Fair Credit Reporting Act Violations: What You Need to Know

Credit reporting errors affect millions of Americans every year, damaging credit scores and limiting financial opportunities. The Fair Credit Reporting Act provides strong protections against these violations.

We at Hays Cauley, P.C. see how a comprehensive Fair Credit Reporting Act violations list can help consumers identify when their rights have been violated and take action to restore their credit standing.

What FCRA Violations Look Like in South Carolina

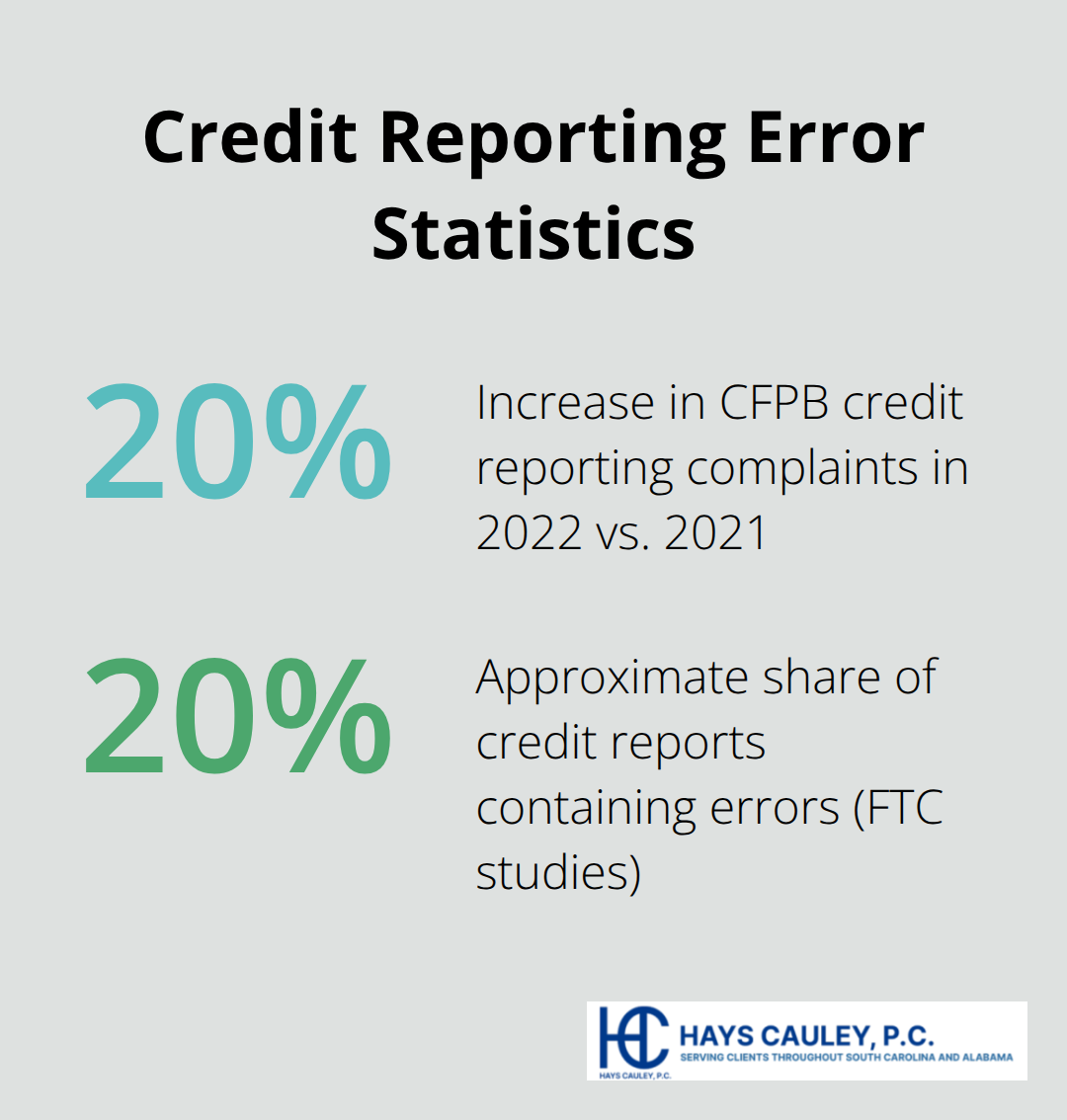

Credit bureaus routinely violate the Fair Credit Reporting Act through systematic failures that devastate consumer credit scores. The Consumer Financial Protection Bureau received 20% more credit reporting complaints in 2022 compared to 2021, with approximately 20% of all credit reports containing errors according to Federal Trade Commission studies. These violations fall into clear patterns that South Carolina consumers can identify and challenge.

Credit Bureau Investigation Failures

Credit bureaus consistently fail their 30-day investigation requirement under FCRA Section 1681i. When consumers dispute errors, bureaus often conduct superficial reviews rather than thorough investigations. They frequently rely on automated systems that flag payments as late without human verification, which leads to systematic violations of your rights under the FCRA. This practice violates federal law and allows inaccurate information to persist on credit reports for years.

Furnisher Reporting Violations

Data furnishers like banks and collection agencies submit unverified information to credit bureaus without proper documentation. They report outdated debts, incorrect payment histories, and accounts that belong to other consumers with similar names. Medical debt furnishers particularly violate FCRA rules when they report collections before the required 365-day wait period. These furnisher errors directly cause credit score drops of 50-100 points per inaccurate account.

Unauthorized Access and Privacy Breaches

Credit bureaus illegally provide consumer reports to entities without permissible purpose under FCRA Section 1681b. Employers, landlords, and insurance companies often access credit reports without proper authorization or consumer consent. Each unauthorized access constitutes a separate FCRA violation worth up to $1,000 in statutory damages (15 U.S.C. § 1681n). South Carolina consumers can recover actual damages plus attorney fees when credit bureaus willfully violate FCRA requirements.

Willful Noncompliance Patterns

Credit bureaus demonstrate willful violations when they knowingly ignore consumer disputes or continue to report information they know is inaccurate. Courts award enhanced damages for willful FCRA violations, which can reach three times actual damages. These patterns become evident when bureaus repeatedly fail to investigate the same disputed items or restore deleted information without proper verification.

Understanding these violation patterns helps consumers recognize when credit bureaus have violated their rights under federal law.

Your Rights Under the Fair Credit Reporting Act

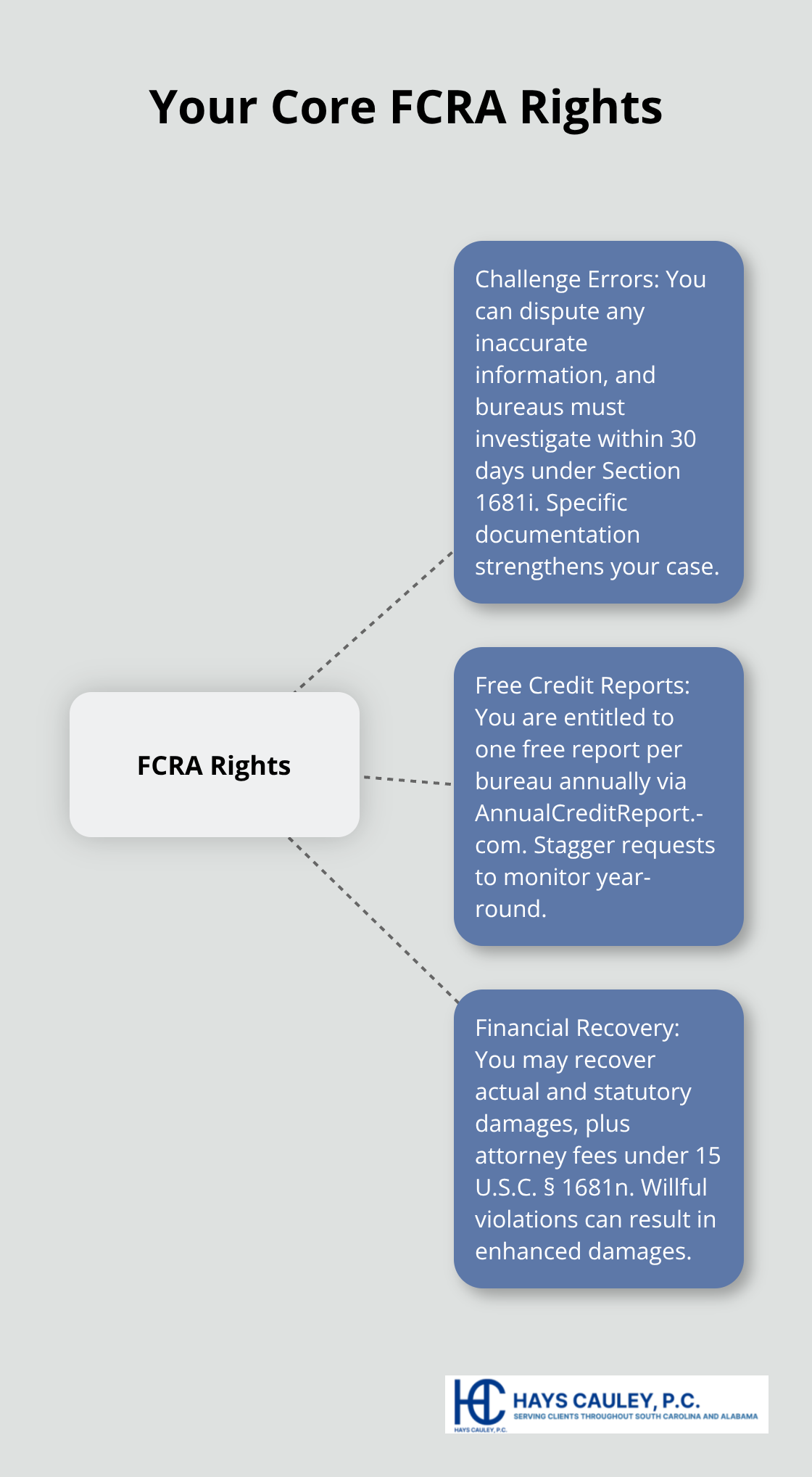

The Fair Credit Reporting Act grants you three fundamental rights that credit bureaus frequently violate through negligence or deliberate misconduct. These rights form the backbone of your protection against inaccurate credit reports, and they put you in control of your financial reputation.

Your Right to Challenge Every Error

You can dispute any inaccurate information on your credit report, and credit bureaus must investigate within 30 days under FCRA Section 1681i. This investigation requirement is not optional – credit bureaus face statutory penalties of up to $1,000 per violation when they fail to properly investigate disputes. The Consumer Financial Protection Bureau reports that 73% of disputes succeed when consumers provide specific documentation.

You can dispute items directly with all three major bureaus – Equifax, Experian, and TransUnion – since they maintain independent databases. Submit separate disputes to each bureau because removal of an error from one bureau does not automatically remove it from the others. Each bureau operates independently and requires individual notification of inaccuracies.

Your Right to Free Credit Monitoring

Federal law requires each major credit bureau to provide you with one free credit report annually through annualcreditreport.com. This means you get three free reports per year – one from each bureau every four months. South Carolina consumers should stagger these requests to monitor their credit throughout the year rather than request all three reports simultaneously.

You can also access free reports after adverse actions like loan denials or when you place fraud alerts on your accounts. These additional free reports help you track changes and verify corrections to your credit file.

Your Right to Financial Recovery

When credit bureaus violate FCRA requirements, you can recover actual damages, statutory damages up to $1,000 per violation, and attorney fees under 15 U.S.C. § 1681n. Courts award enhanced damages for willful violations, which can reach three times your actual damages. You have two years from discovery of a violation (or five years from when it occurred) to file suit.

Document higher interest rates, denied credit applications, and other financial harm caused by inaccurate reports to calculate your actual damages before you pursue legal action. This documentation becomes vital evidence when you take steps to address FCRA violations through formal dispute processes.

How Do You Take Action Against FCRA Violations

Collect Complete Documentation First

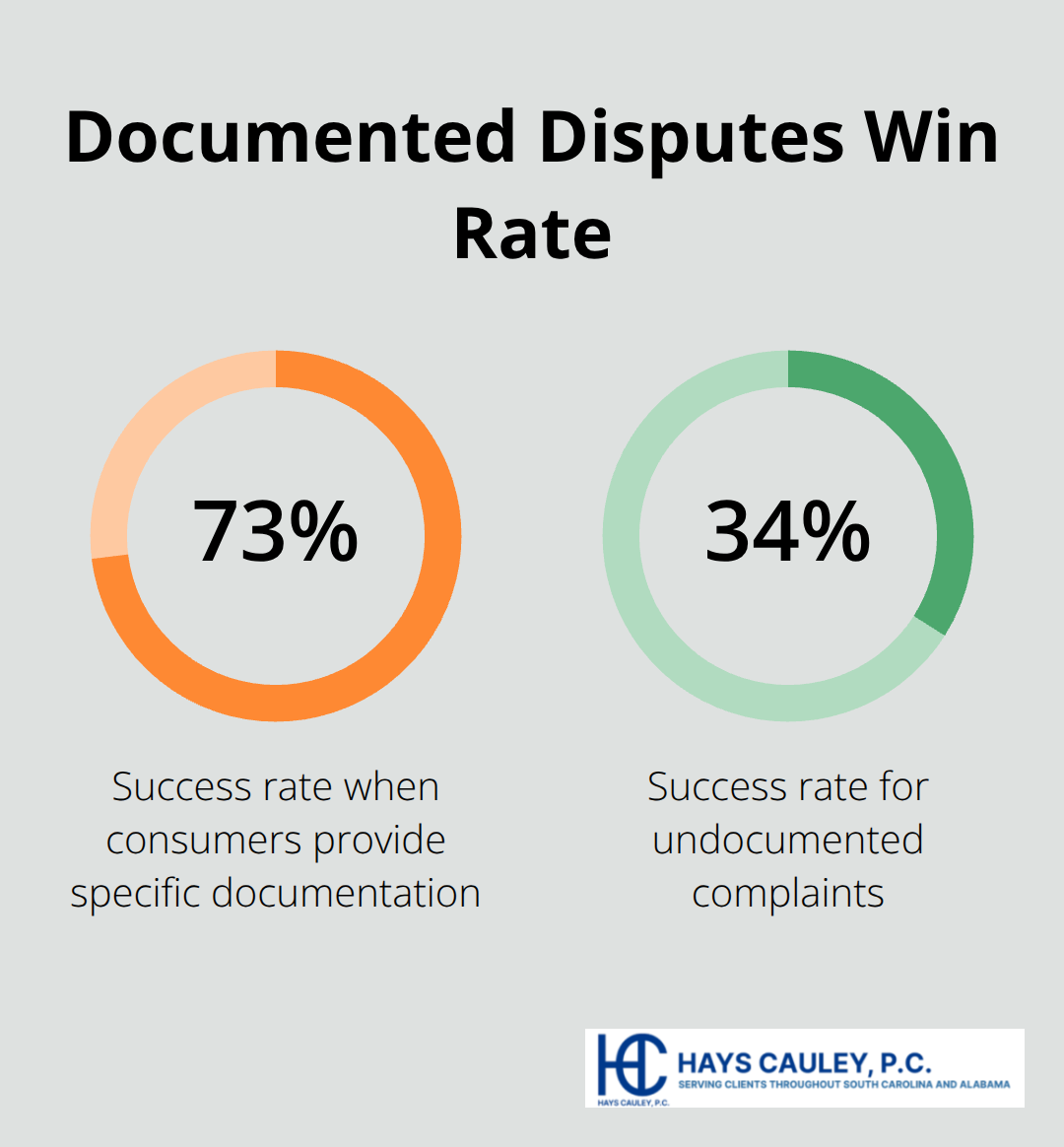

Obtain your credit reports from all three bureaus through annualcreditreport.com and take screenshots of every error you find. Print physical copies and highlight each inaccurate item with red ink – courts require concrete evidence, and digital files can be altered. Create a spreadsheet that lists each error with the account number, creditor name, incorrect information, and the correct information. The Federal Trade Commission found that documented disputes succeed 73% of the time compared to just 34% for undocumented complaints.

Calculate your actual damages when you document denied credit applications, higher interest rates on approved loans, and employment rejections based on credit checks. Save rejection letters and loan documents that show increased rates. Each piece of documentation strengthens your case for actual damages, which courts add to the $1,000 statutory penalty per willful violation under 15 U.S.C. § 1681n.

Submit Strategic Disputes to Multiple Parties

File separate disputes with each credit bureau and the original creditor who furnished the incorrect information. Credit bureaus must investigate within 30 days, but furnishers have the same obligation under FCRA Section 1681s-2. Send disputes via certified mail with return receipts to create legal proof of delivery dates. Include copies of documents like payment records, identity verification, or court judgments that prove the information is wrong.

Write specific dispute letters that reference exact account numbers and describe precisely what information is inaccurate. Avoid form letters or online dispute systems – courts view detailed written disputes as more credible evidence of your good faith efforts to resolve errors.

Maintain Detailed Records for Legal Action

Keep copies of every letter, email, and phone conversation with credit bureaus and furnishers. Note the date, time, and name of representatives you speak with during phone calls (this creates a paper trail for potential legal action). Save all responses from credit bureaus, even if they claim the disputed information is accurate. Document any restored errors that reappear on your credit report after deletion – this pattern shows willful violations that courts penalize with enhanced damages. You have two years from the discovery of violations to file suit, so organized records become vital when you need legal representation to recover damages and attorney fees.

Final Thoughts

The Fair Credit Reporting Act provides powerful protections that put you in control of your credit report accuracy. You can dispute errors, access free annual reports, and recover damages when credit bureaus violate federal law. These rights become meaningless without proper enforcement against violations.

Consider legal action when credit bureaus ignore your disputes, restore deleted errors, or continue to report information they know is inaccurate. Courts award up to $1,000 per willful violation plus actual damages and attorney fees. The two-year statute of limitations from discovery makes prompt action vital for your rights (15 U.S.C. § 1681n).

We at Hays Cauley, P.C. help South Carolina consumers fight credit report errors through strategic dispute processes and litigation when necessary. When you face a Fair Credit Reporting Act violations list on your credit report, professional legal assistance can make the difference between continued financial damage and full recovery. Contact us to discuss your specific situation and protect your financial future.