FCRA compliance requirements: What You Need to Know to Protect Your Credit

Your credit report affects everything from loan approvals to interest rates. Errors on your report can cost you thousands of dollars, yet many people don’t know their rights under the Fair Credit Reporting Act.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, understand FCRA compliance requirements and fight back against violations. This guide shows you what protections you have and how to take action.

What the FCRA Actually Is and Why You Should Care

The Fair Credit Reporting Act, codified at 15 U.S.C. § 1681 and following, is a federal law that controls how your credit information gets collected, used, and shared. It sounds dry, but it’s the only thing standing between your financial life and chaos. The FCRA applies to credit reporting agencies, creditors who report your payment history, and anyone else who pulls your credit file. The Federal Trade Commission enforces this law, and since the Dodd-Frank Act shifted most rulemaking to the Consumer Financial Protection Bureau, you have two agencies watching compliance. This matters because violations are common-the CFPB’s enforcement actions consistently show that credit bureaus and creditors fail to investigate disputes properly, report inaccurate information, and access reports without legitimate business reasons.

Why Accuracy Matters More Than You Think

Inaccurate credit information costs real money. A single error can drop your credit score by 100 points or more, which translates directly to higher interest rates on mortgages, car loans, and credit cards. The FCRA requires that creditors report accurate data to all three bureaus consistently, yet the FTC’s guidance on 40 years of FCRA experience shows this doesn’t happen reliably. Settled debts reported as outstanding, closed accounts listed as active, and late payments you actually paid on time are the most frequent violations we see. Credit bureaus must maintain reasonable procedures to verify accuracy before reporting, and furnishers (the creditors and data suppliers) must promptly correct errors when notified of disputes. If they don’t, you have legal remedies available.

Your Right to Access Your Credit Report

You have the absolute right to access your credit report for free once per year from each of the three major bureaus through annualcreditreport.com. You can also get free weekly reports now due to temporary expansions of credit monitoring access. The FCRA explicitly requires that credit reporting agencies provide you with a clear, understandable copy of your file and explain what each item means. When a creditor or insurer makes an adverse decision based on your report-denying you credit, charging higher rates, or rejecting your rental application-they must notify you and tell you which bureau provided the information. This adverse action notice is your early warning system for problems on your file.

How to Spot Problems and Take Action

Check your reports at least annually, and if you spot errors, the FCRA gives you the power to dispute them directly with the bureau and the company that reported the false information. The law requires credit bureaus to investigate your dispute within 30 days and correct or delete inaccurate items. Furnishers must also respond to your dispute and update their records across all three bureaus. When errors persist despite your efforts, violations have occurred-and that’s when understanding your next steps becomes essential.

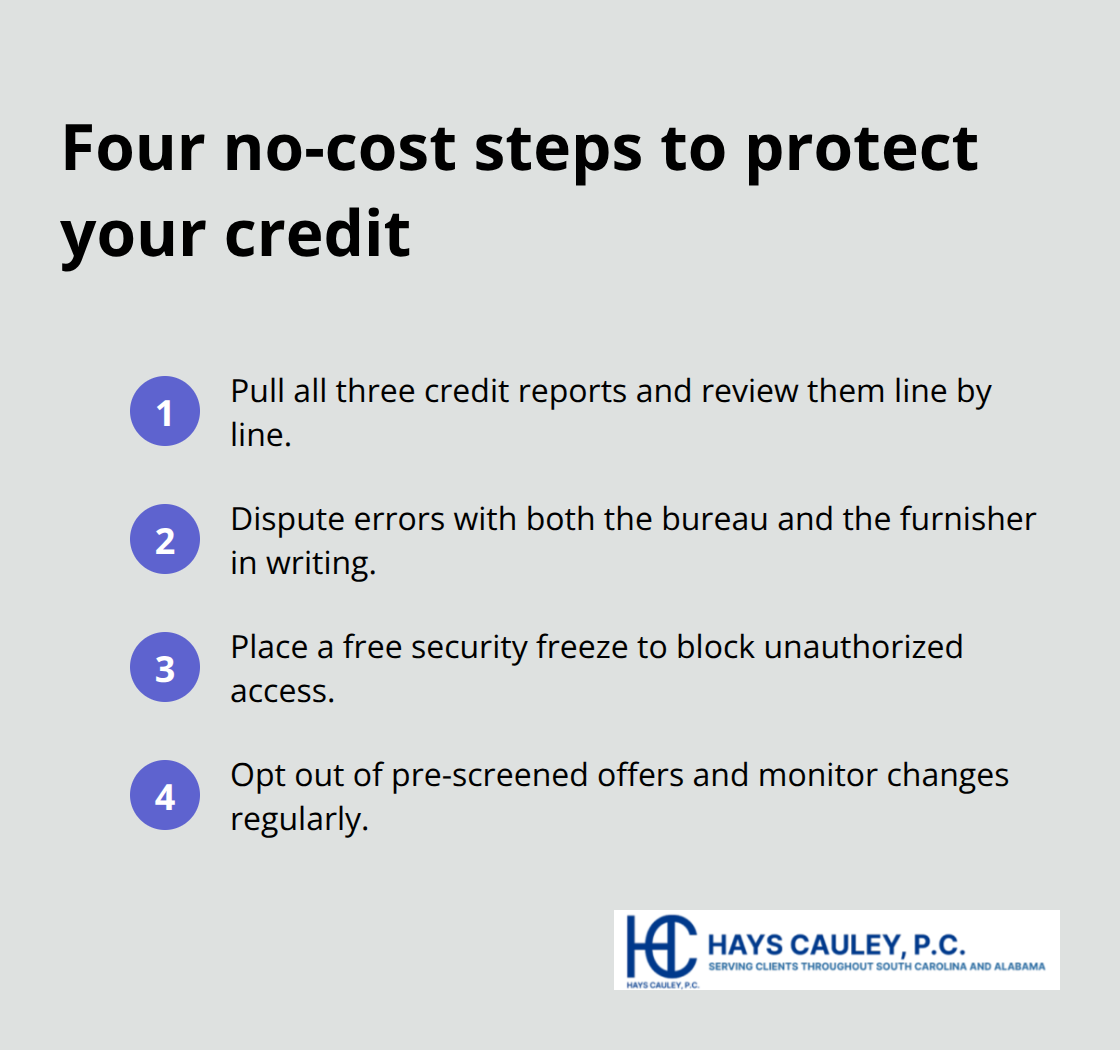

What You Can Actually Do About Your Credit Report

Pull Your Reports and Review Them Carefully

Start by obtaining your credit reports from all three bureaus at annualcreditreport.com and review them line by line. Look for accounts you don’t recognize, balances that don’t match what you owe, late payments on accounts you paid on time, and negative information older than seven years (ten years for Chapter 7 bankruptcy). The FTC reports that one in five consumers finds errors on their credit files, and roughly one in twenty discovers errors serious enough to affect credit decisions. These aren’t rare problems-they’re widespread. Most people skip this step entirely, which means errors persist unchallenged and damage their financial lives.

File a Dispute When You Find Errors

When you find an error, file a dispute immediately with the credit bureau that reported it and also contact the furnisher (the company that supplied the information). The FCRA requires bureaus to investigate within 30 days and correct or delete inaccurate items. Furnishers must do the same and then update all three bureaus with corrections. Send your dispute in writing and keep copies of everything. The 30-day clock is strict, and documentation protects you if the bureau ignores your complaint. This written record becomes critical if you later need to pursue legal action against a bureau or furnisher that refuses to correct errors.

Use a Security Freeze to Block Unauthorized Access

The security freeze costs nothing and blocks credit access without your permission. South Carolina law allows you to place a freeze within five business days of a written request, and the credit reporting agency must remove or temporarily lift it within three business days of your request. You’ll receive a unique PIN or password to control who accesses your file. This is your best defense against identity theft and fraudulent accounts opened in your name. A freeze stops most credit inquiries cold, which means legitimate creditors won’t access your file unless you temporarily lift the freeze during the application process.

Opt Out of Pre-Screened Offers and Monitor Results

You can opt out of pre-screened credit offers by calling 1-888-5-OPTOUT or visiting OptOutPrescreen.com. These offers are based on soft inquiries into your credit file, and opting out reduces the volume of solicitations and slightly lowers your risk of identity theft. None of these steps require hiring anyone-you do them yourself at no cost. The CFPB’s Consumer Complaint Database shows that consumers who monitor their reports and file disputes catch errors faster and recover from violations more effectively than those who ignore their files. Act on what you find, and if a bureau or furnisher refuses to correct errors after your dispute, the violations may entitle you to damages under the FCRA.

The Three Violations That Destroy Your Credit Most Often

Outdated Negative Information That Won’t Disappear

Outdated negative information remains one of the most persistent violations we encounter. The FCRA sets clear timelines: most negative items fall off after seven years, and Chapter 7 bankruptcies after ten years. Yet credit bureaus report accounts as active years after you paid them off, list charge-offs that should have aged out, and fail to update bankruptcy discharge dates. The FTC found that furnishers report settled debts as outstanding and continue reporting late payments long after the statute of limitations passed. South Carolina law reinforces these protections through 37-20 provisions that cross-reference federal FCRA standards.

When a bureau ignores these timelines, it’s not a technical error-it’s a willful violation. Willful violations can justify damages of triple actual harm or at least $1,000 per violation, plus attorney fees. This means a single outdated item on your report can result in substantial recovery if you pursue legal action against the responsible party.

Refusal to Correct Errors After You Dispute Them

The second major violation occurs when bureaus and furnishers refuse to correct errors after you dispute them. The FCRA mandates investigation within 30 days, but the CFPB’s enforcement actions consistently show that bureaus conduct sloppy investigations, ignore furnisher responses, and fail to update all three bureaus when corrections occur. If you dispute a balance, a late payment, or account ownership and the bureau doesn’t correct it within the required timeframe, a violation has occurred.

Furnishers face the same obligation-they must investigate and report corrections back to all three bureaus. Discrepancies across bureaus are common because companies report to some bureaus but not others, leaving inaccurate information on your file even after you’ve fought to correct it. Documentation of your dispute letter, the bureau’s response, and follow-up attempts becomes critical evidence if you later need to pursue claims against the violating parties.

Accessing Your Report Without Legitimate Business Reasons

Accessing your credit report without a permissible purpose constitutes the third violation category. Creditors, employers, landlords, and insurers can only pull your report if they have a legitimate business need connected to a credit decision. A creditor cannot pull your file just to check on you, and an employer cannot access your report without your permission. When this occurs, it’s an impermissible purpose violation.

More commonly, violations occur when companies fail to notify you that they pulled your report or fail to provide adverse action notices when they deny you credit based on your file. These notification failures prevent you from catching errors early. South Carolina residents in Greenville, Columbia, and Charleston should know that identity theft can destroy your credit score and drain your finances in weeks, and if any of these three violations occur on your file, we at Hays Cauley, P.C. can evaluate whether you have grounds for legal action and help you recover damages from the violating parties.

Final Thoughts

Protecting your credit starts with consistent monitoring and swift action when problems surface. Check your reports at least once yearly through annualcreditreport.com, and watch for outdated negative information, refusal to correct errors, and unauthorized access. The moment you spot a problem, file a written dispute with the credit bureau and the furnisher, then keep detailed records of every communication. Most errors get corrected within 30 days when you follow this process, but some companies ignore their legal obligations and violate FCRA compliance requirements.

If a bureau or furnisher refuses to correct errors after your dispute, file a complaint through the CFPB’s online portal at consumerfinance.gov. The CFPB tracks these complaints and uses them to identify patterns of non-compliance across the industry. Your complaint becomes part of the public record and can support enforcement actions against violating companies. Willful violations can result in triple actual damages or at least $1,000 per violation, plus attorney fees, which means serious violations can justify legal action even if the dollar amount seems small.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, recover damages from credit bureaus and furnishers that violate the FCRA. If you’ve found errors on your report, faced identity theft, or dealt with a company that refuses to correct inaccurate information, contact us for a free evaluation of your situation. We handle credit reporting and identity theft cases on a contingency basis, meaning you pay nothing unless we recover damages for you.