A mistake on your credit report can cost you thousands of dollars in higher interest rates and rejected loan applications. Bureau data correction in SC is your legal right, and many South Carolinians don’t realize how quickly they can fix these errors.

At Hays Cauley, P.C., we help residents throughout Greenville, Columbia, and Charleston challenge inaccurate information and reclaim their financial standing. This guide walks you through your options and the steps that actually work.

What Errors Show Up Most Often on South Carolina Credit Reports

Duplicate Accounts and Payment Status Mistakes

Duplicate accounts rank as the most damaging errors we see on South Carolina credit reports. A single debt appears twice under slightly different names or account numbers, artificially tanking your score without any legitimate reason. Incorrect payment statuses follow closely behind-accounts marked as late when you paid on time, or active accounts you closed years ago still showing as open. The FTC found that about 1 in 5 consumers have an error on at least one of their three credit reports, and roughly 1 in 4 errors are serious enough to affect creditworthiness.

Unrecognized Accounts and Personal Information Errors

Unrecognized accounts signal identity theft or administrative mix-ups, and inflated balances misrepresent how much debt you actually carry. Personal information errors like wrong addresses, misspelled names, or incorrect Social Security numbers seem minor but can trigger fraud alerts and prevent legitimate credit applications from going through. South Carolina residents report seeing accounts that belong to someone else entirely, outdated debts marked as current, and closed accounts refusing to disappear from their files.

How Errors Tank Your Score and Cost You Money

A single error can drop your credit score by 50 to 100 points depending on what the mistake is and your overall profile. When your score drops, lenders charge you higher interest rates on mortgages, auto loans, and credit cards-sometimes costing thousands of dollars over the life of the loan. Employers increasingly pull credit reports for hiring decisions, and an error can cost you a job offer. Apartment applications get denied. Insurance rates climb.

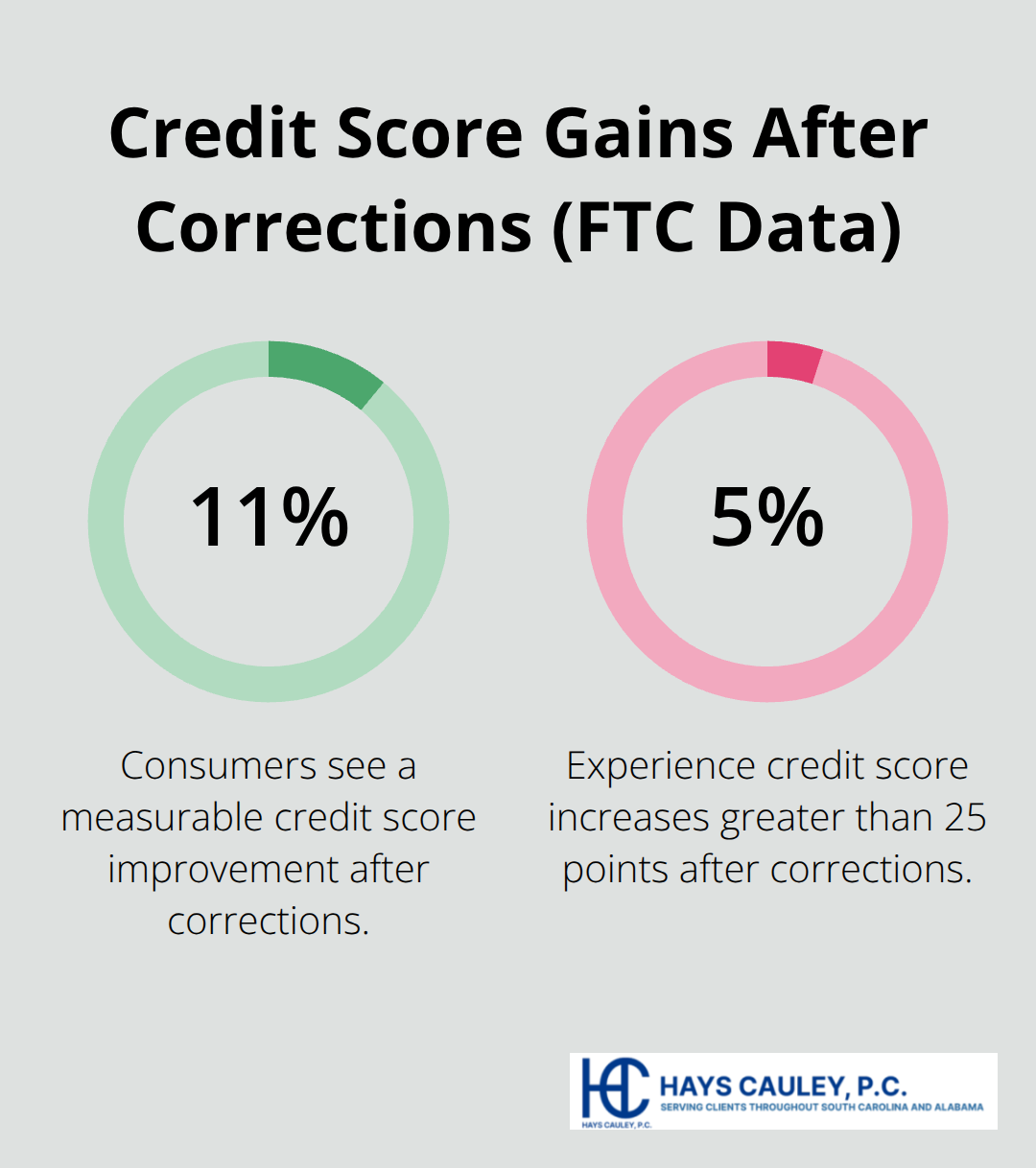

The average South Carolina resident carries about $5,700 in debt, and credit report errors make that debt far more expensive to manage. FTC data show that roughly 11% of consumers see a measurable score improvement after corrections, with about 5% experiencing changes greater than 25 points. Those 25-point improvements translate directly into lower interest rates and better loan terms.

The longer an error stays on your report (inaccurate information can remain for up to seven years), the more damage it inflicts, compounding financial losses month after month.

Understanding what errors appear on your report and how they damage your finances sets the stage for taking action. The next section walks you through obtaining your credit reports and identifying which errors actually belong on your file.

Getting Your Credit Reports and Starting Your Dispute

Obtain Your Free Credit Reports Immediately

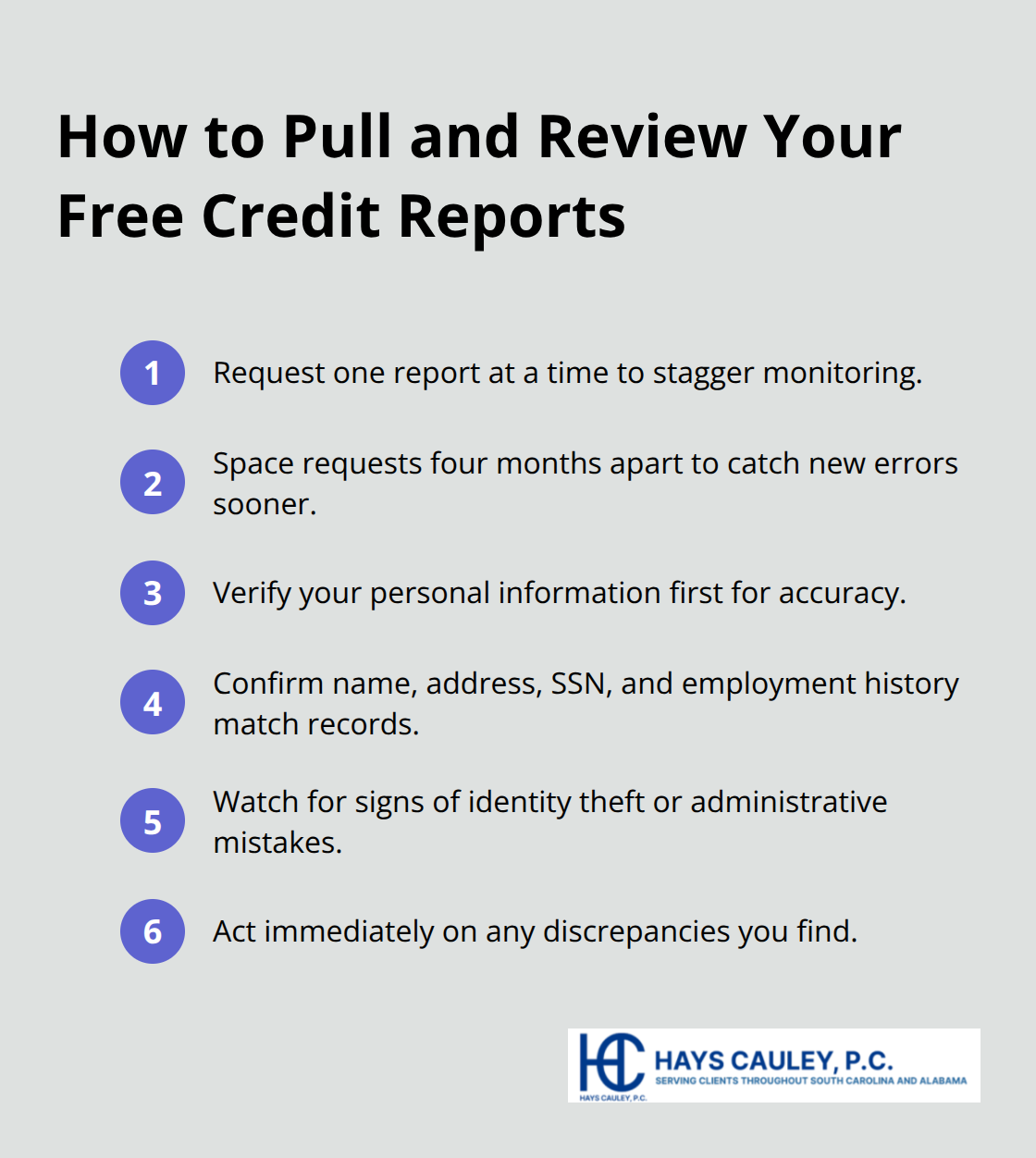

Visit AnnualCreditReport.com, the only government-authorized source for complimentary annual reports. Many South Carolinians waste time on imposter sites that charge fees when legitimate reports cost nothing. Request one report at a time rather than all three simultaneously-space them four months apart so you catch new errors faster and maintain continuous monitoring throughout the year. When your reports arrive, verify personal information first: confirm your name, address, Social Security number, and employment history match your actual records. Errors here signal identity theft or administrative mistakes that require immediate attention.

Scan for Common Errors on Your Report

Next, scan every account listing for status, payment dates, credit limits, and balances. Flag accounts you don’t recognize, closed accounts still showing as active, duplicate entries of the same debt under different names or numbers, and balances that don’t match your records. Document each problem with the creditor name, account number, and specific details of what’s wrong. FTC data confirm that about 70% of consumers who dispute errors see some modification to their reports, meaning action genuinely works.

File Your Dispute With Credit Bureaus

The Fair Credit Reporting Act requires credit bureaus to investigate disputes within 30 days at no cost to you. Send your dispute in writing via certified mail with return receipt requested to create a legally verifiable paper trail-phone disputes leave no documentation if the bureau claims they never received your claim. Use the CFPB’s free template dispute letter to ensure you include your name, address, confirmation number from your credit report, the specific account numbers you’re challenging, a clear explanation of what’s wrong, and what correction you want made. Attach copies of supporting documents like bank statements, payment receipts, or creditor letters that prove your position. Mail separate dispute letters to each of the three bureaus since they maintain independent files.

Contact the Furnisher Directly

After filing with the bureaus, also contact the furnisher-the creditor or collection agency that originally reported the data-in writing with the same documentation. Furnishers typically have about 30 days to investigate and must notify all three bureaus if they find inaccurate information. Track your timeline carefully: disputes take approximately 30 days per bureau, so expect resolution within 4-6 weeks if the error is clear-cut.

Verify Corrections Across All Three Bureaus

Check your updated credit reports 30 to 45 days after filing to verify corrections actually appeared across all three bureaus. Persistence matters significantly in this process, and detailed record-keeping of every communication strengthens your position if escalation becomes necessary. If disputes stall or bureaus ignore your requests, you have additional legal options available under South Carolina and federal law that can accelerate resolution and hold credit reporting agencies accountable for their failures.

What South Carolina and Federal Law Require Credit Bureaus to Do

The 30-Day Investigation Requirement

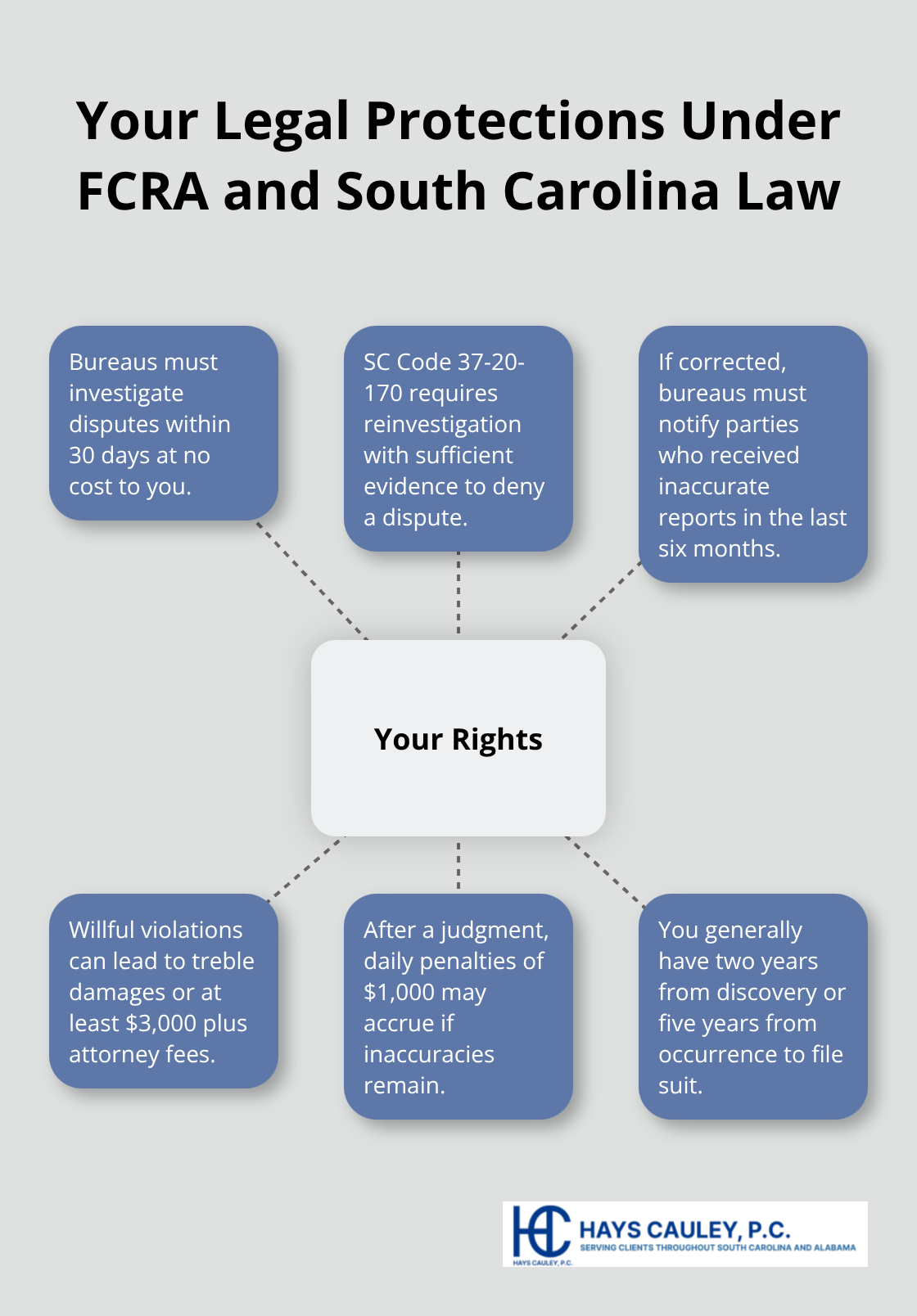

The Fair Credit Reporting Act sets strict federal requirements that credit bureaus must follow, and South Carolina law adds additional protections on top of those. Under the FCRA, credit bureaus must investigate your dispute within 30 days at no cost to you, and they cannot simply ignore your claim or delay indefinitely. South Carolina Code Section 37-20-170 requires that when you dispute an inaccuracy, the bureau must reinvestigate the item and provide sufficient evidence if they deny your dispute. This means they cannot hide behind vague responses or refuse to show their work.

Correction and Notification Obligations

If a dispute is resolved in your favor, the agency must correct the item and notify any party that previously received a report containing the inaccuracy within the last six months. This requirement stops the error from continuing to spread to lenders and employers. When an error gets corrected, request written confirmation from the bureau that the disputed item has been removed or updated. Many South Carolinians skip this step and later discover the error still appears on their file because the bureau failed to process the correction properly.

Damages for Willful and Negligent Violations

South Carolina law provides teeth to enforcement through damages. If a bureau willfully violates your rights, you can recover three times your actual damages or at least $3,000 per incident, plus attorney fees under South Carolina Code Section 37-20-170(D). Negligent violations carry actual damages or at least $1,000 per incident. Most importantly, if an injury to your creditworthiness results from the bureau’s failure to remove inaccurate information after a judgment against them, damages can increase by $1,000 per day until the correction is made.

Your Timeline for Legal Action

This daily penalty structure creates real financial pressure on bureaus to act quickly rather than drag out disputes indefinitely. Under the FCRA, you generally have two years from discovering the error or five years from its occurrence to file suit, giving you a substantial window to take action. The remedial provisions under South Carolina law are cumulative and allow civil actions to seek injunctions, operating in addition to other legal remedies. If bureaus resist corrections despite clear evidence, South Carolina residents have strong legal grounds to escalate beyond informal disputes and hold agencies accountable for their failures.

Final Thoughts on Bureau Data Correction SC

Fixing credit report errors takes time and persistence, but the financial payoff justifies the effort. Most disputes resolve within 30 to 45 days when you follow the process correctly, and FTC data show that roughly 70% of consumers who dispute errors see modifications to their reports. However, some situations demand professional help-if bureaus ignore your disputes, furnishers refuse to investigate, or errors persist after multiple attempts, working with a consumer protection attorney accelerates resolution and opens access to legal remedies unavailable through informal disputes alone.

We at Hays Cauley, P.C. handle credit reporting disputes from start to finish, including demand letters, bureau negotiations, and court representation when necessary. Our team reviews your dispute history, identifies statutory violations, and pursues damages under both federal and South Carolina law. Many South Carolinians discover that legal action resolves cases in weeks rather than months, and the damages recovered often exceed what informal disputes achieve.

After corrections appear, pull updated reports from all three bureaus within 60 days to confirm changes took effect across Equifax, Experian, and TransUnion. Set up automatic payments for all accounts going forward since payment history drives 35% of your credit score, and a single late payment can drop your score by 50 to 100 points. For complex situations or persistent bureau resistance, contact Hays Cauley, P.C. for a confidential consultation.