Identity theft protection plan: Build Your Defense and Recovery Strategy

Identity theft happens faster than most people realize. Criminals can open accounts, rack up debt, or drain savings in days, leaving victims to spend months or years cleaning up the mess.

We at Hays Cauley, P.C. created this guide to help you build a solid identity theft protection plan before trouble strikes. You’ll learn how to spot warning signs, strengthen your defenses, and recover quickly if theft occurs.

Understanding Identity Theft Risks

Financial Identity Theft and Beyond

Financial identity theft dominates the landscape, accounting for the most common form of fraud where criminals use your Social Security number or financial data to steal money or open new credit lines in your name. However, this represents only one threat among many. Tax identity theft occurs when criminals file false returns to claim refunds, and the IRS will never contact you by phone or text about this-if your return gets rejected, contact the IRS immediately and consider obtaining a fraud PIN. Medical identity theft can lead to inappropriate medical care, unexpected bills in your name, and duplicate or conflicting medical records that complicate emergencies, making it particularly dangerous during health crises. Employment identity theft happens when fraudsters use your information for background checks; you can verify which employers have accessed your records through the E-Verify system.

Threats Targeting Vulnerable Populations

Child identity theft exploits the fact that children often have no credit history, making them attractive targets-check their credit reports with all three bureaus and consider freezing or locking their credit if you suspect fraud. Estate identity theft targets deceased persons’ data, so death notices must be added to credit reports promptly. Criminal identity theft occurs when criminals use your information with law enforcement, which requires limiting how much personal data you share online. Synthetic identity theft combines real and fake data to create entirely new identities, requiring constant vigilance across your credit reports.

How Criminals Access Your Information

Criminals obtain your data through multiple pathways, and understanding these vectors helps you close gaps in your defense. Wallet theft, mail theft, and change-of-address forms remain surprisingly effective, while third-party data brokers legally sell your information to anyone willing to pay.

Data breaches continue rising-the Identity Theft Research Center documented 1,862 data compromises in the United States in 2021, a 68% increase from 2020. Phishing emails and smishing texts designed to mimic legitimate companies trick you into surrendering credentials on fake websites. ATM skimming devices capture card data during routine transactions, and unsecured websites or public Wi-Fi expose your information during normal browsing. Impersonation at open houses allows criminals to submit change-of-address requests before you do.

Spotting the Red Flags

The FTC recorded 5.1 million fraud reports in 2023, including identity theft cases, while IdentityTheft.gov logged approximately 1.1 million identity theft reports in 2022. Warning signs appear on your credit report as unfamiliar accounts, late payments or accounts in collections, and unfamiliar or numerous inquiries from lenders. Unexpected loan denials, unexplained withdrawals from bank accounts, multiple tax returns filed in your name, and bills arriving for accounts you never opened signal active fraud. Check for these indicators monthly by reviewing your credit reports from all three nationwide bureaus at annualcreditreport.com, where you receive free copies every 12 months, or monitor Equifax reports more frequently through your myEquifax account. Early detection minimizes damage and sets the stage for faster recovery once you identify the problem.

Building Your Defense Strategy

Monitor Your Credit Reports Regularly

Your credit reports function as a financial mirror reflecting every account opened and transaction made in your name. Criminals count on you never checking them, so pulling your reports every few months becomes your most powerful early warning system. Access free copies from all three bureaus at annualcreditreport.com once yearly, but don’t stop there-use your myEquifax account to monitor Equifax reports monthly at no cost.

When you review these reports, scan for unfamiliar accounts, unexpected inquiries from lenders, or late payments you never made. This monthly habit catches fraud within weeks rather than months, cutting your recovery time dramatically.

Beyond credit reports, monitor your bank and credit card statements weekly for unauthorized transactions. Set up account alerts through your financial institutions so you receive notifications for purchases over a certain threshold or any login from an unfamiliar device.

Strengthen Your Passwords and Enable Two-Factor Authentication

Strong passwords and two-factor authentication form the second pillar of your defense, yet most people treat them as afterthoughts. Your passwords should contain at least 16 characters mixing uppercase, lowercase, numbers, and symbols-a significant jump from the common 8-character minimum that attackers crack in seconds. Change passwords every 90 days and never reuse them across accounts, since one breached database gives criminals keys to your entire digital life.

Two-factor authentication adds a second verification step requiring something you have (a phone or security key) in addition to something you know (your password). Financial institutions, email providers, and social media platforms all support this feature. Activate it everywhere it’s available, prioritizing accounts tied to money or identity recovery like banking, email, and tax filing platforms.

Protect Your Physical Documents and Lock Your Credit

Secure your physical documents by storing sensitive papers in a locked safe, shredding anything with account numbers or Social Security numbers before discarding it, and collecting mail daily to prevent theft. Consider placing a security freeze on your credit reports through Equifax, Experian, and TransUnion-this prevents criminals from opening new accounts even if they possess your personal information, though you’ll need to temporarily lift the freeze when applying for legitimate credit yourself. These defensive measures work best when combined, creating multiple barriers that force attackers to abandon their efforts and move to easier targets. Once your defenses are in place, you need a recovery plan ready for the moment when warning signs appear.

Creating Your Recovery Plan

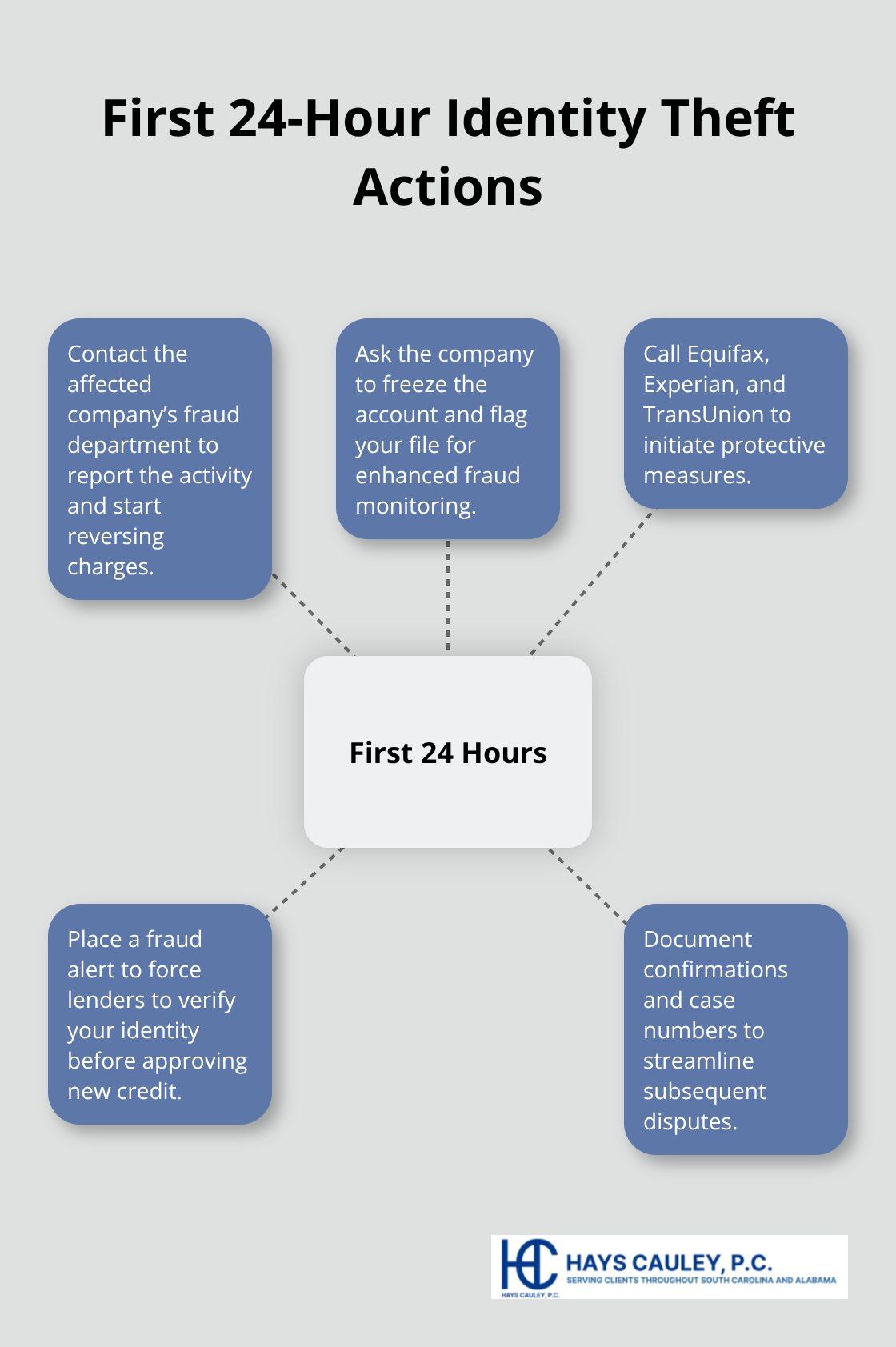

Act Within the First 24 Hours

The first 24 hours after discovering identity theft determine how quickly you’ll regain control. Contact the fraud department of the affected company immediately-whether that’s your bank, credit card issuer, or utility provider-and report the unauthorized activity. Request that they freeze the account, reverse fraudulent charges, and flag your file for fraud monitoring. Then call the three nationwide credit bureaus: Equifax, Experian, and TransUnion.

Place a fraud alert on your credit reports, which informs lenders to heighten scrutiny before approving new credit in your name. This single step gets shared across all three bureaus automatically, creating a coordinated defense.

File Your FTC Identity Theft Report

File an identity theft affidavit with the FTC at identitytheft.gov, which generates a personalized recovery plan tailored to your situation. This plan becomes your roadmap for the weeks ahead, listing specific steps for each type of fraud you’ve experienced. Many victims skip this step thinking it’s unnecessary, but the FTC’s structured process accelerates recovery substantially compared to handling everything independently. File a police report with local law enforcement the same day-this provides official documentation that strengthens your position when disputing fraudulent accounts and supports your recovery efforts with creditors.

Implement Credit Freezes and Ongoing Monitoring

Consider placing a security freeze on your credit reports through Equifax, Experian, and TransUnion if you want maximum protection moving forward. Unlike a fraud alert, a freeze blocks access to your credit report entirely, preventing criminals from opening new accounts even if they have your information, though you’ll need to temporarily lift it when applying for legitimate credit yourself. Monitor your credit reports weekly for the next several months, checking for new fraudulent accounts that might slip through. If you discover additional fraud, contact those creditors immediately and update your FTC report.

Work with Restoration Services and Document Everything

Many identity theft protection services offer dedicated identity restoration specialists who handle communications with creditors on your behalf, which saves substantial time and frustration during recovery. Review your bank and credit card statements line by line for 90 days following discovery, since some fraudsters space out charges to avoid immediate detection. Document everything meticulously: keep records of every phone call with dates and names, save emails from creditors, and maintain copies of dispute letters you send. This documentation proves invaluable if creditors challenge your claims or if the fraud extends into legal territory requiring professional assistance.

Final Thoughts

Building an identity theft protection plan requires action on two fronts: prevention before fraud strikes and swift recovery if it does. The steps outlined in this guide work together to create a comprehensive defense that catches criminals early and limits the damage they can inflict. Start with monthly credit report monitoring, strong passwords with two-factor authentication, and secured physical documents-these habits form your first line of defense and make you a harder target than victims who ignore these basics.

If theft occurs despite your precautions, the first 24 hours matter most. Contact your financial institutions, place fraud alerts with the credit bureaus, and file your FTC identity theft report at identitytheft.gov to obtain your recovery roadmap. This structured approach gives you official documentation that creditors respect and accelerates resolution substantially compared to struggling alone.

Your recovery continues after the initial crisis passes as you monitor your credit reports weekly for several months, document all communications with creditors, and consider placing security freezes for ongoing protection. If you’re facing identity theft or credit reporting issues, Hays Cauley, P.C. helps consumers navigate these challenges and protect their financial futures.