Do I Need Identity Theft Protection?

Identity theft affects millions of Americans each year, and the question “Do I need identity theft protection?” deserves a straightforward answer. The reality is that criminals are constantly finding new ways to steal personal information, from phishing emails to data breaches at major retailers.

At Hays Cauley, P.C., we’ve helped countless South Carolina residents recover from identity theft and rebuild their financial lives. This guide walks you through how theft happens, warning signs to watch for, and the concrete steps to take if you become a victim.

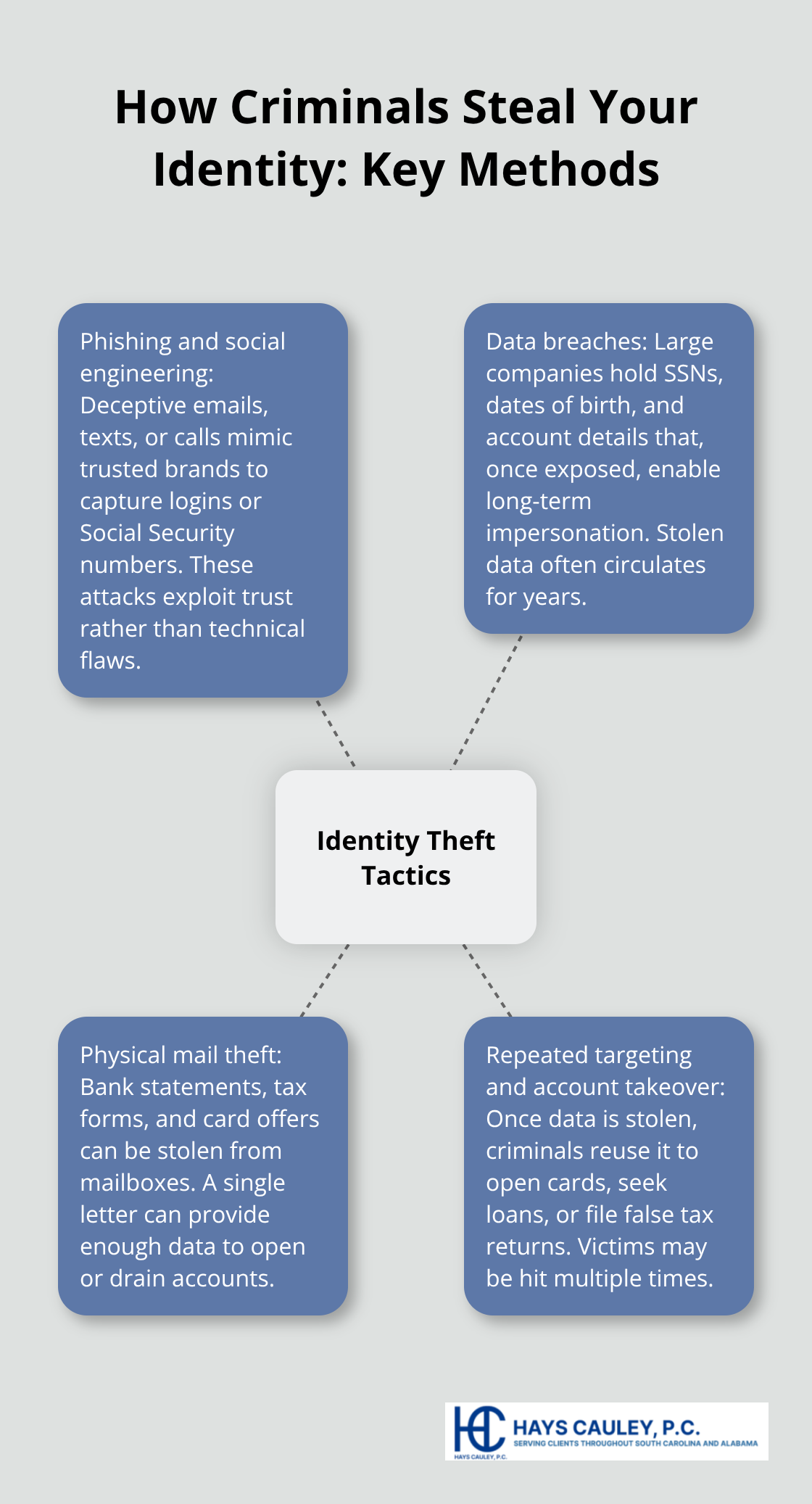

How Criminals Steal Your Identity

Phishing and Social Engineering Attacks

Criminals don’t need to break into your home to steal your identity. Phishing emails that look like legitimate messages from your bank or favorite retailer trick you into entering passwords or Social Security numbers on fake websites. These attacks work because they exploit trust, not technology. A single compromised password opens the door to multiple accounts, and attackers move quickly to drain funds or open new credit lines before you notice anything wrong.

Data Breaches Expose Your Most Sensitive Information

According to the Federal Trade Commission, about nine million Americans have their identities stolen each year. Data breaches at major companies expose millions of records at once-retailers, healthcare providers, and financial institutions all store your most sensitive information, from Social Security numbers to dates of birth, making them attractive targets for hackers. The Verizon Data Breach Investigations Report consistently shows that breaches expose these exact data points, which are nearly impossible to replace once compromised. When criminals obtain this information, they possess everything needed to impersonate you for years.

Physical Mail Theft Creates Immediate Risk

Criminals also steal physical mail containing bank statements, tax documents, or new credit card offers. A stolen piece of mail gives a criminal everything needed to open accounts in your name or drain existing ones. Mail theft happens quietly-you may not notice a missing statement for weeks, giving thieves a significant head start.

The Cycle of Repeated Targeting

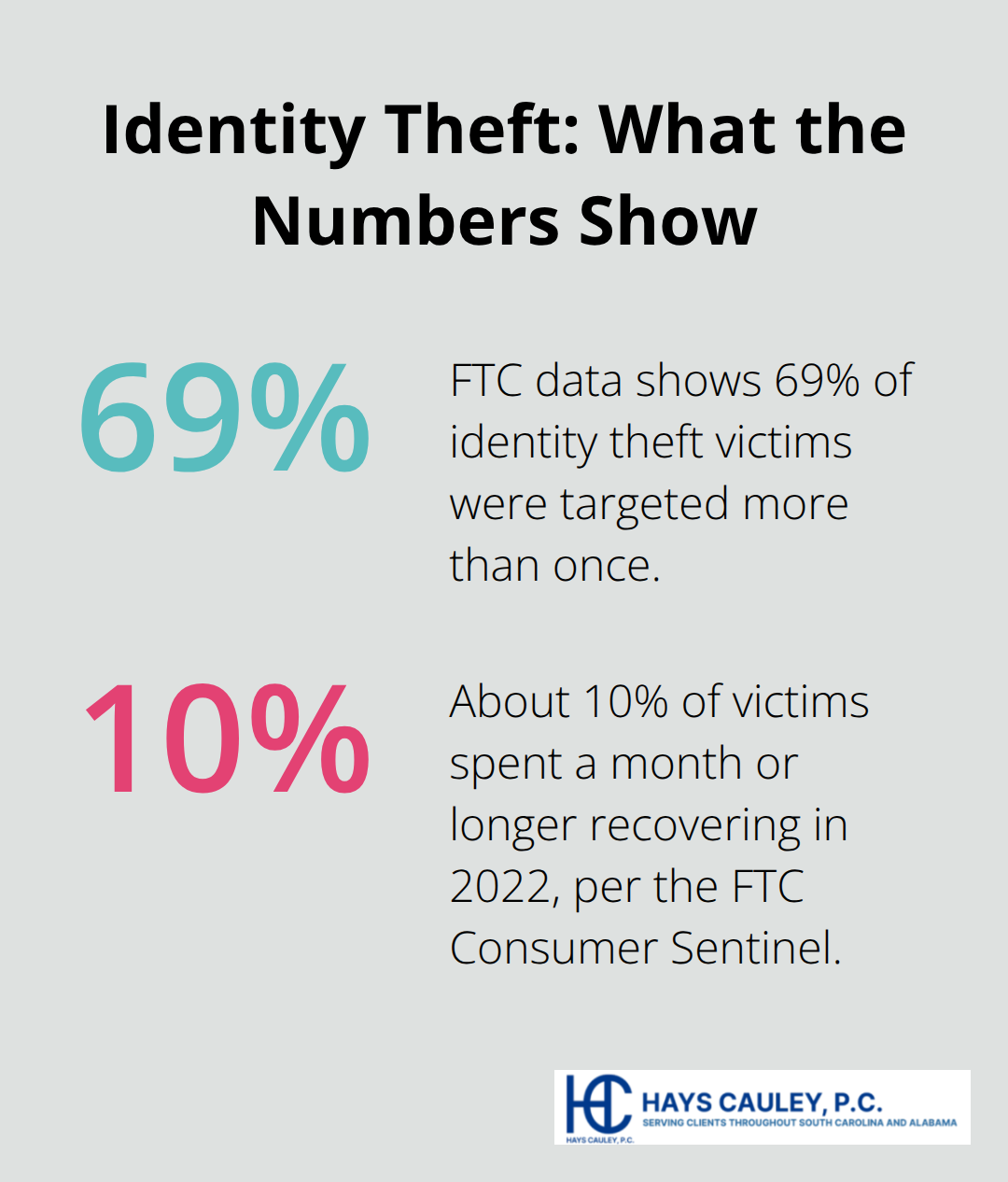

The threat is immediate and ongoing. If you’ve received data breach notifications, you’re not alone-they arrive every few months to a year for many people, signaling that your information circulates in criminal networks. The FTC reports that among identity theft victims, 69% were targeted more than once, showing that thieves often exploit the same stolen data repeatedly. Criminals use stolen identities to open credit cards, apply for loans, file false tax returns, or even rent property in your name.

The Real Cost of Identity Theft

The damage extends beyond financial loss. Victims spend extensive time resolving fraud, face credit-score damage that takes years to repair, and may discover unauthorized accounts opened years after the original theft. The Federal Trade Commission’s Consumer Sentinel Network Data Book shows that identity theft victims in 2022 spent weeks or months recovering, with about 10% spending a month or longer dealing with the aftermath. This extended recovery period disrupts your finances, your peace of mind, and your ability to access credit when you need it.

Understanding how theft happens is the first step toward protection. The next section reveals the warning signs that indicate you may already be a victim-signs you need to act on immediately.

Warning Signs You’re Already a Victim

Catch Unauthorized Charges Before They Multiply

The moment you notice something off with your finances, act fast. Criminals count on delayed detection to maximize damage. Check your credit card and bank statements monthly, not annually. The Federal Trade Commission reports that victims who caught fraud within 30 days limited their losses significantly compared to those who discovered theft months later. Look for charges you don’t recognize, no matter how small. Fraudsters often test stolen cards with tiny purchases before attempting larger transactions. If you spot even a single unauthorized charge, contact your bank immediately and request a replacement card. Many banks reverse fraudulent charges within days if you report them promptly.

Review Your Credit Reports for Hidden Accounts

Suspicious activity on your credit report reveals theft that’s harder to spot than missing money. Pull your free credit reports from annualcreditreport.com three times per year, spacing them out every four months. Review each report carefully for accounts you never opened, inquiries from companies you didn’t contact, or address changes you didn’t authorize. Hard inquiries from lenders you didn’t apply to signal that someone used your identity to seek credit. The Federal Trade Commission’s Consumer Sentinel Network Data Book shows that new account fraud and credit card fraud rank among the most common identity theft complaints.

If you find suspicious inquiries or accounts, place a fraud alert immediately by contacting any of the three major bureaus: Experian, Equifax, or TransUnion. A fraud alert requires lenders to verify your identity before opening new accounts, creating a critical barrier against further damage. Additionally, consider placing a credit freeze with all three bureaus, which blocks access to your credit file entirely unless you temporarily unfreeze it. Freezes cost nothing and prevent criminals from opening accounts in your name.

Respond to Unexpected Debt Collection Calls

Debt collectors calling about accounts you never opened represents a red flag you cannot ignore. Scammers file false applications for loans, credit cards, or utilities using your stolen information. When you receive a collection call for debt you don’t recognize, do not assume it’s a mistake. Request written verification of the debt within 30 days as required by the Fair Debt Collection Practices Act. If the collector cannot verify the debt or if verification shows fraudulent information, dispute it in writing. File a complaint with the Consumer Financial Protection Bureau simultaneously. This creates an official record that protects you if the same fraudulent account appears on your credit report.

Contact the creditor directly using the phone number on your statement rather than the number provided by the collector, as scammers sometimes pose as legitimate debt collectors. Report the fraud to the Federal Trade Commission at IdentityTheft.gov, which generates a recovery plan tailored to your situation and provides templates for letters to creditors and bureaus. These steps position you to respond effectively when identity theft strikes-and the next section explains exactly what to do when you confirm that theft has occurred.

What to Do If Identity Theft Occurs: Serving South Carolina, including Greenville, Columbia and Charleston

File a Report with the Federal Trade Commission

Speed matters more than panic when you confirm identity theft. The Federal Trade Commission reports that victims who acted within 30 days of discovery limited their financial losses significantly compared to those who waited weeks or months. Your first step is creating an official record at IdentityTheft.gov, the federal government’s dedicated recovery platform. This site generates a personalized recovery plan based on your specific situation and provides ready-made letters to send to creditors, credit bureaus, and debt collectors. The plan outlines exactly which agencies to contact, in what order, and what documentation you need. Print everything and keep copies in a folder-you’ll reference these documents repeatedly over the coming weeks. Filing this report also protects you legally if fraudulent accounts appear later, as it establishes the timeline of your discovery and response.

Contact Your Banks and Credit Card Companies Immediately

Contact each of your banks and credit card companies directly using the phone numbers on your statements, never numbers provided by callers or collection agencies. Tell them you’re a victim of identity theft and ask them to freeze your accounts immediately, review recent transactions, and issue replacement cards. Request written confirmation of fraudulent transactions and the fraud dispute process. Most banks limit your liability to $50 if you report within 60 days, and many waive this entirely if you report promptly. Ask about credit monitoring services your bank may offer for free-many major financial institutions now provide complimentary monitoring to customers.

Place a Fraud Alert on Your Credit Reports

Contact all three credit bureaus-Experian, Equifax, and TransUnion-to place a fraud alert on your credit file. A fraud alert requires creditors to verify your identity before opening new accounts, creating a critical barrier against further damage. This alert lasts one year and costs nothing. If you prefer stronger protection, place a credit freeze instead, which completely blocks access to your credit file unless you temporarily unfreeze it. Freezes also cost nothing and prevent criminals from opening accounts using your stolen identity. You can place both a fraud alert and a freeze if you want maximum protection.

Document Every Communication

Document every phone call with dates, times, names of representatives, and what was discussed. These notes become essential if disputes arise later and creditors claim they never received your fraud report. Keep all written correspondence in one location (a folder, binder, or digital file) so you can access it quickly when you need to reference details or provide proof of your actions to creditors or bureaus.

Final Thoughts

Identity theft remains a persistent threat to South Carolina residents and Americans nationwide, with nine million people falling victim each year. The question “Do I need identity theft protection?” deserves serious consideration based on your personal circumstances-if you receive regular data breach notifications, maintain multiple online accounts, or have dependents relying on your financial stability, the answer leans toward yes. The cost of inaction far exceeds the price of protection when criminals drain accounts, damage credit scores, or file fraudulent tax returns in your name.

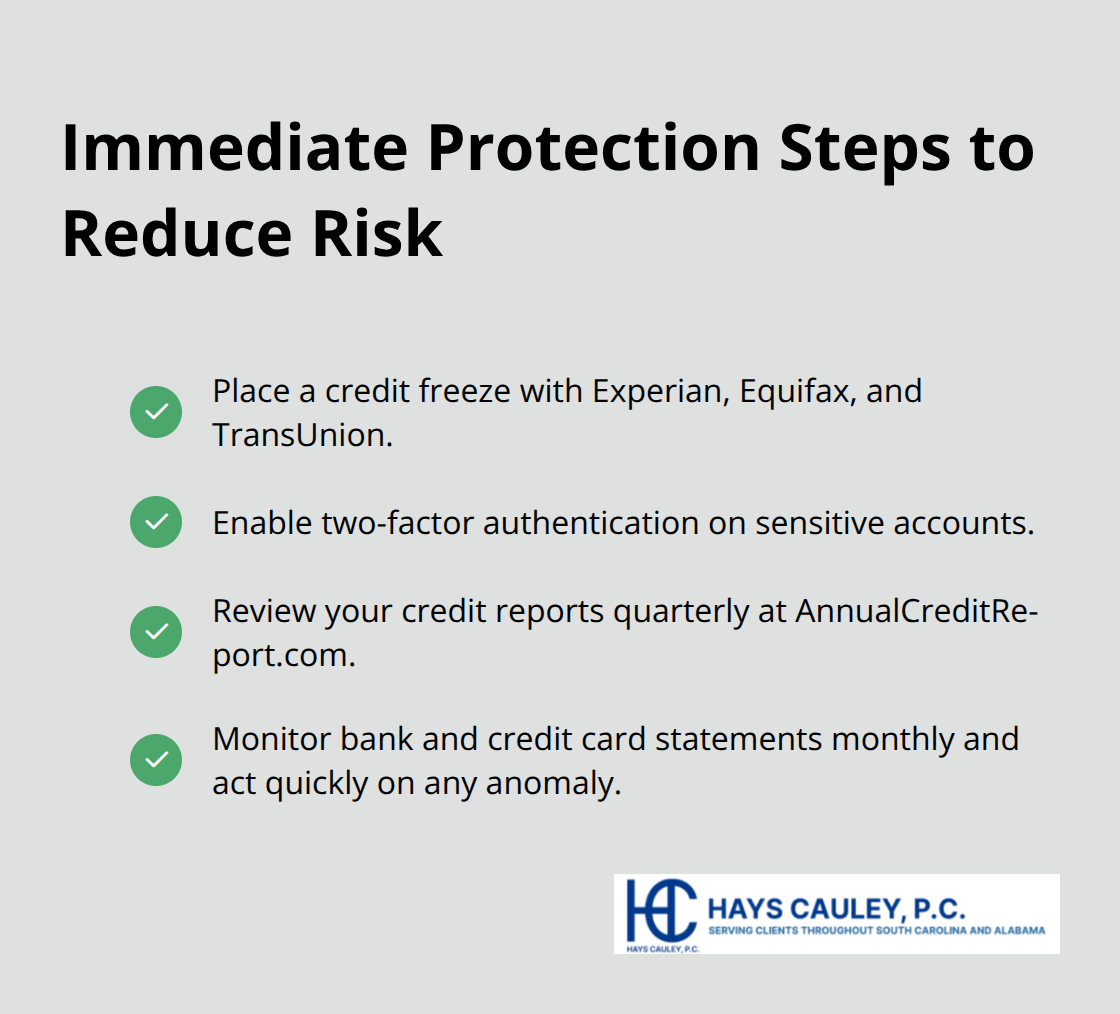

Taking preventative steps now protects your financial future and reduces recovery time if theft occurs. Place a credit freeze with all three bureaus at no cost, enable two-factor authentication on sensitive accounts, review your credit reports quarterly using annualcreditreport.com, and monitor bank and credit card statements monthly rather than annually. These actions create multiple barriers that slow criminals down and give you early warning when something goes wrong. When identity theft strikes, speed determines the outcome-victims who acted within 30 days of discovery limited their losses significantly compared to those who delayed.

We at Hays Cauley, P.C. help South Carolina residents navigate credit reporting issues, identity theft recovery, and debt-related problems that result from fraud. If you’re struggling to resolve identity theft or need guidance on your next steps, contact us for a consultation to discuss your situation and explore your options for recovery and rebuilding.