Identity Theft Safety Tips: Techniques to Protect Your Finances

Identity theft costs Americans over $20 billion annually, with the Federal Trade Commission reporting more than 2.6 million fraud complaints in 2023. Criminals are getting smarter about stealing personal information, and waiting to act puts your finances at serious risk.

We at Hays Cauley, P.C. created this guide to give you practical identity theft safety tips that actually work. You’ll learn how theft happens, what steps protect you right now, and exactly what to do if you become a victim.

How Criminals Steal Your Information and Damage Your Finances

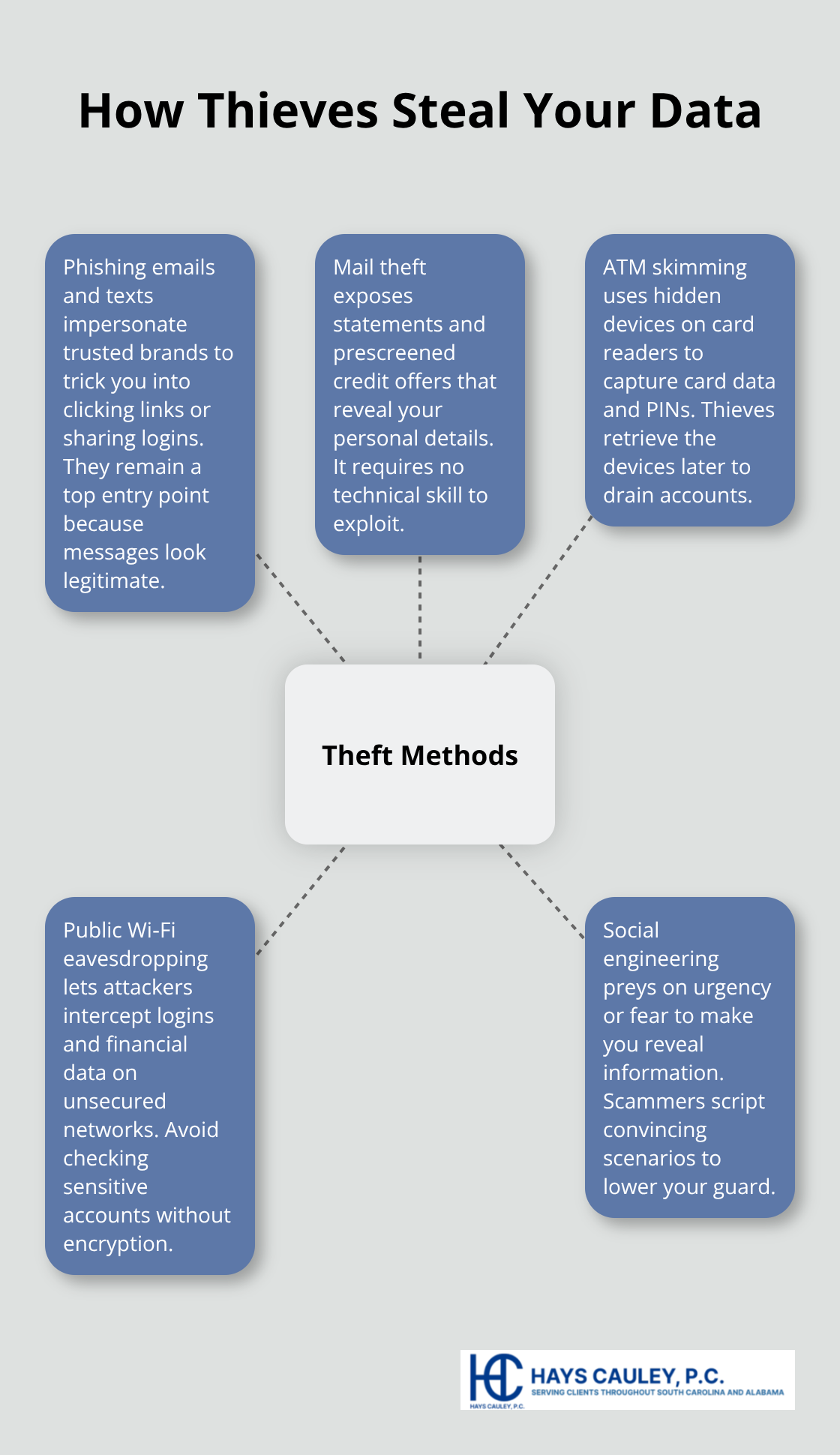

Methods Criminals Use to Steal Your Data

Criminals don’t need sophisticated hacking skills to steal your identity. The Federal Trade Commission reported more than 1 million identity theft cases last year, and the methods used are often surprisingly simple. Phishing emails and text messages remain the most effective attack vector, accounting for a massive portion of successful thefts. Scammers send messages that look legitimate, asking you to verify account information or click a link, and most people fall for them because the emails mimic real companies you trust.

Mail theft is equally dangerous and requires zero technical knowledge-a criminal simply takes your mail and finds credit card statements, tax documents, or prescreened credit offers with your name and address. ATM skimming represents another common tactic where thieves install hidden devices on card readers to capture your account information when you withdraw cash. Public Wi-Fi networks expose your data constantly; using unsecured networks to check your bank account or enter passwords hands your information directly to anyone monitoring that network.

How Identity Theft Damages Your Credit Score

When criminals open credit cards in your name, they damage your credit score, which affects your ability to get loans, mortgages, or even employment. The average victim spends between $1,000 and $15,000 out of pocket to resolve fraudulent charges, and recovery can take months or years. Tax refund theft happens when criminals file fraudulent tax returns using your Social Security number, blocking you from claiming your legitimate refund.

Immediate Financial Threats You Face

Bank account drains pose immediate threats-criminals can transfer funds or set up unauthorized wire transfers within hours. Health insurance fraud is particularly dangerous because it creates false medical records under your name, potentially leading to incorrect diagnoses or treatment conflicts if you need emergency care. The emotional toll is substantial too; victims report severe stress, anxiety, and difficulty trusting financial institutions long after the theft is resolved.

These threats make it clear why taking protective action now matters far more than waiting until after theft occurs.

Protect Your Credit and Personal Data Right Now: Serving South Carolina, including Greenville, Columbia and Charleston

Monitor Your Credit Reports Throughout the Year

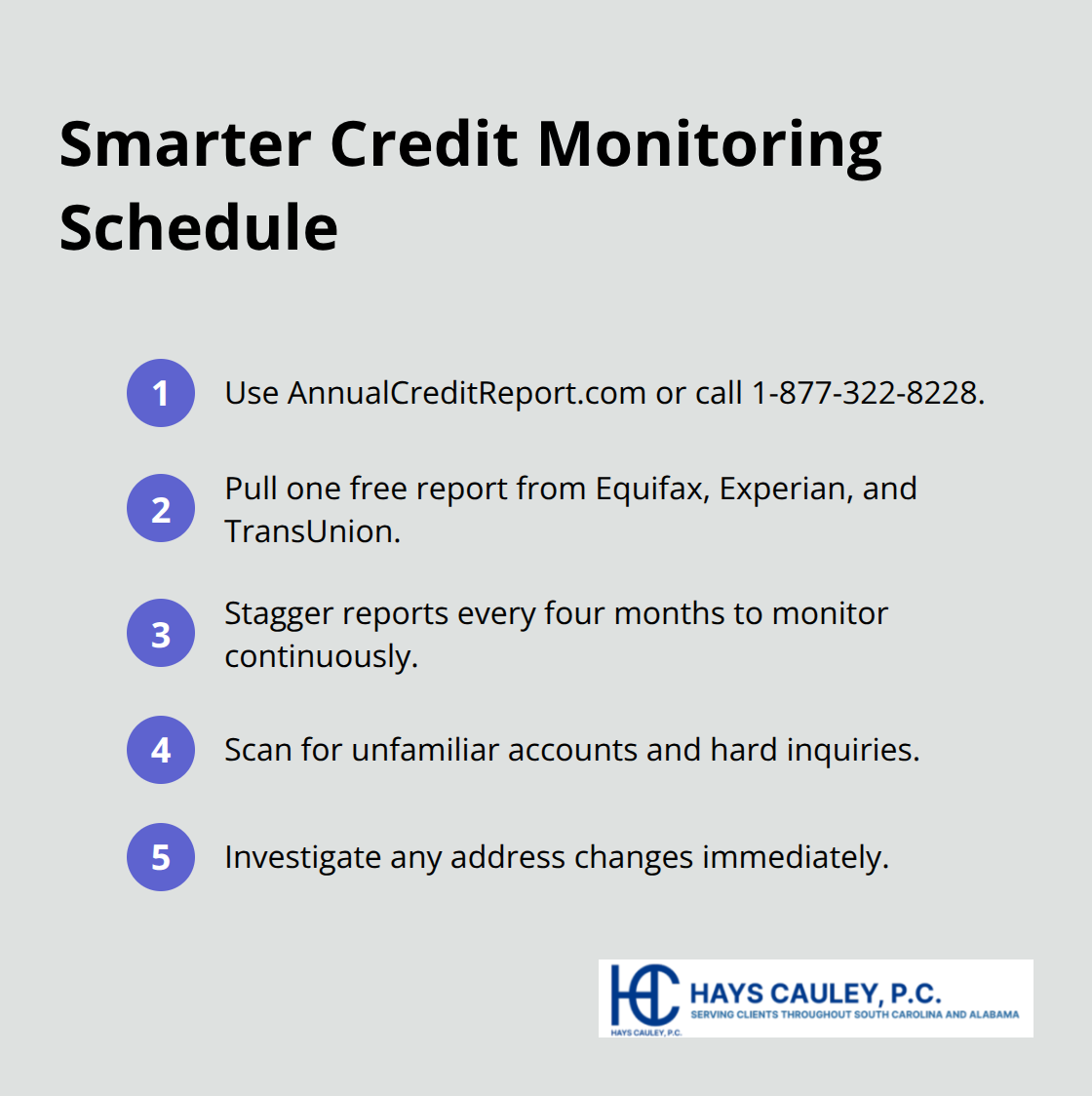

You cannot catch identity theft before criminals drain your accounts without checking your credit report. The Federal Trade Commission allows you to access one free credit report annually from each of the three major credit bureaus-Equifax, Experian, and TransUnion-through annualcreditreport.com or by calling 1-877-322-8228. Most people pull all three reports at once, but a smarter approach spreads them out every four months so you monitor your credit continuously throughout the year. When you review each report, look for accounts you never opened, inquiries from companies you didn’t contact, and address changes you didn’t authorize. These red flags indicate someone is using your identity.

Open and read your bank and credit card statements the moment they arrive; unauthorized charges often appear within days of theft, and catching them quickly limits your liability. If your normal statements stop arriving by mail, contact the company immediately because missing statements frequently signal an address change used to hide fraudulent activity.

Create Passwords That Actually Stop Thieves

Using the same password across multiple accounts guarantees that one data breach compromises everything you own. The Federal Trade Commission recommends passwords with a minimum of 8 characters that include letters, numbers, and symbols, but longer passwords work better. Change passwords every few months and never reuse old ones, which means writing them down securely or using a password manager rather than relying on memory. When you access financial accounts online, use only secure websites showing https in the address bar and a padlock icon, and log out completely after finishing. For online shopping, use a single credit card rather than your debit card, which offers stronger fraud protection under federal law. Never enter sensitive information on public Wi-Fi networks; if you must use unsecured networks, connect through a virtual private network or VPN to encrypt your data.

Guard Your Physical Information Like Cash

Your Social Security card should stay locked in a safe at home unless you need it for a specific appointment. Shred receipts, credit offers, loan applications, insurance forms, and bank statements using a cross-cut shredder before discarding them, as criminals routinely search trash for discarded documents containing your information. Collect your mail daily and place a hold with the postal service if you travel, preventing thieves from stealing prescreened credit offers or statements. Limit what you carry in your wallet to one or two credit cards and leave your Social Security card at home entirely. When you receive credit card receipts, verify they display only your last four digits; if a receipt shows your full account number, report it to your state’s Attorney General office immediately.

Secure Your Online Activity on Any Network

Install and maintain a personal firewall on your device and keep your security software up to date with automatic updates (anti-virus, anti-spyware, anti-spam). Secure your home wireless network with encryption and turn off wireless connectivity if you leave your computer unattended. When using a hotspot or unencrypted wireless, disable wireless ad hoc mode to prevent rogue connections and disable file and printer sharing. Access your brokerage account from your own computer on a secure connection and log out completely when finished. These steps (combined with strong passwords and regular statement reviews) create multiple layers of protection that make your accounts far less attractive targets for criminals.

The steps you take today determine whether you spend months recovering from identity theft or catch fraud before it causes serious damage. Understanding what to do if theft does occur gives you the confidence to act quickly and minimize losses.

What to Do If Identity Theft Happens to You

Act Within 24 Hours to Limit Damage

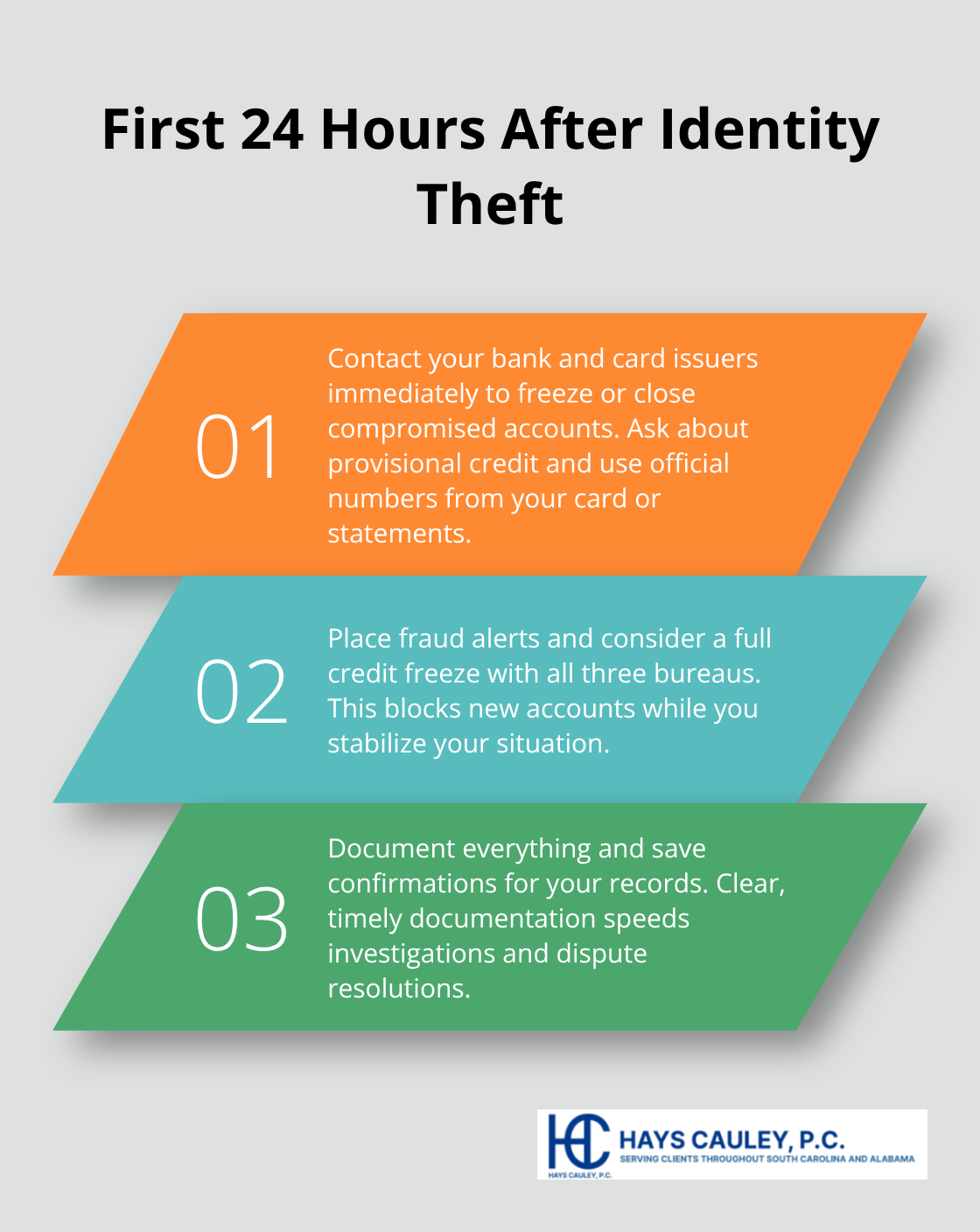

Act within 24 hours of discovering identity theft because criminals move fast and every hour matters. Your first call should go to your bank and credit card issuers-tell them fraud occurred and ask them to freeze or close compromised accounts immediately. Contact the fraud departments directly using the phone numbers on the back of your cards or on your statements, never numbers from unknown sources or internet searches, as scammers impersonate financial institutions constantly. Request that your financial institutions place a fraud alert on your accounts and ask about provisional credit for unauthorized charges, which federal law allows banks to provide while they investigate.

Place a Credit Freeze and File Your FTC Report

Place your freeze immediately with all three major credit bureaus-Equifax, Experian, and TransUnion-by calling or visiting their websites, which prevents thieves from opening new accounts in your name even if they have your Social Security number. The Federal Trade Commission updated guidance in 2025 emphasizing that a credit freeze represents one of the strongest first steps to stop identity thieves. File a report immediately on IdentityTheft.gov, the official FTC platform that documents your theft and creates a recovery plan tailored to your situation. If you cannot reach IdentityTheft.gov, call 1-877-438-4338 to report to the FTC directly. This documentation becomes critical if you need to dispute fraudulent charges or accounts later.

Provide Detailed Information to Financial Institutions

Working with your financial institutions means providing them with detailed information about fraudulent transactions, account numbers, and dates when theft occurred. Request written confirmation of all fraud reports and freeze requests for your records-these documents prove you reported the theft quickly if disputes arise later. If tax-related identity theft occurred, file Form 14039 with the IRS immediately to flag the fraudulent return and protect your refund.

Dispute Fraudulent Accounts on Your Credit Reports

Review your credit reports from all three bureaus after filing your report and look for accounts you never opened, inquiries from companies you didn’t contact, and unauthorized address changes. Dispute every fraudulent item directly with the credit reporting agencies in writing, providing copies of your FTC identity theft report as evidence. The agencies must investigate disputes within 30 days and remove unverified information from your report. Monitor your credit reports for at least one year and continue checking for new fraudulent accounts or inquiries. Many victims discover additional fraud months after the initial incident, so ongoing vigilance prevents criminals from causing further damage.

Get Professional Help When Recovery Becomes Complex

Coordinating with multiple financial institutions and government agencies becomes overwhelming quickly. Hays Cauley, P.C., a consumer protection law firm dedicated to helping consumers with credit reporting and identity theft issues, works with victims navigating this complex recovery process and understands that having professional guidance makes the difference between recovering efficiently and spending months resolving preventable complications.

Final Thoughts

Identity theft prevention starts with action, not hope. The identity theft safety tips covered throughout this guide work because they address how criminals actually operate, not theoretical threats. Monitoring your credit reports every four months, using strong passwords across different accounts, and securing your physical documents create layers of protection that make your information far less attractive to thieves.

If theft occurs, your response in the first 24 hours determines your outcome. Contacting your financial institutions, placing a credit freeze, and filing your FTC report on IdentityTheft.gov stops most damage before it spreads. South Carolina residents can access the same federal resources as everyone else, including free credit reports from annualcreditreport.com and fraud reporting through the FTC.

Recovery becomes complicated when fraudulent accounts multiply across multiple institutions or when criminals file tax returns in your name. Coordinating disputes with credit bureaus, working with the IRS on tax-related theft, and managing provisional credit claims requires tracking numerous deadlines and documentation requirements. We at Hays Cauley, P.C. help victims with credit reporting and identity theft issues when recovery becomes overwhelming.