Identity theft affects roughly 26 million Americans annually, and the financial fallout can reach thousands of dollars per victim. Understanding identity theft insurance cost helps you decide whether this protection fits your budget and security needs.

At Hays Cauley, P.C., we’ve seen firsthand how identity theft disrupts lives across South Carolina, including Greenville, Columbia and Charleston. This guide breaks down what you’ll actually pay for coverage and whether it’s worth the investment.

What Does Identity Theft Insurance Actually Cost?

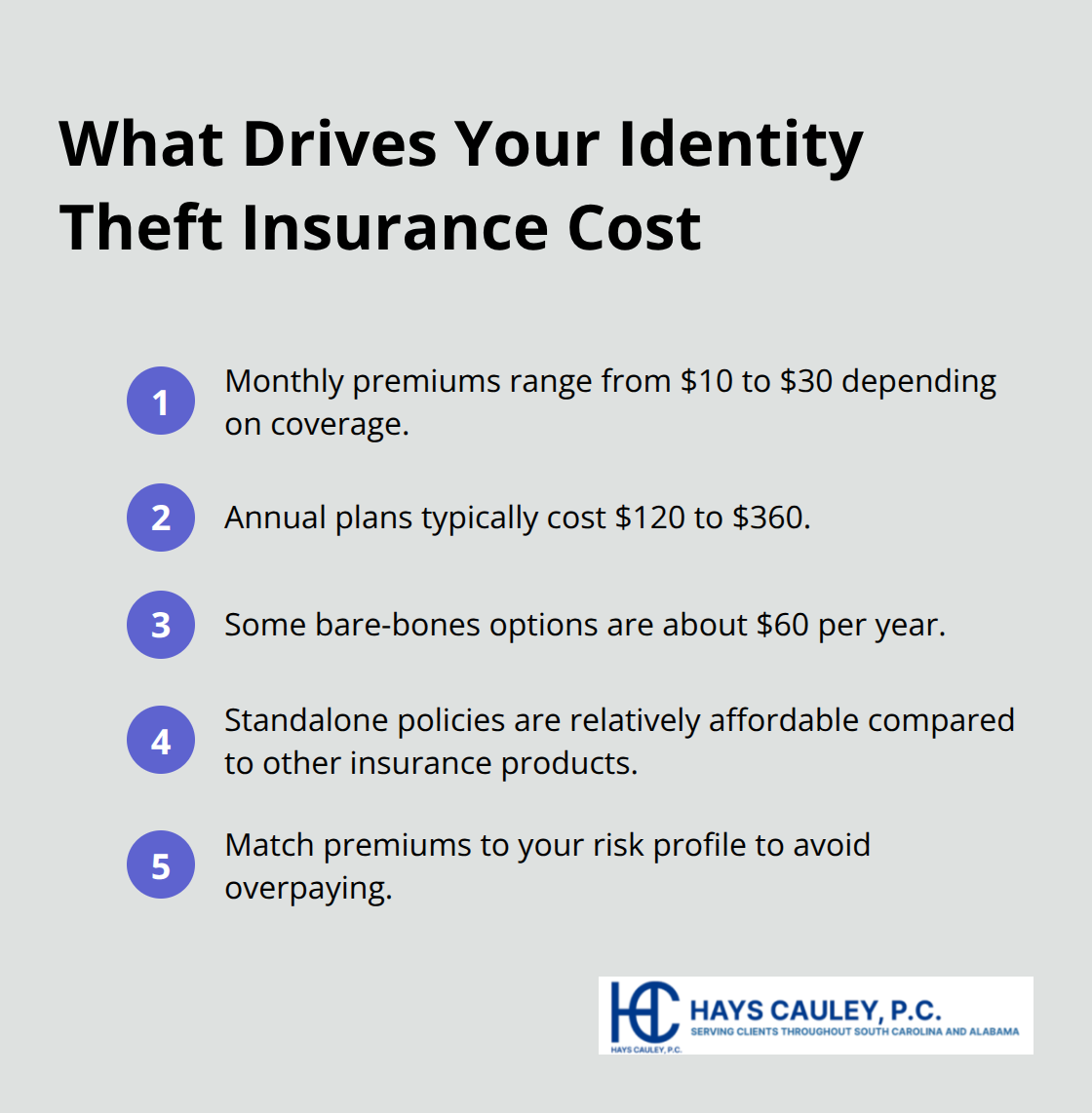

Identity theft insurance premiums range from about $10 to $30 monthly, depending on coverage depth and the provider you choose. Annual plans typically run between $120 and $360, though some bare-bones options start as low as $60 per year. The National Association of Insurance Commissioners reports that standalone identity theft policies remain relatively affordable compared to other insurance products, making them accessible for most households. What matters most is matching the premium to your actual risk profile rather than paying for coverage you won’t use. Someone with excellent credit and minimal online activity needs far less protection than a business owner managing multiple accounts and sensitive data daily.

Coverage depth drives most price differences

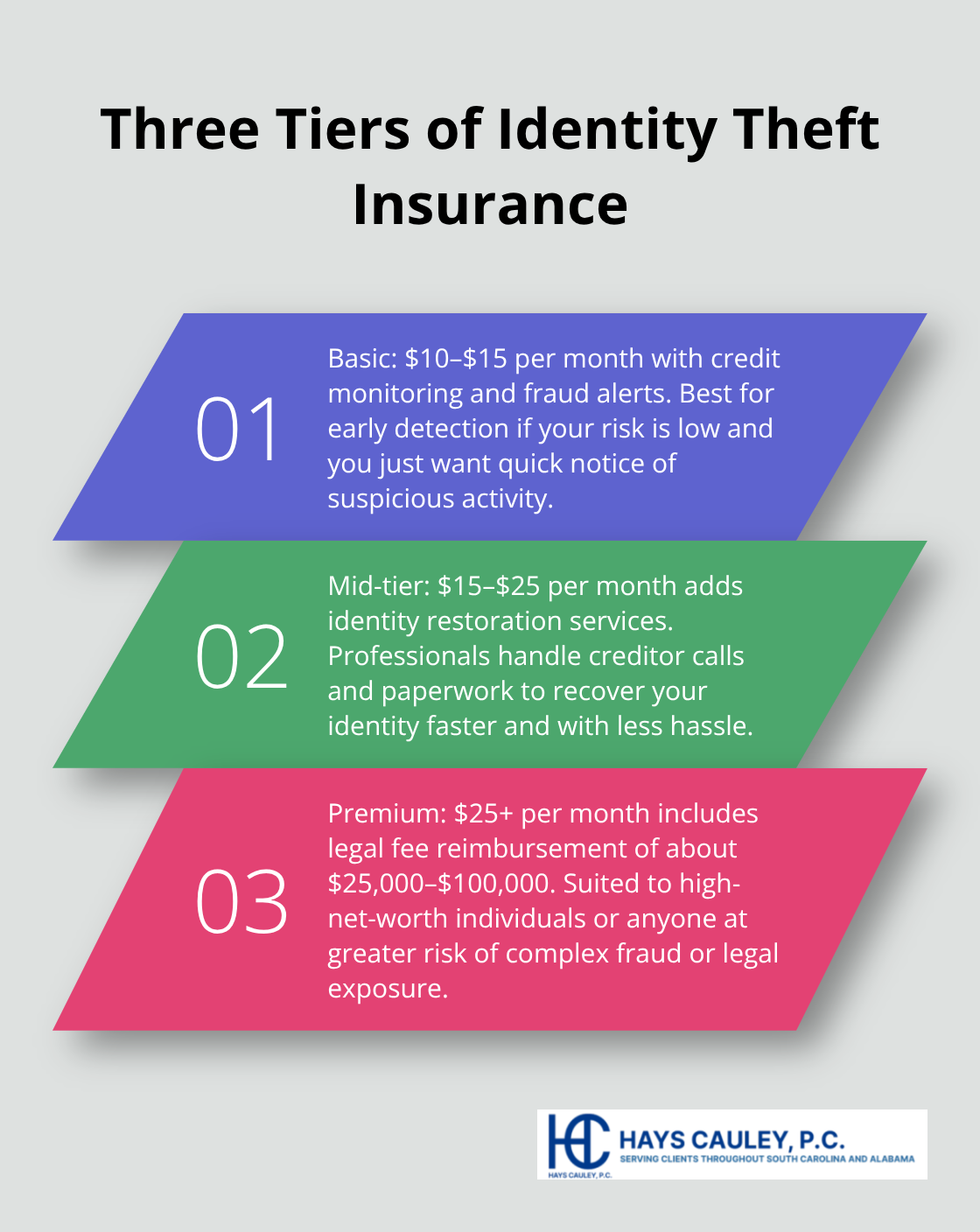

The primary cost variable is what’s actually covered. Basic plans offering credit monitoring and fraud alerts run $10-15 monthly and work fine if you’re primarily concerned about detecting unauthorized accounts early.

Mid-tier plans at $15-25 monthly add identity restoration services, meaning the company actively helps recover your identity if theft occurs-handling calls to creditors and filing reports on your behalf. Premium plans exceeding $25 monthly include legal fee reimbursement up to $25,000-$100,000, which protects you if identity theft leads to lawsuits or criminal proceedings. Victims often face unexpected legal expenses when theft escalates, making this coverage worth the additional cost for high-net-worth individuals and those in vulnerable positions. Your income level and assets directly influence whether premium protection justifies the expense.

Age, location, and prior incidents reshape your rate

Insurance companies adjust pricing based on several concrete factors. Younger consumers typically pay less because they have shorter financial histories to steal, while those over 65 face significantly higher premiums due to increased vulnerability.

Your state matters too-residents in high-fraud states like California and Florida pay more than those in lower-risk areas. Prior identity theft incidents can double your premium or make some insurers refuse coverage altogether, pushing you toward specialized high-risk providers that charge substantially more. Employment in fields handling sensitive data (such as healthcare or finance) may qualify you for discounts through employer-sponsored plans, which often cost 30-40% less than individual policies purchased directly.

What separates affordable from expensive coverage

Price differences between providers stem from how aggressively they monitor your accounts and how quickly they respond to fraud. Some companies offer 24/7 monitoring across multiple credit bureaus, while others check your credit quarterly. Response time matters significantly-faster intervention prevents more damage and reduces your out-of-pocket costs. The breadth of covered scenarios also affects pricing; some plans cover only financial identity theft, while others include medical identity theft and synthetic identity fraud. These distinctions explain why two policies at similar price points may offer vastly different protection levels.

Understanding these cost factors positions you to evaluate which coverage type actually fits your situation, rather than simply choosing the cheapest option available.

Coverage Types and What They Cost

Credit Monitoring Services Start at the Lowest Price Point

Credit monitoring services form the foundation of most identity theft insurance plans, and they’re where pricing starts lowest. Basic credit monitoring costs $10-15 monthly and tracks your credit reports from the three major bureaus-Equifax, Experian, and TransUnion-typically checking them quarterly or monthly depending on the plan tier. The Federal Trade Commission allows you one free credit report annually from each bureau through AnnualCreditReport.com, but paid monitoring accelerates detection significantly. When monitoring services catch fraudulent accounts within days rather than weeks, you avoid thousands in unauthorized charges and damage to your credit score. However, credit monitoring alone won’t help you recover if theft already occurred; it only alerts you to the problem after someone exploits your identity.

Identity Restoration Assistance Costs More but Saves Time

Identity restoration assistance jumps the cost to $15-25 monthly because the insurance company actively intervenes on your behalf when fraud happens. This service means trained professionals contact creditors, dispute fraudulent accounts, file police reports, and work with credit bureaus to remove false information from your file. The Identity Theft Resource Center reports that the average identity theft victim spends 200-400 hours resolving the damage, so paying extra for professional help becomes genuinely valuable. Mid-tier plans typically cover restoration costs up to $100,000 in liability, which protects you if criminals open credit lines or take out loans in your name. This coverage level suits most households because it addresses the actual financial and administrative burden of recovery without the premium pricing of legal protection.

Legal Fee Coverage Protects Your Assets

Legal fee coverage and reimbursement represents the highest tier, running $25-40+ monthly, and covers attorney fees up to $25,000-$100,000 if identity theft results in lawsuits or criminal proceedings against you. Victims occasionally face civil suits from creditors or encounter criminal charges related to fraudulent accounts opened in their name, making legal representation essential. This protection matters most for high-net-worth individuals, business owners managing sensitive financial data, and those in positions vulnerable to sophisticated fraud schemes.

Matching Coverage to Your Actual Risk Profile

The difference between these three tiers comes down to your actual risk exposure. Someone with significant assets and complex finances needs legal protection, while a wage earner with modest savings may find restoration assistance sufficient for recovery needs. Your income level, employment field, and financial complexity should guide which tier you select rather than price alone. The next section compares identity theft insurance against other protection methods you might already have available.

Identity Theft Insurance vs. Other Protection Methods: Serving South Carolina, including Greenville, Columbia and Charleston

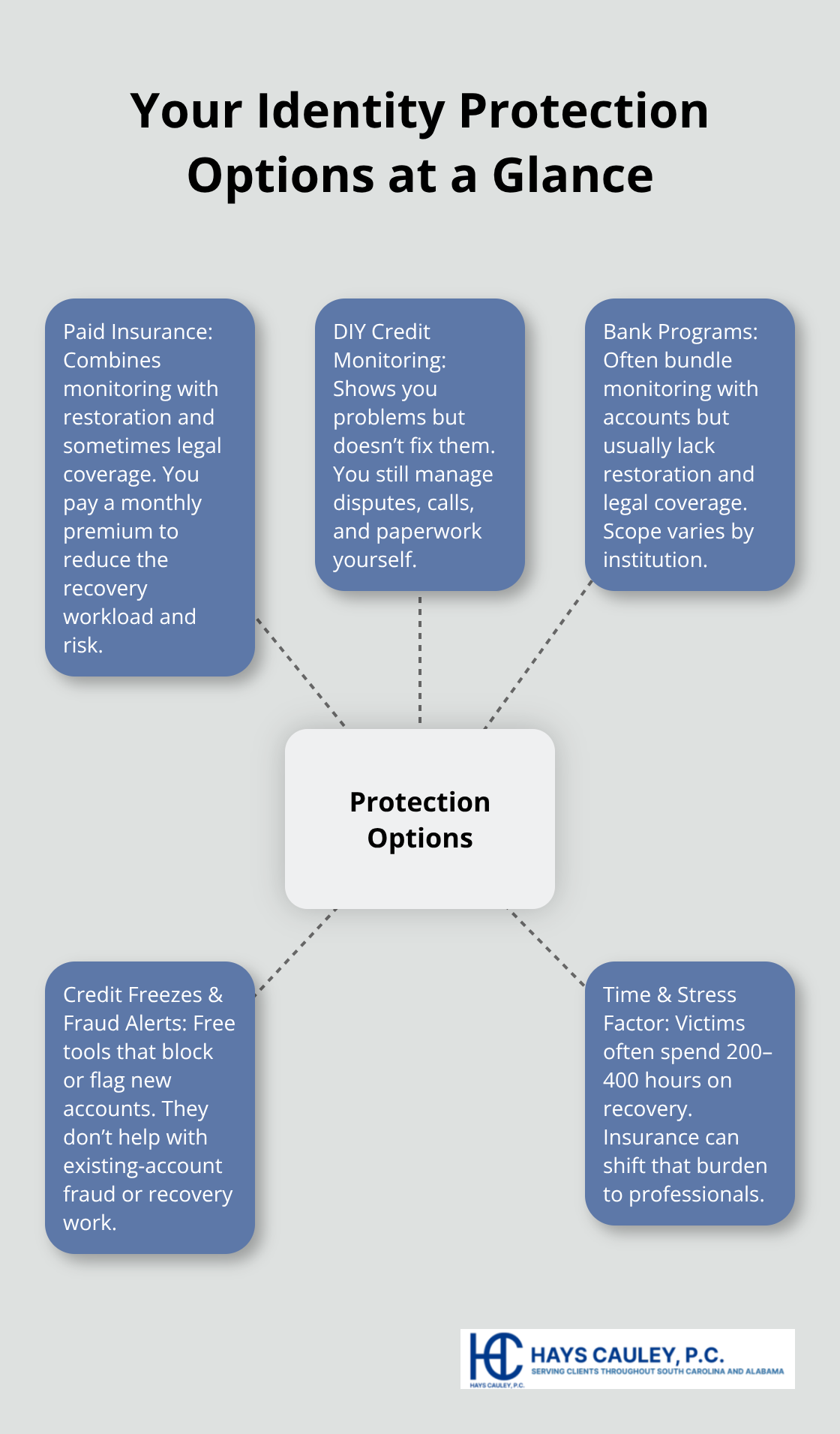

Paid identity theft insurance isn’t your only option for fighting fraud, and understanding what free or low-cost alternatives actually accomplish helps you decide whether the monthly premium makes sense. Many people already have some protection through their bank or employer, while others rely on credit freezes and fraud alerts available directly from credit bureaus.

The critical distinction is that these alternatives typically handle detection or prevention but rarely cover the restoration work that consumes hundreds of hours and thousands of dollars when theft occurs.

DIY Credit Monitoring Tools Show You Problems Without Fixing Them

DIY credit monitoring through free annual reports or paid services like Credit Karma shows you what’s on your credit file, but it doesn’t fix anything after damage happens. You still handle all the calls, disputes, and paperwork yourself when fraud appears on your report. The Federal Trade Commission provides one free credit report annually from each major bureau through AnnualCreditReport.com, which costs nothing but requires you to monitor actively rather than receiving automatic alerts. Paid DIY tools offer faster detection than annual checks, yet they stop short of the restoration assistance that professional identity theft insurance provides. This approach works only if you have time to act quickly when fraud appears.

Bank-Provided Identity Protection Offers Limited Coverage

Bank-provided identity protection programs, often bundled with premium checking accounts or credit cards, offer monitoring similar to basic insurance plans but usually lack restoration assistance and legal coverage. Your bank monitors your accounts and alerts you to suspicious activity, which prevents some fraud but doesn’t help after criminals open new accounts in your name. These programs vary widely in scope-some cover only your bank’s accounts while others monitor all three credit bureaus. The protection stops at detection; you still must handle the restoration work yourself if theft occurs. Most consumers don’t realize their bank’s protection has significant gaps until fraud actually happens.

Credit Freezes and Fraud Alerts Prevent New Accounts

Credit freezes and fraud alerts from Equifax, Experian, and TransUnion cost nothing and prevent new accounts from opening in your name, yet they don’t help if someone steals your existing accounts or commits medical identity theft using your information. A credit freeze blocks access to your credit file entirely, making it nearly impossible for criminals to open new credit lines (though you must temporarily lift the freeze when you apply for legitimate credit yourself). Fraud alerts last one year and notify creditors to verify your identity before opening accounts, but they require you to monitor your credit actively. Neither option addresses the hundreds of hours required to recover from identity theft that already occurred.

The Time and Stress Factor Determines Real Value

The real question is whether your time and stress tolerance justify avoiding paid insurance. If you have the bandwidth to spend 200-400 hours resolving identity theft yourself, as the Identity Theft Resource Center documents, then stacking multiple free tools might work-combining annual credit reports, bank monitoring, and a credit freeze covers basic detection. However, if your job demands focus, you manage significant assets, or you simply value your peace of mind, the $180-$300 annual cost for mid-tier identity theft insurance becomes reasonable compared to the restoration burden. The difference between those who had professional restoration assistance and those attempting recovery alone is stark-insured victims recover in weeks while uninsured victims spend months untangling fraud.

Final Thoughts

Identity theft insurance cost ranges from $60 to $360 annually, but the real value lies in matching that expense to your actual risk profile rather than choosing based on price alone. Basic plans at $10-15 monthly work if you’re primarily concerned with early detection, while mid-tier coverage at $15-25 monthly becomes worthwhile when you factor in the 200-400 hours the Identity Theft Resource Center reports victims spend recovering from fraud. Premium plans exceeding $25 monthly make sense for high-net-worth individuals and those managing sensitive financial data, since legal fee coverage protects assets that could otherwise disappear during recovery.

The comparison between paid insurance and free alternatives reveals a hard truth: credit freezes, fraud alerts, and bank monitoring catch problems but don’t fix them. You still handle the restoration work yourself unless you pay for professional assistance. That distinction matters enormously when criminals open accounts in your name or commit medical identity theft using your information, and the time burden alone justifies the annual premium for most households (particularly those where both spouses work full-time or manage complex finances).

If you’re relying solely on free tools or bank-provided monitoring, evaluate whether you have the bandwidth to spend months resolving identity theft if it happens. If not, a mid-tier plan covering credit monitoring and identity restoration assistance addresses most household needs without excessive cost. Those with significant assets should prioritize legal fee coverage to protect against the unexpected lawsuits and criminal charges that sometimes accompany sophisticated fraud schemes, and Hays Cauley, P.C. helps consumers navigate credit reporting, identity theft, and debt-related problems.