SC FCRA Attorney Finding The Right Legal Support

Your credit report shapes your financial future. Errors on that report-whether from a credit reporting agency’s mistake or identity theft-can cost you thousands in denied loans and higher interest rates.

We at Hays Cauley, P.C. help South Carolina consumers fight back against these violations. An SC FCRA attorney can force credit reporting agencies to fix inaccurate information and compensate you for the damage.

What the Fair Credit Reporting Act Actually Protects

The Fair Credit Reporting Act is a federal law that controls how credit reporting agencies, furnishers, and employers handle your personal financial data. Under the FCRA, you have three core rights: access to your credit file, the ability to dispute inaccuracies, and control over who sees your information. Credit reporting agencies process hundreds of millions of transactions daily, which means errors happen constantly. The three major bureaus-Equifax, Experian, and TransUnion-maintain files on roughly 200 million Americans, and studies show that one in four consumers find errors on their reports. These aren’t small mistakes; inaccurate reporting directly impacts loan approvals and interest rates. A single error can raise your mortgage costs by thousands of dollars or trigger an outright denial. The FCRA also protects you when employers, landlords, or insurance companies pull your report. They must have a permissible purpose to access it, and if they take adverse action based on your credit report, they must notify you and tell you which bureau they used.

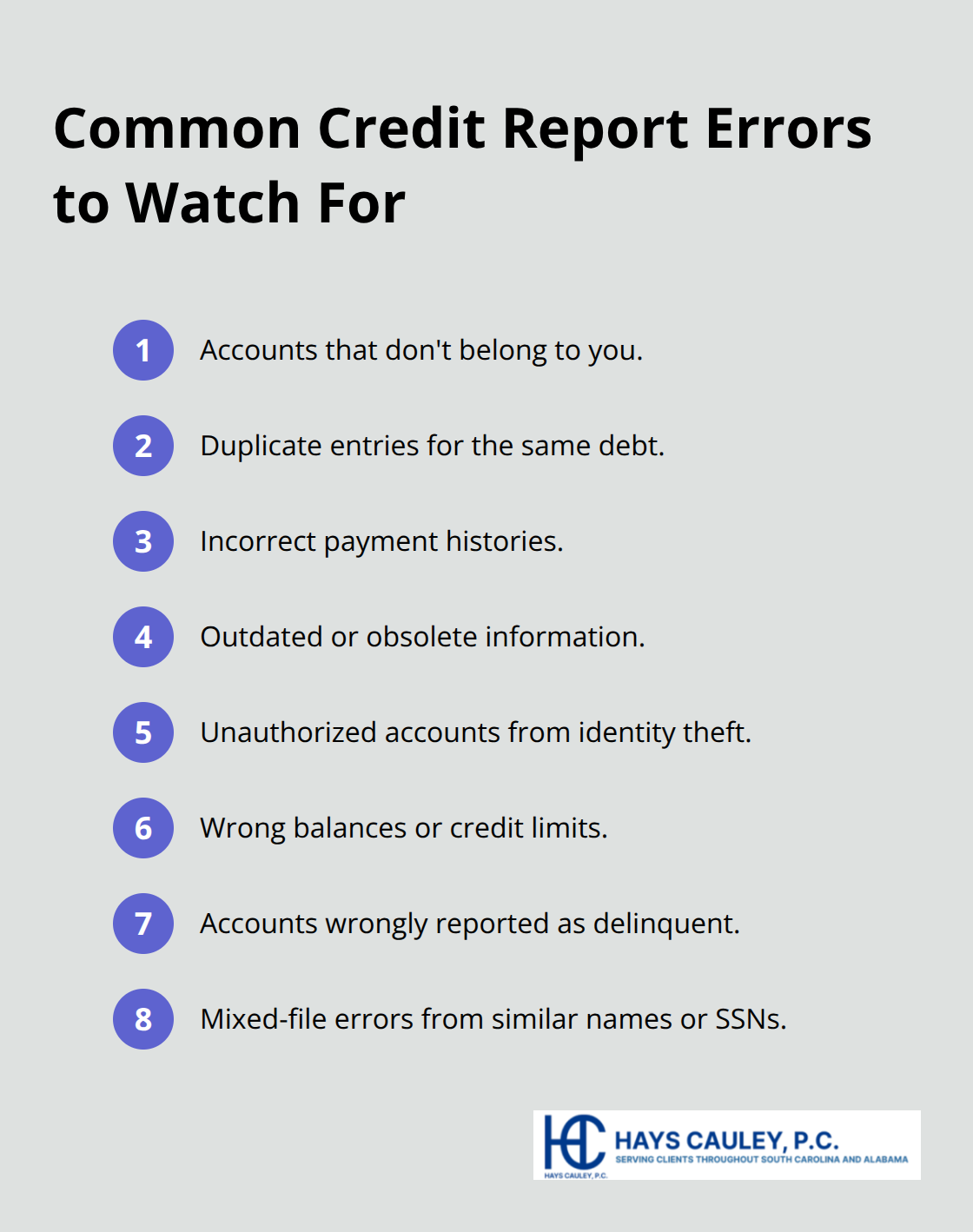

Common Errors That Destroy Your Credit

Accounts that don’t belong to you, duplicate entries, incorrect payment histories, and outdated information appear regularly on credit reports. Identity theft generates unauthorized accounts that can tank your score within weeks. Wrong balances, accounts marked as delinquent when you paid on time, and accounts belonging to someone with a similar name also show up frequently.

Credit bureaus must investigate disputes within 30 days and remove or correct unverifiable information, but many ignore this requirement entirely. When a bureau fails to remove inaccurate data after you’ve won a dispute, damages accrue up to $1,000 per day until correction. The statute of limitations is two years from discovery or five years from the violation, so delays cost you money and shrink your legal window. Continued reporting of disputed information represents the most actionable violation for recovering damages.

Financial Impact You Can Measure

A single late payment can lower your score by 100 points or more. Denied credit based on errors means lost opportunities-whether a mortgage, car loan, or rental approval. Higher interest rates from bad credit cost homebuyers an average of $40,000 over a 30-year mortgage. Identity theft victims spend an average of 200 hours resolving fraud, and many lose employment opportunities when background checks pull false information. Tenant screening errors block qualified renters from housing. Medical information companies and background check firms also fall under FCRA rules, so errors in those reports carry the same weight as credit bureau mistakes.

Why Credit Reporting Agencies Resist Corrections

Credit reporting agencies have little financial incentive to fix errors without legal pressure. They profit from volume, not accuracy. When you file a dispute, the bureau must investigate, but many conduct cursory reviews and report back that the information is verified-even when it isn’t. Furnishers (lenders, credit card companies) must respond to disputes and update reporting, yet they often ignore consumer complaints. This pattern of non-compliance continues because most consumers don’t know they can sue for violations. The FCRA allows you to recover actual damages, statutory damages up to $1,000 per violation, and attorney’s fees. Willful violations may result in punitive damages as well. This legal framework exists specifically to force agencies and furnishers to take disputes seriously.

What Happens When You Don’t Act

Inaccurate information stays on your report for years unless you challenge it. Each month that an error remains costs you in higher interest rates or missed credit opportunities. The longer you wait, the closer you move toward the statute of limitations deadline. Once that window closes, you lose your right to sue for damages. Your credit score reflects the damage, and rebuilding takes time even after corrections occur. The financial harm compounds-denied mortgages, rejected rental applications, and lost job offers all stem from a single error that a credit bureau could have fixed in 30 days.

Understanding what the FCRA protects is the first step. The next step is recognizing when violations have occurred in your own credit file and knowing what legal options exist to force corrections and recover damages.

When You Need an FCRA Attorney in South Carolina

Disputes That Stall With Credit Bureaus

Most consumers attempt to handle credit report errors alone. They shouldn’t. The moment a dispute stalls with a credit bureau, you lose leverage and time works against you. When you file a written dispute and receive no satisfactory response within 30 days, the credit reporting agency violates the FCRA. The law requires investigation and a response; silence or a form letter claiming the information is verified constitutes non-compliance. Credit bureaus must investigate disputes within 30 days and remove or correct unverifiable information, yet many ignore this requirement entirely. At that point, legal action becomes necessary to force compliance.

Denied Credit, Employment, or Housing Based on Your Report

When denied credit, employment, housing, or insurance based on your credit report, you must receive notification that identifies the bureau involved. If you didn’t receive this notice, or if the information used was demonstrably false, you have a legal claim. Lenders, employers, and landlords cannot pull your report without a permissible purpose, and they cannot take adverse action without telling you which bureau they used. Many companies violate this requirement, leaving consumers unaware of why they were rejected. These violations carry the same damages as inaccurate reporting itself.

Identity Theft and Unauthorized Accounts

Identity theft creates unauthorized accounts that spiral quickly. A single fraudulent account can lower your score 100 points within weeks. Attempting to resolve identity theft alone means fighting with multiple furnishers and bureaus simultaneously while your credit deteriorates daily. The statute of limitations is two years from discovery or five years from the violation, so delays shrink your legal window. Clients who wait six months before seeking help often discover that their remaining window has contracted from five years to just 18 months. That delay costs thousands in potential damages.

The Financial Case for Legal Action

The financial threshold for hiring an attorney is lower than most people think. A mortgage denied due to a reporting error costs you an average of $40,000 30 years in higher interest rates. A rental application rejected because of tenant screening report errors means months of housing instability. An employment opportunity lost to background check inaccuracies cannot be recovered. If your credit report contains errors that impact major financial or life decisions, legal representation pays for itself immediately.

South Carolina law allows you to recover actual damages, statutory damages up to $1,000 per violation, and attorney’s fees when you win. This means you don’t pay out of pocket. Many consumer protection law firms work on a contingency basis for qualifying cases, which means you pay nothing unless they recover money for you. The FCRA exists specifically to make credit reporting agencies and furnishers accountable. Without legal action, they have no reason to fix errors or compensate you for harm. With legal action, they must respond.

Knowing when to hire an attorney is one part of the equation. Knowing what to look for in that attorney determines whether you actually recover damages and restore your credit.

What to Look for in an SC FCRA Attorney Serving South Carolina, Including Greenville, Columbia and Charleston

Track Record in FCRA Litigation

Finding the right FCRA attorney in South Carolina means examining what actually matters: whether the firm has won cases, understands South Carolina’s legal landscape, and structures fees so you pay nothing upfront. Most FCRA cases settle or resolve through litigation, and the difference between a firm that recovers $5,000 for you and one that recovers $50,000 comes down to experience and leverage. Ask potential attorneys for specific case outcomes, not vague claims about success. A firm that has resolved FCRA disputes, including both individual and class-wide cases, demonstrates the ability to handle complexity and scale. You need someone who has actually sued credit bureaus and furnishers, not someone handling FCRA cases as a side practice.

South Carolina Consumer Protection Law Knowledge

South Carolina has its own consumer protection statutes that layer on top of federal FCRA rights, and an attorney unfamiliar with state law leaves money on the table. South Carolina allows recovery of actual damages, statutory damages up to $1,000 per violation, and attorney’s fees, but an attorney must know how to plead and prove each element under both federal and state frameworks. When you call a firm, ask directly: Have you filed FCRA lawsuits in South Carolina federal court? Do you know the differences between FCRA claims and South Carolina consumer protection claims? Can you cite specific recent cases you’ve handled? Vague answers mean the attorney lacks depth in this practice area.

Contingency Fee Structure and Cost Alignment

Contingency representation separates serious FCRA firms from those treating the practice as occasional work. A contingency basis means you pay nothing unless the attorney recovers money for you. This structure aligns incentives perfectly: the firm only profits if you win, so they fight harder and turn down cases that lack merit. When an attorney asks for upfront fees or hourly rates for FCRA work, they have less motivation to maximize your recovery. The statute of limitations runs two years from discovery or five years from the violation, and delays shrink your window. An attorney working on contingency moves fast because time erodes both your rights and their potential fee.

Ask whether the firm covers costs like filing fees, expert reports, and discovery expenses during the case, or whether you pay those out of pocket. Quality FCRA firms absorb these costs because they expect to recover them from the defendant. If a firm quotes you an hourly rate or retainer for FCRA work, ask why they don’t work on contingency. The answer often reveals doubt about case strength or a business model built on hourly billing rather than results.

Initial Consultation and Case Assessment

Your initial consultation should be free, and the attorney should spend time reviewing your credit reports and dispute history before committing to representation. That investment of time signals confidence in the case and commitment to your outcome. A thorough review takes more than a few minutes-the attorney must examine what errors appear on your report, when you filed disputes, what responses you received from credit bureaus, and whether furnishers ignored your complaints. This detailed assessment determines whether your case has merit and what damages you can recover. An attorney who rushes through this process or commits to representation without examining your documents will likely produce weak results.

Final Thoughts

Credit reporting errors cost you thousands in denied loans and rejected applications, and the statute of limitations window shrinks with every passing month. Once that deadline passes, you lose your right to recover damages entirely. An SC FCRA attorney forces credit reporting agencies and furnishers to comply with federal law by investigating your reports, identifying violations, and demanding corrections backed by legal authority. When agencies refuse to act, your attorney files a lawsuit seeking actual damages for financial harm, statutory damages up to $1,000 per violation, and recovery of attorney’s fees.

We at Hays Cauley, P.C. help South Carolina consumers recover from credit reporting violations and work on a contingency basis for qualifying cases, which means you pay nothing unless we recover money for you. Your initial consultation is free, and we review your credit reports and dispute history thoroughly before committing to representation. This approach aligns our success with yours, and you can reach us at 843-665-1717 or through our website.

Start by gathering your credit reports from Equifax, Experian, and TransUnion through annualcreditreport.com and document any errors you find. If disputes have stalled, if you were denied credit based on inaccurate information, or if identity theft created unauthorized accounts, contact us now. The two-year statute of limitations window is real, and delays cost you thousands in potential recovery.