How To Fix Errors a Practical Guide To Credit Report Corrections

Your credit report shapes your financial life, yet errors on it are surprisingly common. We at Hays Cauley, P.C. know that inaccurate information can tank your credit score and cost you thousands in higher interest rates.

Learning how to fix errors on your credit report is one of the most powerful steps you can take. This guide walks you through identifying mistakes, disputing them, and protecting your rights.

What Errors Actually Appear on Credit Reports

Personal Information and Account Ownership Problems

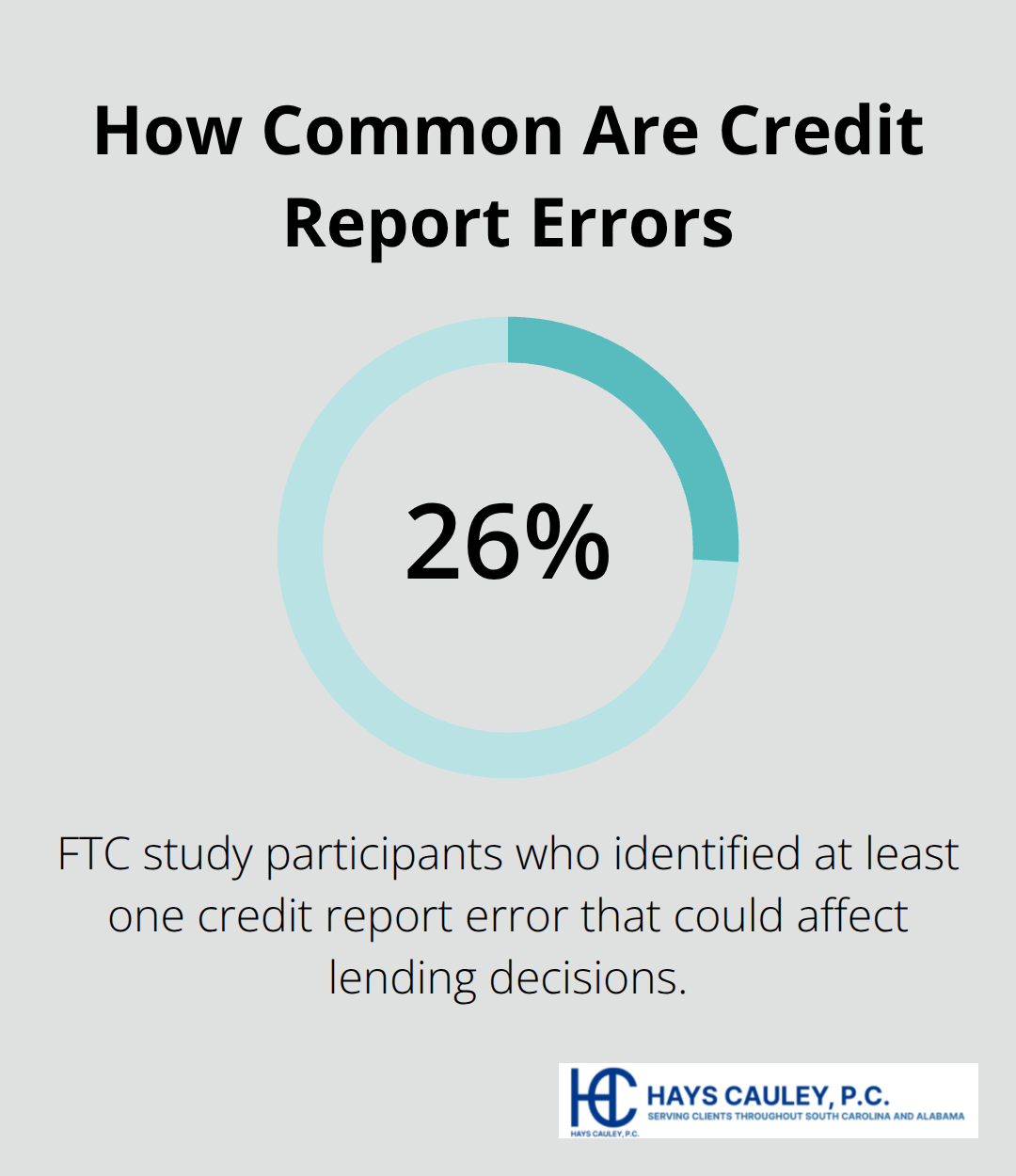

Credit report errors plague millions of Americans far more often than most people realize. The Consumer Financial Protection Bureau reports that incorrect information ranks as the top complaint about credit reports, and a Federal Trade Commission study found that 26% of participants identified at least one error on their credit report that could affect lending decisions. These aren’t rare edge cases-they’re systematic problems affecting your financial stability.

Personal information mistakes represent one category of errors you need to watch for closely. Name variations, address changes, Social Security number typos, or employer details can signal a mixed-file situation where your record has been combined with someone else’s. Scan your personal information section first before anything else, because these foundational errors often cascade into larger problems. Account ownership errors create another critical problem area-you might see accounts listed where you’re only an authorized user rather than the actual owner, which incorrectly inflates your debt obligations.

Payment and Account Status Errors

Misapplied payments and duplicate entries frequently appear on reports, sometimes showing the same debt twice or crediting a payment to the wrong account. Closed accounts mislabeled as open or accounts marked delinquent when they’re actually current can severely damage your score. Divorce situations commonly create errors where a former spouse’s debts appear on your report even after separation. Identity theft often reveals itself through mysterious accounts you never opened, hard inquiries from unfamiliar lenders, or fraudulent loans you don’t recognize.

Why Regular Monitoring Matters

Pull your credit reports from all three bureaus-Equifax, Experian, and TransUnion at least once annually through annualcreditreport.com, which provides free access per FTC requirements. The Federal Trade Commission has made weekly free access to all three reports permanent, so you have no reason to skip regular reviews. Reports differ between bureaus because not all creditors report to all three, meaning errors on one report might not appear on another. Comparing all three reports reveals which mistakes are widespread versus isolated to a single bureau.

Negative but accurate information can stay on your report for seven years, so timing matters when you discover errors-the sooner you dispute, the sooner corrections appear. If you spot potential identity theft, visit IdentityTheft.gov for a personalized recovery plan backed by the FTC. Checking regularly also helps you monitor whether previous disputes were actually corrected, since bureaus don’t always update information across all three reports simultaneously. This ongoing vigilance prevents small errors from compounding into larger credit damage over time.

Now that you understand what errors look like and why they matter, the next step involves taking action. Gathering the right documentation and filing your dispute properly can mean the difference between a quick resolution and months of back-and-forth with the bureaus.

Taking Action Against Credit Report Errors

Collect Your Documentation

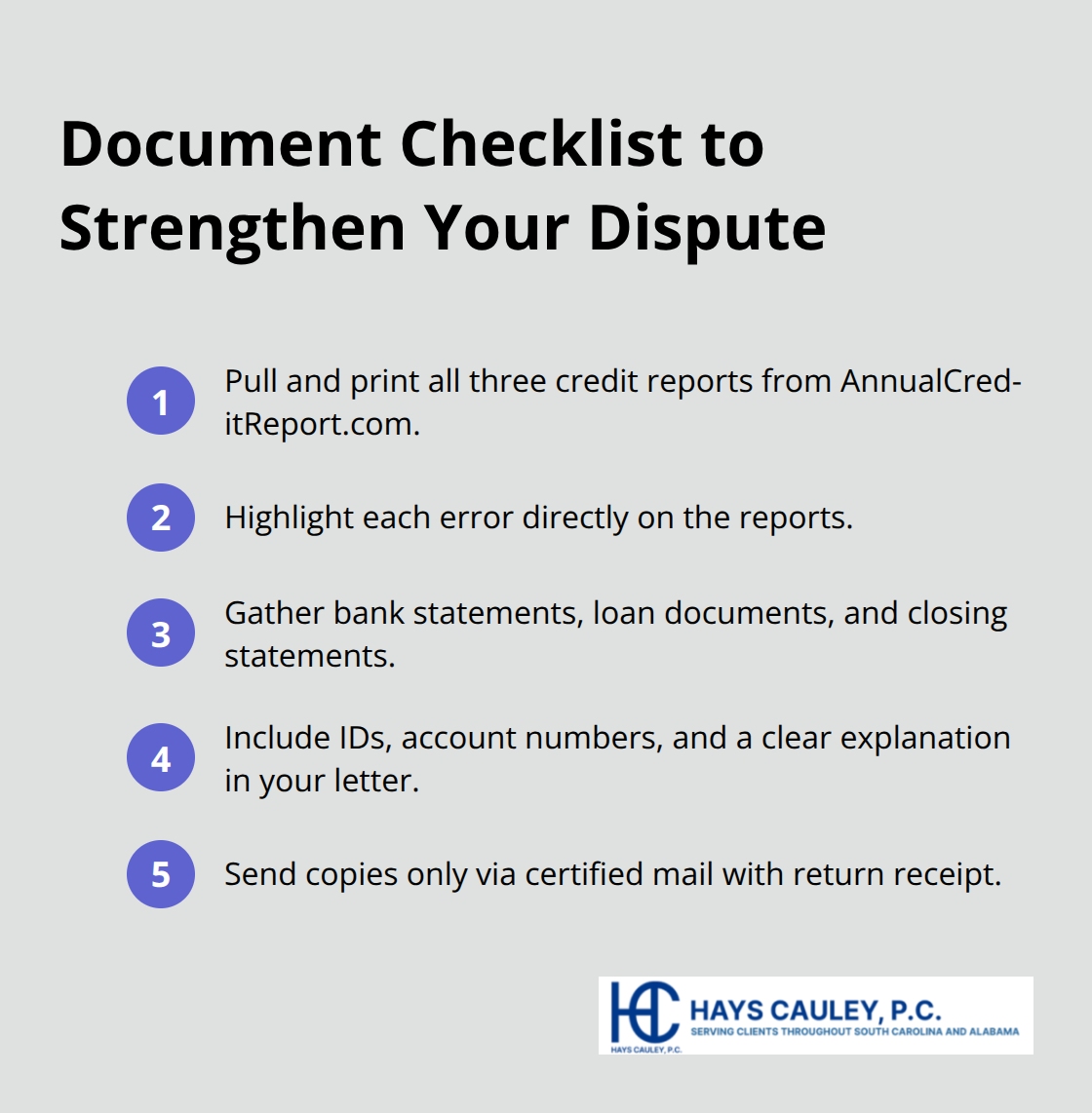

Start your dispute by gathering the right documents first. Pull copies of your credit reports from all three bureaus through annualcreditreport.com and print them immediately. Mark up each error directly on the report with a highlighter or pen, circling the specific inaccuracies you plan to dispute. Gather supporting documents that prove the error: bank statements showing correct payment dates, loan documents proving you’re not an authorized user, closing statements from paid-off accounts, or correspondence with creditors.

The FTC provides a sample dispute letter template on its website that you can customize with your specific details. Your letter should include your full name and address, your credit report confirmation number from each bureau, the specific account number for each disputed item, a clear explanation of why each item is wrong, and your requested outcome (removal or correction). Send copies of your supporting documents along with a marked-up copy of your credit report-never originals.

File Your Dispute Properly

Use certified mail with return receipt when mailing disputes to create verifiable proof that the bureau received your submission on a specific date. You can also file disputes online or by phone: Equifax accepts disputes at 866-349-5191, Experian at 888-397-3742, and TransUnion at 800-916-8800. Online filing through each bureau’s website often moves faster than mail, though certified mail creates a stronger paper trail if you need evidence later.

Track Your Progress Systematically

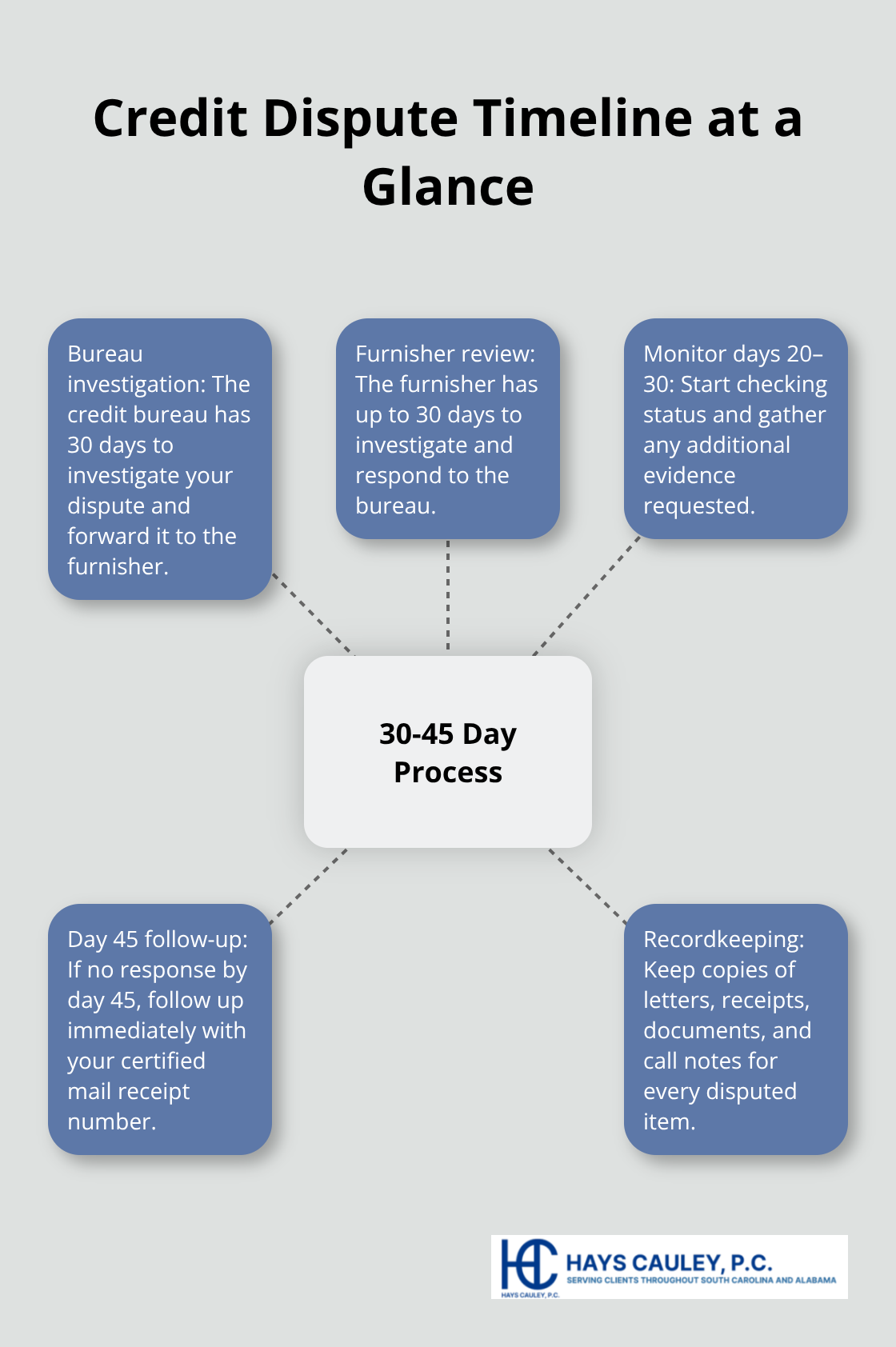

After filing your dispute, the credit bureau has 30 days to investigate and forward your complaint to the furnisher (the creditor that reported the information). The furnisher then has up to 30 days to investigate and respond. Start monitoring your case between days 20 and 30 after filing. If you don’t receive a response by day 45, follow up immediately using your certified mail receipt number as reference.

Maintain meticulous records throughout the entire process: keep copies of every dispute letter, certified mail receipts, marked-up reports, supporting documents, and notes of any phone conversations with dates and names. Track each disputed item separately in a spreadsheet or folder, noting the date filed, the bureau contacted, and the furnisher involved.

Verify Corrections and Next Steps

If the investigation finds inaccuracies, the furnisher must notify all three bureaus to correct the information. Pull updated copies of your reports from all three bureaus after corrections are made to verify the changes appeared everywhere, since bureaus don’t always update simultaneously. If the investigation concludes the information is accurate and you disagree, you can request a dispute statement be added to your file explaining your position.

Should problems persist after the investigation closes, file a complaint with the Consumer Financial Protection Bureau at its website, which will forward your complaint to the company and track their response. This structured approach transforms a frustrating process into manageable steps with clear timelines and documentation. Once you understand your rights under federal law, you’ll recognize the protections available to you throughout this entire process.

Your Legal Protections and Where to Find Help

What the Fair Credit Reporting Act Guarantees You

The Fair Credit Reporting Act, enacted in 1970 and strengthened by the Fair and Accurate Credit Transactions Act in 2003, gives you specific legal protections to challenge inaccuracies. Under the FCRA, both credit bureaus and furnishers must investigate your disputes within 30 days at no cost to you. This is not a suggestion or courtesy-it’s a legal obligation enforced by the Federal Trade Commission and state attorneys general. The law prohibits bureaus and furnishers from ignoring disputes or charging you to fix errors they created.

If a furnisher continues reporting information you’ve disputed and proven inaccurate, they face regulatory action from the Consumer Financial Protection Bureau. This enforcement mechanism matters because it means the system has teeth when companies ignore their obligations. You can also add a dispute statement to your file if you disagree with investigation results, and request that statement be sent to previous creditors and employers who received your report in the past six months (or two years for employment purposes).

Free Resources You Should Use First

The Consumer Financial Protection Bureau and Federal Trade Commission offer free resources you should use before paying anyone. The CFPB provides downloadable dispute templates and detailed guidance on its website, while the FTC maintains IdentityTheft.gov for personalized recovery plans if you suspect fraud. All three bureaus-Equifax, Experian, and TransUnion-accept disputes online, by phone, or by mail at no charge.

Equifax offers six free reports annually through 2026 beyond your standard annual access. Avoid paid third-party credit monitoring services; the free tools from government agencies and the bureaus themselves are comprehensive and reliable. These official channels cost nothing and provide the same protections as any paid alternative.

When to Contact an Attorney

If disputes don’t resolve your problem after exhausting the 30-day investigation process and filing a CFPB complaint, that’s when you should contact a consumer protection attorney. An attorney can evaluate whether you have grounds for legal action against furnishers or bureaus that violated the FCRA, potentially recovering damages for violations and your attorney fees. We at Hays Cauley, P.C. handle credit reporting disputes and identity theft cases for consumers who’ve hit dead ends with the bureaus.

Final Thoughts

Fixing errors on your credit report requires action, not patience. You’ve learned how to identify mistakes, file disputes with the three bureaus, and track progress through the 30-day investigation period. Inaccuracies cost you real money through higher interest rates and missed opportunities, so acting quickly when you spot errors makes the difference between a resolved problem and years of financial damage.

An accurate credit report directly impacts your ability to borrow, rent housing, secure employment, and obtain insurance at reasonable rates. The FCRA guarantees you the right to dispute inaccuracies for free, and furnishers must investigate within 30 days. This legal framework holds companies accountable when they report false information about you, and you can file a complaint with the Consumer Financial Protection Bureau if disputes don’t resolve your situation after 45 days.

If you’ve exhausted the standard dispute process without success, contact Hays Cauley, P.C. to discuss whether legal action fits your situation. We help consumers with credit reporting and identity theft issues when the standard process fails. Your credit report belongs to you-protect it by taking action today.