Identity theft reporting SC: How to Report and Recover in SC

Identity theft is growing faster in South Carolina than many residents realize. If your personal information has been compromised, knowing how to report identity theft in SC and take immediate action can mean the difference between a quick recovery and months of financial damage.

We at Hays Cauley, P.C. have helped countless South Carolina residents navigate this process. This guide walks you through reporting requirements, recovery steps, and practical protection strategies.

What Identity Theft Looks Like in South Carolina

Financial Identity Theft Dominates SC Reports

Financial identity theft leads all fraud categories in South Carolina, with criminals opening credit cards, taking out loans, and draining bank accounts in victims’ names. The South Carolina Department of Consumer Affairs tracks security breaches across the state, and the pattern is unmistakable: fraudsters target Social Security numbers, driver’s license information, and checking account details because these credentials provide immediate access to money. Medical identity theft is rising too-scammers use your information to obtain prescription medications or file false insurance claims. Criminal identity theft occurs less frequently but carries serious legal consequences when someone uses your identity to avoid law enforcement. South Carolina Code Section 16-13-510 makes both financial identity fraud and identity fraud felonies with penalties up to 10 years imprisonment, so this isn’t a minor offense in the state’s legal system.

Spot the Red Flags Before Damage Spreads

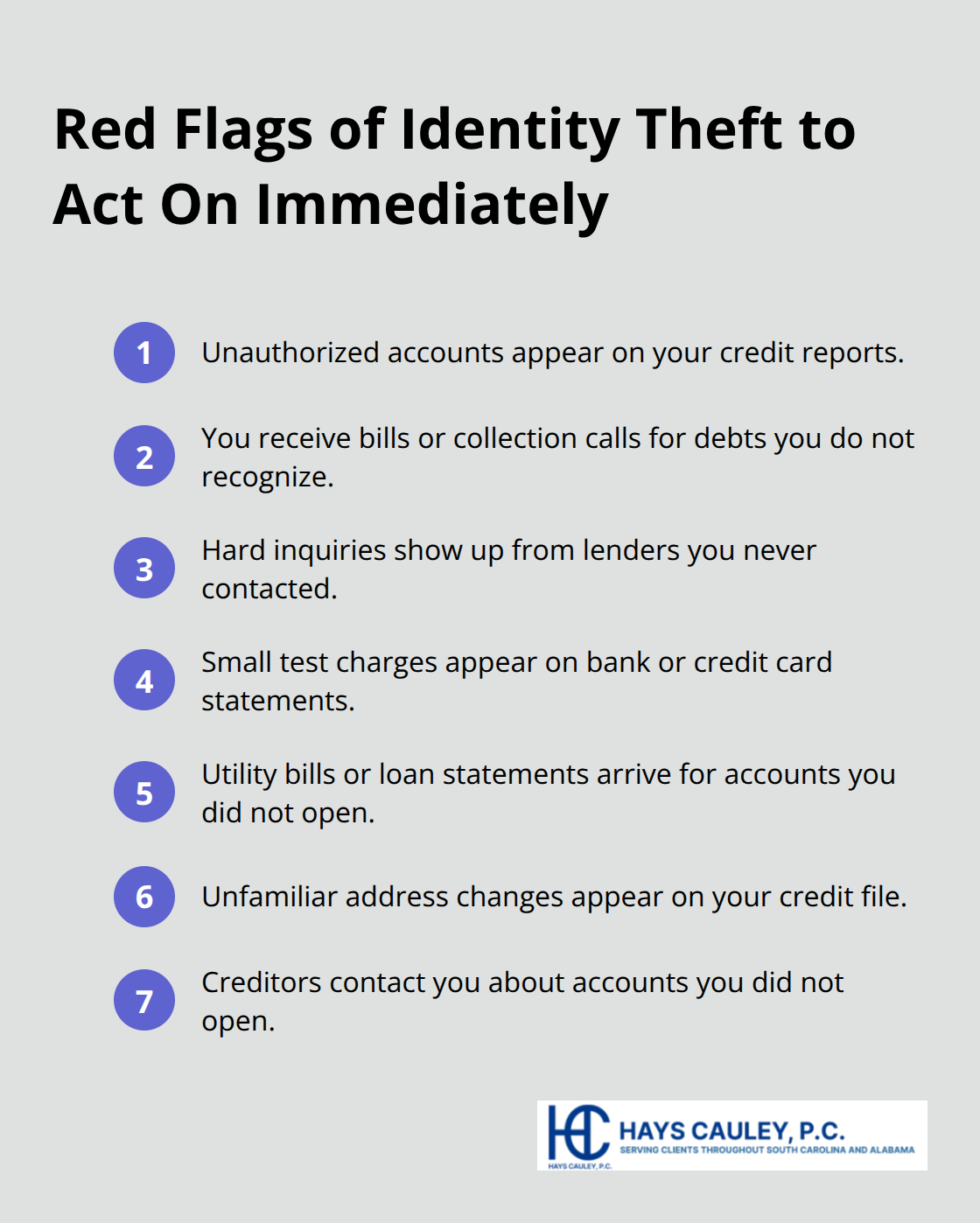

Unauthorized accounts on your credit reports signal trouble immediately. Unexpected bills from creditors you never contacted and collection calls about debts you didn’t create are clear warning signs. The Federal Trade Commission receives millions of identity theft reports annually, and one consistent finding stands out: victims who catch fraud within 30 days limit their losses significantly. Pull your credit reports from all three bureaus at annualcreditreport.com-this service is free and you’re entitled to one report per bureau per year, though you can pull them more frequently if you suspect fraud. Hard inquiries from lenders you never applied to indicate someone applied for credit in your name. Examine your bank and credit card statements monthly for small fraudulent charges; scammers often test stolen card numbers with small purchases before making larger ones. A bill for a utility account you didn’t open or a loan statement you don’t recognize demands immediate action. The SC Department of Consumer Affairs at 1-800-922-1594 guides you through next steps, and filing a report creates an official record that strengthens your credibility with creditors and law enforcement.

Act Within Hours, Not Days

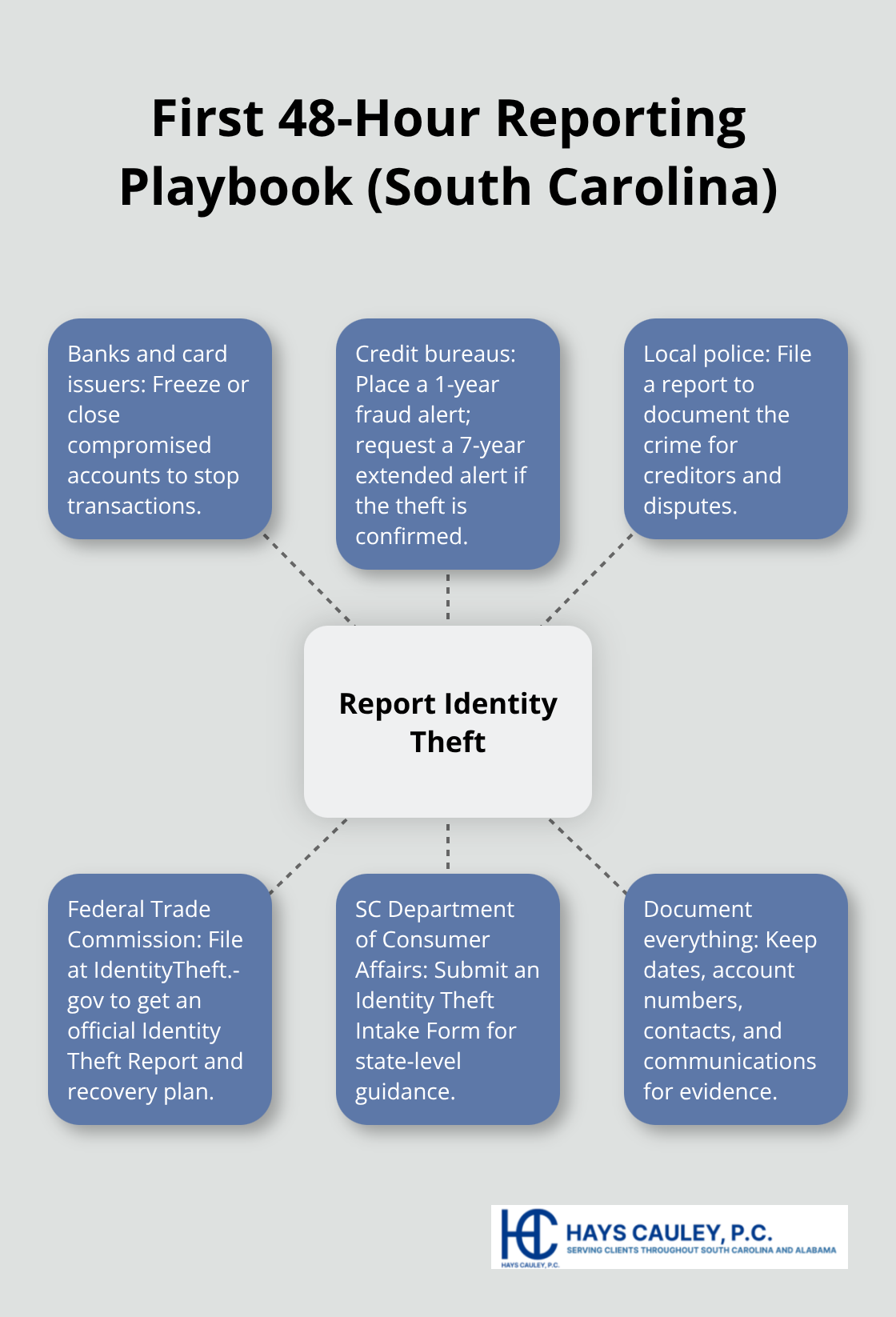

Contact your banks and credit card issuers the moment you suspect identity theft to freeze or close compromised accounts. Place a fraud alert with one of the three credit bureaus-Experian, Equifax, or TransUnion-and they’ll notify the others, which typically stops new account applications for one year. If the theft is confirmed, you can request a seven-year extended fraud alert instead. File a police report with your local South Carolina law enforcement agency; this creates documentation that creditors will want to see when you dispute fraudulent charges. Then file an official identity theft report through the Federal Trade Commission at IdentityTheft.gov, which provides you a personalized recovery plan and an official report you can send to creditors and bureaus. Contact the SC Department of Consumer Affairs to file an Identity Theft Intake Form, which connects you with state-level resources and guidance tailored to your situation. Document everything-dates, account numbers, creditor contact information, and all communications-because you’ll need this evidence to dispute fraudulent accounts and potentially recover losses through restitution. With these reports filed and your accounts secured, you’re ready to move into the formal reporting process that strengthens your position with creditors and law enforcement.

How to Report Identity Theft in South Carolina

File a Police Report Immediately

Contact your local South Carolina law enforcement agency’s non-emergency line and file a report for identity theft. Provide specific details about fraudulent accounts, unauthorized charges, and the dates you discovered the theft. The police report creates an official record that creditors will demand when you dispute fraudulent accounts, and it establishes that you reported the crime promptly rather than ignoring suspicious activity.

Bring documentation of the fraud with you-bank statements showing unauthorized transactions, credit card offers you never requested, collection notices for accounts you didn’t open, and any communications from creditors about accounts in your name. The report number becomes critical; creditors use it to verify your claim and remove fraudulent entries from your accounts. Many South Carolina police departments allow online reporting for identity theft, which saves time if you prefer not to visit in person. Request a copy of the report for your records and keep it accessible as you contact creditors and credit bureaus over the coming weeks.

Report to the Federal Trade Commission

File an official identity theft report with the Federal Trade Commission at IdentityTheft.gov. This report carries weight that a police report alone does not. The FTC report generates a personalized recovery plan customized to your specific situation-whether you’re dealing with credit card fraud, loan accounts, or tax-related identity theft-and provides an official Identity Theft Report that creditors and credit bureaus recognize as authoritative.

The FTC receives millions of identity theft reports annually, and their system integrates with major creditors and bureaus to flag your accounts. This official report strengthens your position far more than verbal claims or informal documentation. Print your Identity Theft Report and keep multiple copies; you’ll send this document to creditors, credit bureaus, and financial institutions throughout your recovery process.

Contact South Carolina’s Consumer Affairs Department

Call the South Carolina Department of Consumer Affairs at 1-800-922-1594 or email IDTheftHelp@scconsumer.gov to file an Identity Theft Intake Form. This step connects you with state resources and allows South Carolina to track patterns in identity theft affecting residents. The SCDCA maintains a database of security breaches dating back to 2015, so they can identify whether your information was compromised in a known breach affecting South Carolina residents or businesses.

The state-level report creates a second official record that complements your police report and FTC filing. State authorities can provide tailored guidance based on the type of identity theft you experienced and connect you with additional resources specific to South Carolina law and protections.

Notify Credit Bureaus and Financial Institutions

Contact all three credit bureaus-Experian, Equifax, and TransUnion-and notify them of the fraudulent accounts on your reports. Request that they remove unauthorized inquiries and accounts. Send written notification rather than calling, as written records provide documentation for disputes. Include copies of your police report and FTC Identity Theft Report with your letters to strengthen your credibility and speed up the removal process.

Contact your banks and credit card issuers immediately with your police report number and FTC report number. Creditors are far more likely to process disputes and remove fraudulent charges when you provide these official reports rather than making claims without documentation. Each creditor will have a specific dispute process; follow their procedures carefully and maintain records of all communications. With these reports filed and creditors notified, you transition from reporting the theft to actively monitoring and disputing the fraudulent accounts that now appear on your credit profile.

Recovery Steps After Identity Theft

Monitor Your Credit Reports Weekly in the First Month

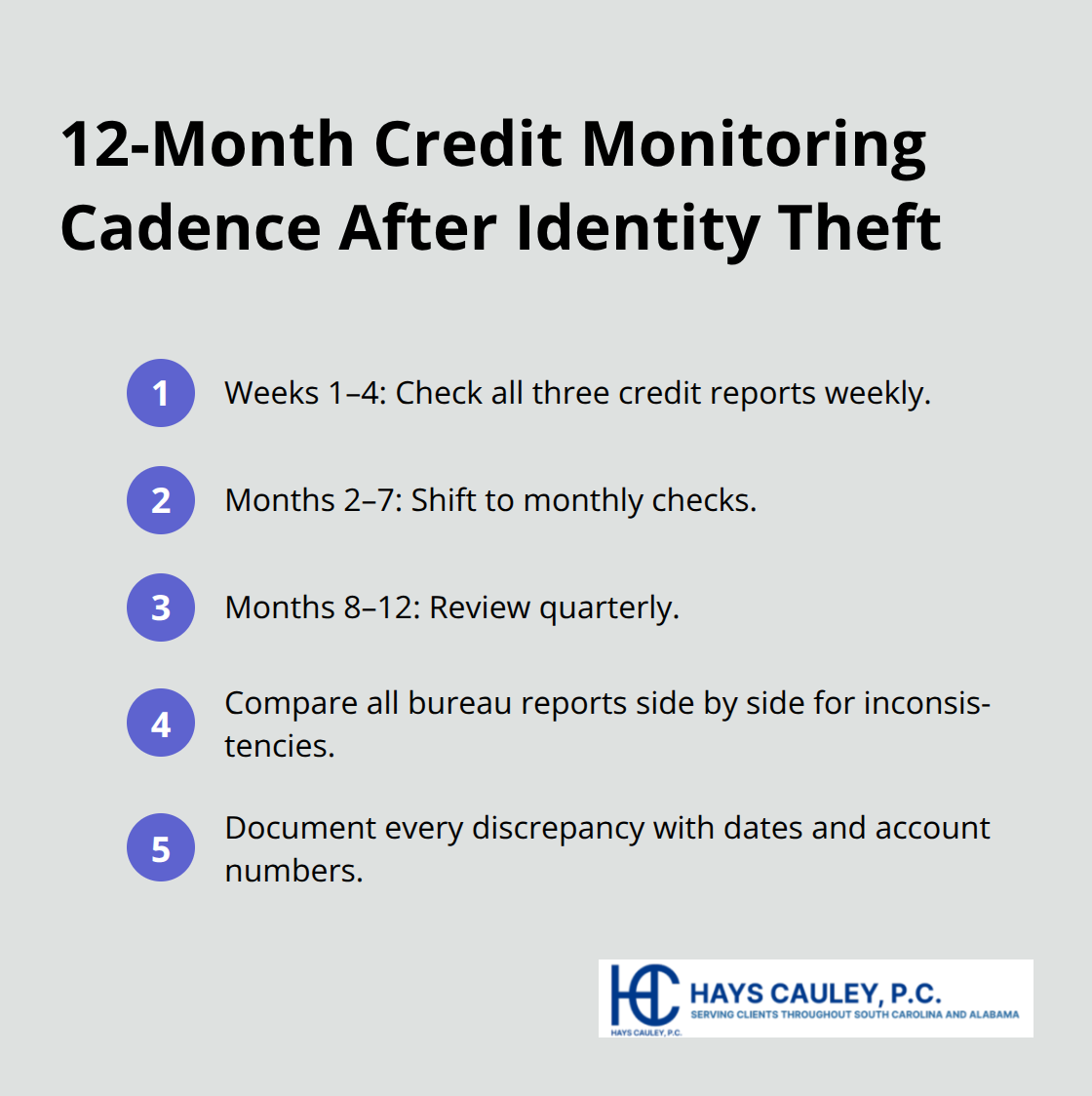

Check your credit reports weekly during the first month after identity theft strikes. Pull reports from annualcreditreport.com, which provides free access to all three bureaus, and compare them side by side to spot discrepancies. Look for accounts you never opened, inquiries from lenders you didn’t contact, and address changes that signal fraudulent activity. The Federal Trade Commission emphasizes that victims who catch new fraudulent accounts within 30 days substantially limit their losses, so this intensive early monitoring directly impacts your financial recovery timeline.

After 30 days, shift to monthly checks for at least six months, then quarterly reviews for a full year. Many fraud victims discover secondary accounts opened weeks or months after the initial theft, so persistence matters more than a single sweep of your reports. Document every fraudulent entry with dates and account numbers because you’ll reference this information repeatedly when disputing charges and communicating with creditors.

Send Written Dispute Letters to Credit Bureaus and Creditors

Dispute fraudulent accounts through written letters sent to credit bureaus and creditors simultaneously. Include your police report number and FTC Identity Theft Report with every communication, as these documents carry legal weight that phone calls never achieve. The Fair Credit Reporting Act requires credit bureaus to investigate disputes within 30 days, and most fraudulent accounts are removed within 45 days when you provide official documentation.

Contact your banks and credit card issuers separately from the credit bureaus, as each entity handles disputes through different channels. For fraudulent charges on accounts you actually own, dispute them directly with your card issuer rather than the credit bureau; card companies typically reverse unauthorized charges within 10 business days if you report them promptly.

Track Every Dispute and Follow Up Systematically

Create a spreadsheet tracking every fraudulent account, the date you disputed it, the dispute reference number, and the resolution date. This organized approach prevents you from missing follow-ups and provides evidence if disputes stall. Hays Cauley, P.C., a consumer protection law firm dedicated to helping consumers with credit reporting and identity theft issues, works with South Carolina residents navigating these disputes and can assist when creditor disputes become complex.

Rebuild Your Credit Score with Secured Cards

Secured credit cards with deposits as low as $300 to $500 allow you to establish fresh credit history within six months. This strategy works because card issuers report your payment activity to credit bureaus, and on-time payments gradually restore your credit score. Serving South Carolina, including Greenville, Columbia and Charleston, residents can access these products through most major banks and credit unions to accelerate their financial recovery after identity theft.

Final Thoughts

Identity theft reporting in SC demands immediate action, but your recovery extends far beyond filing reports. The steps you take in the weeks and months following the theft determine whether you regain control of your finances quickly or face prolonged damage to your credit and accounts. Most victims resolve their cases within three to six months, though some fraudulent accounts linger longer-persistence matters more than speed.

South Carolina residents have access to strong state-level resources through the SC Department of Consumer Affairs, which maintains breach records dating back to 2015 and provides tailored guidance for victims. The Federal Trade Commission’s IdentityTheft.gov remains your most comprehensive tool, offering personalized recovery plans and official reports that creditors recognize. annualcreditreport.com gives you free access to all three credit bureaus, and monitoring those reports weekly during your first month catches secondary fraud before it spreads.

Document everything, follow up on every dispute, and don’t assume accounts are removed until you see them gone from your credit reports. If disputes stall or creditors resist removing fraudulent entries, Hays Cauley, P.C. helps South Carolina residents navigate complex credit reporting and identity theft issues when the process becomes overwhelming. Treat prevention as seriously as recovery by monitoring your accounts monthly, using strong passwords with two-factor authentication, and limiting your exposure to future fraud.