SC credit report protections: What They Do and Don’t Do

Your South Carolina credit report protections give you real power-but only in specific situations. Many people assume these laws fix every credit problem, when the truth is more complicated.

At Hays Cauley, P.C., we help clients understand exactly what SC credit report protections actually do and where the gaps exist. This guide shows you the real boundaries of your rights and how to use them effectively.

What South Carolina Credit Report Laws Actually Protect

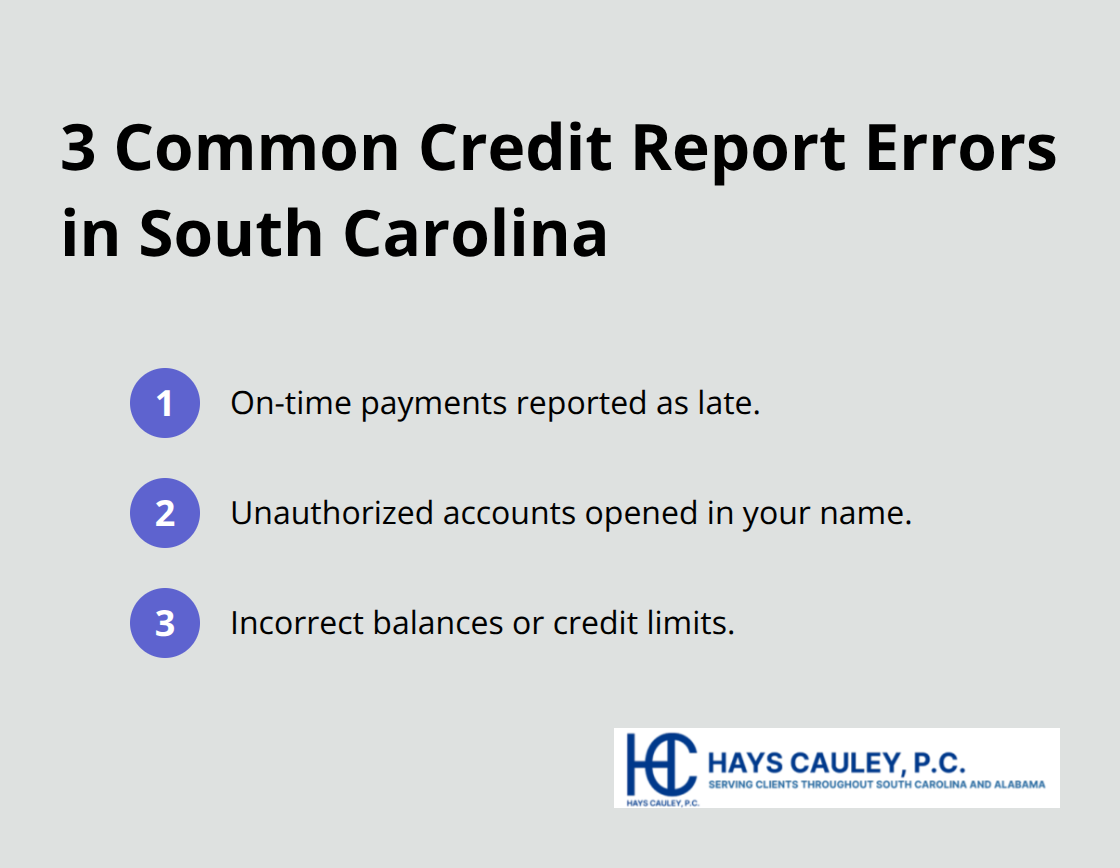

South Carolina’s credit report protections operate within strict boundaries, and understanding those boundaries prevents wasted effort on disputes that won’t succeed. The Fair Credit Reporting Act combined with South Carolina’s Title 37, Chapter 20 gives you the right to challenge inaccurate information, access your reports, and stop unauthorized use of your credit file. The FTC reports that about one in five consumers have errors on their credit reports, making accuracy disputes the most practical tool available to you. When you find an error, credit bureaus must investigate within 30 days under federal law, and South Carolina requires furnishers (creditors reporting the information) to investigate independently as well. This dual investigation approach matters because furnishers sometimes correct errors faster than bureaus. You can dispute in writing via certified mail with return receipt, and the bureau must remove information it cannot verify within that 30-day window. The three most common errors to watch for are late payments reported as late when paid on time, unauthorized accounts opened in your name, and incorrect balances or credit limits. You should document everything from the start: print exact account names and numbers, reported balances, and the specific inaccuracies.

A successful dispute typically improves your credit score within 30 to 45 days, with the impact varying by how many errors existed and how significantly they affected your score.

Accessing Your Credit Information Without Barriers

You have the absolute right to see what’s in your credit report, and South Carolina law guarantees this access at no cost. Pull free annual reports from all three bureaus through annualcreditreport.com, and Equifax offers six additional free reports per year by calling 1-866-349-5191. Many people waste money on paid credit monitoring services when free options exist. If a creditor denies you credit based on your report, you receive a free copy of that specific report regardless of when you last pulled one. Your report includes personal details, credit accounts, payment history, negative marks, and recent inquiries. Review all sections carefully because errors hide in plain sight. South Carolina law also gives you the right to know who accessed your credit report within the last year (two years for employment purposes), which helps you detect identity theft early. FTC data showed 18,935 identity theft cases in South Carolina in 2022, making this monitoring capability genuinely valuable.

Security Freezes and Access Control

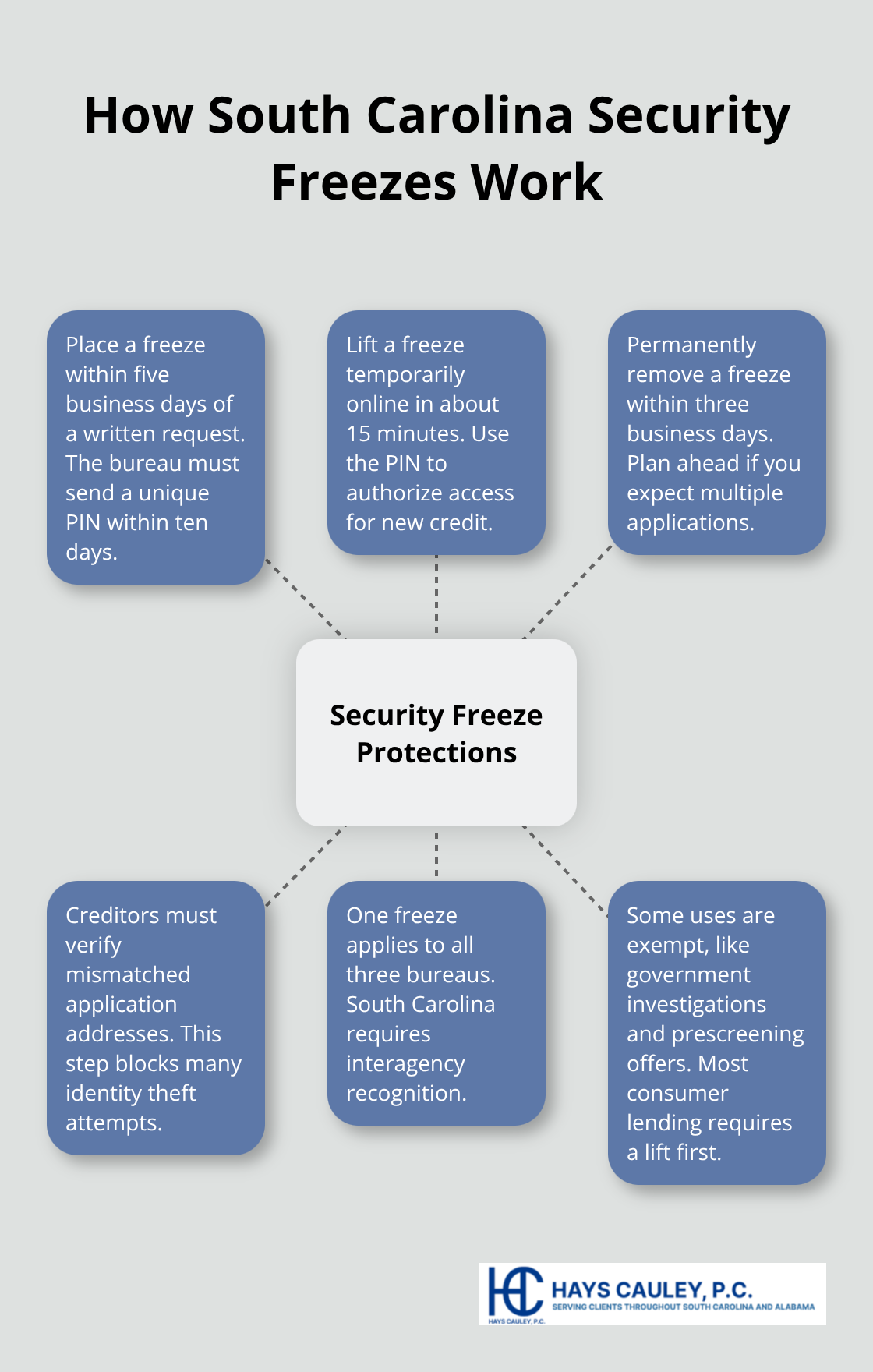

South Carolina provides security freezes at no cost, and this protection stops most lenders from accessing your report without explicit permission. You can place a freeze within five business days of a written request, and the bureau must provide you a unique PIN within ten days. Temporary electronic lifts take about 15 minutes and permanent removal takes three business days. When you apply for new credit and the application address differs from the bureau’s file, creditors must verify the address before issuing cards or approving accounts. This address verification requirement catches identity theft attempts before accounts open in your name.

Freezes apply across all three major bureaus because South Carolina requires interagency recognition, so one freeze covers Equifax, Experian, and TransUnion simultaneously. Certain uses remain exempt from freezes (including government investigations and prescreening offers), but most consumer lending requires you to lift the freeze first. Understanding these protections sets the stage for knowing what you can actually accomplish when errors appear on your report.

What Your SC Credit Report Rights Cannot Fix

Credit report laws protect you in narrow, specific situations, and most people overestimate what these protections accomplish. The Fair Credit Reporting Act and South Carolina law do not fix every credit problem or erase legitimate negative information from your file. If you missed payments and paid them late, that accurate history stays on your report for seven years regardless of disputes. Credit bureaus can legally report accurate late payments, charge-offs, collections, judgments, and liens because these items truthfully reflect your payment history. You cannot dispute accurate information simply because it damages your credit score. Many people contact credit bureaus expecting removal of factual negative marks and waste months on futile disputes.

South Carolina law specifically protects you against inaccurate information, unauthorized accounts, and identity theft, but it does not protect you against the consequences of your own late payments or defaults. The FTC receives thousands of complaints annually from consumers who misunderstand this boundary. Negative information that is accurate, properly reported, and within the seven-year window (ten years for bankruptcy) will remain on your report. Your only realistic option involves improving your credit behavior going forward by paying on time and reducing balances. Disputing accurate information wastes your time and the credit bureau’s resources.

Why the 30-Day Investigation Window Misleads You

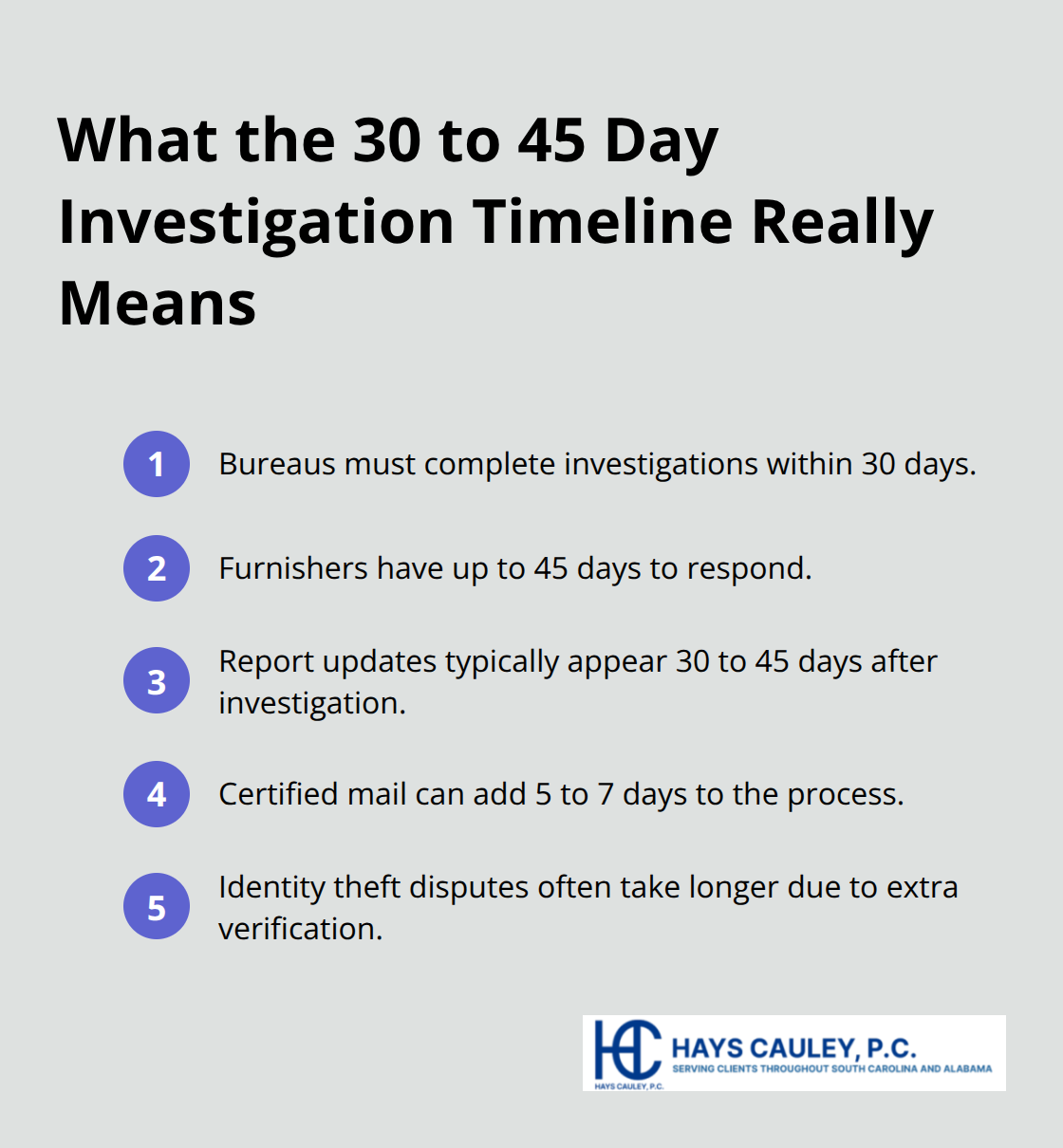

Dispute timelines create another misconception that frustrates many South Carolina residents. While credit bureaus must complete investigations within 30 days under federal law, this does not mean your credit report updates within 30 days or that your score improves immediately. The 30-day window covers only the bureau’s investigation period, and furnishers (the creditors reporting the information) have up to 45 days to respond independently. After the bureau completes its investigation and removes inaccurate information, the updated report typically appears within 30 to 45 additional days.

If you filed your dispute on January 1, you should not expect to see results on your credit report until mid-February or later. Many people assume the 30-day rule means instant correction and become frustrated when their score does not improve within weeks. Identity theft cases take considerably longer because the furnisher must investigate whether someone fraudulently opened the account, which requires additional verification steps beyond standard disputes. You must also account for mail delivery time when disputing via certified mail with return receipt, which adds five to seven days to the process.

How to Accelerate Results Across Multiple Agencies

Sending disputes simultaneously to both the credit bureau and the furnisher accelerates results because the furnisher may correct the error faster than the bureau processes its investigation. This dual approach (sending to both the bureau and the creditor) often yields faster corrections than waiting for the bureau alone. The furnisher sometimes corrects errors within weeks rather than the full 45-day window, which means your report updates sooner. Coordinating these simultaneous disputes requires you to send separate letters with identical documentation to each entity, but the time savings justify the extra effort.

What Credit Laws Cannot Cover at All

Gaps exist in what credit laws cover at all. Medical debt, utility bills, rental history, and employment records do not appear on standard credit reports, so credit report laws cannot help you dispute these items. If a utility company reported you to a collection agency and that collection appears on your report, you can dispute the collection. However, if the utility simply cut off your service for non-payment without reporting to a bureau, credit report protections do not apply because no credit report entry exists. Certain types of debt fall outside credit reporting entirely, meaning your legal remedies differ significantly.

Understanding these boundaries prevents you from pursuing disputes that cannot succeed and helps you focus on actionable steps that actually improve your financial situation. The next section shows you exactly how to leverage the protections that do work, starting with obtaining and reviewing your actual credit report to identify which errors you can realistically challenge.

How to Get Results From Your SC Credit Report Rights

Obtain and Review Your Credit Report Systematically

Start with the foundation: obtain your actual credit report and review it methodically before filing any disputes. Pull free annual reports from annualcreditreport.com or call 1-877-322-8228, and request one report every four months rather than all three at once. This staggered approach lets you monitor changes across the year and catch fraudulent activity faster. When your report arrives, examine every section systematically. Look for unrecognized accounts, duplicate listings, misapplied payments, incorrect balances, outdated negative items, and wrong personal information. The FTC found that one in five consumers have errors on their reports, so assume you will find something worth investigating.

Build Your Evidence File for Each Error

Create a separate file for each error you identify, recording the exact account name, account number, reported balance, and the specific inaccuracy. Gather supporting documents like bank statements, payment records, and correspondence with the creditor. This documentation becomes your evidence when you dispute, and credit bureaus take disputes more seriously when you attach proof rather than making vague claims.

Send Disputes to Both the Bureau and Furnisher

Send written disputes to both the credit bureau and the furnisher simultaneously using certified mail with return receipt. Address your dispute to the bureau’s dispute department and include your name, address, account number, dispute date, the specific inaccuracy, why it is wrong, and your supporting documents. The bureau must investigate within 30 days and remove information it cannot verify. Send an identical dispute package to the furnisher at the same time because furnishers often correct errors faster than bureaus investigate them. This dual approach typically accelerates results by two to three weeks compared to disputing the bureau alone.

Track Your Timeline and Monitor Progress

Track your timeline carefully: expect the bureau to complete investigation around day 30, then allow another 30 to 45 additional days for the corrected information to appear on your report. Check your report again around day 35 after mailing to see if the bureau has removed the inaccurate item. If the error persists after the investigation period, the bureau may have verified the information with the furnisher, which means you need different evidence or legal review. At this point, contact a consumer protection law firm to evaluate whether the investigation was adequate or whether violations occurred.

Address Identity Theft and Implement Security Measures

For identity theft cases, place a fraud alert immediately by contacting any one bureau, which alerts all three. South Carolina law lets you place a free security freeze within five business days of a written request, stopping most lenders from accessing your report without your explicit permission. Lift the freeze temporarily when you apply for new credit by providing your PIN, which takes 15 minutes electronically. Monitor your report every 30 days during disputes and continue checking quarterly after disputes resolve because criminals sometimes attempt identity theft months or years after initial fraud. Document every action you take: keep originals of all correspondence, record dates and names of anyone you contact, and maintain a timeline of all events.

Final Thoughts

South Carolina credit report protections give you real tools to fix inaccurate information, access your reports, and stop unauthorized use of your credit file. The Fair Credit Reporting Act combined with South Carolina’s Title 37, Chapter 20 creates a framework that works when you understand its actual boundaries. You can dispute errors at no cost, place security freezes without fees, and hold credit bureaus accountable for investigations that fall short.

The gap between what people expect and what SC credit report protections actually accomplish causes frustration and wasted effort. Accurate late payments stay on your report for seven years regardless of how many times you dispute them, and legitimate collections, charge-offs, and judgments remain reportable as long as they are factual and within the reporting window. Your real power lies in identifying inaccurate items, documenting them thoroughly, and sending disputes to both the credit bureau and the furnisher simultaneously.

Pull your free credit reports every four months through annualcreditreport.com and review them systematically for errors. If disputes seem inadequately investigated or errors persist, contact a consumer protection law firm to evaluate whether violations occurred. We at Hays Cauley, P.C. help South Carolina residents understand their credit rights and pursue remedies when bureaus or furnishers fail to investigate properly, serving South Carolina, including Greenville, Columbia and Charleston.