Which is a Possible Effect of Identity Theft?

Identity theft happens faster than most people realize. A criminal can open accounts, rack up debt, and damage your credit score in days.

Which is a possible effect of identity theft? The financial fallout can include unauthorized charges, rejected loan applications, and years of recovery work. We at Hays Cauley, P.C. help victims navigate this process and protect their rights, Serving South Carolina, including Greenville, Columbia and Charleston.

How Identity Theft Damages Your Credit Immediately

Fraudulent Accounts Tank Your Score Fast

Criminals don’t wait weeks to exploit stolen identities. Within 24 to 48 hours, a thief can open new credit accounts in your name, apply for loans, or max out existing cards. The Federal Trade Commission reports that identity theft complaints reached over 2.6 million in 2023, with credit card fraud and new account fraud accounting for the largest share of cases. When unauthorized accounts appear on your credit report, they tank your credit score instantly because credit bureaus treat them as legitimate debt you owe.

A single fraudulent account can drop your score by 50 to 100 points, depending on the account size and your existing credit profile. The damage compounds because creditors see these accounts as proof you’re irresponsible with credit, making it harder to qualify for mortgages, car loans, or even rental agreements. What makes this worse is that you might not notice for months. Most people discover identity theft when applying for a loan and getting rejected, or when they check their credit report and see accounts they never opened.

The Cost of Inaction Multiplies Over Time

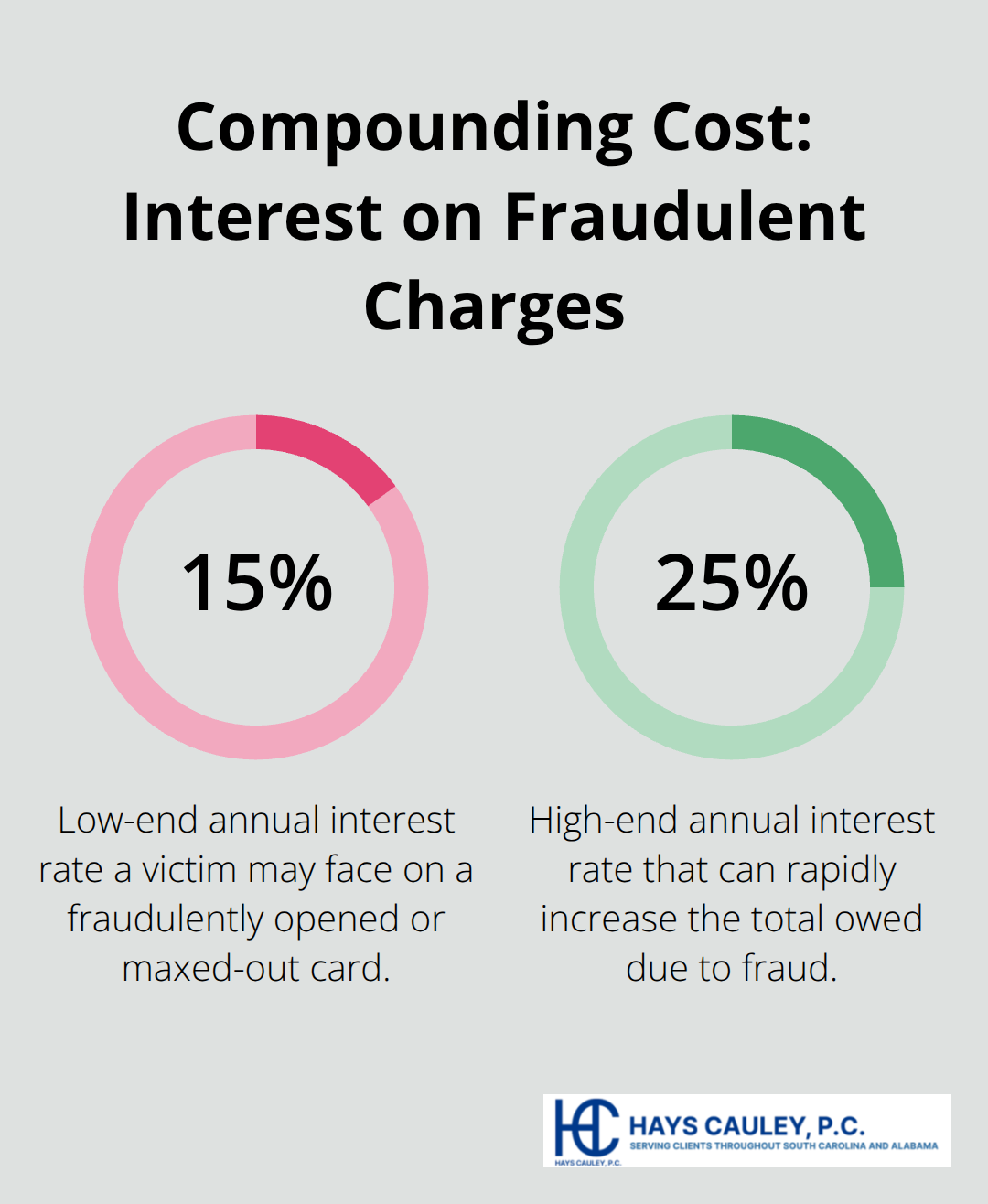

The longer fraudulent accounts remain on your report, the deeper the damage spreads through your credit history. Fraudulent charges accumulate interest and late fees, making the total amount owed grow substantially. If a thief opens a credit card with a $10,000 limit and maxes it out, you’re not just fighting $10,000 in unauthorized charges-you’re fighting interest rates that could be 15 to 25 percent annually.

Experian data shows that identity theft victims spend an average of 200 hours resolving the fraud and restoring their credit, spread across months or years of back-and-forth with creditors and credit bureaus. This isn’t just a time burden; it’s a financial one. Many victims hire an attorney to handle disputes and recovery, adding legal fees to an already mounting bill.

What Happens Next

The financial impact extends far beyond the initial fraudulent charges. Your damaged credit score affects everything from your ability to rent an apartment to the interest rates you’ll pay for years to come. Understanding how quickly identity theft spreads is the first step toward protecting yourself-and knowing when to seek help from a consumer protection law firm like Hays Cauley, P.C. can make the difference between months of struggle and a faster path to recovery.

How Identity Theft Wrecks Your Financial Future

Lenders Reject Your Application Immediately

Lenders reject your application the moment they see fraudulent accounts on your credit report. Within weeks of identity theft, you’ll face denials for mortgages, auto loans, credit cards, and even apartment rentals. Landlords pull credit reports as a standard screening tool, and a damaged credit file signals risk to them.

The rejection happens faster than most victims expect. A single fraudulent account can trigger automatic denials from lenders who use automated systems to screen applicants. You won’t get a second chance to explain the fraud during this initial screening phase.

Higher Interest Rates Cost You Tens of Thousands

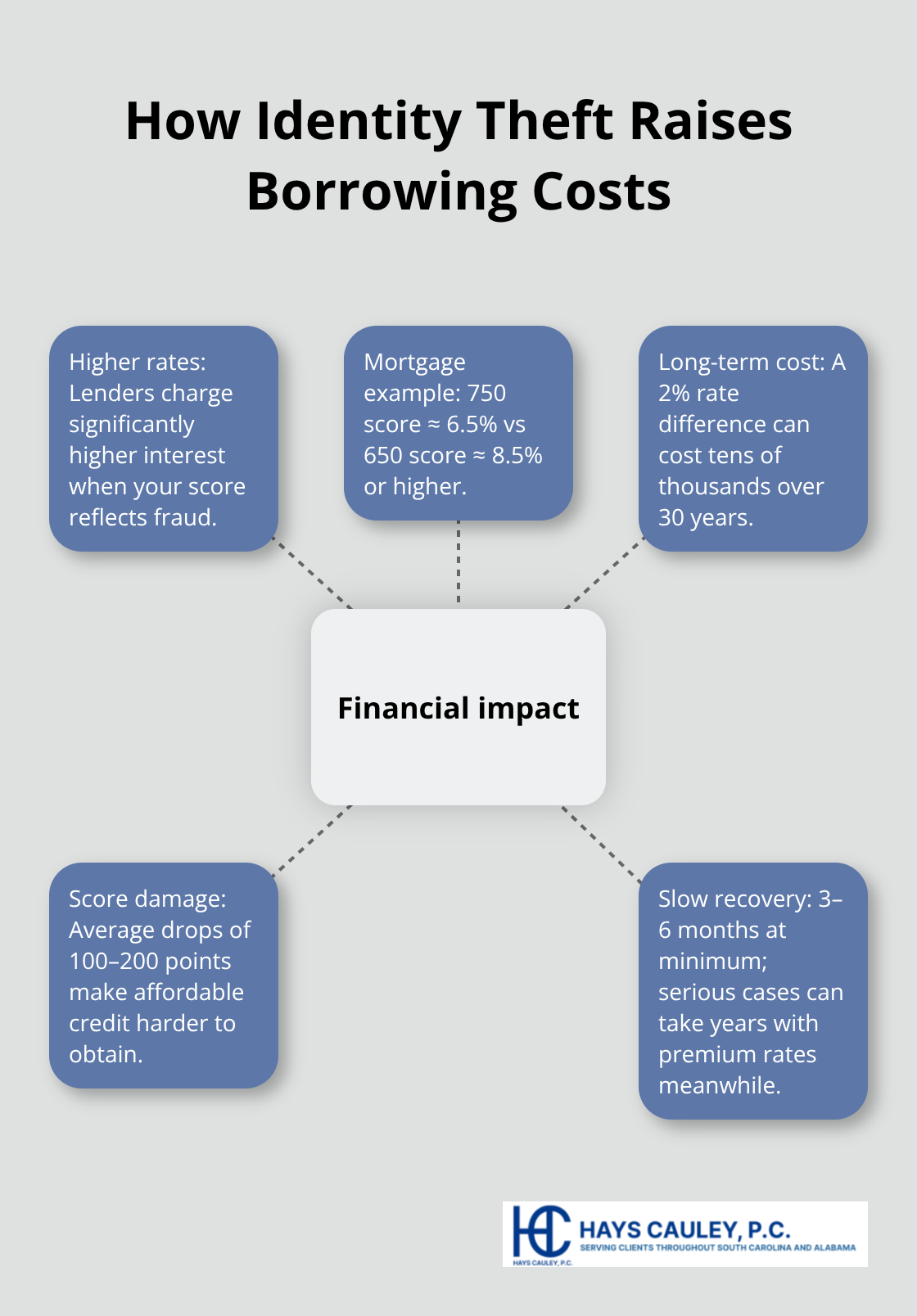

If you do qualify for credit after identity theft, lenders charge significantly higher interest rates because your credit score now reflects the fraud. Someone with a 750 credit score might qualify for a mortgage at 6.5 percent, while an identity theft victim with a 650 score pays 8.5 percent or higher. Over a 30-year mortgage, that 2 percent difference costs you tens of thousands of dollars in extra interest.

Experian reports that the average identity theft victim’s credit score drops 100 to 200 points. Recovery takes 3 to 6 months at minimum, though serious cases stretch to years. During this entire period, you pay premium rates on every loan you obtain.

The Hidden Cost: Time and Money Fighting the Fraud

The hidden cost most people underestimate is the time and money spent fighting the fraud itself. The Federal Trade Commission estimates identity theft victims spend an average of 200 hours resolving the damage. That equals five full work weeks of phone calls, paperwork, disputes with credit bureaus, and correspondence with creditors.

You’ll need to file disputes with each bureau, send proof of fraud to creditors, and gather documentation. Initial responses often get lost or mishandled, requiring follow-up calls and repeated submissions. Many victims hire an attorney to navigate this process, which adds $1,000 to $5,000 in legal fees depending on complexity.

Moving Forward With Professional Help

The real cost of identity theft isn’t just the fraudulent charges; it’s the years of higher borrowing costs and the hundreds of hours spent proving those accounts aren’t yours. A consumer protection law firm like Hays Cauley, P.C. can handle these disputes and help you recover your financial standing, saving you from months of frustration and compounding damage.

The next step involves taking immediate action to stop the bleeding and prevent further damage to your credit profile.

Act Now to Stop Identity Theft Damage

Contact Your Banks and Credit Bureaus Immediately

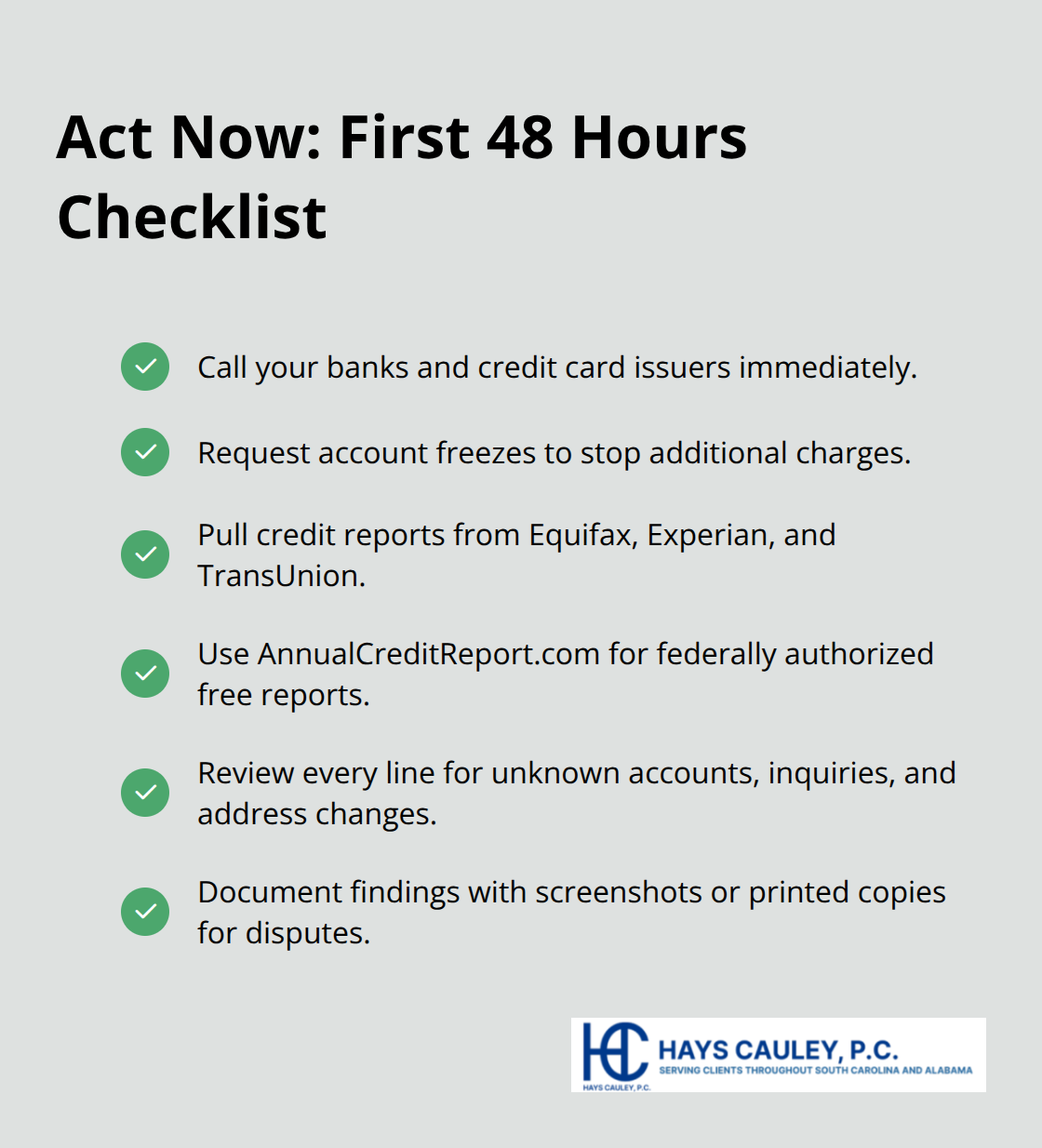

Speed matters more than perfection when identity theft strikes. The first 48 hours are critical because every day you delay allows fraudsters to open more accounts and rack up additional charges. Call your banks and credit card companies immediately to report any unauthorized transactions and request account freezes. Then pull your credit reports from all three bureaus at annualcreditreport.com, the only federally authorized source for free reports.

The Federal Trade Commission reports that 26 percent of identity theft victims didn’t discover the fraud for over a year, which means months of unchecked damage. Request copies from Equifax, Experian, and TransUnion on the same day you discover the theft, then review them line by line for accounts you didn’t open, inquiries you didn’t authorize, and address changes that aren’t yours. Document everything you find with screenshots or printed copies because you’ll need this evidence for disputes and potential legal action.

Place Fraud Alerts and File Official Reports

Contact the three credit bureaus to place a fraud alert on your file, which requires creditors to verify your identity before opening new accounts. Call the fraud department at each bureau and request an initial fraud alert, valid for one year, or consider an extended fraud alert lasting seven years if the theft is serious. The Federal Trade Commission also requires you to file an identity theft report at IdentityTheft.gov, which generates an official report you can share with creditors and law enforcement. This report carries legal weight that generic complaints lack.

File a police report with your local law enforcement agency and obtain a case number, even if the police seem reluctant to investigate. Many jurisdictions treat identity theft as low priority, but the case number strengthens your disputes with creditors and credit bureaus.

Send Written Disputes to Credit Bureaus

Send written disputes to each bureau listing the fraudulent accounts and include copies of your police report and FTC report. Use certified mail with return receipt so you have proof of delivery. Credit bureaus have 30 days to investigate, though serious cases often require follow-up disputes.

If you face substantial fraud or the process becomes overwhelming, a consumer protection law firm like Hays Cauley, P.C. can file disputes on your behalf and handle creditor negotiations. This approach accelerates recovery and prevents critical deadlines from slipping past.

Final Thoughts

Identity theft causes serious financial damage that extends far beyond the initial fraudulent charges. The effects ripple through your credit score, borrowing costs, and personal finances for years. A single stolen identity can result in unauthorized accounts, rejected loan applications, and tens of thousands of dollars in higher interest rates.

Which is a possible effect of identity theft? Your credit score drops 100 to 200 points within days, lenders deny your applications automatically, and landlords reject your rental applications. Every loan you eventually qualify for costs significantly more because your credit profile now reflects fraud you didn’t commit. The time burden alone-averaging 200 hours of dispute work-makes recovery a grueling process that most people underestimate.

Immediate action protects your financial future and prevents the damage from compounding. Contact your banks, pull your credit reports, place fraud alerts, and file an official report with the Federal Trade Commission within the first 48 hours. If the process becomes overwhelming or you face resistance from creditors and bureaus, contact Hays Cauley, P.C. to discuss your situation and explore your options for faster recovery, Serving South Carolina, including Greenville, Columbia and Charleston.