correct credit report errors a practical correction guide

A credit report error can tank your credit score and cost you thousands in higher interest rates. Inaccurate information appears on millions of reports every year, yet most people don’t know how to correct credit report errors effectively.

We at Hays Cauley, P.C. help South Carolina residents fight back against these mistakes. This guide walks you through identifying errors, disputing them, and knowing your legal rights.

Finding Errors on Your Credit Reports

Access Your Reports from All Three Bureaus

Start by obtaining copies of your credit reports from all three bureaus: Equifax, Experian, and TransUnion. Since 2026, you can access six free reports per year through annualcreditreport.com, the official source run by the FTC. Avoid third-party sites that charge fees or push credit monitoring subscriptions. Pull your reports now, and check again in three months to catch errors early. The FTC reports that inaccurate information appears on millions of credit reports annually, yet most people never review theirs.

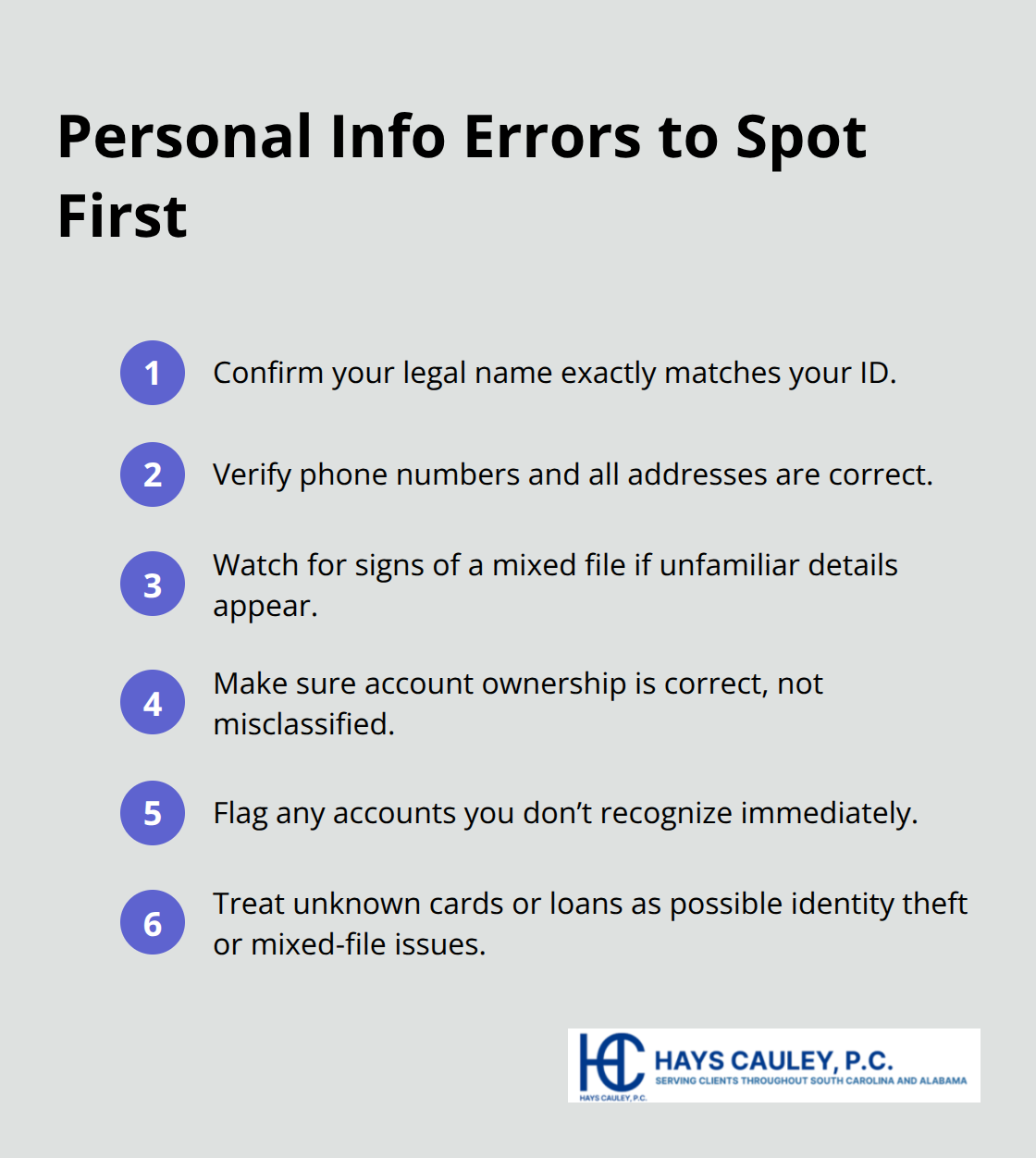

Scan for Personal Information Errors

When you receive your reports, print them out and read every line carefully. Look for personal information errors first: wrong name, phone number, or address. These mistakes signal that your file may be mixed with someone else’s. Check account ownership with special attention. If you appear as the account owner when you’re actually just an authorized user, that’s a reportable error.

Scan for accounts you don’t recognize. Unknown credit cards, loans, or lines of credit could indicate identity theft or a mixed-file error where another person’s accounts appear on your report.

Verify Account Status and Dates

Look at account status fields closely. Closed accounts should show closed, not open. Current accounts should never show as late or delinquent. Incorrect dates represent another red flag: wrong account opening date, wrong last payment date, or wrong first delinquency date. If the same debt appears twice under different names, that’s a duplicate error you must dispute. Check the current balance and credit limit fields for data entry mistakes. These errors directly impact your credit score calculation.

Identify Fraudulent Accounts and Inquiries

Fraudulent accounts and unauthorized inquiries deserve immediate attention because they indicate identity theft. If you spot accounts you never opened or inquiries from lenders you never contacted, take action right away. Hard inquiries from companies you don’t recognize should raise alarms. One fraudulent account or inquiry won’t destroy your credit overnight, but multiple errors compound the damage. The Fair Credit Reporting Act gives you the right to dispute any inaccurate information in your file, and both the credit bureau and the furnisher (the company that reported the information) must investigate your claim. This obligation is not optional for them.

Understand Your Right to Correction

If you find errors, you’re not stuck with them. The law requires these organizations to correct or remove inaccurate information for free after you dispute. Don’t delay-the longer inaccurate information sits on your report, the more it damages your credit score and borrowing power. Once you’ve identified the errors on your reports, the next step involves sending a formal dispute letter to the credit bureau and the furnisher.

How to File Your Dispute Letter and Track Results

Structure Your Dispute Letter Correctly

Your dispute letter forms the foundation of correcting credit report errors. The FTC provides sample dispute letters specifically designed for disputing with credit bureaus and furnishers, and using these templates matters because they include the exact language and structure that credit reporting companies expect. When you write your dispute letter, state every inaccuracy you found on your report, explain clearly why each item is wrong, and include copies of supporting documents like statements, receipts, or letters that prove your case. Include your contact information, the credit report confirmation number if available, each account number associated with the error, and a clear request for either removal or correction of the inaccurate information.

Send Your Letter via Certified Mail

Send your letter via certified mail with return receipt requested to both the credit bureau and the furnisher organization that originally reported the incorrect information. The certified mail approach creates a verifiable record proving the bureau received your dispute on a specific date, which matters because the credit bureau has exactly 30 days from receipt to investigate your claim according to the FTC. Equifax accepts disputes at P.O. Box 740256, Atlanta, GA 30348; Experian at P.O. Box 4500, Allen, TX 75013; and TransUnion at P.O. Box 2000, Chester, PA 19016.

You can also file disputes online or by phone with Experian at 888-397-3742, TransUnion at 800-916-8800, and Equifax at 866-349-5191, though mailed disputes with certified receipts create stronger documentation.

Document and Organize Everything

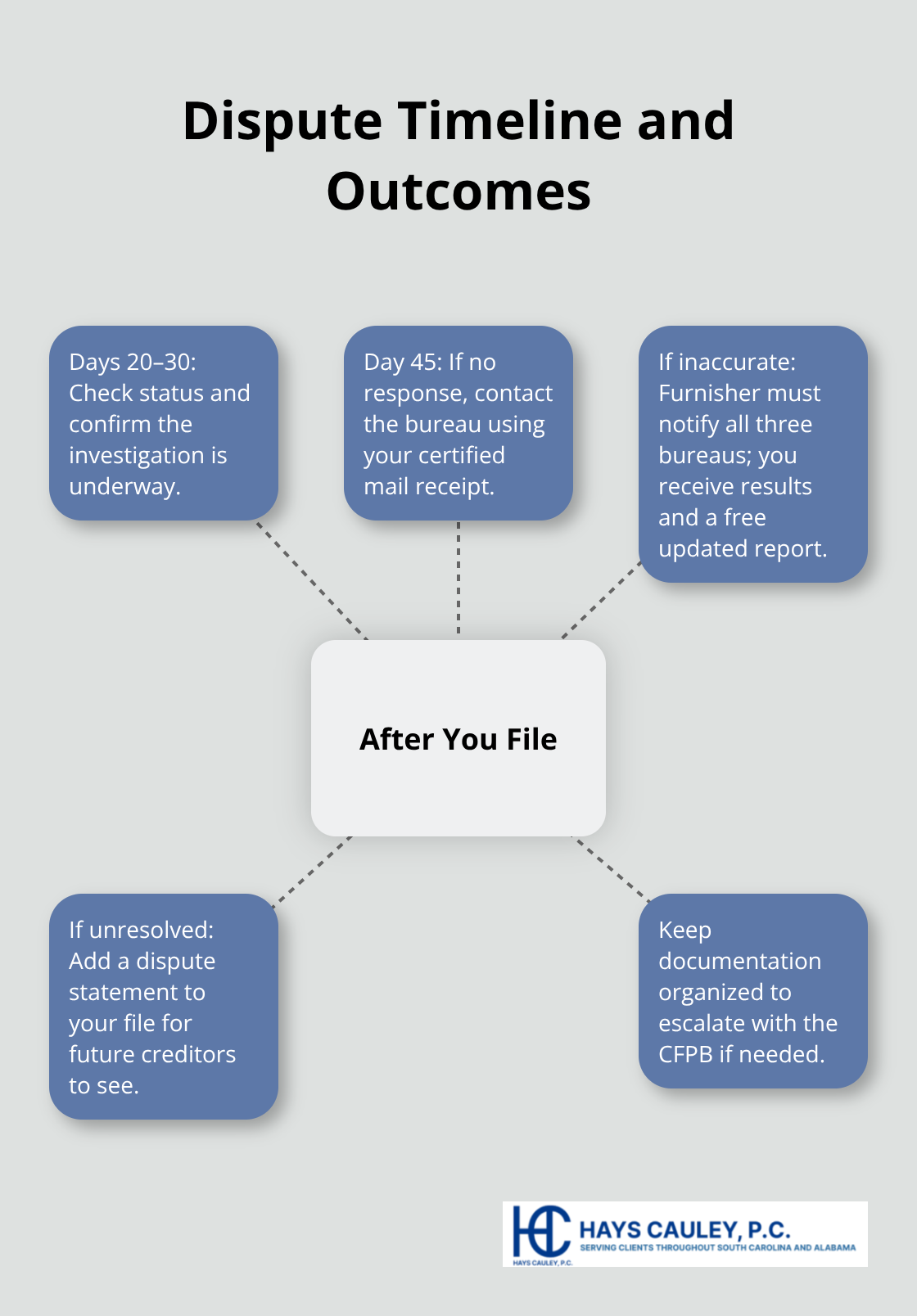

After you file your dispute, save every piece of paper related to the process. Keep copies of your dispute letters, the certified mail receipts, your marked-up credit reports with errors circled, and all supporting documents in a dedicated folder. The credit bureau will forward your evidence to the furnisher, who must investigate and report results back to the bureau within approximately 30 days. Track these documents meticulously because they protect you if disputes stall or if you need to escalate the matter to the Consumer Financial Protection Bureau, which investigates consumer complaints about credit reporting failures.

Monitor Your Dispute Status and Follow Up

Monitor your dispute status between day 20 and day 30 after you send your letter, and if you don’t receive a response by day 45, contact the bureau again with your certified mail receipt number. If the investigation finds the information inaccurate, the furnisher must notify all three bureaus, and you’ll receive written results plus a free copy of your updated credit report. If the dispute doesn’t fully resolve the issue, you can request that a dispute statement be included in your file and on future reports sent to potential creditors.

Once you understand your legal rights under the Fair Credit Reporting Act, you’ll recognize that credit bureaus and furnishers cannot ignore your disputes-they must respond, investigate, and correct errors or face regulatory consequences.

What the Fair Credit Reporting Act Actually Requires

The Fair Credit Reporting Act, passed in 1970 and updated significantly through the Fair and Accurate Credit Transactions Act in 2003, gives you concrete legal power that most people never use. The FTC enforces this law alongside state attorneys general, and credit bureaus know they face real consequences for ignoring your rights. The law doesn’t give you optional protections-it mandates that credit bureaus and furnishers investigate disputed information within 30 days and correct errors for free.

How the Investigation Process Works

This obligation applies whether the error is a typo, a mixed file with someone else’s accounts, or fraudulent information from identity theft. When you file a dispute, the credit bureau must forward your evidence to the furnisher, who then has 30 days to investigate and report back. If the furnisher finds the information inaccurate, they must tell all three bureaus immediately. If they confirm the information is accurate, you can request that a dispute statement be added to your file, which appears on all future credit reports sent to potential lenders, employers, or landlords.

Why Proper Procedures Matter

What separates people who successfully correct errors from those who don’t is understanding that this process works only if you follow specific procedures. The FTC provides sample dispute letters because credit bureaus receive thousands of disputes monthly, and poorly written letters get rejected as frivolous or incomplete. Include your account numbers, explain why each item is wrong, provide copies of supporting documents, and use certified mail with return receipt-this creates proof of delivery that protects you if a bureau claims they never received your dispute.

Furnisher Obligations and Your Protections

The furnisher also has obligations: they must investigate your claim, cannot simply ignore it, and must respond within the 30-day window. If they fail to investigate or falsely confirm inaccurate information, that’s a violation the CFPB takes seriously. After the investigation closes, if you remain unsatisfied, you can file a complaint with the Consumer Financial Protection Bureau, which will forward it to the company and track their response. The FTC reports that most disputes that follow proper procedures result in corrections or removal of inaccurate information, but disputes that lack documentation or fail to specify which items are wrong often stall.

Building Your Strongest Case

Your strongest position comes from combining the certified mail receipt showing delivery, copies of your dispute letter, marked-up credit reports with errors circled, and supporting documents like bank statements or payment receipts. These materials (when organized and submitted correctly) demonstrate that you took the dispute seriously and followed legal requirements. Credit bureaus and furnishers cannot ignore disputes backed by this level of documentation without facing regulatory action from the CFPB or FTC.

Final Thoughts

Correcting credit report errors follows a clear path: identify inaccurate information on your reports from all three bureaus, send written dispute letters via certified mail to both the credit bureau and furnisher, and track the investigation for 30 days. Most errors that receive proper documentation get corrected or removed without additional effort. The key is following procedures exactly as the FTC outlines them and maintaining meticulous records throughout the process.

Your credit report directly affects your borrowing costs, job prospects, insurance rates, and housing options. Negative but accurate information stays on your report for seven years, which means inaccurate information can damage your financial life for years if left uncorrected. Review your reports at least annually through annualcreditreport.com, and pull additional free reports if you suspect identity theft or mixed-file errors.

If disputes stall, if furnishers ignore your claims, or if you need guidance navigating the process, Hays Cauley, P.C. can help you take the next step. We serve South Carolina, including Greenville, Columbia and Charleston, and we know the Fair Credit Reporting Act inside and out. Contact us if credit report errors are affecting your financial future.