Challenge Credit Report SC Your Path To Clean Data

Credit report errors are more common than you might think, and they can damage your financial future without you even realizing it. Inaccurate information on your credit report can lower your score, making it harder to get loans or favorable interest rates.

The good news is that you have legal rights to challenge credit report SC errors. At Hays Cauley, P.C., we help South Carolina residents, including those in Greenville, Columbia, and Charleston, take control of their credit data and fix mistakes that shouldn’t be there.

How Credit Report Errors Happen in South Carolina

The Scale of the Problem

Credit report errors in South Carolina are not rare accidents-they are systemic failures that affect roughly 1 in 5 consumers according to the Federal Trade Commission. The three major credit bureaus-Equifax, Experian, and TransUnion-receive data from thousands of creditors and collection agencies, creating multiple points where mistakes slip through. Equifax reported a 99.81% accuracy rate as of February 2026, which sounds impressive until you realize that 0.19% error rate still impacts millions of people.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. South Carolina residents rank 13th in identity theft per 100,000 residents, making the state particularly vulnerable to fraudulent accounts and mixed-file errors.

Types of Errors That Damage Your Credit

Common mistakes include settled debts still showing as unpaid, duplicate entries where the same loan appears twice, fraudulent accounts opened in your name, incorrect payment histories, wrong addresses, and accounts merged due to name or Social Security number similarities. A single late payment error can drop your credit score by 50 or more points. A Zillow analysis shows that a credit score drop from the 760–850 range to 620–639 adds roughly $288 monthly to mortgage costs-about $103,626 in interest 30 years. These errors remain on your file for seven years, damaging your ability to borrow, the rates you receive, and even employment or housing decisions.

Why Bureaus Fail to Catch Mistakes

The credit reporting system prioritizes speed over accuracy. When furnishers like banks and collection agencies report data to the bureaus, they often send incomplete or conflicting information. The bureaus then match this data to existing files using algorithms that rely heavily on name, address, and Social Security number-the very information most vulnerable to typos and identity theft. South Carolina law requires bureaus to reinvestigate disputed items within 30 days, but complaints to the Consumer Financial Protection Agency surged from about 175,000 in 2020 to nearly 5 million in 2025, signaling that investigations are increasingly rushed or incomplete. CFPB funding has been significantly reduced under the current administration, weakening oversight of the major bureaus and leaving errors unchecked.

The Cost of Inaction

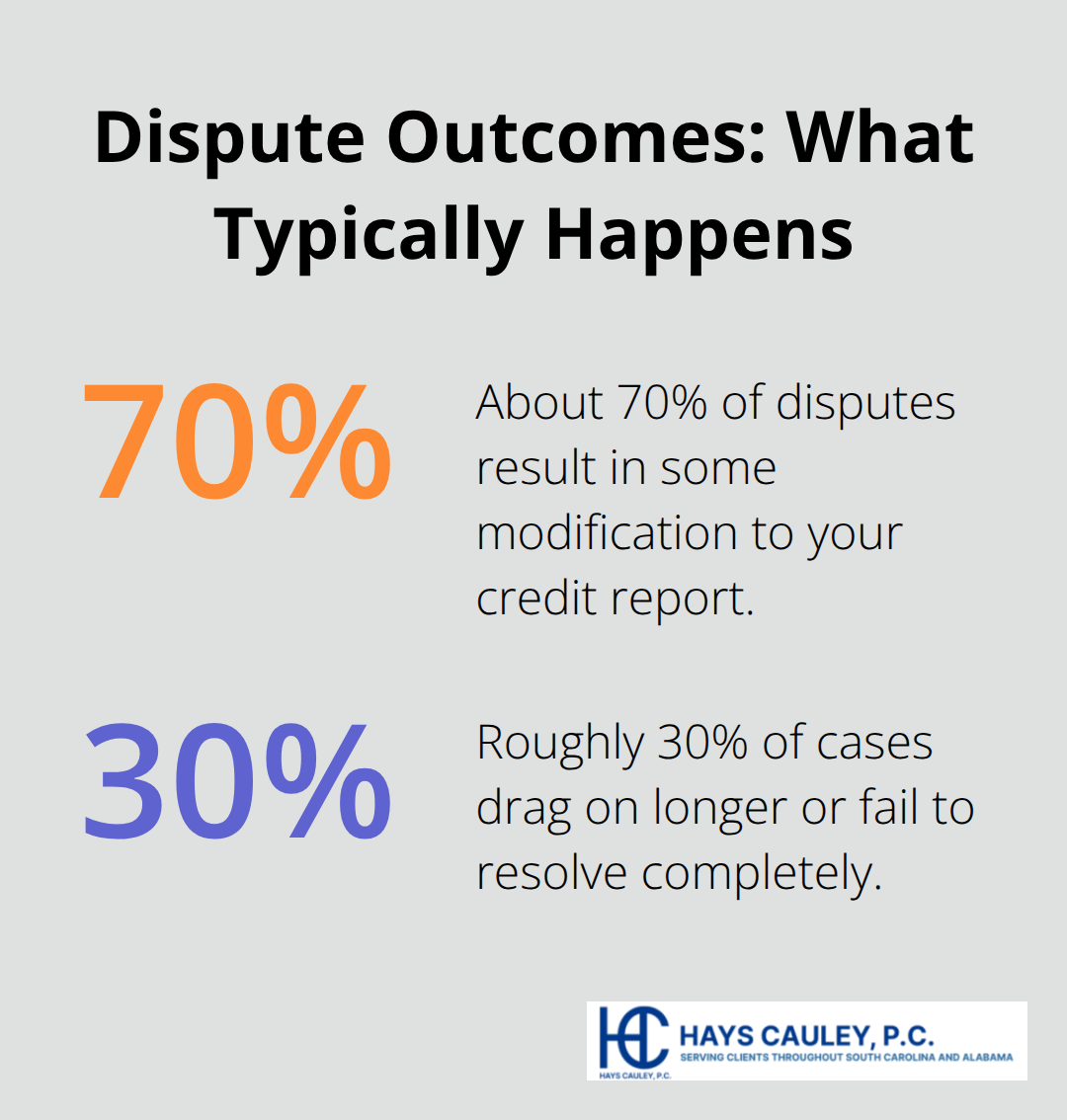

About 70% of disputes result in some modification, but many issues remain partially unresolved because furnishers ignore dispute notices or fail to conduct reasonable investigations. If you don’t actively challenge errors, they persist on your file uncorrected. The longer you wait, the more damage compounds to your credit profile and borrowing power. Understanding how these errors occur is the first step toward fixing them-and taking action requires knowing exactly what mistakes appear on your reports and how to document them properly.

Steps to Challenge Inaccurate Information on Your Credit Report

Obtaining Your Credit Reports for Free

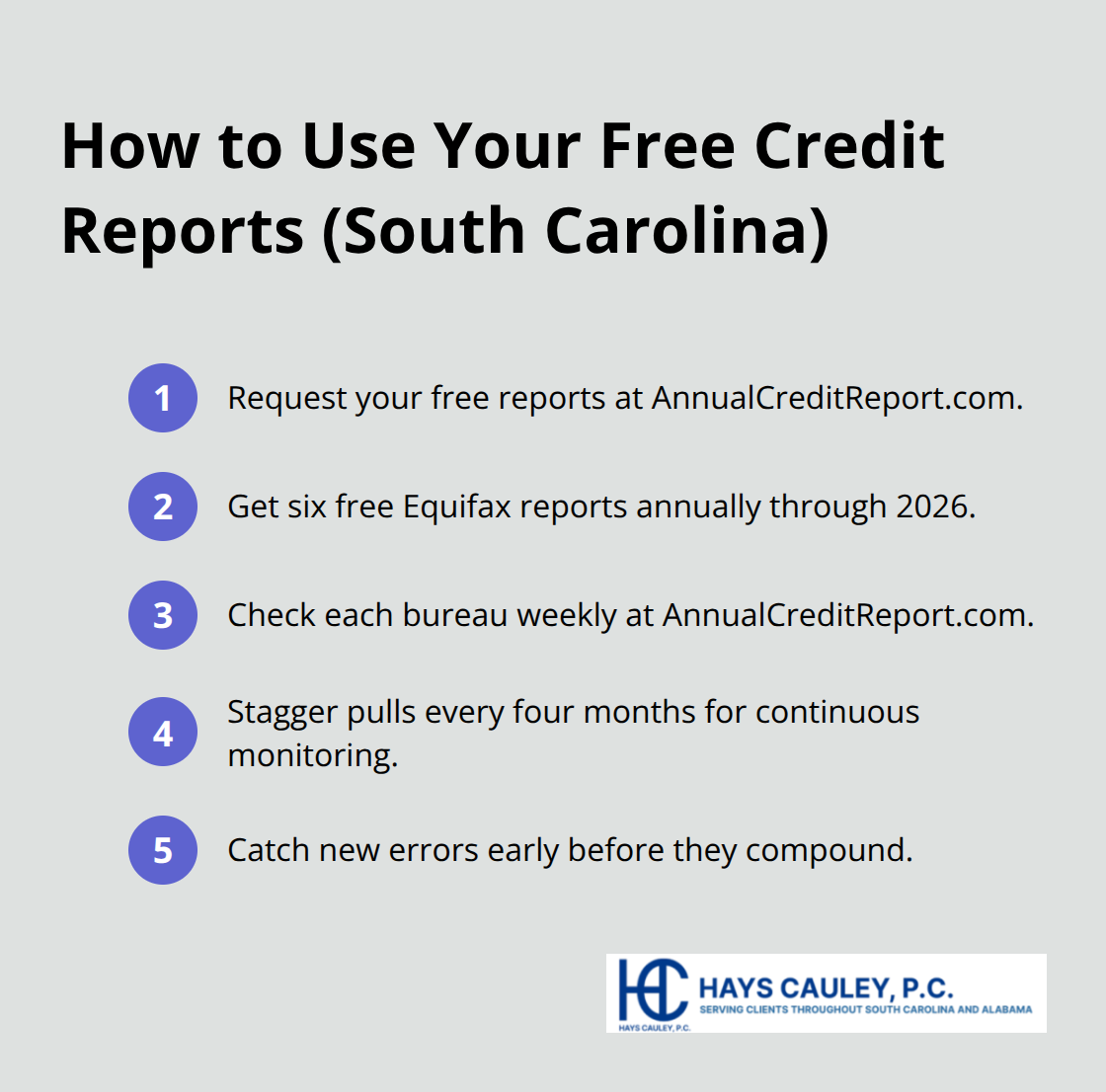

Start by pulling your credit reports from annualcreditreport.com, the official FTC-managed source where you can request free reports from Equifax, Experian, and TransUnion without entering a credit card. South Carolina residents gain an additional advantage: Equifax offers six free credit reports annually through 2026, available by visiting equifax.com or calling 1-866-349-5191. The FTC now allows you to check each bureau’s report for free once weekly at annualcreditreport.com, on top of your standard annual reports.

Pull one report from each bureau now, then stagger the remaining reports every four months for continuous visibility throughout the year. This rotating approach catches new errors before they compound.

Reviewing Your Reports for Errors

When you open your reports, start with the personal information section. Verify the correct spelling of your name, your Social Security number, and all current and previous addresses. Mixed-file errors occur frequently when bureaus confuse similar names or SSNs, so catching these details prevents future damage. Next, scan the accounts section for unfamiliar creditors, unknown credit cards, or collection agencies you don’t recognize. Verify that each account’s status, payment history, dates opened, and balances match your actual records. Check credit limits and current balances to spot inflated utilization that hurts your score. Review the inquiries section carefully for hard inquiries from lenders you didn’t authorize; multiple inquiries in a short period signal potential fraud.

Documenting the Errors You Find

Create a simple spreadsheet that documents the exact error, the account number, which bureau reported it, and supporting evidence like bank statements or creditor correspondence. This documentation becomes your dispute roadmap and proves invaluable when filing complaints. List each inaccuracy with precision-note the account name, the reported balance versus your actual balance, payment status discrepancies, and any fraudulent accounts. Attach copies of statements, receipts, or correspondence that contradict what the bureaus report. The more thorough your documentation, the stronger your case when you submit disputes to both the bureaus and the furnishers.

Filing Your Dispute the Right Way

Dispute the bureaus in writing rather than online or by phone. Include the exact error, copies of supporting documents, and a copy of your credit report. Send everything via certified mail with return receipt to the disputes department at the correct address: Equifax Information Services LLC, P.O. Box 740256, Atlanta, GA 30348; Experian Information Solutions, P.O. Box 4500, Allen, TX 75013; or TransUnion LLC Consumer Dispute Center, P.O. Box 2000, Chester, PA 19016. Keep your tracking numbers. On the same day you mail the bureau, notify the furnisher (the original creditor) with an identical dispute letter and documentation. Many furnishers ignore disputes, but sending written notice with supporting evidence triggers a dual investigation that increases pressure on both parties to respond.

What Happens After You File

South Carolina law requires bureaus to reinvestigate within 30 days and provide results in writing. If the item cannot be verified by the furnisher, the bureau must remove it. About 70 percent of disputes result in some modification to your credit report, though persistence matters because many issues remain partially unresolved on the first attempt.

If your initial dispute does not produce the results you need, you can file again with additional documentation or escalate your complaint to the Consumer Financial Protection Agency. The investigation process takes time, and some errors require multiple rounds of disputes before removal occurs.

What to Expect During the Dispute Process

The 30-Day Investigation Window

The 30-day investigation window that South Carolina law requires is a hard deadline, but it does not mean your case closes at day 31. Bureaus often conduct cursory investigations, sending minimal inquiries to furnishers and accepting their responses without pushing back when information is vague or incomplete. The furnisher must conduct what the law calls a reasonable investigation, but many creditors and collection agencies treat dispute letters as nuisances and respond with form letters claiming they verified the account without actually reviewing your documentation.

Why Persistence Matters in Disputes

This is where persistence matters. Most disputes resolve within 30 to 90 days, but roughly 30 percent of cases drag on longer or fail to resolve completely. The Consumer Financial Protection Agency reported that TransUnion’s relief rate fell about 50 percent in 2025, and Experian’s share of successful resolutions dropped from approximately 20 percent in 2024 to under 1 percent in 2025, meaning the bureaus are increasingly resistant to removing errors even when evidence supports your claim. After the bureau completes its investigation, you receive written results. If the item is removed, you get a free updated credit report and the correction must be reported to the other two bureaus and anyone who received your report in the past six months.

What to Do When Disputes Fail

If the bureau denies your dispute, do not stop. You have the right to add a written statement of dispute to your file that appears on future reports. File a complaint with the CFPB by calling 855-411-2372 or visiting their website. The complaint goes directly to the bureau and furnisher, and the agency tracks whether they respond within required timeframes.

Your Rights Under Federal Law

The Fair Credit Reporting Act gives you the right to dispute inaccurate information, receive investigation results in writing, and demand removal of items the furnisher cannot verify. If a bureau violates the FCRA through willful misconduct, you can pursue damages up to three thousand dollars per incident plus attorney fees. Negligent violations carry at least one thousand dollars per incident in damages. South Carolina law mirrors and reinforces these protections, with similar damage thresholds and the added requirement that if a bureau fails to correct inaccurate information within 10 days after a judgment, damages increase to one thousand dollars per day until the correction occurs.

When Legal Help Becomes Necessary

Many furnishers ignore disputes because they bet consumers will not pursue legal action. An attorney letter referencing the FCRA often prompts immediate accountability because furnishers know the liability exposure. If your disputes stall after 90 days, the error persists despite your documentation, or identity theft complications arise, legal help becomes worthwhile. We at Hays Cauley, P.C. help South Carolina residents including those in Greenville, Columbia, and Charleston navigate these disputes and hold bureaus and furnishers accountable when they refuse to correct errors.

Final Thoughts

Challenging credit report errors in South Carolina requires action on your part. You must obtain your free reports, document the inaccuracies, file written disputes with certified mail, and follow through when bureaus fail to respond. About 70 percent of disputes result in some modification, which means most errors can be removed if you persist and provide solid documentation.

A single error costs you thousands in higher interest rates over the life of a mortgage or loan. Your credit report affects your ability to borrow, the rates you receive, and even employment or housing decisions. Taking control of your data now prevents years of damage later.

If your disputes stall after 90 days, the error persists despite your documentation, or identity theft complications arise, legal help becomes necessary. Many furnishers ignore disputes because they assume consumers will not pursue accountability, but an attorney letter referencing the Fair Credit Reporting Act often prompts immediate action. We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, challenge credit report errors and hold bureaus and furnishers accountable when they refuse to correct them.