Should You Freeze Your Credit After Identity Theft?

Identity theft happens fast, and your credit is vulnerable the moment a thief uses your personal information. A credit freeze identity theft protection strategy can stop criminals from opening new accounts in your name, but only if you act quickly.

At Hays Cauley, P.C., we help South Carolina residents, including those in Greenville, Columbia, and Charleston, understand their options after identity theft strikes. This guide walks you through whether freezing your credit is the right move for your situation.

How a Credit Freeze Actually Protects You

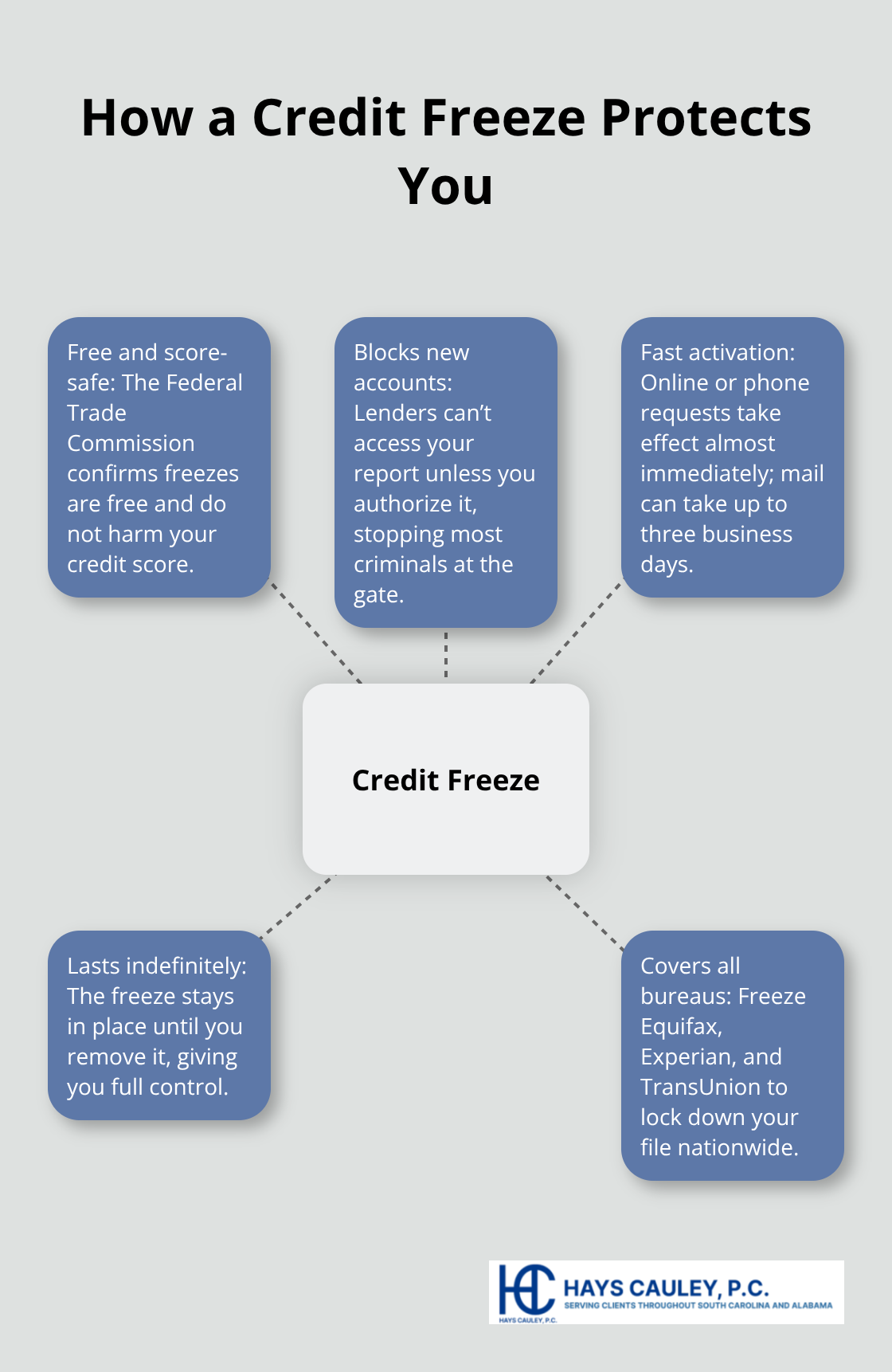

A credit freeze blocks lenders from accessing your credit report when someone tries to open new accounts in your name. The Federal Trade Commission confirms that freezes are free to place and do not harm your credit score. When you freeze your credit with Equifax, Experian, and TransUnion, you tell these bureaus to restrict access to your file unless you explicitly authorize it. This stops most criminals because lenders cannot verify your creditworthiness without seeing your report. The freeze takes effect almost immediately for online or phone requests, though mail requests can take up to three business days.

Once active, the freeze remains in place indefinitely until you request its removal, giving you complete control over how long the protection lasts.

Freezes Last as Long as You Need Them

Unlike fraud alerts that expire after one year or seven years, a credit freeze has no expiration date. You control when it stays active and when it comes down. If you need to apply for a mortgage, car loan, or credit card, you can temporarily lift the freeze for a specific lender or time period. Most lifts happen within 15 minutes when you request them online or by phone, and you can set them to last anywhere from a few days to several months. This flexibility means you maintain permanent protection without sacrificing your ability to access credit when you genuinely need it. South Carolina law requires that placing, lifting, or removing a freeze be completely free, so you’ll never pay to manage your protection.

Why Freezes Beat Fraud Alerts and Locks

A fraud alert is weaker protection. It lasts only one year for an initial alert or seven years for an extended alert, and it merely requires lenders to verify your identity before opening credit. Criminals can still access your report and may succeed in opening accounts despite the verification step. A credit lock, offered through some credit monitoring services, functions similarly to a freeze but is not the same thing legally and may not provide identical protections. South Carolina law specifically defines and protects security freezes, making them the most powerful tool available. You cannot have both a freeze and a lock on your Equifax report simultaneously, so a freeze is the clear winner if you must choose one.

What Happens When You Lift Your Freeze

Lifting a freeze temporarily allows lenders to access your report for legitimate credit applications. You can set a lift window (typically 15 days or longer) and then the freeze automatically reactivates. This means you don’t have to remember to re-freeze manually after your application processes. If you apply for credit with multiple lenders, lift the freeze at the specific bureau that lender uses rather than all three at once. This targeted approach limits exposure and keeps your other reports locked down while you shop for the best rates.

Moving Forward with Your Protection Strategy

A credit freeze is your strongest defense against new account fraud, but it works best as part of a larger protection plan. You’ll also want to monitor your existing accounts and credit reports regularly to catch any unauthorized activity that may have already occurred before you placed the freeze.

When Identity Theft Strikes

Recognize the Warning Signs

Identity theft reveals itself through specific red flags that demand immediate attention. Accounts you never opened appear on your credit report, inquiries from unfamiliar lenders show up without your applications, bills arrive for services you didn’t purchase, or debt collectors call about debts you didn’t incur. The Federal Trade Commission reports that detecting identity theft early reduces recovery time significantly, making the first 24 to 48 hours after discovery absolutely critical. These warning signs tell you that criminals have already used your personal information and that action cannot wait.

Act Within the First 48 Hours

Speed determines whether criminals succeed or fail once you suspect identity theft. File an Identity Theft Report at IdentityTheft.gov immediately-this report strengthens your ability to dispute fraudulent accounts and supports an extended fraud alert lasting seven years. Call your banks and credit card companies to report the theft and freeze those specific accounts before thieves drain them further. Then contact all three credit bureaus: Equifax at 888-298-0045, Experian at 888-397-3742, and TransUnion at 888-909-8872 to place a credit freeze. South Carolina law requires these bureaus to activate your freeze within five business days, though online and phone requests typically take effect almost immediately.

Document Everything With a Police Report

Criminals work fast once they have your information, and every day you wait gives fraudsters more opportunity to open accounts, rack up debt in your name, or sell your data to other criminals. If you’ve already discovered fraudulent accounts, file a police report in your jurisdiction-this documentation strengthens your position when disputing charges and provides evidence that supports legal action if needed. Your freeze, combined with your Identity Theft Report and police documentation, creates a record that protects you when creditors attempt to verify suspicious applications.

Prepare for the Lift-and-Freeze Cycle

Placing your freeze before you apply for new credit yourself is essential because you’ll need to temporarily lift it when you legitimately need credit. If you apply for a mortgage, car loan, or credit card, lift the freeze at the specific bureau that lender uses rather than all three at once (this targeted approach limits exposure and keeps your other reports locked down while you shop for the best rates). Most lifts happen within 15 minutes when you request them online or by phone, and you can set them to last anywhere from a few days to several months.

The steps you take in these first days-filing reports, contacting bureaus, and placing your freeze-form the foundation of your recovery. What happens next depends on whether you’ve caught the theft before or after fraudsters opened accounts in your name.

How to Freeze Your Credit Right Now

Contacting the three bureaus takes minutes, and South Carolina law requires them to activate your freeze within five business days. Call Equifax at 888-298-0045, Experian at 888-397-3742, and TransUnion at 888-909-8872 to place your freeze by phone. Online freezes work faster-visit myEquifax.com, Experian.com, or TransUnion.com to freeze directly. You can also mail freeze requests, though this method takes longer and defeats the purpose when you need immediate protection after identity theft. Do not call just one bureau hoping they’ll coordinate with the others; each bureau operates independently, and you must contact all three separately.

Online and phone requests typically take effect almost immediately, while mail requests can take up to three business days.

Prepare Your Documents Before Calling

Have one proof of identity and two proofs of your current address ready before calling. Acceptable identity documents include your Social Security card, military ID, driver’s license, or a letter from the Social Security Administration. For address verification, use recent utility bills, bank statements, or lease agreements-these must be unexpired and show your current name and address. The bureaus will ask verification questions based on your credit file, so prepare to answer about accounts, previous addresses, or credit inquiries. If you mail your freeze request, include copies of these documents (never originals) and send them to the dedicated freeze address for each bureau. South Carolina residents can freeze credit for minors under 16 or incapacitated adults using the appropriate protected consumer forms, though these require mailing with proof of authority.

Understand the Extended Fraud Alert Option

If you file an extended fraud alert (which lasts seven years), you’ll need either an FTC Identity Theft Report from IdentityTheft.gov or a police report to strengthen your position with creditors. This extended alert removes your name from prescreened credit offers for five years and requires lenders to verify your identity before opening new accounts. The extended alert provides additional protection beyond a standard fraud alert, which lasts only one year. You can file this report at the same time you place your freeze, creating a comprehensive protection strategy.

Access Free Credit Monitoring Resources

Victims of identity theft receive free annual credit reports from all three bureaus through IdentityTheft.gov. The Federal Trade Commission provides this service at no cost, and you can monitor your credit file for new fraudulent accounts or inaccuracies. You can also add a consumer statement to your credit report explaining your situation to any creditor who reviews your file. South Carolina law makes placing, lifting, or removing your freeze completely free-you’ll never pay a cent for these essential protections.

Know When to Seek Legal Assistance

If you discover that fraudsters opened accounts in your name or that creditors failed to verify fraudulent applications, legal action may be necessary. Hays Cauley, P.C. helps South Carolina residents recover from identity theft and hold creditors accountable for failing to verify fraudulent applications.

Moving Forward After Identity Theft

Check your credit reports from all three bureaus within 30 days of placing your freeze to catch fraudulent accounts that criminals may have already opened. The Federal Trade Commission provides free annual reports through annualcreditreport.com, and identity theft victims receive additional free reports at no cost. Look for accounts you never opened, inquiries from lenders you didn’t contact, and balances that don’t match your records, then document every discrepancy for potential disputes or legal action.

Monitor your existing bank and credit card accounts weekly for unauthorized transactions and set up account alerts with your banks to catch suspicious activity immediately. An extended fraud alert lasts seven years (when supported by an FTC Identity Theft Report or police report) and requires lenders to verify your identity before opening new accounts. These tools work together with your credit freeze identity theft protection to create multiple barriers against further fraud.

If creditors opened accounts in your name despite your freeze or fraud alert, or if they failed to verify fraudulent applications, you may have grounds for legal action against them. Creditors have a responsibility to verify identity before extending credit, and violations of federal credit reporting laws carry real consequences. Contact Hays Cauley, P.C. if fraudsters have damaged your credit or if you need guidance navigating disputes with creditors who failed to protect your information-we help South Carolina residents, including those in Greenville, Columbia, and Charleston, hold creditors accountable and recover damages from identity theft.