Identity Theft Case Help: How to Get Expert Support Fast

Identity theft strikes fast, and the damage spreads faster. Criminals open accounts in your name, rack up charges, and leave you fighting to reclaim your financial life.

We at Hays Cauley, P.C. help victims get identity theft case help when they need it most. This guide walks you through what happens after theft, the immediate steps that matter, and how legal support protects your rights and recovery.

How Criminals Steal Your Identity and What It Costs

Criminals don’t need to break into your home to steal your identity. Data breaches expose millions of people every year, and thieves use that stolen information to open credit accounts, file fraudulent tax returns, and drain bank accounts. According to the Identity Theft Resource Center, recent breach alerts in January 2026 show compromises across healthcare, financial services, and technology sectors, meaning your information could be at risk from any company you do business with. The Federal Trade Commission received over 2.6 million identity theft reports in 2023, with the average victim spending 40 hours or more trying to resolve the damage.

How Thieves Access Your Information

Criminals use multiple methods to steal personal data. Phishing emails trick you into clicking malicious links or attachments. Fake websites mimic legitimate companies and capture login credentials when you enter them. Social engineering manipulates you into revealing sensitive information through phone calls or messages. If you receive a W-2 from an employer you never worked for or see unemployment benefits you didn’t apply for, someone is already using your identity.

Data breaches (which happen constantly across industries) hand thieves ready-made lists of names, Social Security numbers, and financial details without any effort on their part.

Immediate Financial Damage

Identity theft victims face sudden and severe financial consequences. Fraudulent charges appear on credit cards within days. Unauthorized loans get opened in your name, and your credit score plummets, making it harder to secure legitimate loans or mortgages for years. The IRS reports that tax identity theft happens when criminals file returns using your Social Security number to claim refunds. You’ll learn about this when your actual return gets rejected or you receive a notice about a duplicate return.

Long-Term Health and Financial Impact

Medical identity theft creates a different nightmare. Criminals use your insurance to receive treatment, and their medical records get mixed with yours, affecting future coverage and treatment decisions. The 2025 ITRC Business Impact Report shows that costs from cybercrimes are passed to consumers, meaning you’ll pay higher premiums and fees as companies absorb breach costs. Beyond money, victims report significant emotional stress, anxiety about their financial future, and frustration navigating the recovery process alone.

The financial and emotional toll of identity theft makes immediate action essential. Understanding what happened to you is the first step toward recovery, and knowing your legal rights becomes critical as you work to restore your identity and finances.

What to Do Right Now After Identity Theft: Serving South Carolina, including Greenville, Columbia and Charleston

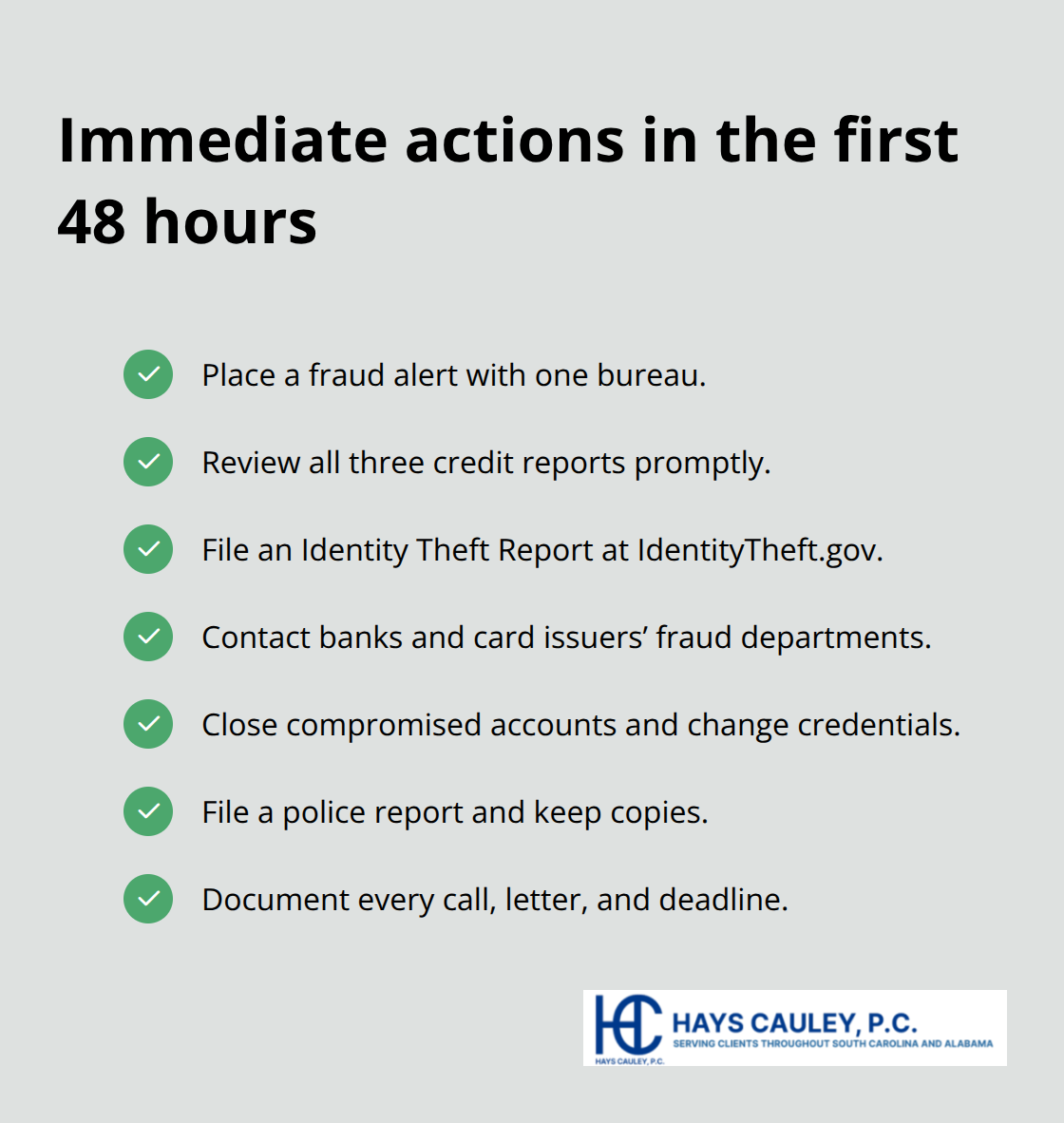

Speed matters more than perfection when you respond to identity theft. The first 24 to 48 hours determine whether you can stop additional damage or whether thieves continue opening accounts in your name. Act immediately to protect yourself.

Place a Fraud Alert on Your Credit File

Contact the three major credit bureaus-Equifax, Experian, and TransUnion-to place a fraud alert on your credit file. You only need to call one bureau, and that bureau will notify the other two automatically. A fraud alert tells creditors to verify your identity before opening new accounts, which stops most criminals in their tracks.

After placing the alert, you receive one free credit report from each bureau, and you should review all three carefully within days. Look for unfamiliar inquiries, accounts you didn’t open, and debts you can’t explain. Monitoring accounts during the first year after identity theft is critical because that’s when most fraudulent activity occurs. If you find fraudulent information on your reports, request its removal immediately and document everything in writing with certified mail and return receipt.

File an Official Report with the Federal Trade Commission

File an official report through IdentityTheft.gov to generate an Identity Theft Report that creditors must accept to stop reporting fraudulent debts and to close fraudulent accounts. This report carries legal weight that a simple police report doesn’t always provide. The FTC enters your information into the Identity Theft Data Clearinghouse to assist investigations and help law enforcement track patterns.

Contact Your Banks and Credit Card Companies

Call your banks and credit card companies directly to report fraud on existing accounts-not through email or the company’s website, but through the fraud department phone number on your statement. Ask the fraud department for their dispute forms and request written confirmation that disputed accounts are closed and fraudulent debts are discharged. Close any accounts you believe have been compromised, even if you’re not certain, and when opening new accounts afterward, use unique PINs and passwords that avoid easily accessible information like your maiden name, birthdate, or sequential numbers.

File a Police Report and Document Everything

File a police report and request that an Identity Theft Complaint form be attached to it, then provide a copy of that police report to creditors to accelerate dispute resolution. Keep detailed logs of every conversation with authorities and financial institutions, including dates, names, phone numbers, and time spent, because this documentation supports potential restitution claims later. Confirm every conversation in writing and send correspondence by certified mail with return receipt; maintain copies of all letters and documents.

These immediate steps stop the bleeding and create an official record of what happened to you. The next phase involves understanding how legal protections work in your favor and what rights you have as you move forward with recovery.

How Legal Protection Works in Your Favor

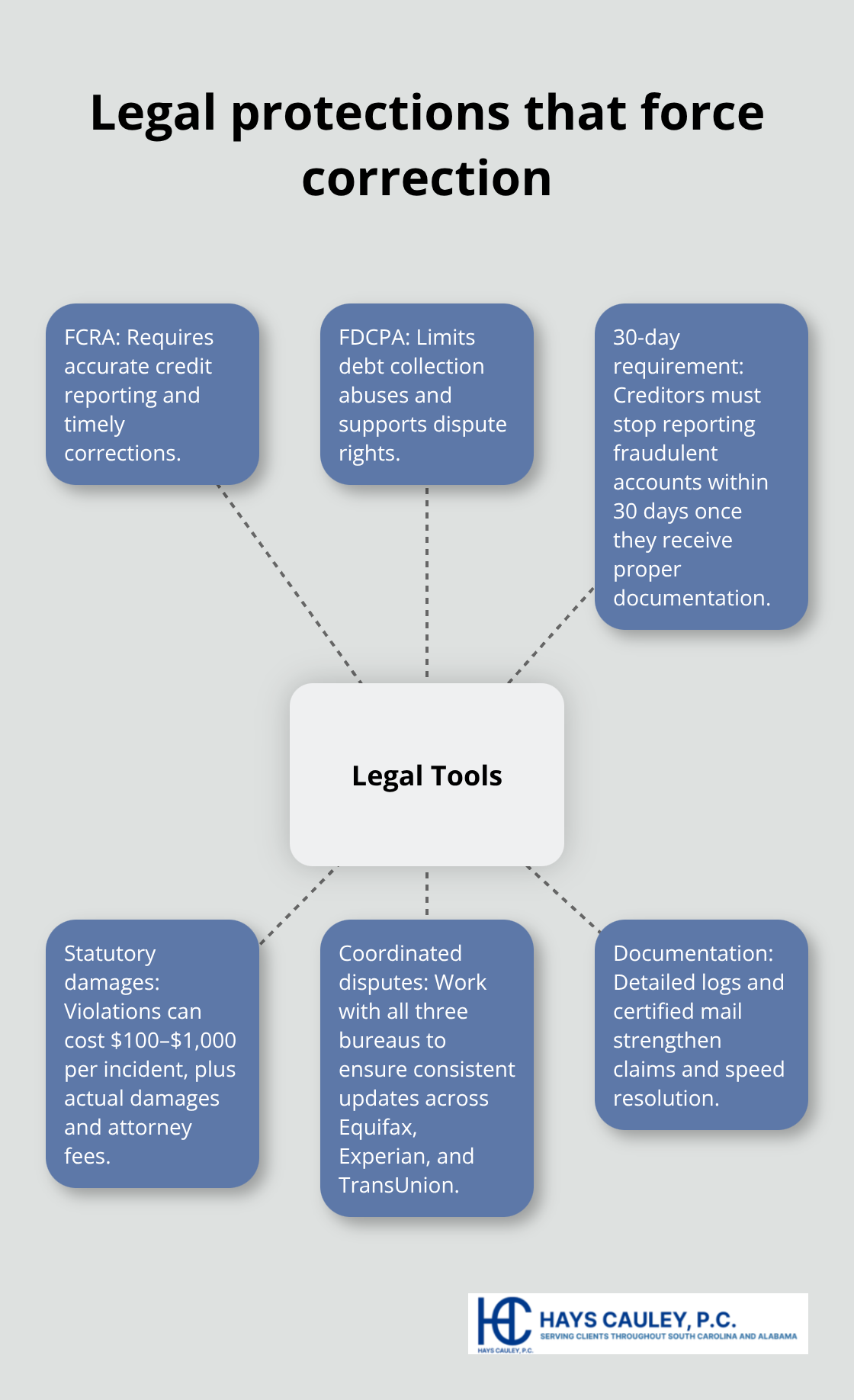

Creditors Ignore Your Disputes Without Legal Backing

Creditors drag their feet when you report fraud on your own. They refuse to acknowledge your Identity Theft Report and continue reporting false debts to credit bureaus. This is where legal protection becomes your strongest tool. The Fair Credit Reporting Act and Fair Debt Collection Practices Act give you legal weapons that most victims don’t know how to use. Creditors must stop reporting fraudulent accounts within 30 days of receiving proper documentation, and they must remove false information from your credit file. If they ignore this requirement, they face statutory damages of $100 to $1,000 per violation, plus your actual damages and attorney fees.

This financial incentive makes creditors take your dispute seriously when a law firm sends the letter instead of you sending it yourself.

Credit Score Damage Requires Coordinated Action

Your credit score damage is real and measurable-victims report score drops of 100 points or more after identity theft-and restoring that score requires forcing creditors and credit bureaus to correct their records. A consumer protection law firm coordinates with all three credit bureaus simultaneously, ensuring they remove fraudulent accounts and update your file consistently across Equifax, Experian, and TransUnion. This coordination prevents the frustrating situation where one bureau removes fraudulent information while another two continue reporting it.

Different Types of Identity Theft Require Different Recovery Steps

Tax identity theft requires separate action through the IRS, including obtaining an Identity Protection PIN to prevent future fraudulent returns and filing Form 14039 or using the Identity Theft Verification Service depending on your situation. The IRS reports that victims of tax identity theft should call 800-908-4490 to verify their tax account status and confirm no duplicate returns exist. Medical identity theft demands contacting your insurance provider and correcting your medical records to prevent future treatment denials. Each type of identity theft follows different rules, different timelines, and different recovery steps.

Documentation Accelerates Resolution and Restitution

Navigating these processes alone means missing deadlines, filing incorrect forms, and watching recovery drag on for months or years. Documentation matters enormously-the Identity Theft Resource Center emphasizes that detailed logs of conversations with authorities, financial institutions, and creditors support restitution claims and accelerate resolution. A law firm maintains this documentation throughout your case and uses it to demand restitution from creditors who violated your rights. You also need to dispute fraudulent charges with your banks and credit card companies, file complaints with the Consumer Financial Protection Bureau if creditors refuse to cooperate, and potentially pursue legal action for damages if they violate the law.

Moving Forward with Confidence After Identity Theft

Identity theft recovery demands coordination with creditors, credit bureaus, and government agencies to restore your financial life. The Fair Credit Reporting Act and Fair Debt Collection Practices Act protect you by requiring creditors to verify your disputes within 30 days and remove false information from your credit file. When creditors ignore these requirements, they face statutory damages of $100 to $1,000 per violation, plus your actual damages and attorney fees.

Different types of identity theft require different approaches-tax identity theft demands an Identity Protection PIN from the IRS, medical identity theft means correcting your insurance records, and employment identity theft involves notifying the Social Security Administration if you receive a W-2 from an employer you never worked for. Each path follows different timelines and procedures, and missing a deadline can delay your recovery by months. We at Hays Cauley, P.C. help victims navigate this complexity by coordinating with creditors and credit bureaus on your behalf, maintaining detailed documentation of every step, and pursuing restitution when companies violate your rights.

Having someone manage your identity theft case help means you stop fighting creditors alone and start moving toward actual resolution. Contact Hays Cauley, P.C. to discuss your situation and learn how legal protection accelerates your path forward. Recovery takes time, but you don’t have to do it by yourself.