact the creditor directly because they often respond faster. Place a security freeze on your file to block unauthorized credit, and respond immediately if identity theft occurs by contacting law enforcement and the Federal Trade Commission. When disputes stall or bureaus refuse to correct legitimate errors, litigation may become necessary to protect your rights, and we at Hays Cauley, P.C. help consumers fight credit reporting errors and identity theft when the process becomes complicated.