Late Payments and the Fair Credit Reporting Act in South Carolina

Late payment errors on credit reports can devastate your financial standing and limit access to loans, housing, and employment opportunities. The Fair Credit Reporting Act provides strong protections for consumers facing these issues.

We at Hays Cauley, P.C. see how Fair Credit Reporting Act late payments violations harm South Carolina residents daily. Understanding your rights helps you fight back against inaccurate credit reporting.

What Rights Does the FCRA Give You

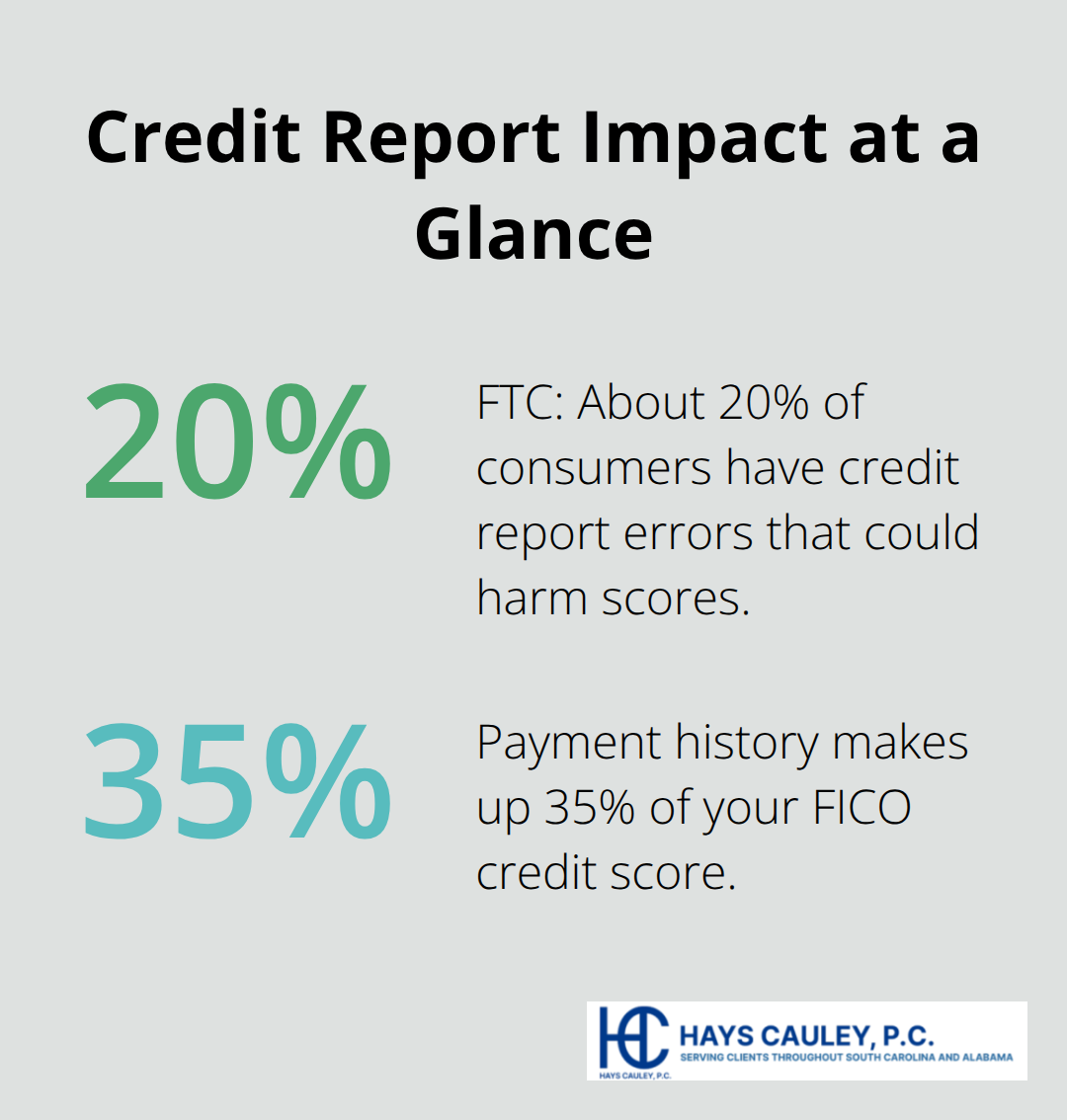

The Fair Credit Reporting Act forces credit bureaus to maintain accurate records and provides you with powerful tools to fight back when they fail. Credit reporting companies must investigate disputes within 30 days and remove unverified information from your report. The Federal Trade Commission found that approximately 20% of consumers have errors on their credit reports that could damage their credit scores, which makes these protections vital for South Carolina residents.

Maximum Time Limits Protect You

Late payments can only appear on your credit report for seven years maximum, regardless of the amount owed. Credit bureaus routinely violate this rule when they allow older negative information to remain active. Payment history accounts for 35% of your credit score, so even one incorrectly reported late payment can cost you thousands in higher interest rates. The law requires immediate removal of any payment marked late beyond the seven-year limit.

You Control Who Sees Your Information

Creditors cannot report late payments without strict verification requirements under the FCRA. They must have accurate records that show the exact date they received and processed payments. Many creditors report payments as late when system errors or delays cause the problem (not actual consumer behavior). You have the right to demand proof that any reported late payment actually occurred on the date claimed.

Credit Bureaus Must Verify Disputed Information

Credit bureaus must delete disputed information they cannot verify within the investigation period. The FCRA places the burden of proof on creditors and credit bureaus, not on you as the consumer. When you dispute a late payment, the credit bureau must contact the original creditor and request documentation. If the creditor fails to respond or cannot provide adequate proof within 30 days, the bureau must remove the negative mark from your report.

South Carolina consumers face specific challenges when creditors fail to follow proper procedures, which leads us to examine the most common violations that occur in our state.

Common Late Payment Reporting Violations in South Carolina

Creditors and credit bureaus routinely break FCRA rules when they report late payments, and South Carolina consumers pay the price through damaged credit scores and higher costs. The Federal Trade Commission receives thousands of complaints annually about these violations, with payment disputes representing the largest category of credit report errors. Most creditors use automated systems that flag payments as late without human verification, which leads to systematic violations of your rights under the FCRA.

Payment Processing Games Cost You Money

Banks and creditors often receive payments on time but process them days later to generate late fees and negative credit marks. This practice violates FCRA accuracy requirements because the payment date should reflect when the creditor received your money, not when they chose to apply it to your account. Credit card companies particularly abuse this system by setting early cutoff times or claiming payments received before 5 PM arrived the next business day.

The Consumer Financial Protection Bureau found that payment processing delays account for 23% of late payment disputes, yet creditors continue these practices because they generate millions in additional revenue. These delays can cost you hundreds of dollars in fees and thousands more in higher interest rates on future loans.

Inaccurate Payment History Documentation

Creditors frequently report payment information without proper documentation to support their claims. They must maintain accurate records that show the exact date they received and processed each payment, but many creditors rely on incomplete or corrupted data systems. Some creditors report payments as late when technical glitches or system maintenance caused the delay (not actual consumer behavior).

South Carolina consumers face particular challenges when creditors merge accounts or transfer servicing rights between companies. These transitions often result in lost payment records or incorrect late payments that appear on credit reports for years.

Missing Updates Destroy Credit Scores

Creditors frequently fail to update corrected payment information even after they acknowledge their mistakes, which leaves negative marks on your credit report indefinitely. When you pay off a disputed late payment or prove the payment was made on time, the creditor must notify all three credit bureaus within 30 days. Many creditors ignore this requirement entirely or send incomplete corrections that leave partial negative information active.

Regional creditors in South Carolina often lack proper FCRA compliance systems, which makes manual corrections nearly impossible to track or verify. These violations can persist for months or years without proper legal intervention, making it essential to understand how to dispute these errors effectively.

Steps to Dispute Late Payment Errors on Your Credit Report

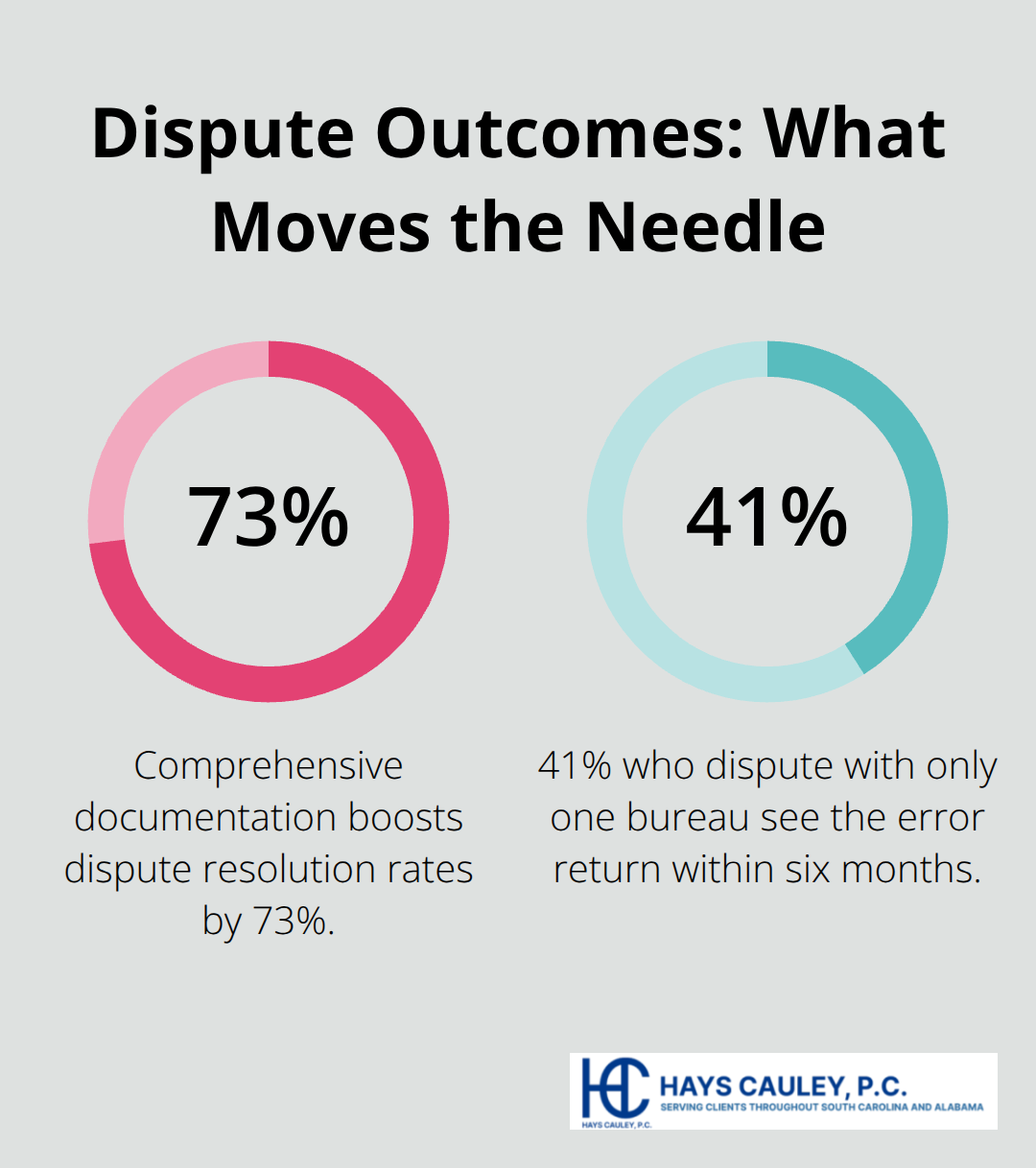

Success in late payment disputes requires strategic documentation and aggressive follow-through with credit bureaus that often ignore consumer rights. The Consumer Financial Protection Bureau reports that consumers who provide comprehensive documentation see dispute resolution rates 73% higher than those who submit basic complaints. Credit bureaus profit from inaccurate information because creditors pay them millions annually for services, which creates inherent conflicts of interest against consumers.

Document Every Payment and Communication

Gather bank statements, canceled checks, and payment confirmations that prove you made payments on time or before due dates. Credit card companies and loan servicers must provide payment histories upon request within 30 days under FCRA requirements, yet many delay or provide incomplete records. Screenshot online payment confirmations immediately after you make payments because many creditors delete these records after 90 days to avoid dispute documentation. Save email receipts, text message confirmations, and any written correspondence about payment issues because these become evidence of creditor violations.

Attack All Three Credit Bureaus Simultaneously

File identical disputes with Equifax, Experian, and TransUnion within the same week because each bureau operates independently and may respond differently to identical evidence. The Federal Trade Commission found that 41% of consumers who dispute with only one bureau see the error reappear on other reports within six months. Send disputes via certified mail with return receipts to create legal proof of delivery dates (which starts the mandatory 30-day investigation clock). Include specific language that demands removal of inaccurate late payment marks and request written confirmation of all corrections made to your file.

Force Compliance Through Persistent Follow-Up

Credit bureaus frequently send form letters that claim they investigated disputes without actually contacting creditors or reviewing evidence. Contact the original creditor directly and demand written confirmation that they will correct the error with all three bureaus within 30 days. When credit bureaus fail to remove verified errors or provide inadequate investigation results, file complaints with the Consumer Financial Protection Bureau and your state attorney general simultaneously. Document every phone call, letter, and email exchange because patterns of non-compliance become evidence of willful FCRA violations that can result in monetary damages (up to $1,000 per violation plus attorney fees).

Final Thoughts

The Fair Credit Reporting Act gives South Carolina consumers powerful weapons against inaccurate late payment reports, but these rights mean nothing without aggressive action. Credit bureaus and creditors count on consumer ignorance and inaction to maintain profitable violations that cost you thousands in higher interest rates and denied credit opportunities. Fair Credit Reporting Act late payments violations happen daily across South Carolina, yet most consumers accept these errors as permanent damage to their financial futures.

The law requires credit bureaus to investigate disputes within 30 days and remove unverified information, but they routinely ignore these requirements until they face legal consequences. You must document every payment, dispute errors with all three bureaus simultaneously, and demand written proof of corrections. When credit bureaus fail to comply with FCRA requirements, legal action becomes necessary to protect your rights and recover damages (up to $1,000 per violation plus attorney fees).

We at Hays Cauley, P.C. fight back against credit report violations for South Carolina consumers. Consumer protection laws exist to level the field against billion-dollar credit companies that profit from your inaccurate information. Take action now to protect your financial future and hold these companies accountable for their violations.