Identity Theft Resolution SC: How Victims Reclaim Their Credit and Peace of Mind

Identity theft can devastate your financial life within days. Fraudulent accounts appear on your credit report, your score plummets, and lenders suddenly deny you credit you’ve earned.

We at Hays Cauley, P.C. help South Carolina residents navigate identity theft resolution SC by walking through the exact steps to reclaim your credit and financial stability. This guide shows you what to do immediately and how to rebuild your financial standing.

How Identity Theft Damages Your Credit Report

Identity theft doesn’t just drain your bank account-it systematically destroys your credit file. When a thief opens fraudulent accounts in your name, each new account generates a hard inquiry on your credit report, and these inquiries lower your score by a few points each. More damaging are the fraudulent accounts themselves. Every missed payment on accounts you never opened tanks your credit score further. In South Carolina, over 15,000 identity theft cases were reported in 2024 according to the SC Hospital Association, with financial identity theft making up 68% of incidents. These fraudulent accounts stay on your credit report for seven years unless you actively dispute and remove them, meaning years of damage to your borrowing power. The average identity theft victim in South Carolina faced out-of-pocket losses around $3,500 in 2024, but the credit damage often costs far more in the long run through higher interest rates and denied loan applications.

How Your Credit Score Gets Damaged

Your credit score drops the moment fraudulent activity hits your report. Hard inquiries from new account applications knock points off immediately. Late payments on accounts you never opened cause steeper declines-missed payments damage your score far more than inquiries. If the thief maxes out credit cards in your name, your credit utilization ratio skyrockets, which is one of the most heavily weighted factors in credit scoring. A victim with a clean 750 credit score can see it plummet to 600 or lower within weeks of identity theft. This isn’t theoretical: without professional help, identity theft recovery takes roughly 180 days according to Javelin Strategy & Research, but many victims wait months just to discover the fraud exists.

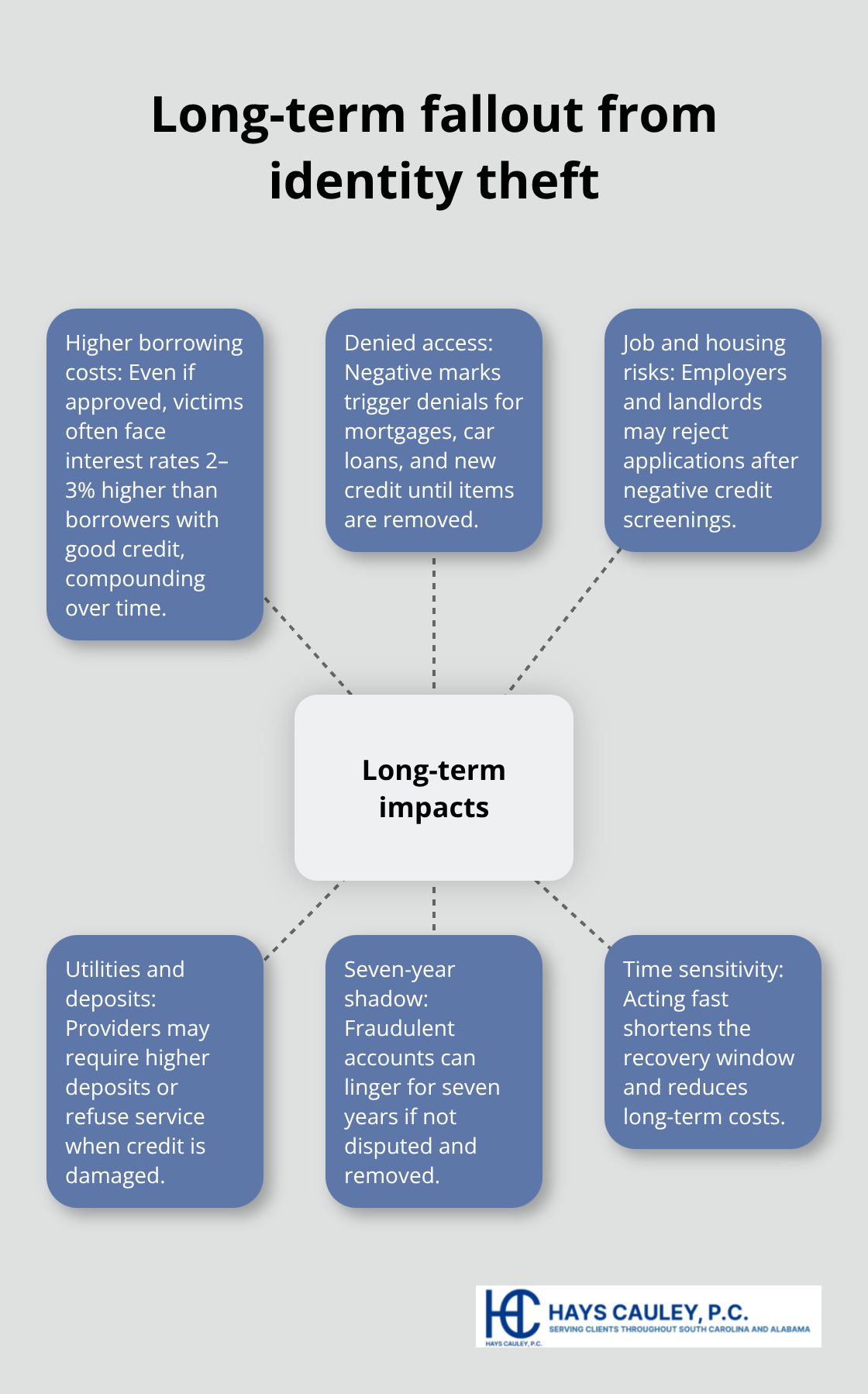

Long-Term Financial Consequences

The real cost emerges when you try to rebuild your life. Lenders see negative marks and deny you mortgages, car loans, and credit cards. If they do approve you, you’ll pay higher interest rates-sometimes 2-3% more than borrowers with good credit. That difference costs tens of thousands of dollars over a 30-year mortgage. Employers and landlords pull credit reports too, and negative marks can cost you job opportunities and rental approvals. Utility companies check credit before connecting service. The fraudulent accounts remain on your report for seven years, creating a persistent barrier to financial opportunity.

This is why acting immediately matters: the faster you dispute fraudulent items and remove them, the sooner your credit begins recovering and the fewer years you spend paying penalties for someone else’s crimes.

Why Speed Matters in Recovery

The timeline of your recovery determines how much financial damage you ultimately suffer. With professional assistance and case management, many victims resolve identity theft cases in about 30 days according to Javelin Strategy & Research-a dramatic difference from the 180-day average without help. Each month you delay, fraudulent accounts age on your report and additional unauthorized charges accumulate. The sooner you contact credit bureaus, file reports, and dispute false information, the sooner you stop the bleeding and start rebuilding. Your next step involves taking immediate action to alert the right agencies and protect yourself from further damage.

What to Do Right Now When Identity Theft Strikes

The first 48 hours after discovering identity theft determine whether you stop the damage or let it spiral. Your immediate goal is to alert the three credit bureaus and freeze your credit file before the thief opens more accounts.

Place a Fraud Alert Immediately

Contact Equifax at 800-685-1111, Experian at 888-397-3742, and TransUnion at 888-909-8872 to place a fraud alert, which lasts one year and forces creditors to verify your identity before opening new credit. When you place the alert with any one bureau, it automatically notifies the other two, so you only need to call once. Request a free copy of your credit report from each bureau as part of the fraud alert process-this is separate from your annual free reports and lets you scan for unauthorized accounts immediately.

Freeze Your Credit File

After placing your fraud alert, contact the same three bureaus again to request a security freeze, which costs nothing in South Carolina and blocks creditors from accessing your credit file entirely. Unlike fraud alerts, freezes prevent new accounts from being opened in your name because lenders cannot see your credit report to approve applications. You will receive a PIN or password within ten business days for each freeze; store these PINs somewhere safe because you’ll need them to unfreeze your credit temporarily when you legitimately apply for loans or credit.

File Official Reports

While the fraud alert and freeze are processing, file a report with the Federal Trade Commission at IdentityTheft.gov, which generates a personalized recovery plan tailored to your situation and creates an official identity theft report that creditors and credit bureaus must honor. The FTC report is free and takes about 10 minutes to complete. Then contact your local police department and file a police report, which you’ll need to prove identity theft when disputing fraudulent accounts and pursuing restitution under South Carolina law. Many victims skip this step, but without a police report, credit bureaus and creditors will question whether fraud actually occurred.

Document Every Fraudulent Item

Pull your three credit reports immediately using the free copies provided by your fraud alert and look for accounts you do not recognize, inquiries from creditors you never contacted, and address changes you did not authorize. Write down every fraudulent item with the account number, creditor name, and the amount owed. This list becomes your roadmap for the next phase of recovery. Do not delay this process hoping the problem resolves itself-each day you wait allows the thief to rack up more charges and age fraudulent accounts further into your credit history. With your documentation complete and your credit file protected, you now move into the active work of removing fraudulent items from your report and restoring your financial standing.

Recovering Your Credit and Financial Standing

Send Formal Dispute Letters to Credit Bureaus

Disputing fraudulent accounts is the core work of identity theft recovery, and the process is far more straightforward than most victims assume. Under federal law, credit bureaus must investigate your dispute within 30 days and remove any items they cannot verify as accurate. Send a dispute letter to each of the three credit bureaus for every fraudulent account on your report. Include your police report number, a copy of your identity theft report from IdentityTheft.gov, and a clear description of each fraudulent item with account numbers. Written disputes create a paper trail and carry legal weight that phone calls do not. Mail your letters certified with return receipt requested so you have proof the bureaus received them. South Carolina law requires credit bureaus to respond within 30 days, and if they cannot verify the debt as legitimate, they must remove it from your report. If a bureau fails to remove fraudulent information within 10 days after a court judgment in your favor, damages increase under South Carolina Code Section 37-20-170, which means bureaus take removal seriously when you follow the formal process.

Contact Creditors Directly for Faster Removal

Creditors themselves often remove fraudulent charges faster than the dispute process because they want to avoid fraud liability. Contact each creditor directly and provide your police report and identity theft report, then request they close the fraudulent account and issue a written statement that the account resulted from identity theft. Many creditors will remove the account from your credit report voluntarily rather than litigate. This direct approach can shorten your recovery timeline significantly compared to waiting for the formal bureau dispute process to complete.

Monitor Your Credit Reports Every Four Months

Once disputed items are removed or accounts are closed, monitor all three credit reports every four months. Stagger your free annual reports from Equifax, Experian, and TransUnion through annualcreditreport.com pull from one bureau every four months so you catch any new fraud immediately. If fraudulent items reappear after removal, file another dispute immediately; bureaus sometimes reinstate deleted items through creditor error, and persistent monitoring catches these problems before they damage your score again. This active management phase typically lasts three to six months, after which most victims see their credit scores begin climbing as fraudulent accounts age off their reports and legitimate payment history accumulates.

Final Thoughts

Identity theft resolution in South Carolina requires immediate action, but recovery is absolutely possible when you follow the steps outlined in this guide. The first 48 hours determine whether you contain the damage or watch it spiral, so place your fraud alert and security freeze before doing anything else. File your reports with the FTC and local police, then systematically dispute every fraudulent item on your credit reports. Most victims see significant improvement within three to six months of consistent monitoring and disputing.

South Carolina provides strong legal protections for identity theft victims through free security freezes, mandatory 30-day investigations by credit bureaus, and restitution rights under state law. The SC Department of Consumer Affairs offers free resources, and the FTC’s IdentityTheft.gov platform provides personalized recovery plans at no cost. You also have the right to block fraudulent information from your credit report entirely once you file an official identity theft report, which stops creditors from pursuing those debts.

We at Hays Cauley, P.C. help South Carolina residents reclaim their credit and financial stability through identity theft resolution SC. Our team understands the frustration of fraudulent accounts, denied credit applications, and the months of work required to restore your financial standing, and we work with you to dispute fraudulent items, communicate with creditors and credit bureaus, and pursue restitution under South Carolina law. Contact Hays Cauley, P.C. to discuss your situation and learn how we can accelerate your recovery. Serving South Carolina, including Greenville, Columbia and Charleston.