Identity Theft Recovery Steps: Rebuilding After a Breach

Identity theft can derail your finances and peace of mind in minutes. The good news is that identity theft recovery steps are straightforward when you know what to do first.

At Hays Cauley, P.C., we’ve helped many South Carolina residents navigate this process. This guide walks you through immediate actions, rebuilding your credit, and long-term protection strategies.

First Steps When Identity Theft Strikes

Act Immediately to Protect Your Accounts

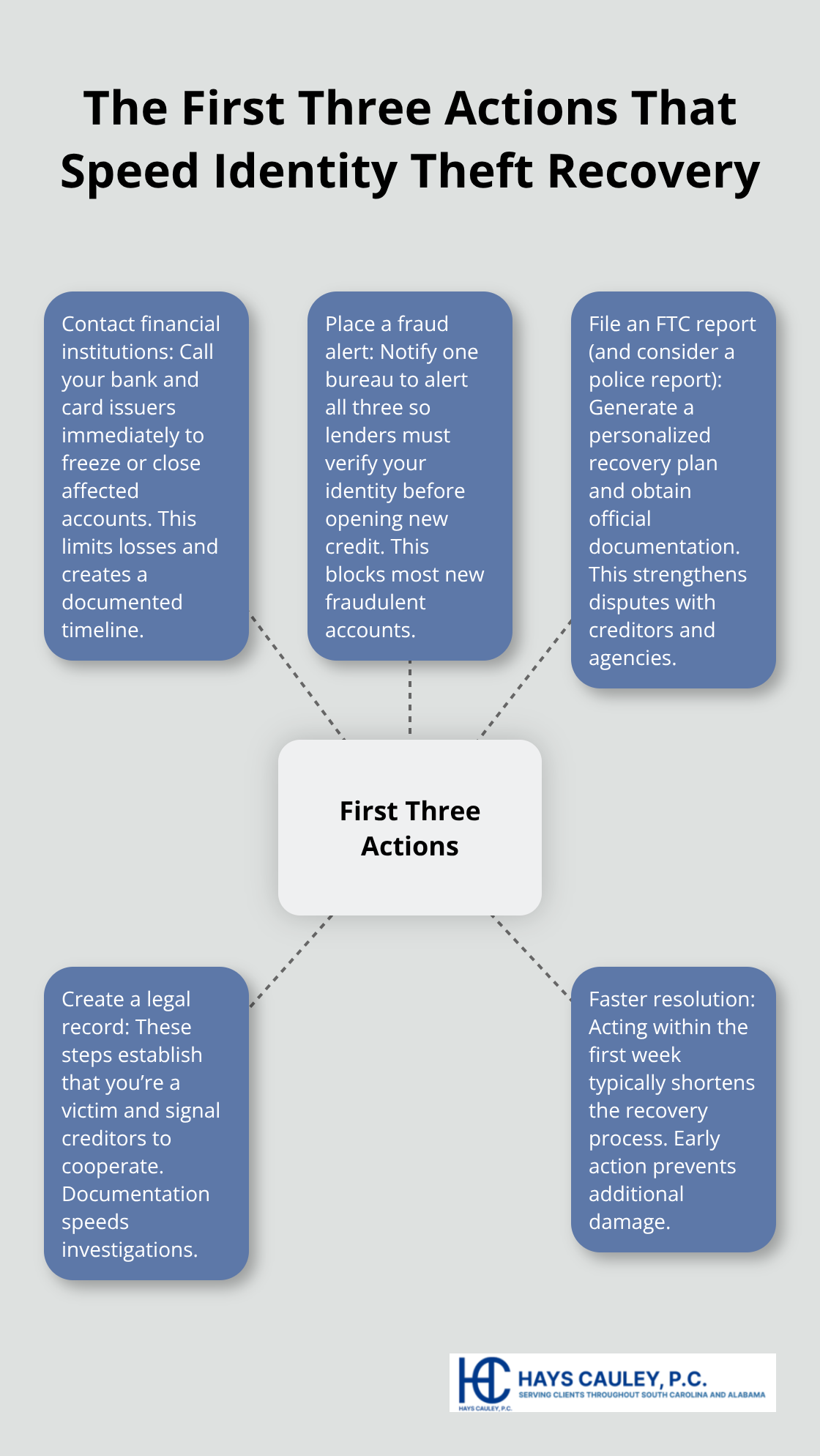

The first hours after discovering identity theft matter most. Call your bank and credit card companies immediately, before anything else. Tell them your account may be compromised and ask them to freeze or close the affected accounts. Many financial institutions have fraud departments that operate 24/7, so don’t wait for business hours. Request written confirmation of your call and note the date, time, and representative’s name. Your bank can reverse unauthorized charges, but only if you report them quickly. Federal law limits your liability to $50 per card if you report fraud within 60 days, according to the Federal Trade Commission.

Contact the Credit Bureaus for a Fraud Alert

After you contact your financial institutions, place a fraud alert with the three nationwide credit bureaus: Equifax at 800-685-1111, Experian at 888-397-3742, and TransUnion at 888-909-8872. You only need to call one bureau, and that bureau will notify the other two. The initial fraud alert lasts one year and requires lenders to verify your identity before opening new credit in your name. This single action stops most identity thieves because they cannot open accounts without jumping through extra verification steps.

File Your FTC Report and Police Report

Next, file a report with the Federal Trade Commission at IdentityTheft.gov. This step generates a personalized recovery plan tailored to your situation, covering issues beyond just credit fraud (including government ID theft, utility account takeover, and tax identity theft). The FTC’s recovery plan coordinates actions with lenders, creditors, and government agencies to help you rebuild. You can also file a police report with your local law enforcement agency, which gives you additional legal protections and documentation for disputing fraudulent accounts. Bring copies of your credit reports and any evidence of unauthorized activity to the police station.

Why These Three Actions Matter

These three actions-contacting financial institutions, placing a fraud alert, and filing an FTC report-create a legal record that protects you and signals to creditors that you’re a victim. Most identity theft victims who take these steps within the first week see significantly faster resolution than those who delay. With your immediate defenses in place, you can now focus on examining what damage the theft caused to your credit profile.

Rebuild Your Credit After Identity Theft: Serving South Carolina, including Greenville, Columbia and Charleston

Get Your Credit Reports and Spot the Damage

Your credit reports show exactly what accounts opened in your name and which charges are fraudulent. Obtain your free credit reports immediately from annualcreditreport.com or by calling 877-322-8228. Federal law entitles you to one free report from each of the three bureaus every 12 months, and you can check your reports for free once per week at annualcreditreport.com. Go through each report line by line and mark every account you don’t recognize. Look for new credit cards, loans, utility accounts, or phone lines opened without your permission. Many identity theft victims find unauthorized accounts within the first two weeks of checking their reports. Write down the account numbers, creditor names, and amounts for every fraudulent entry you find.

Contact Creditors and File Disputes

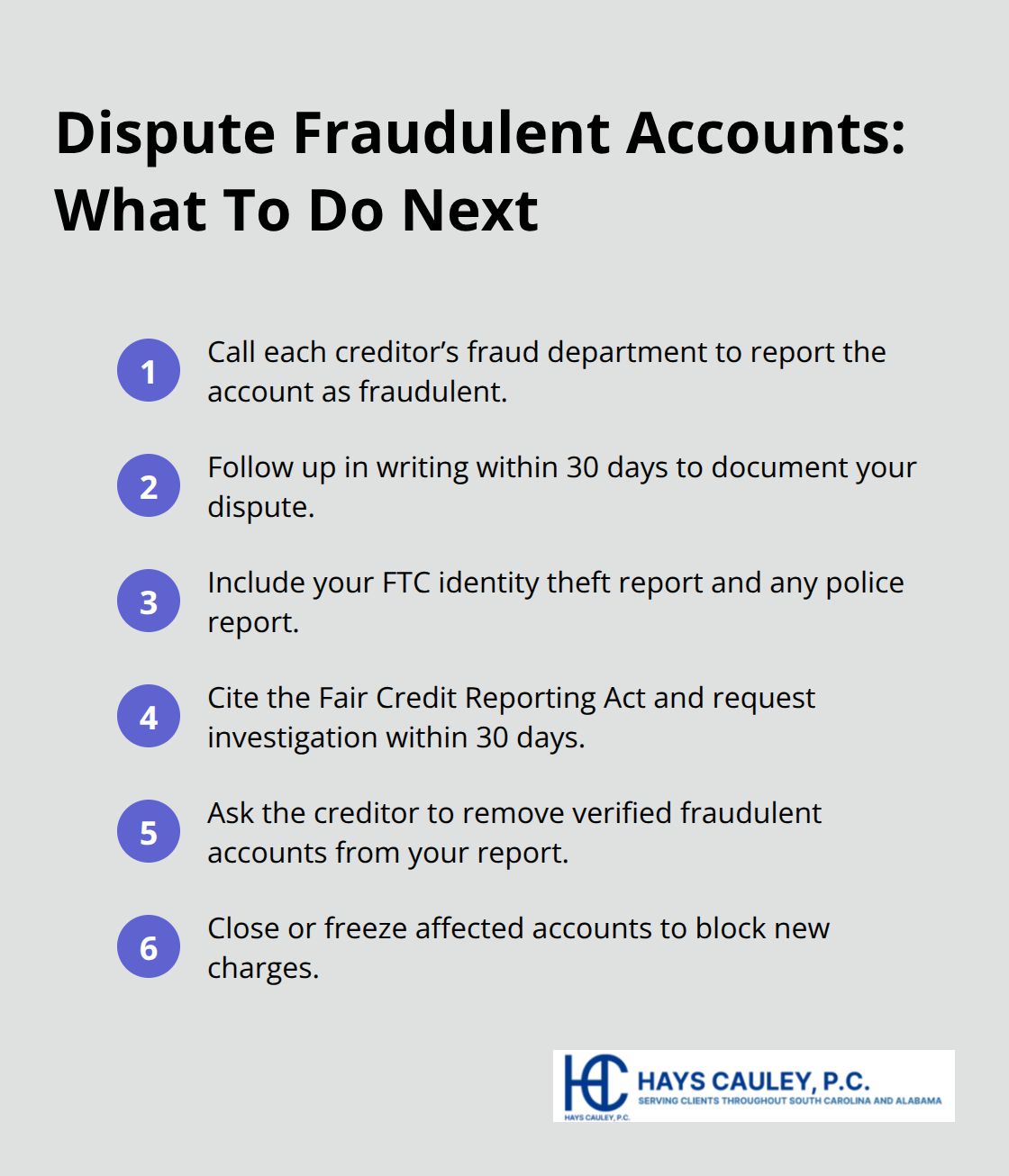

Disputing fraudulent accounts is where recovery actually happens. Contact each creditor directly and tell them the account is fraudulent, then follow up in writing within 30 days. Include copies of your FTC identity theft report and police report with your dispute letter. The Fair Credit Reporting Act requires creditors to investigate disputes within 30 days and remove verified fraudulent accounts from your credit report.

Call the fraud department of every company where fraud occurred to close or freeze the affected accounts so new charges cannot be added. Change your passwords and PINs for any legitimate accounts immediately. File disputes with the credit bureaus themselves by submitting a dispute form on their websites or through your online account.

Monitor Your Credit Recovery Progress

Your credit score will take a hit after identity theft, but it recovers faster than most people expect. Monitor your credit score monthly using free tools available from your bank or credit card company. Most victims see their scores rebound within 6 to 12 months as fraudulent accounts are removed and the fraud alert expires. Do not obsess over small score fluctuations during recovery. Focus instead on removing fraudulent entries and preventing new unauthorized accounts. As your credit stabilizes, you’ll want to implement stronger protections that stop identity thieves before they strike again.

Protecting Yourself from Future Identity Theft

Set Up Credit Monitoring to Catch Fraud Early

Credit monitoring services watch your credit reports and alert you to suspicious activity before it spirals into major fraud. After identity theft, most victims benefit from continuous monitoring beyond the first year of free service offered by the breached company. Services like Equifax Complete Premier provide three-bureau credit scores and reports with ongoing monitoring, alerts, and dark web monitoring for your Social Security number. These tools cost between $10 and $30 monthly and catch new fraudulent accounts within days instead of months. Check your credit reports weekly at annualcreditreport.com for the first few months after identity theft recovery, then monthly afterward. This habit catches mistakes early and prevents small problems from becoming expensive ones.

Strengthen Your Passwords and Enable Two-Factor Authentication

Your passwords and authentication methods are your strongest defense against future identity theft. Use passwords with at least 16 characters that combine uppercase letters, numbers, and symbols, and never reuse the same password across multiple accounts. Enable two-factor authentication on every financial account, email address, and sensitive service you use, including your bank, credit card companies, and the three credit bureaus themselves. Two-factor authentication requires a second verification step beyond your password, making it nearly impossible for thieves to access your accounts even if they steal your credentials. After a breach, change logins, passwords, and PINs for all compromised accounts immediately and update passwords for any accounts where you reused credentials.

Review Financial Statements Consistently

Review your financial statements weekly during the first six months of recovery, then at least monthly afterward. Look for unfamiliar charges, new accounts, or suspicious activity that escaped initial detection. Many identity theft victims discover secondary fraud months after the initial breach because they failed to monitor statements consistently. Set calendar reminders for the first of each month to review statements from every financial institution where you hold accounts (your bank, credit cards, investment accounts, and loan servicers).

This routine takes 20 minutes but catches fraud that monitoring services sometimes miss, protecting your recovery progress and preventing new damage.

Final Thoughts

Identity theft recovery steps take time, but most victims regain financial stability within 6 to 12 months when they act decisively. Your first week determines whether you stop the thief cold or spend months fighting fraudulent accounts. Contact your bank, place a fraud alert, file your FTC report, then systematically dispute fraudulent accounts and monitor your credit reports.

Ongoing vigilance matters after identity theft because thieves often return to victims they’ve already compromised. Review your financial statements monthly, check your credit reports quarterly, and keep your passwords and two-factor authentication current (these habits take minimal time but catch secondary fraud before it causes additional damage). Many victims who skip this step discover new unauthorized accounts months later, forcing them to restart their recovery process.

Resources exist to support you throughout recovery and beyond. The Federal Trade Commission’s IdentityTheft.gov provides free personalized recovery plans, and annualcreditreport.com gives you free access to your credit reports weekly. If you face complex disputes, creditor resistance, or credit reporting errors that won’t resolve, we at Hays Cauley, P.C. help South Carolina residents navigate these challenges.