What Is Synthetic Identity Theft?

Criminals are stealing pieces of your identity to build fake credit profiles that rack up debt in your name. A synthetic identity theft definition covers fraudsters who blend real and fabricated information to create entirely new identities, then exploit them for financial gain.

At Hays Cauley, P.C., we help South Carolina residents, including those in Greenville, Columbia, and Charleston, fight back against identity fraud. Understanding how this crime works is your first line of defense.

How Synthetic Identity Theft Actually Works

Synthetic identity theft operates differently from traditional identity theft because criminals don’t steal your existing identity-they manufacture a new one using your real information mixed with fabricated details. The Federal Trade Commission reported that synthetic identity fraud resulted in approximately $20.2 billion in losses across the U.S. financial system in recent years. Criminals start by obtaining a real Social Security number, often through data breaches, the dark web, or purchases of stolen credentials from other criminals. They then pair this legitimate SSN with a completely fabricated name, address, and employment history. This hybrid approach makes synthetic fraud harder to detect because it doesn’t immediately trigger the alarm bells associated with someone using your actual name and address. The criminal opens accounts in this fake name using the real Social Security number, which means the fraudulent activity appears on credit reports but under a different identity than yours.

The Criminal’s Strategy Unfolds

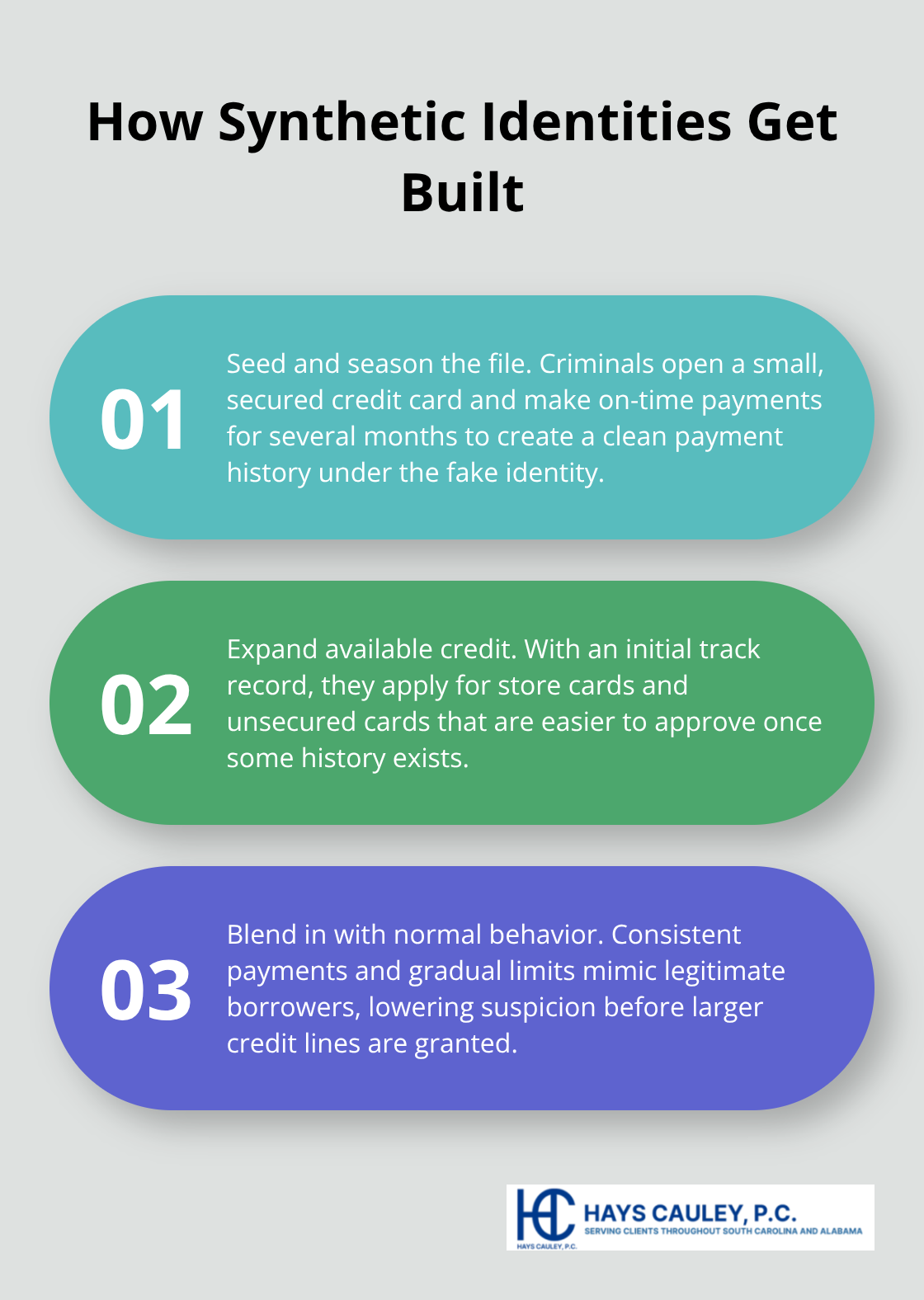

Criminals follow a deliberate roadmap once they establish a synthetic identity. They typically start by obtaining a secured credit card, depositing cash to back the credit line, and making consistent payments for three to six months. This creates a positive payment history under the fake identity.

Next, they apply for additional credit products like retail store cards or unsecured credit cards, which creditors approve more readily after the applicant demonstrates initial payment responsibility. The entire process mimics legitimate credit-building behavior, which is precisely why it works so effectively.

Building False Credibility

Some fraudsters strengthen the false profile further by establishing utility accounts, phone contracts, or rental histories in the synthetic name. Financial institutions see what appears to be a legitimate consumer with growing credit capacity and limited history, so they approve larger credit lines. At this point, the synthetic identity has become valuable enough for the criminal to max out multiple accounts simultaneously and disappear, leaving creditors holding worthless debt. This coordinated fraud can result in hundreds of thousands of dollars in losses before the scheme unravels. Understanding how criminals build these fake profiles reveals why detection remains so difficult-and why your vigilance matters when monitoring your own credit activity.

The Real Cost of Synthetic Identity Theft

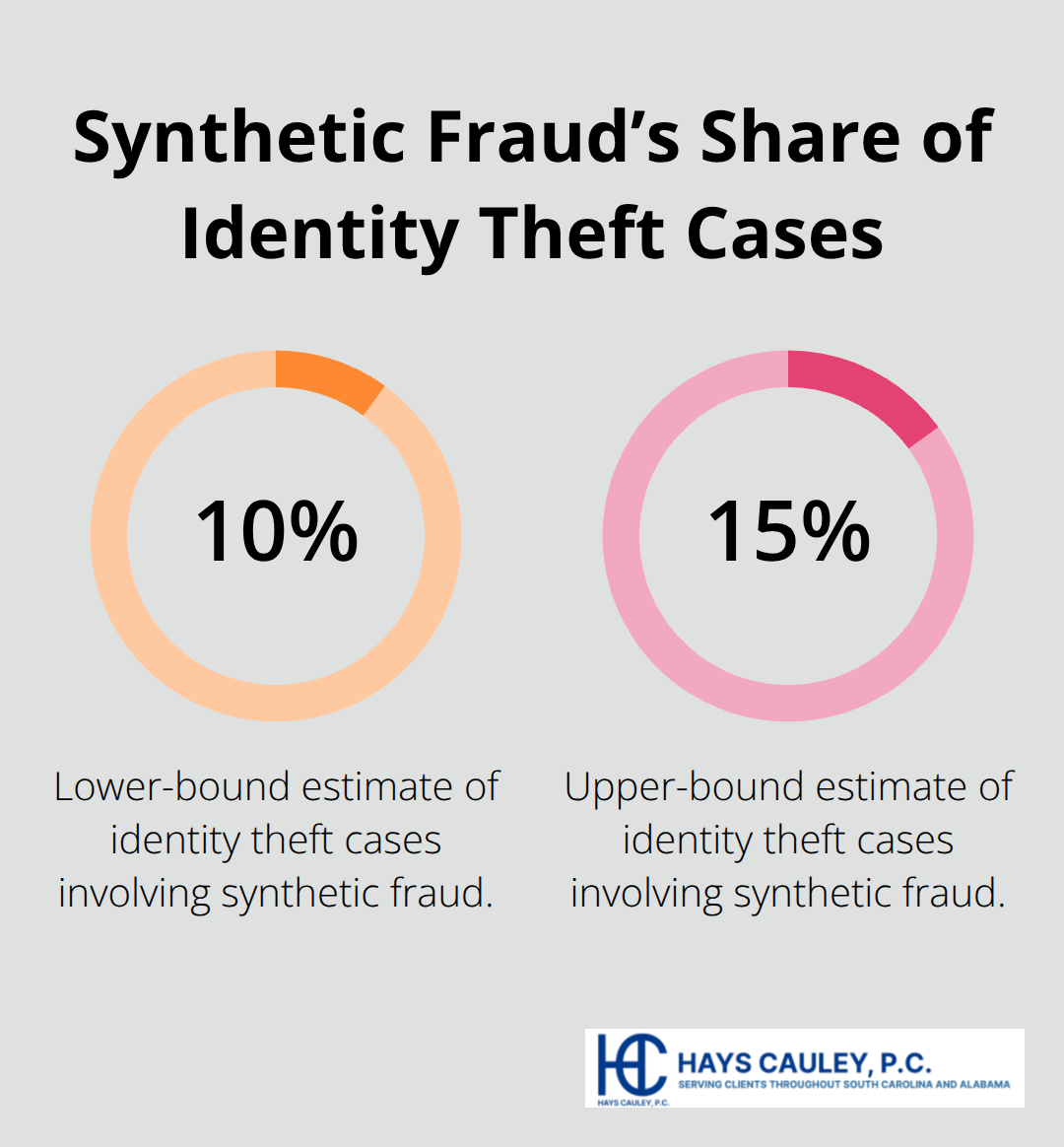

Synthetic identity theft inflicts damage that extends far beyond the initial fraud. The Federal Trade Commission’s Identity Theft Report documented that synthetic fraud accounts for approximately 10-15% of all identity theft cases, yet it produces substantially higher financial losses per incident compared to traditional identity theft. When criminals max out multiple accounts simultaneously, victims often face $10,000 to $50,000 in fraudulent debt before they discover the scheme.

Your credit report becomes a battleground where accounts appear under a name you don’t recognize, making the cleanup process exhausting and time-consuming. Unlike traditional identity theft where creditors might recognize the fraud immediately because transactions don’t match your usual patterns, synthetic fraud looks legitimate on the surface. Creditors see consistent payment history followed by coordinated default across multiple accounts, which they classify as standard delinquency rather than fraud. This misclassification means the fraudulent accounts remain on your credit report longer, dragging your credit score down even after you’ve reported the crime.

How Your Credit Gets Damaged

The damage to your credit profile happens in stages. First, the fraudulent accounts accumulate on your credit report under the synthetic name, but because that fake identity shares your real Social Security number, credit bureaus may link the accounts to your file. Second, when the criminal stops paying and defaults across multiple accounts simultaneously, the negative marks stack up rapidly. Third, debt collectors may contact you about accounts in a name you don’t recognize, creating confusion about whether you’re actually responsible. The longer these accounts remain active and delinquent, the more they suppress your credit score. Some victims report score drops of 100-150 points within months of synthetic fraud occurring on their file. Rebuilding from this damage takes years, not months.

Long-Term Financial Consequences

Victims face ongoing consequences well after the initial fraud ends. A damaged credit score makes obtaining mortgages, auto loans, or even rental approval significantly harder for years. Lenders view the delinquency history as proof of financial irresponsibility, even though you never incurred the debt. Some employers conduct credit checks during hiring, meaning synthetic fraud could affect your employment prospects. The Federal Trade Commission reports that identity theft victims spend an average of 40-100 hours resolving the issue, representing real time and money lost from your life. Medical debt tied to synthetic identities creates additional complications because healthcare providers may refuse treatment if they see delinquent accounts under your Social Security number. Victims must continually prove their identity isn’t responsible for fraudulent accounts, placing the burden of proof on the wrong shoulders.

Why Detection Matters Now

The challenge intensifies because you won’t immediately notice synthetic fraud on your own credit file. Criminals operate under a different name, so you won’t see suspicious charges on your bank statements or recognize unfamiliar accounts. The fraud only surfaces when you apply for credit yourself and lenders reject your application, or when debt collectors contact you about accounts you never opened. By that time, months or even years of fraudulent activity may have accumulated. This delayed detection means criminals operate with minimal risk of interruption during the critical credit-building phase. The longer the synthetic identity remains active and undetected, the more damage it inflicts on your financial future and the harder you’ll work to restore your reputation with creditors. Taking steps to protect yourself from financial identity theft and using identity theft protection services can help you detect and prevent this type of fraud before it causes irreversible damage.

Spotting Synthetic Identity Theft Before It Destroys Your Credit

Detecting synthetic identity theft requires aggressive monitoring because the fraud operates invisibly until significant damage accumulates. The most reliable warning sign appears when you apply for credit and lenders reject your application despite having strong payment history on your existing accounts. Another critical indicator surfaces when debt collectors contact you about accounts under your Social Security number but in a name you don’t recognize. If you receive mail addressed to unfamiliar names at your address, or if you notice inquiries on your credit report from creditors you never contacted, synthetic fraud may already be active on your file. The Federal Trade Commission reports that victims typically discover synthetic fraud within 12 to 18 months after the initial fraudulent account opens, meaning months of damage occur before you even know the crime happened. This delay underscores why waiting for obvious red flags is dangerously passive. You need a proactive system that catches fraud during the earliest stages, not after it has already ravaged your credit profile.

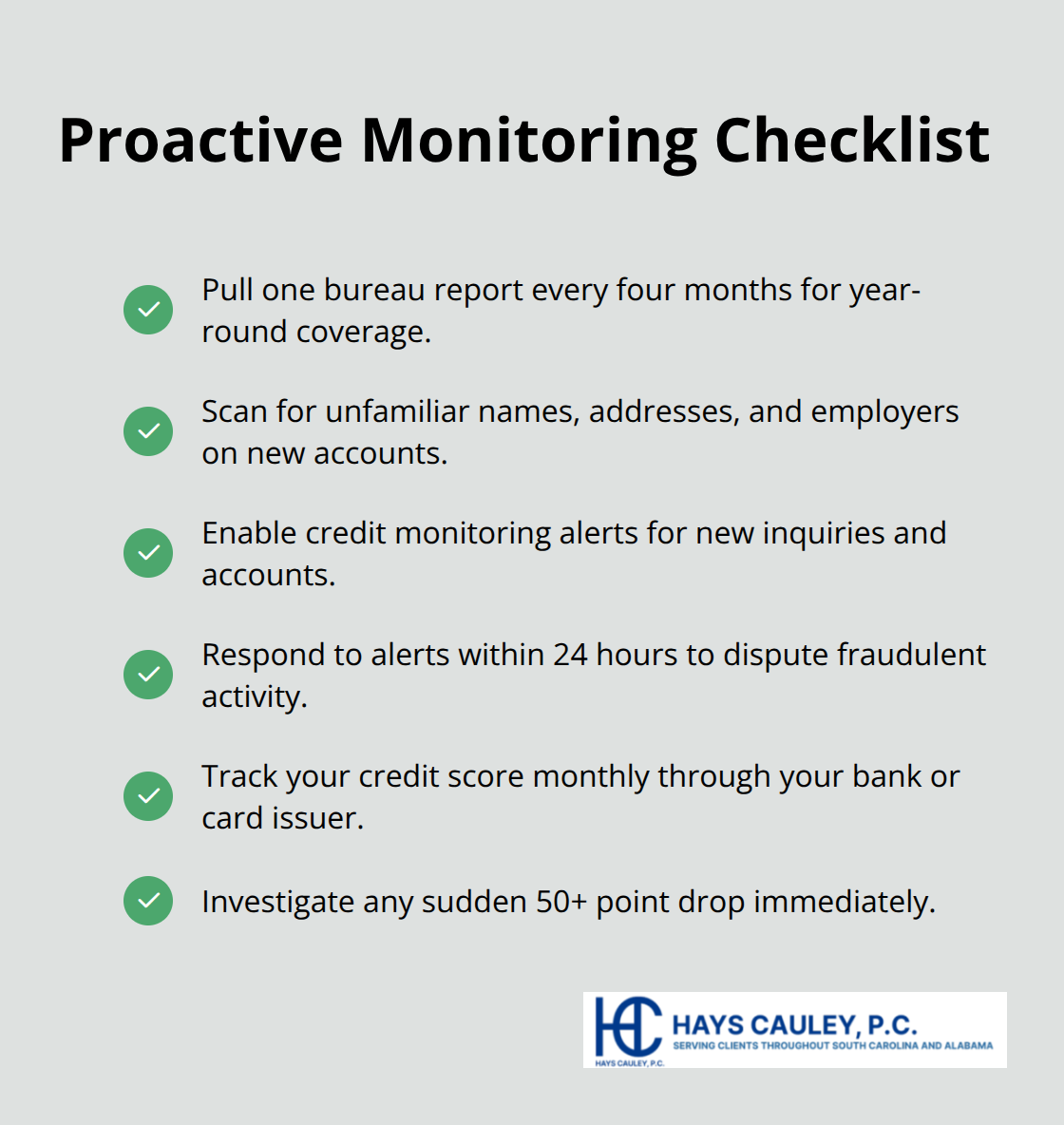

Monitor Your Credit Report Quarterly, Not Annually

Annual credit report checks from annualcreditreport.com provide a baseline, but they leave nine-month gaps where criminals operate freely. Pull your full credit report from all three bureaus (Equifax, Experian, and TransUnion) every four months instead of once yearly, staggering one bureau every four months to maintain continuous coverage. This approach costs nothing and immediately reveals new accounts you never opened. Look specifically for accounts with unfamiliar names, addresses, or employers because synthetic fraud creates these exact inconsistencies.

Credit monitoring services like Equifax’s free monitoring, Experian’s IdentityWorks, or third-party services provide real-time alerts when new accounts appear on your file. These services typically cost $10 to $25 monthly and send notifications within 24 hours of suspicious activity, giving you time to dispute fraudulent accounts before damage intensifies. Check your credit score monthly through your bank’s free monitoring or credit card issuer’s built-in tools. A sudden score drop of 50 points or more without obvious cause demands immediate investigation.

Take Action Immediately When You Find Fraud

Speed determines outcomes in synthetic identity theft response. Contact all three credit bureaus simultaneously through their fraud departments, not their general customer service lines. File a dispute claiming identity theft and request a fraud alert on your file, which requires creditors to verify your identity before opening new accounts under your Social Security number. The Federal Trade Commission recommends filing an official identity theft report at IdentityTheft.gov, which creates a legally binding document that strengthens your position with creditors and law enforcement. This report gives you specific rights under the Fair Credit Reporting Act that make disputing fraudulent accounts faster and more effective. Contact the fraudulent creditors directly and provide your identity theft report number, demanding they close the accounts and remove them from your credit file. Many creditors will cooperate once you provide documentation, though some require persistence. File a police report with your local police department or state attorney general’s office, creating an official record that supports your dispute claims. Request written confirmation from creditors acknowledging the fraud, then keep these documents permanently because you’ll reference them when applying for credit in the future. Serving South Carolina, including Greenville, Columbia and Charleston.

Final Thoughts

Synthetic identity theft definition encompasses a serious financial crime where fraudsters blend real and fabricated information to create entirely new identities and exploit them for profit. The damage extends far beyond initial fraud, affecting your credit score for years and complicating your ability to secure loans, housing, or employment. Criminals operate invisibly during the critical credit-building phase, meaning you won’t discover the fraud until substantial damage accumulates on your credit file.

Quarterly credit report monitoring, real-time alerts from credit bureaus, and immediate action when you spot unfamiliar accounts represent your strongest defense against this crime. The Federal Trade Commission reports that victims typically discover synthetic fraud within 12 to 18 months after accounts open, leaving months of unchecked damage. This timeline proves that waiting for obvious warning signs leaves you vulnerable to financial devastation.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, navigate credit reporting issues and identity theft cases. If you’ve discovered fraudulent accounts on your credit file or received collection notices for accounts you never opened, contact us to discuss your options. We work to protect your rights and hold creditors accountable when they fail to verify your identity before opening accounts in your name.