Identity theft resolution SC: Steps to Protect and Restore Your Identity

Identity theft can happen to anyone, and the consequences are serious. At Hays Cauley, P.C., we help South Carolina residents navigate identity theft resolution SC by understanding their rights and taking concrete action.

This guide walks you through what to do if you’ve been victimized, how to protect yourself legally, and how to rebuild your financial life.

How Identity Theft Happens and Warning Signs

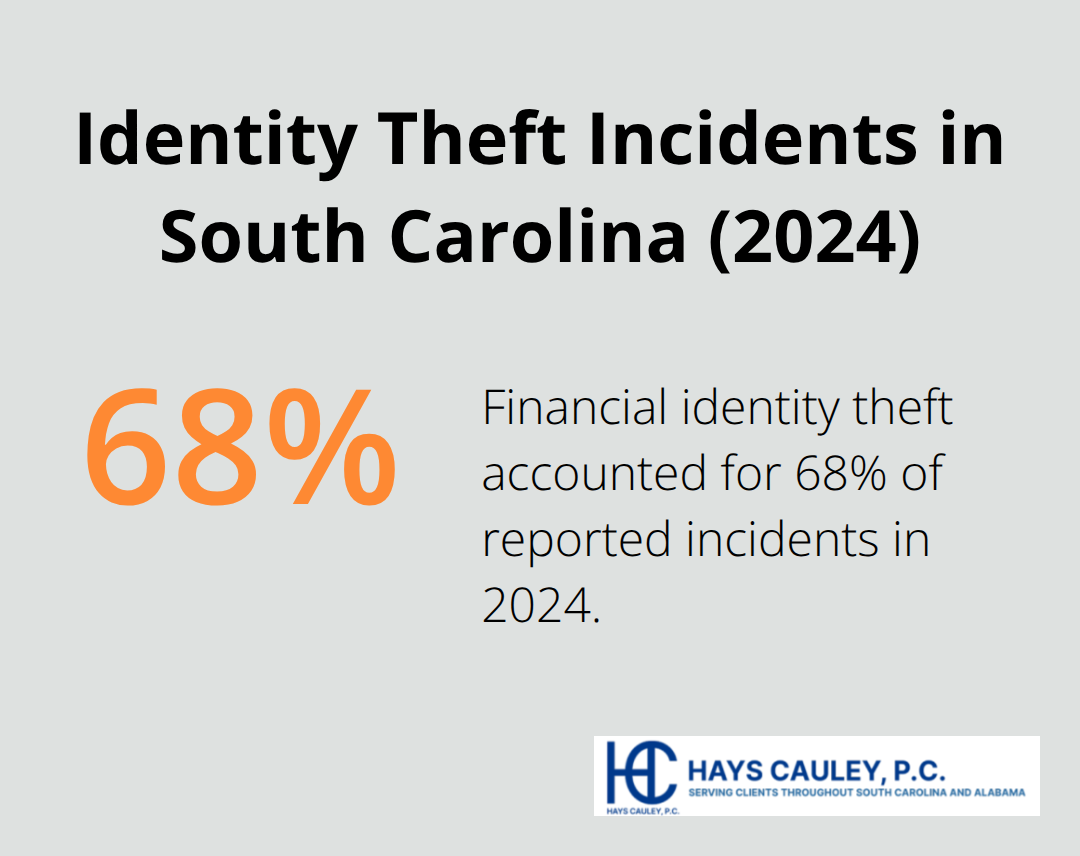

Identity theft in South Carolina is widespread and growing. The SC Hospital Association reported over 15,000 identity theft cases in 2024, with financial identity theft accounting for 68% of incidents. Criminals steal your personal identifying information through phishing emails, data breaches at retailers or healthcare providers, unsecured public Wi-Fi networks, mail theft, and phone calls where they impersonate legitimate companies.

They target Social Security numbers, driver’s license numbers, checking and savings account numbers, credit card numbers, dates of birth, and addresses-anything that gives them access to your financial resources. Once they have this information, they open fraudulent accounts, drain bank balances, or take out loans in your name. The average victim in South Carolina faced approximately $3,500 in out-of-pocket losses in 2024, but the real damage extends far beyond immediate costs. Fraudulent accounts generate hard inquiries and missed payments that can drop a healthy credit score of 750 to 600 or lower within weeks, and these accounts remain on your credit report for seven years unless you actively dispute and remove them.

Red flags that signal compromise

Watch for warning signs that indicate your identity has been compromised. Unexpected credit card or bank statements, denial of credit applications you know you qualify for, calls from creditors about accounts you never opened, and unfamiliar inquiries on your credit report are immediate red flags. The IRS Identity Theft guide identifies additional warning signs specific to taxes: a rejected tax return, W-2s or 1099s from employers you didn’t work for, unexpected unemployment notices, and password-reset alerts on accounts you didn’t change. If you spot any of these signs, act immediately.

Your first 48 hours matter most

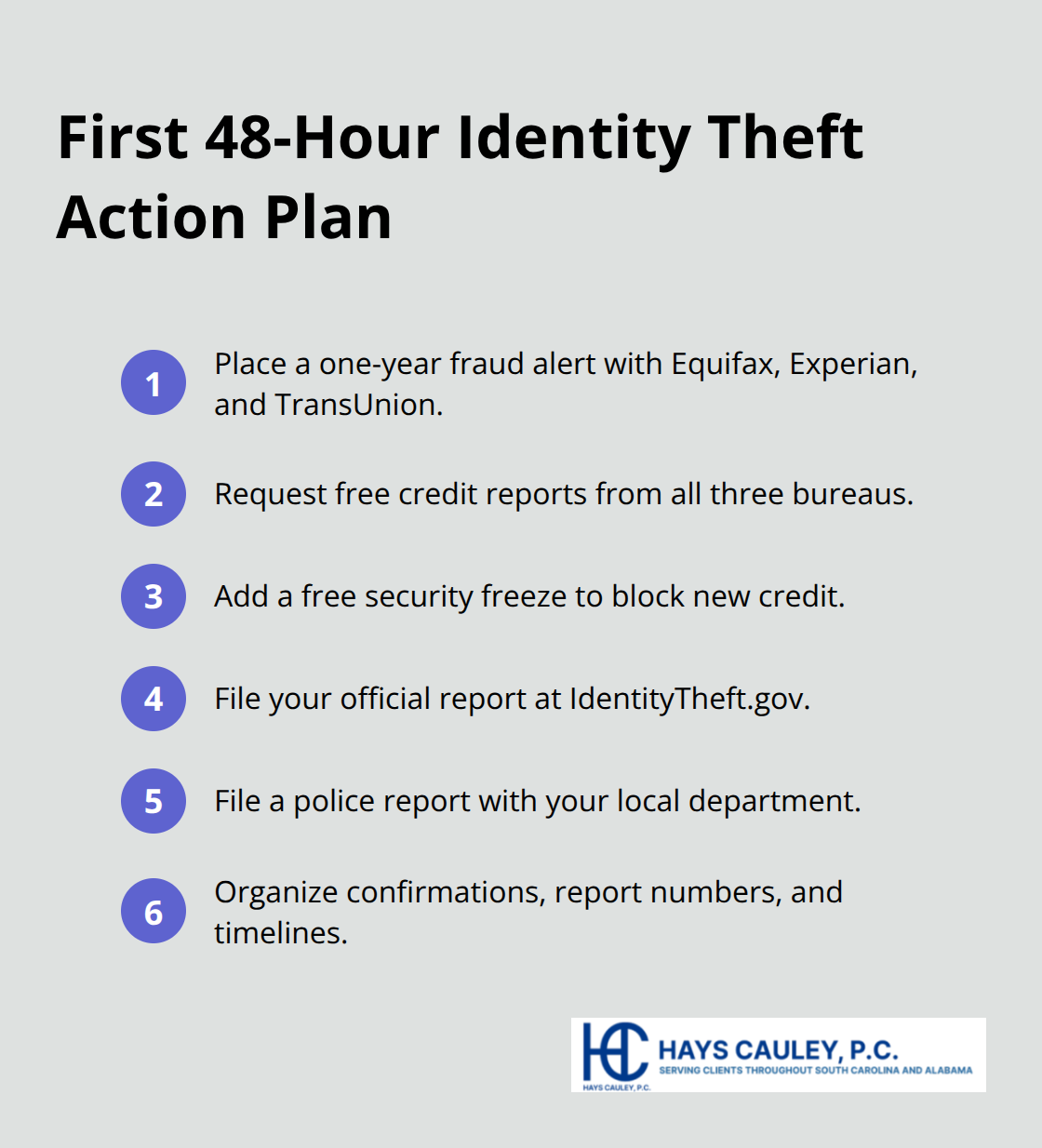

In the first 48 hours, place a fraud alert with Equifax at 800-685-1111, Experian at 888-397-3742, and TransUnion at 888-909-8872. The alert lasts one year and notifies other bureaus automatically, which prevents criminals from opening new accounts in your name. Then request free copies of your credit reports from all three bureaus to identify unauthorized accounts. Request a security freeze on your credit file, which is free in South Carolina and blocks new credit applications entirely. File an official identity theft report at IdentityTheft.gov to receive a personalized recovery plan and an official document you’ll need for creditors and law enforcement. Finally, file a police report with your local department to document the crime and support potential restitution.

Why speed determines your recovery timeline

Under South Carolina law, financial identity fraud is a felony with penalties up to 10 years in prison, and victims can receive court-ordered restitution from convicted perpetrators. Speed matters significantly-victims who use professional help typically resolve cases in about 30 days, while those working alone average 180 days. Every day you delay allows more fraudulent charges to accumulate and more accounts to age on your credit report. The sooner you take action, the faster your financial life stabilizes. Your next step involves understanding the legal protections available to you and how to use them effectively.

What Laws Protect You and How to Use Them

South Carolina law treats identity theft with serious consequences for perpetrators. Under SC Code §16-13-510, financial identity fraud qualifies as a felony carrying penalties up to 10 years in prison, and courts can order restitution to victims. This means if your case reaches prosecution, you have a legal pathway to recover losses directly from the person who harmed you. Federal law provides equally strong protections through the Fair Credit Reporting Act and the Identity Theft Enforcement and Restitution Act, which grant you the right to dispute fraudulent accounts and demand removal from your credit report. The Federal Trade Commission enforces these rights and maintains IdentityTheft.gov as your official resource for filing reports and receiving a personalized recovery plan. When you file at IdentityTheft.gov, you receive a document that creditors and credit bureaus must recognize as proof of identity theft, which accelerates removal of fraudulent items from your reports.

Your strongest defenses: fraud alerts and credit freezes

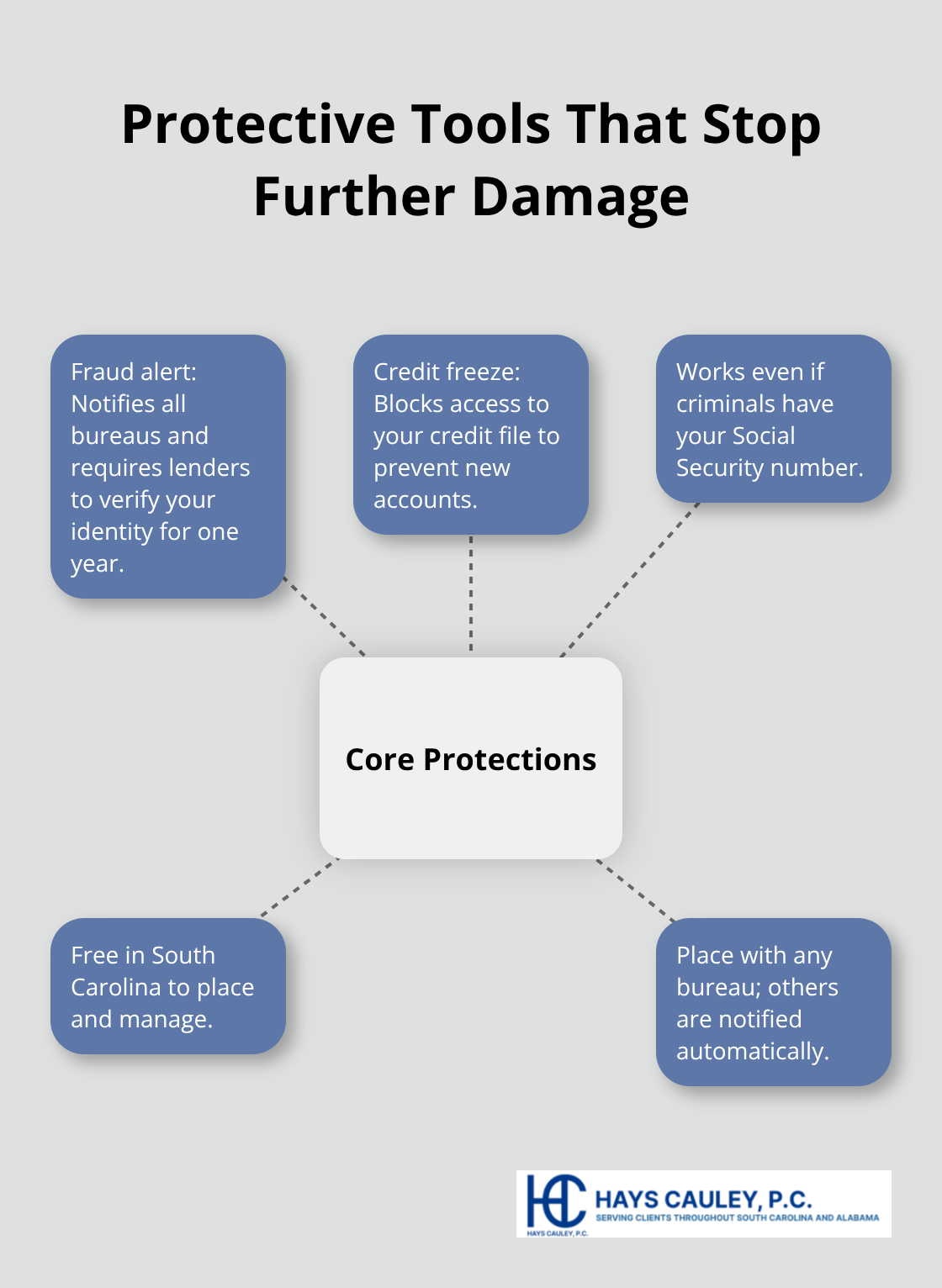

Your immediate action should focus on the fraud alert and credit freeze because they are your strongest defenses against further damage. A fraud alert placed with any of the three credit bureaus-Equifax, Experian, or TransUnion-automatically notifies the others, and lenders must verify your identity before extending new credit for one year. A security freeze goes further by blocking access to your credit file entirely, preventing criminals from opening accounts even if they have your Social Security number. In South Carolina, both protections cost nothing.

Filing reports that creditors must recognize

After placing these protections, file your official identity theft report with the FTC at IdentityTheft.gov, then file a police report with your local law enforcement agency. The police report number becomes critical because credit bureaus and creditors require it when you dispute fraudulent accounts. When you send dispute letters to the three bureaus for each fraudulent item, include your police report number and your IdentityTheft.gov report confirmation. Credit bureaus must investigate within 30 days, and if they cannot verify the debt belongs to you, they must remove it. This is not optional-it is required under federal law.

What happens if bureaus ignore your disputes

If a bureau fails to remove a verified fraudulent item or ignores your dispute, South Carolina law under SC Code 37-20-170 allows you to pursue damages. Document everything: keep copies of all letters sent, police report numbers, bureau responses, and correspondence with creditors. This documentation becomes your evidence if you need to escalate to legal action or pursue restitution from a convicted perpetrator. The strength of your case depends on how thoroughly you track each step of your recovery process, which means your next focus should turn to the specific mechanics of disputing fraudulent accounts and rebuilding your credit score.

Restoring Your Credit and Financial Records

Take action to dispute fraudulent accounts

Disputing fraudulent accounts requires direct action-items remain on your report indefinitely without your intervention. Pull all three credit reports from annualcreditreport.com and document every fraudulent item: account numbers, balances, opening dates, and creditor names. Credit bureaus must investigate disputes within 30 days under federal law, but they only investigate what you formally dispute. Send certified letters with return receipt to Equifax, Experian, and TransUnion for each fraudulent account. Include your police report number, your IdentityTheft.gov confirmation, specific account details, and a statement that you did not authorize the account. The FTC provides fillable dispute letters on IdentityTheft.gov that creditors recognize immediately.

Do not stop after contacting the bureaus. Contact the creditor directly and request they close the fraudulent account with a written statement confirming it resulted from identity theft. This dual approach accelerates removal significantly. Javelin Strategy & Research found that victims using professional assistance resolve cases in approximately 30 days versus 180 days without help, largely because they pursue both bureau and creditor disputes simultaneously. If a bureau cannot verify the debt within 30 days, federal law requires removal. Expect 4 to 6 weeks for bureaus to respond and remove items from your report.

Understand how your credit score recovers

Your credit score will drop immediately when fraudulent accounts appear, but recovery starts the moment you remove them. A healthy score of 750 can plummet to 600 or below within weeks due to hard inquiries and missed payments on accounts you never opened. The damage compounds because fraudulent accounts remain reportable for seven years unless actively disputed. However, scores typically recover within 3 to 6 months once fraudulent items are removed, assuming you maintain on-time payments on legitimate accounts.

Long-term consequences of delayed action are severe: denials for mortgages, auto loans, and credit cards, plus higher interest rates that add tens of thousands in costs over a 30-year loan. The sooner you remove fraudulent items, the sooner your score stabilizes and lenders view you as a lower-risk borrower.

Monitor your reports continuously

Stagger your free annual credit reports every four months by pulling one bureau at a time rather than all three simultaneously. This approach provides continuous monitoring throughout the year and catches new fraud before it compounds. If fraudulent items reappear after removal-which happens due to creditor error or reinstatement-dispute them again immediately. Persistent monitoring combined with swift re-disputes prevents compounding damage as items can be reinstated without your knowledge.

Final Thoughts

Identity theft resolution SC requires immediate action, but you don’t have to navigate this process alone. Place fraud alerts with all three credit bureaus within the first 48 hours, request your free credit reports to identify fraudulent accounts, and file your official identity theft report at IdentityTheft.gov. These steps take a few hours but prevent weeks of additional damage. When you contact your local police department to document the crime, you create the foundation for potential restitution under South Carolina law.

Send certified dispute letters to each credit bureau and contact creditors directly to request account closure with written confirmation of the fraud. Monitor your credit reports every four months using staggered annual requests, and re-dispute any items that reappear. If you face more than five fraudulent accounts, if bureaus refuse to remove items after 30 days, or if you’re dealing with employment identity theft or tax-related fraud, professional guidance from Hays Cauley, P.C. becomes valuable for enforcing your rights under SC Code §16-13-510 and the Fair Credit Reporting Act.

South Carolina residents have access to free resources through the SC Department of Consumer Affairs Identity Theft Unit at 800-922-1594 or IDTheftHelp@scconsumer.gov, and the FTC’s IdentityTheft.gov provides personalized recovery plans. Most victims resolve cases within three to six months when they follow these steps consistently and pursue professional assistance when complexity demands it. Your recovery timeline depends on how quickly you act, but established support systems exist specifically for you.