Your credit report shapes your financial life, yet many South Carolinians don’t fully understand their SC credit reporting rights. Credit bureaus make mistakes, and those errors can cost you thousands in higher interest rates or denied loans.

We at Hays Cauley, P.C. created this guide to show you exactly what protections federal and state law give you. You’ll learn how to access your report, challenge inaccurate information, and take action if your rights are violated.

Your Rights Under the Fair Credit Reporting Act: Serving South Carolina, Including Greenville, Columbia and Charleston

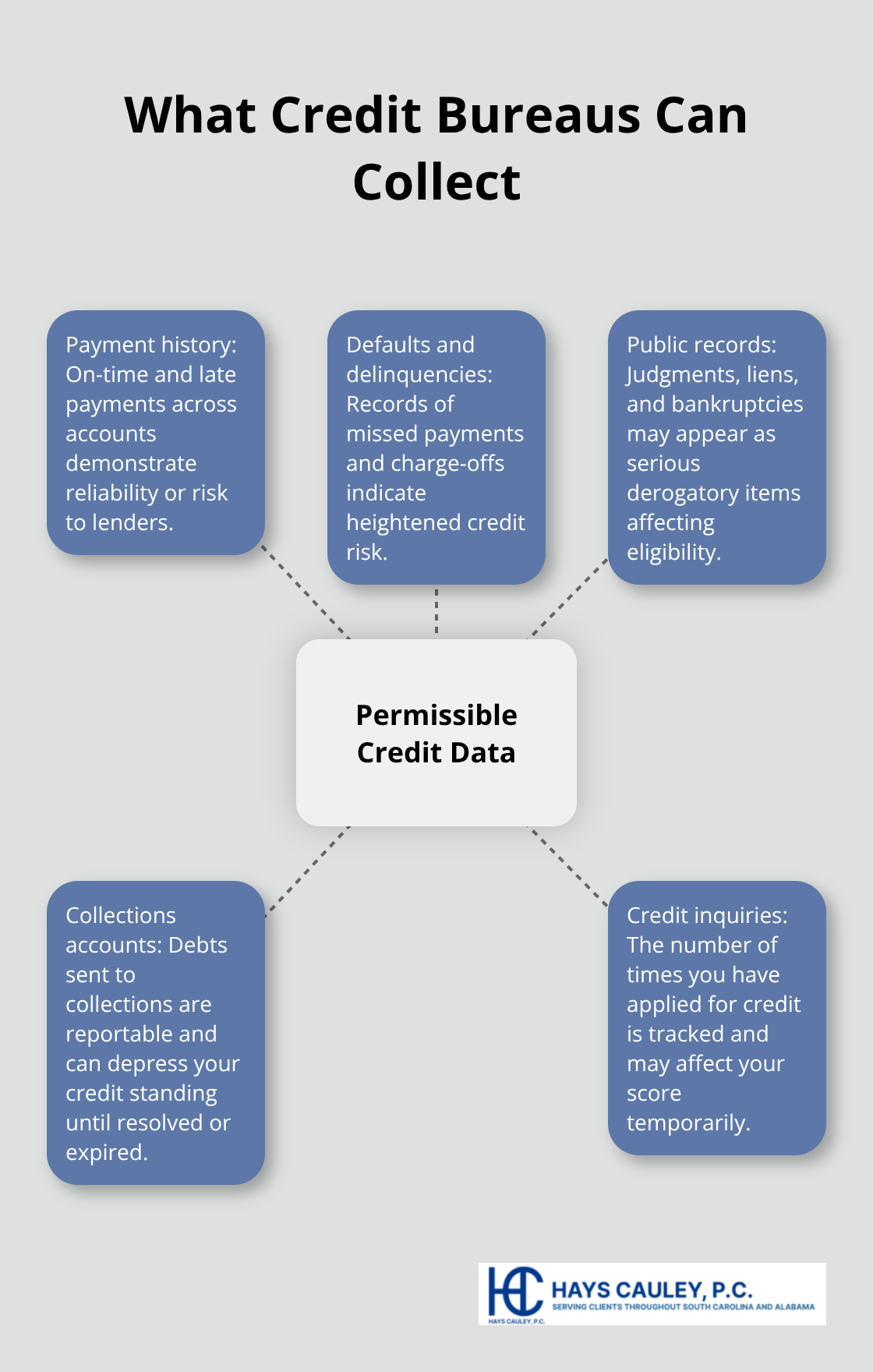

The Fair Credit Reporting Act gives you specific rights, but understanding what credit bureaus can and cannot collect is where your protection actually begins. Federal law limits credit bureaus to information that relates to your creditworthiness, credit standing, character, general reputation, personal characteristics, or mode of living. That sounds broad, but it has real boundaries. They cannot collect information about your medical history, political affiliations, religious beliefs, or sexual orientation unless it directly impacts your ability to pay debts. They also cannot legally access information about vehicular accidents or driving violations in South Carolina under state law. What they can collect includes your payment history, defaults, judgments, liens, bankruptcies, collections accounts, and the number of times you have applied for credit. The FTC reports that about one in five consumers have errors on their credit reports, yet many people never check them, which means errors compound over time without anyone catching them.

What Information Credit Bureaus Can Collect

Credit bureaus operate within strict legal boundaries, though those boundaries may feel wide. Federal law permits them to gather data about your creditworthiness and financial behavior, but prohibits collection of protected information (medical history, political views, religious beliefs, or sexual orientation). South Carolina law adds another layer of protection by excluding vehicular accidents and driving violations from what bureaus can report. The information they legally collect-payment history, defaults, judgments, liens, bankruptcies, and credit inquiries-directly affects your ability to obtain loans, insurance, or employment. Understanding this distinction matters because it helps you identify what should not appear on your report and what you can legitimately challenge.

Your Right to Access Your Credit Report

You have an absolute right to see what information credit bureaus hold about you, and this step must come first. Pull your free annual credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com. Equifax also offers six free reports annually if you call 1-866-349-5191. Do not rely on your credit score alone because the score does not reveal what is actually written on your report. When you pull your report, print it and read every line for unrecognized accounts, duplicate listings, incorrect payment histories, wrong balances, outdated negative items, and wrong personal information. Look for late payments marked as late when you paid on time, duplicate accounts under different creditor names, balances that do not match your statements, and accounts you never opened. Common errors include misapplied payments or disputes not properly recorded, so verify the account status and opening dates. Simple errors like a misspelled name resolve in about a week, while payment history disputes typically take closer to 30 days.

Disputing Inaccurate or Incomplete Information

Once you identify an error, you have the right to dispute it in writing to the credit bureau at no charge. South Carolina law requires the bureau to investigate within 30 days. Send your dispute via certified mail with return receipt to the dispute department, include your name, address, account number, and the dispute date, and clearly identify the item and explain why it is inaccurate. Attach copies of supporting documentation like bank statements or payment records. The bureau then forwards your dispute to the furnisher (the creditor providing the data) within five days, and the furnisher has up to 45 days to investigate if you submit additional documents. If the furnisher finds inaccuracy, they must notify all three bureaus to correct or remove the information. Send a separate dispute letter directly to the creditor as well because furnishers must investigate disputes too, and this dual-track approach often yields faster results. After the investigation, pull an updated report to verify the correction. If corrected, the bureaus must send you a free updated copy separate from your annual report. Corrected information can meaningfully improve your credit score within 30 to 45 days, with impact varying by item removed. Removing a late payment or a duplicate account often yields faster gains, and improved utilization can boost your score quickly, potentially helping you qualify for better loan terms and lower interest rates.

Beyond federal protections, South Carolina state law provides additional safeguards that strengthen your position when credit reporting errors occur or your rights are violated.

South Carolina State Laws Protecting Your Credit: Serving South Carolina, Including Greenville, Columbia and Charleston

South Carolina strengthens federal protections with its own identity theft and credit reporting laws, providing additional remedies that federal law alone does not offer. Under Title 37, Chapter 20 of the South Carolina Code, you obtain rights that extend beyond the Fair Credit Reporting Act.

Security Freezes and Address Verification

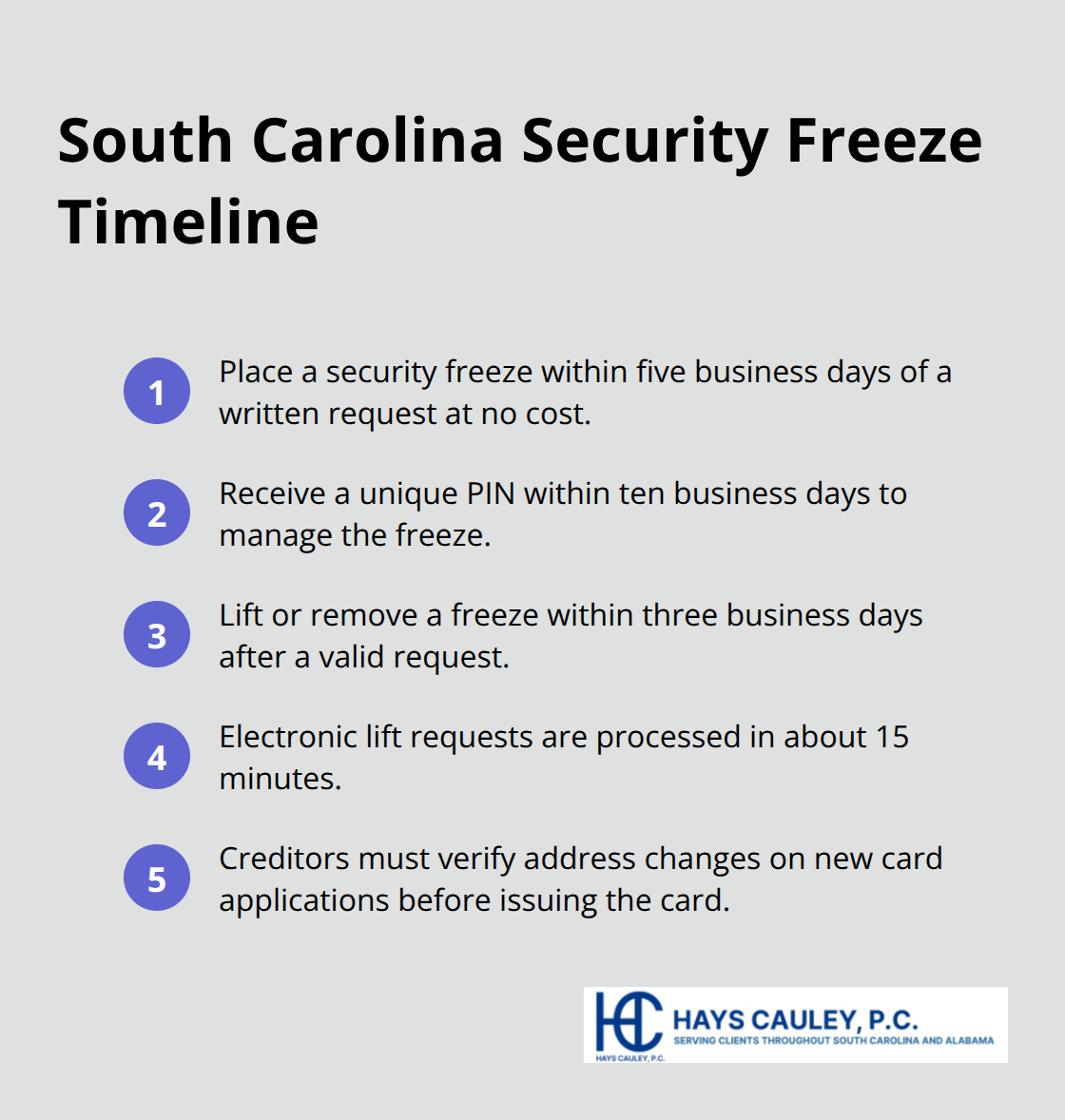

The state requires credit bureaus to place a security freeze on your file within five business days of a written request at no cost. You receive a unique PIN within ten business days to manage it. Removal or temporary lifting of a freeze occurs within three business days after a valid request, with electronic requests processed in about 15 minutes.

A security freeze blocks unauthorized access to your credit file, preventing someone from opening accounts in your name without your explicit permission. South Carolina also mandates that when you apply for a new credit card and the address on your application differs from the bureau’s file, the bureau must notify the creditor. The creditor then must verify the address change before issuing the card. This additional verification step catches identity theft attempts that might otherwise slip through undetected.

Reinvestigation Rights and Damages

When you dispute an item on your credit report in South Carolina, the bureau must reinvestigate at no charge within 30 days and provide evidence supporting accuracy if the dispute is denied. If the inaccuracy harms your creditworthiness and remains uncorrected after judgment, damages escalate to up to $1,000 per day until corrected. This creates real financial pressure on bureaus to fix errors promptly. Willful violations of South Carolina’s credit reporting protections trigger damages of up to three times your actual damages or at least $1,000 per incident, plus attorney’s fees. Negligent violations yield actual damages or at least $1,000 per incident. This statutory framework means violations carry teeth that motivate compliance.

Truth in Lending Act Violations and Complaints

If a creditor violates disclosure requirements under the Truth in Lending Act, you can recover actual damages plus up to twice the finance charge, plus attorney’s fees. Willful violations can incur penalties up to $5,000 and potential jail time. File a complaint with the South Carolina Department of Consumer Affairs to address violations directly with state enforcement. You can file complaints online through the SC official website, which handles issues with debt collectors, credit reporting, or other consumer concerns. Contact the SC Department of Consumer Affairs at 803-734-4200 or scdca@scconsumer.gov for guidance on your rights.

Negative Items and Statute of Limitations

Inaccurate negative information can legally remain on your report for seven years, while bankruptcy stays for ten years. Once that period expires, the bureau must remove the item. If a bureau continues reporting an item beyond the statutory period, that constitutes a violation you can challenge. Victims of identity theft in South Carolina can initiate a law enforcement investigation by reporting to a local agency, which must take the report, provide a copy, and begin an investigation. If the identity thief used your name for a crime, you can petition for an expedited judicial determination of factual innocence with potential expunction of the erroneous conviction. The State Law Enforcement Division maintains victim identity theft records, with access limited to criminal justice agencies, though you or your authorized representatives may access relevant records.

Cure Rights for Secured Loans

Secured single-payment loans in South Carolina give you the right to cure a default with at least 20 days’ notice before further action proceeds. Keep copies of all cure notices, responses, and enforcement communications to document your rights and timelines. These protections create a framework that holds credit bureaus and creditors accountable, but violations still occur-and when they do, you need to know how to identify them and respond effectively.

Common Credit Reporting Violations and How to Address Them: Serving South Carolina, Including Greenville, Columbia and Charleston

When Credit Bureaus Fail to Investigate Your Disputes

The law requires credit bureaus to investigate your disputes within 30 days, but many investigations lack real depth. Bureaus contact the furnisher once and accept whatever response arrives without pushing for verification. The CFPB notes that well-documented disputes improve investigation quality and outcomes, which means you must make your investigation so thorough that the bureau cannot ignore it.

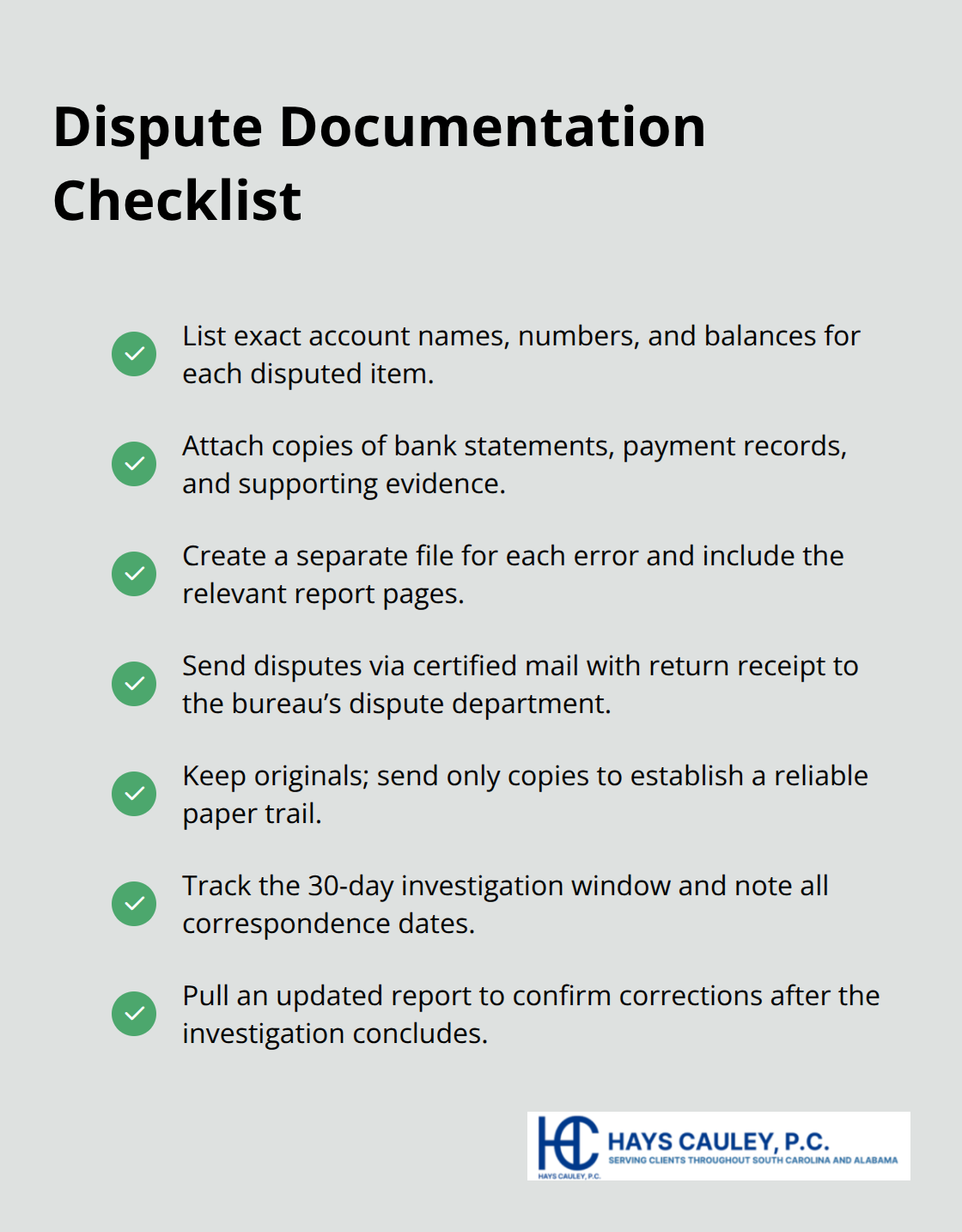

When you dispute an item, document everything with exact account names, account numbers, balances, and attach supporting documentation like bank statements or payment records proving the error. Build a separate file for each error with copies of evidence and your report pages, keeping originals and sending copies to the bureaus to create a solid paper trail. Send your dispute letter via certified mail with return receipt to the dispute department, not general customer service, because this creates proof the bureau received your challenge.

In your letter, clearly identify the specific item, explain exactly why it is inaccurate with reference to attached evidence, and request removal if not verified after investigation. Send a separate dispute letter directly to the creditor or furnisher as well, since furnishers must investigate disputes under the Fair Credit Reporting Act and this dual-track approach forces faster resolution. Many bureaus count on consumers abandoning efforts after the first investigation fails, so monitor progress carefully. Expect the 30-day investigation window, check your credit report around day 35, and expect corrections to take about 30 to 45 days from filing.

If results seem inadequate or the investigation stalls, that signals a potential federal Fair Credit Reporting Act violation. At that point, seek legal review to determine whether you have remedies available. Willful violations under federal law yield damages of up to three times actual damages or at least $1,000 per incident, while negligent violations yield actual damages or at least $1,000 per incident, plus potential attorney’s fees.

Reporting Outdated Negative Items

Negative information can legally remain on your report for seven years, with bankruptcy staying for ten years, but once that period expires, the bureau must remove the item. If a bureau continues reporting an item beyond the statutory period, that constitutes a violation you can challenge immediately.

Pull your report and identify the opening date of the account. Calculate when seven years ends and dispute the outdated item with documentation showing the violation. The bureau cannot legally report information beyond these timeframes, and continued reporting after expiration violates federal law. This violation carries the same remedies as other Fair Credit Reporting Act breaches (actual damages or at least $1,000 per incident for negligent violations; up to three times actual damages or at least $1,000 per incident for willful violations).

Unauthorized Access to Your Credit Report

Unauthorized access occurs when someone pulls your report without a permissible purpose under federal law, which includes credit, insurance, or employment purposes. If you see inquiries on your report you did not authorize, that signals identity theft or a furnisher accessing your file improperly.

Request documentation from the bureau showing which entity accessed your report and why. If the entity cannot provide a legitimate reason, file a complaint with the South Carolina Department of Consumer Affairs at 803-734-4200 or scdca@scconsumer.gov and consider placing a security freeze at no cost to prevent future unauthorized access. A security freeze blocks access to your credit file, forcing anyone wanting to open accounts in your name to contact you first using the PIN you receive within ten business days of placing the freeze.

Final Thoughts

Your SC credit reporting rights give you real power to fix errors and hold bureaus accountable, but only if you act on them. The federal Fair Credit Reporting Act sets the baseline, while South Carolina law adds protections that go further. You can access your reports for free, dispute inaccurate information at no cost, place security freezes without paying a dime, and recover damages if your rights are violated.

If your rights have been violated, document everything immediately and gather copies of your credit reports, dispute letters, responses from bureaus, and any communications showing the violation. Contact the South Carolina Department of Consumer Affairs at 803-734-4200 or scdca@scconsumer.gov to file a complaint, and if you believe a willful violation occurred, you may have grounds to pursue legal remedies including damages and attorney’s fees. Many violations go unchallenged simply because consumers do not know they have legal recourse.

Pull your free reports regularly through AnnualCreditReport.com and monitor for changes, and if you need legal assistance evaluating whether a violation occurred or what remedies apply to your situation, Hays Cauley, P.C. stands ready to help you protect your SC credit reporting rights and financial stability.