Credit Dispute Lawyer SC When To Call a Specialist

A credit dispute lawyer SC can make the difference between fixing errors on your report and watching them damage your finances for years. Inaccurate information on your credit file costs you money through higher interest rates and rejected loan applications.

We at Hays Cauley, P.C. help South Carolina residents challenge credit bureaus and reporting agencies when they get the facts wrong. This guide shows you when to fight alone stops working and why professional help matters.

When DIY Credit Disputes Fail

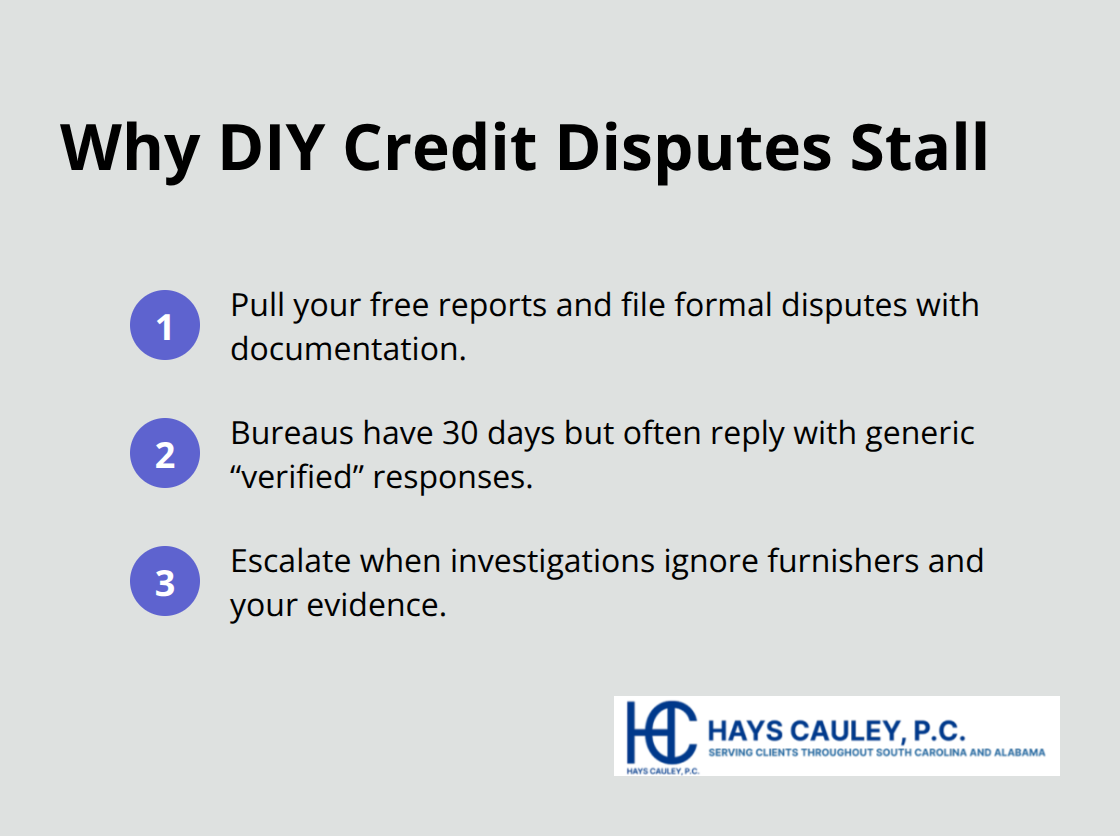

Most people try handling credit disputes alone first, and many hit a wall within weeks. The FTC reported over 175,000 credit reporting complaints in 2020, yet about 1 in 5 consumers find errors on at least one of their three reports from Equifax, Experian, or TransUnion. Pulling your free annual report from annualcreditreport.com and filing a formal dispute with documentation sounds straightforward, but credit bureaus often dismiss disputes without meaningful investigation. When you send a dispute letter citing a wrong balance or misreported late payment, the bureau has 30 days to investigate, but many send back generic responses claiming the data is verified even though they never actually contacted the furnisher or reviewed your supporting documents.

If you discover an inaccurate late payment that costs you 0.5 to 1 percent higher interest rates on a $300,000 mortgage, that error translates to roughly $1,500 to $3,000 more per year. The Fair Credit Reporting Act gives you a two-year window from discovery or five years from the error occurrence to pursue legal action, but delays cost you financially every single month the error remains.

Why Bureaus Ignore Your Disputes

Credit bureaus process thousands of disputes daily and have little incentive to remove accurate-looking data, even if your documentation proves otherwise. The Consumer Financial Protection Bureau recently updated credit report dispute procedures to require more meaningful investigation and clearer responses from furnishers, but implementation remains uneven across the industry. Many consumers resubmit disputes multiple times, only to receive the same dismissal. The CFPB now expects bureaus to provide robust explanations instead of generic statements, yet many still fail to meet this standard. If a late payment, duplicate account, or fraudulent entry remains after your own attempts, you need someone who understands how to escalate beyond the standard 30-day process. An attorney can draft a demand letter citing specific FCRA violations, document the bureau’s failure to investigate properly, and threaten litigation if corrections don’t follow.

The Real Cost of Waiting

Inaccurate credit reports damage your financial life immediately and compound over time. Unfamiliar accounts on your report can indicate identity theft, risking score damage and unknown collection calls that follow you for months. Incorrect payment histories block mortgage approvals, refinancing, and job opportunities in fields requiring credit checks. The longer an error sits on your file, the more interest you pay and the harder it becomes to prove the mistake was the bureau’s fault rather than yours. If you’ve already spent 60 to 90 days disputing without resolution, waiting longer means losing ground on that two-year legal window.

When to Stop Fighting Alone

A credit dispute attorney reviews your entire dispute history, identifies where the bureau failed its legal obligations, and accelerates corrections through demand letters and litigation if necessary. Federal penalties under the FCRA include up to $1,000 per violation plus actual damages and attorney fees, which means bureaus face real consequences when they ignore your rights. Timeline expectations run 30 to 90 days for dispute resolution through demand letters; 6 to 12 months for litigation, with the legal window closing after discovery (two years) or occurrence (five years). Local South Carolina representation brings familiarity with SC courts, judges, and asset-exemption considerations that can impact credit disputes and judgments. When selecting an attorney, verify they routinely handle cases under both federal and SC law and aren’t a generalist handling credit disputes as a minor service. In your initial consultation, ask whether they’ve filed SC suits and recovered damages under both federal and state theories, and request concrete examples based on your dispute history.

How a Credit Dispute Lawyer Wins Your Case

An attorney fighting credit reporting errors operates in a completely different arena than the DIY dispute process. When you file your own dispute with Equifax, Experian, or TransUnion, you work within a system designed to process volume, not accuracy. A lawyer shifts the burden back onto the credit bureaus by invoking their statutory obligations under the Fair Credit Reporting Act. The FCRA requires bureaus to conduct a reasonable investigation when you dispute an item, which means actually contacting the furnisher of the data and reviewing the documents you submit. Most bureaus skip this step entirely and send form-letter responses that claim verification without evidence.

How Attorneys Shift the Legal Burden

An attorney documents bureau failures through demand letters that cite specific FCRA violations and threaten litigation if corrections don’t follow within a defined timeframe. Federal law allows you to recover up to $1,000 per violation plus actual damages and attorney fees, which creates genuine financial pressure on bureaus to investigate properly rather than dismiss your claim outright. The CFPB’s updated dispute procedures now require more meaningful investigation and clearer explanations from furnishers, yet many bureaus still drag their feet. An experienced lawyer knows exactly which violations to highlight and how to escalate beyond the standard 30-day process that traps most consumers in endless cycles of rejection.

Identifying What Bureaus Actually Violated

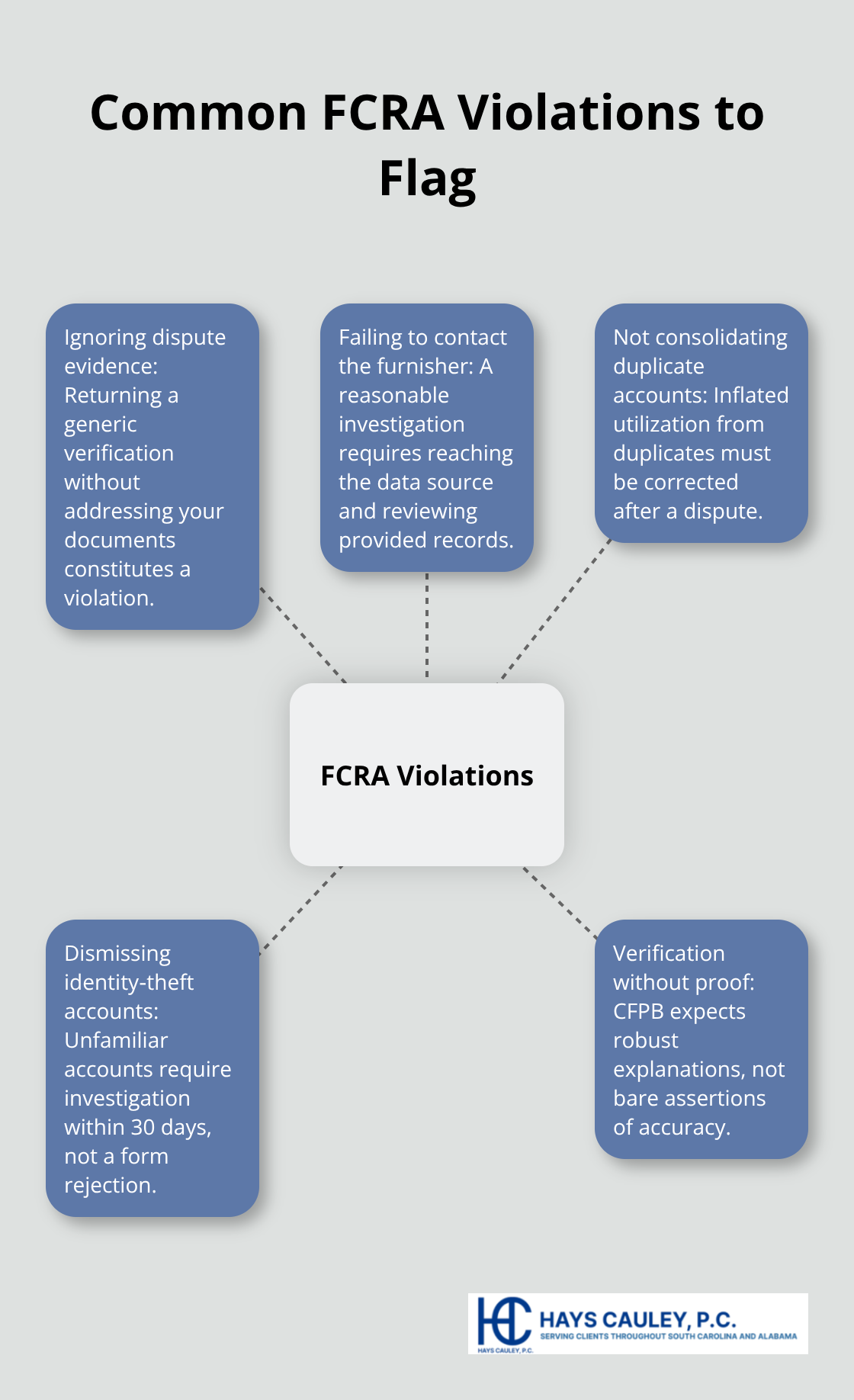

Your attorney starts by reviewing your complete dispute history to pinpoint where the bureau failed its legal obligations. If you submitted documentation proving a late payment never occurred or that a balance is wrong, yet the bureau returned a generic verification letter without addressing your evidence, that constitutes an FCRA violation. Duplicate accounts that inflate your credit utilization also trigger violations when bureaus fail to consolidate them after dispute.

Unfamiliar accounts signaling identity theft must receive investigation within 30 days, not dismissal.

A lawyer examines whether the furnisher actually responded to the bureau’s inquiry or whether the bureau simply assumed the data was correct. The Consumer Financial Protection Bureau now expects bureaus to provide robust explanations instead of claiming verification without proof, yet enforcement remains inconsistent. An attorney documents each failure methodically, building a record that proves the bureau chose convenience over compliance. This documentation becomes your leverage in settlement negotiations or the foundation of a lawsuit that forces corrections and compensation. Your two-year legal window from discovery or five years from occurrence closes fast, so an attorney moves quickly to identify violations while evidence remains fresh.

Building Leverage Through Demand Letters

A demand letter from an attorney carries weight that your personal dispute never will. The letter cites specific FCRA requirements, references the bureau’s documented failure to investigate properly, attaches copies of your original dispute and supporting documents, and quantifies the financial harm caused by the inaccuracy. If an incorrect late payment costs you 0.5 to 1 percent higher interest on a $300,000 mortgage, that equals $1,500 to $3,000 annually in additional costs, which your attorney calculates and includes.

The letter gives the bureau a defined deadline, typically 14 to 30 days, to correct the error or face litigation. Many bureaus respond within this window because their internal cost analysis shows that correcting the error costs far less than defending a lawsuit. An attorney familiar with South Carolina courts and judges understands which threats carry credibility in your jurisdiction. The demand letter process typically resolves disputes within 30 to 90 days without courtroom involvement, saving you months of waiting and stress.

What Happens When Bureaus Refuse to Settle

Once violations are documented, many bureaus settle rather than face litigation costs and potential statutory damages that exceed the cost of correcting errors immediately. If a bureau refuses to respond to your demand letter or continues to deny the violation, your attorney moves toward filing suit in South Carolina courts. Federal penalties under the FCRA include up to $1,000 per violation plus actual damages and attorney fees, which means bureaus face real consequences when they ignore your rights. Timeline expectations run 30 to 90 days for dispute resolution through demand letters; 6 to 12 months for litigation, with the legal window closing after discovery (two years) or occurrence (five years). An attorney who understands South Carolina’s asset-exemption rules and local court procedures can navigate these complexities far more effectively than you can alone.

The next step involves understanding what to expect when you actually hire an attorney and begin the formal process of challenging your credit report.

What to Expect When Working With a Credit Dispute Lawyer Serving South Carolina, Including Greenville, Columbia and Charleston

Initial Consultation and Case Evaluation

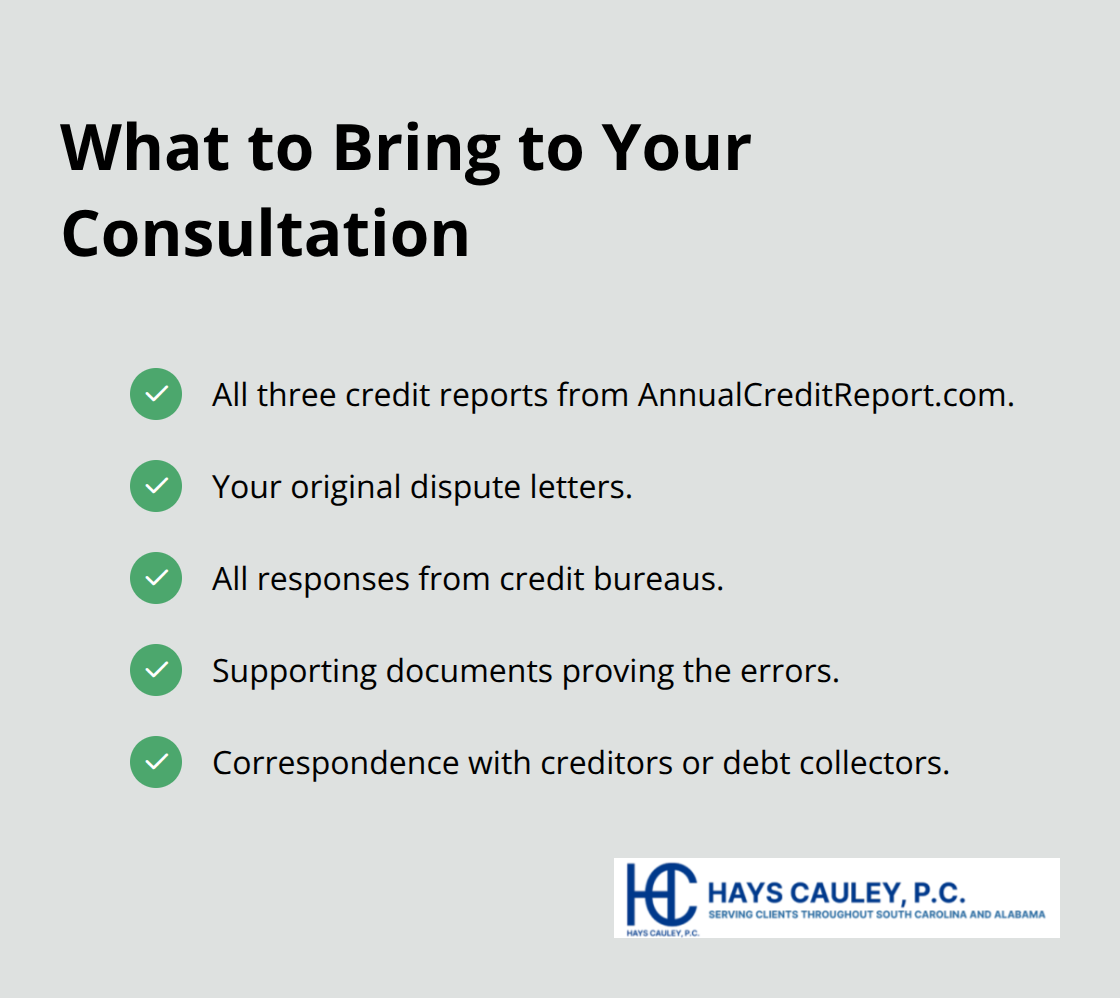

Your initial consultation determines whether your case justifies litigation or settles through a demand letter, so arrive prepared with complete documentation. Bring copies of all three credit reports pulled from annualcreditreport.com, your original dispute letters, any responses from credit bureaus, supporting documents proving the errors, and correspondence with creditors or debt collectors. An attorney reviews this material to identify specific FCRA violations and calculate your potential damages based on actual financial harm.

If an inaccurate late payment costs you 0.5 to 1 percent higher interest on a mortgage, that translates to real dollars your attorney quantifies immediately.

The consultation typically lasts 30 minutes to an hour and costs $50 or less through the South Carolina Bar Association Lawyer Referral Service, making it an affordable first step. During this meeting, ask directly whether the attorney has filed suits in South Carolina courts and recovered damages under both federal and state law. Request concrete examples tied to similar disputes, not hypothetical scenarios. Clarify the fee structure upfront: some firms charge for demand-letter work while others operate entirely on contingency, meaning they collect only if you recover compensation. This distinction matters because it affects your net recovery and the attorney’s incentive to settle quickly versus litigate aggressively.

The Dispute Process and Timeline

Your attorney typically sends a demand letter within two to four weeks, citing specific FCRA violations and setting a 14 to 30-day deadline for the bureau to correct errors or face litigation. Many bureaus respond within this window because their cost analysis shows correction costs less than defense litigation. If the bureau ignores the demand letter or refuses to acknowledge violations, your attorney files suit in South Carolina court within 60 to 90 days.

Litigation timelines extend six to 12 months from filing to resolution, but your two-year legal window from discovery closes fast, so moving quickly matters. The demand letter process typically resolves disputes within 30 to 90 days without courtroom involvement, saving you months of waiting and stress. An attorney familiar with South Carolina’s courts and judges understands which threats carry credibility in your jurisdiction and navigates these proceedings far more effectively than DIY litigation.

Potential Outcomes and Compensation

Potential outcomes include corrected credit reports sent to lenders who accessed your file, statutory damages of up to $1,000 per FCRA violation plus actual damages, and attorney fees paid by the bureau. Most cases settle before trial because bureaus understand the financial exposure. Settlement amounts depend on the number of violations, the severity of financial harm, and how thoroughly your attorney documents the bureau’s failure to investigate properly.

Federal penalties under the FCRA create genuine leverage in negotiations. When your attorney quantifies the financial harm (such as $1,500 to $3,000 annually in higher mortgage interest), bureaus recognize that settling costs far less than litigation. An attorney who understands South Carolina’s asset-exemption rules and local court procedures can navigate these complexities far more effectively than you can alone, positioning your case for maximum recovery.

Final Thoughts

Credit disputes that linger unresolved drain your finances month after month through higher interest rates, rejected loan applications, and missed opportunities. The Fair Credit Reporting Act gives you legal rights, but exercising those rights requires understanding where credit bureaus fail their obligations and documenting those failures methodically. A credit dispute lawyer SC can identify violations you’d miss on your own, draft demand letters that force meaningful investigation, and recover statutory damages when bureaus ignore your rights.

Federal penalties of up to $1,000 per violation plus actual damages create real leverage that transforms your case from a dismissed DIY dispute into a credible legal threat. Your two-year legal window from discovery closes fast, so you need to move quickly to identify violations while evidence remains fresh and your rights remain actionable. Contact Hays Cauley, P.C. for an initial consultation and bring copies of your three credit reports, dispute letters, bureau responses, and supporting documents that prove the errors.

An affordable consultation typically costs $50 or less through the South Carolina Bar Association Lawyer Referral Service and determines whether your case justifies litigation or settles through demand letters. Stop waiting for credit bureaus to correct mistakes on their own. Take action today and protect your financial future from the damage inaccurate reporting causes.