How to Protect Yourself from Identity Theft

Identity theft happens faster than most people realize. Criminals can open accounts, rack up debt, and damage your credit score without you knowing until it’s too late.

We at Hays Cauley, P.C. understand how devastating this crime can be for South Carolina residents. This guide walks you through the warning signs, immediate steps to take if it happens, and practical ways to protect yourself before trouble starts.

Spot Identity Theft Before It Spirals

The moment someone uses your name to open a credit card or take out a loan, the damage clock starts ticking. South Carolina ranks as the 13th highest state for identity theft reports per 100,000 citizens, meaning your neighbors face real risk. The South Carolina Department of Consumer Affairs reported that identity theft losses totaled over 2.2 million dollars across 431 reports in 2024, with financial theft accounting for nearly 69 percent of all cases. Most victims don’t catch the crime until weeks or months later, which means the thief has already maxed out accounts and trashed credit scores.

Watch for Unauthorized Credit Inquiries

The fastest way to spot identity theft is to watch for unauthorized credit inquiries on your credit file, which often signal someone applying for new accounts in your name. A hard inquiry appears instantly when a lender checks your credit, so pull your free annual credit report and look for lender names you don’t recognize. If you see unfamiliar inquiries, contact those companies immediately and ask them to pull the applications. This single step catches many identity theft cases before criminals open multiple accounts in your name.

Monitor Your Mail and Bills Closely

Missing mail is a massive red flag that most people ignore. Thieves often redirect your statements to a different address or intercept mail at your home to hide fraudulent accounts. If your credit card statement doesn’t arrive on time or you receive unexpected bills from creditors you never contacted, assume identity theft until proven otherwise.

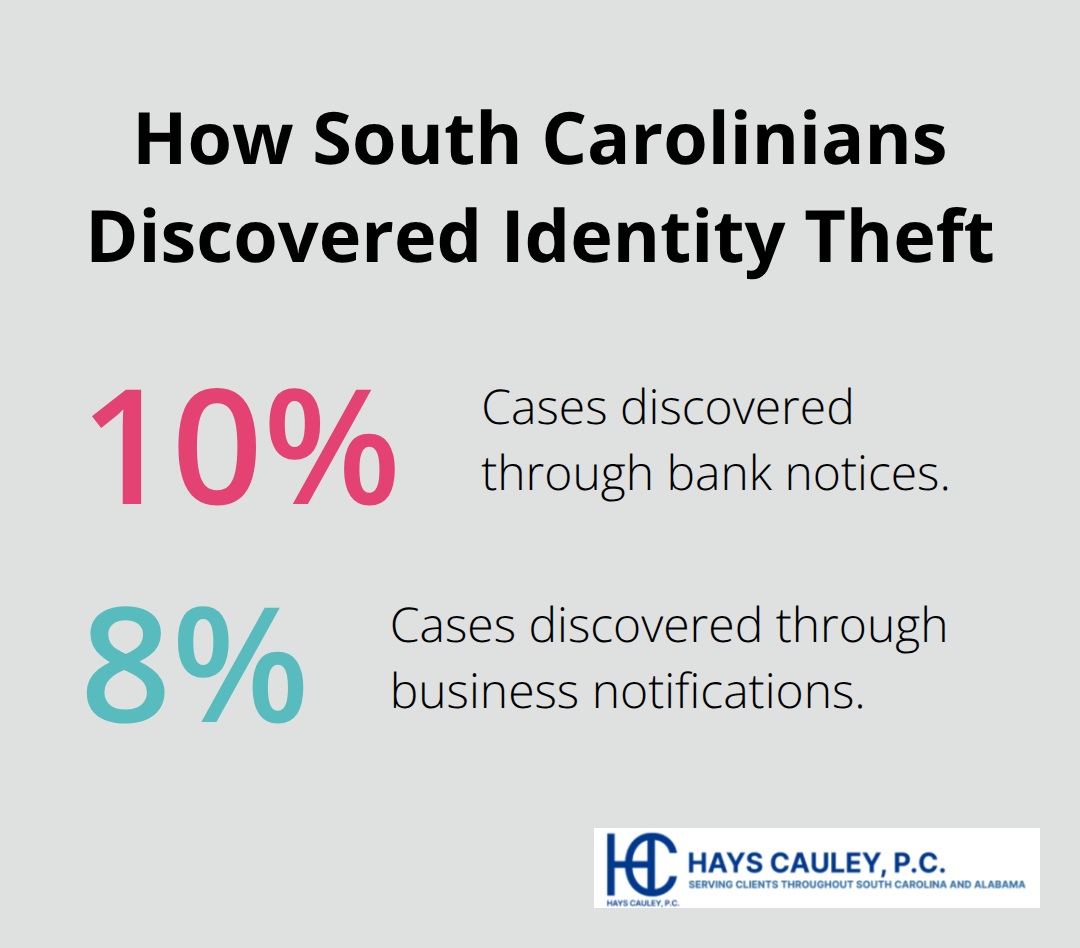

The South Carolina Department of Consumer Affairs found that bank notices and business notifications helped victims discover 10 and 8 percent of identity theft cases respectively, proving that staying alert to correspondence matters. Open and review every statement the moment it arrives, and if something looks wrong, call the company using the number on your actual card or statement, not any number from a suspicious letter.

Recognize Credit Application Rejections as Warning Signs

Denied credit applications or sudden interest rate increases signal that your credit file has been damaged by fraudulent accounts. When you apply for a mortgage, car loan, or credit card and get rejected without explanation, request your credit report immediately to see what’s tanking your score. Legitimate lenders won’t approve new accounts when fraudulent entries appear, so a rejection often means criminals are already working your file. The sooner you catch these red flags, the faster you can stop additional damage and start the recovery process.

Act Fast When Identity Theft Strikes

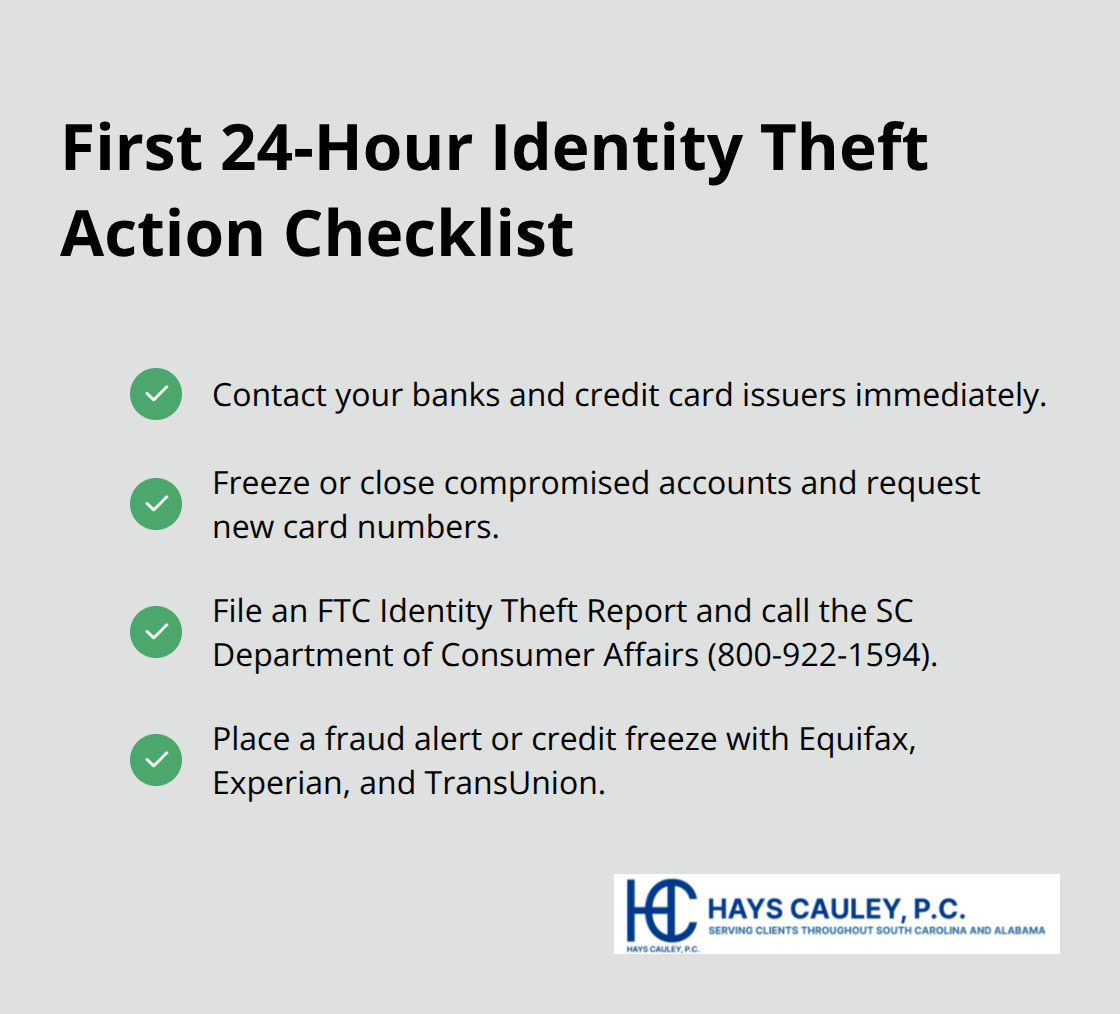

The first 24 hours after discovering identity theft matter more than most people understand. Your immediate actions determine how much additional damage criminals can inflict and how quickly you can reclaim your credit file.

Contact Your Banks and Credit Card Companies Immediately

Call your bank and credit card companies directly using the phone numbers on your actual cards or statements-never numbers from suspicious letters or emails. Tell them fraud has occurred, ask them to freeze or close compromised accounts, and request written confirmation of the fraud report. Banks can reverse unauthorized charges within specific timeframes, but only if you report them quickly, so don’t delay this step. While you’re on the phone, ask each institution to flag your account for fraud and request new cards with different account numbers.

File an Official Report with the FTC and South Carolina

File a report with the Federal Trade Commission at IdentityTheft.gov by selecting Report Identity Theft, or call the South Carolina Department of Consumer Affairs at 800-922-1594. The FTC creates an Identity Theft Report that you’ll need for creditors and credit bureaus, and this report documents the crime officially. This step takes about 15 minutes online but creates a paper trail that protects you legally when disputing fraudulent accounts.

Place a Credit Freeze or Fraud Alert with Credit Bureaus

The final critical action is placing a credit freeze or fraud alert with all three credit bureaus: Equifax, Experian, and TransUnion. A fraud alert notifies lenders that you’ve been a victim and requires them to verify your identity before opening new accounts, which stops most criminals cold. A credit freeze is stronger because it blocks access to your credit file entirely unless you temporarily lift it, and the bureaus must implement a freeze within five business days of your request. You’ll receive a unique PIN to manage the freeze, and removing it takes only three business days once you provide proper identification. South Carolina law allows you to place a freeze at no cost if you’ve been a victim of identity theft, so there’s no financial barrier to this protection.

Monitor Your Credit Reports and Dispute Fraudulent Accounts

After placing the freeze, monitor your credit reports for 60 days minimum by ordering free reports from annualcreditreport.com, watching for any accounts you didn’t open. If you spot fraudulent accounts, dispute them directly with the credit bureau in writing, and the bureau must reinvestigate at no charge and respond within 30 days according to federal law. This monitoring phase catches accounts criminals may have opened before your freeze took effect, and each dispute you file strengthens your case if you need legal help recovering your identity.

Stop Identity Theft Before It Starts

Waiting to catch identity theft after criminals strike puts you in a defensive position where damage is already done. The smarter approach is building layers of protection that make your identity a harder target than easier victims. South Carolina Department of Consumer Affairs data shows that 19 percent of identity theft victims discovered the crime through credit reports, meaning regular monitoring catches problems early when they’re easiest to fix.

Monitor Your Credit File Regularly

Check your credit file at least twice yearly by ordering free reports from annualcreditreport.com, and watch for accounts you never opened or inquiries from lenders you never contacted. If you spot anything suspicious, dispute it immediately in writing with the credit bureau, which must reinvestigate at no charge and respond within 30 days under federal law. This monitoring habit takes 20 minutes per quarter but stops most identity theft from spiraling into years of recovery work.

Secure Your Passwords and Digital Accounts

Your digital security determines whether criminals can access accounts that hold your most sensitive information. The Cybersecurity and Infrastructure Security Agency recommends passwords with at least eight characters mixing uppercase, lowercase, numbers, and special characters, plus two-factor authentication on every account that offers it. Never reuse passwords across different sites because a breach at one company gives criminals access to your entire digital life.

Protect Physical Documents and Mail

For physical documents, invest in a cross-cut shredder and destroy anything containing your Social Security number, account numbers, or dates of birth before throwing it away. Thieves pull financial statements from trash and recycling bins regularly, so shredding is not optional. Keep documents with personal information in a locked drawer or safe at home, limit what you carry daily (leave your Social Security card and Medicare card at home unless needed), and pick up mail promptly using a secure mailbox to prevent mail theft. These actions cost minimal money but eliminate the easiest ways criminals access your identity.

Final Thoughts

Identity theft and how to protect yourself requires two parallel strategies that work together. First, you stop criminals before they strike by monitoring your credit regularly, securing your passwords with two-factor authentication, and destroying documents containing personal information. Second, you respond fast if theft happens by contacting banks, filing reports with the FTC and South Carolina Department of Consumer Affairs, and placing a credit freeze with all three bureaus. Neither strategy alone is enough, but combined they dramatically reduce your risk and limit damage.

South Carolina residents face real threats, with the state ranking 13th nationally for identity theft reports per 100,000 citizens and 2024 showing over 2.2 million dollars in losses across 431 cases. The good news is that most identity theft is preventable with consistent action-regular credit monitoring catches 19 percent of cases before criminals cause major damage, while strong passwords and two-factor authentication stop digital account breaches. Shredding documents and securing mail eliminate the easiest theft methods that criminals exploit.

If you discover identity theft, speed matters because the first 24 hours determine how much additional fraud criminals can commit. Contact your banks immediately, file reports with the FTC at IdentityTheft.gov and the South Carolina Department of Consumer Affairs at 800-922-1594, and place a credit freeze with Equifax, Experian, and TransUnion. If you need legal help addressing identity theft or credit reporting issues, contact us at Hays Cauley, P.C. to discuss your specific situation and explore your options for recovery.