How to Choose Identity Theft Insurance Coverage

Identity theft affects millions of Americans annually, and the financial and emotional toll can be devastating. At Hays Cauley, P.C., we help clients understand their options for protecting themselves, including identity theft insurance coverage.

This guide walks you through what to look for in a policy, how to compare plans, and how to select coverage that matches your actual needs. You’ll learn what these policies cover, what they don’t, and how to avoid paying for protection you don’t need.

Understanding Identity Theft Insurance Coverage

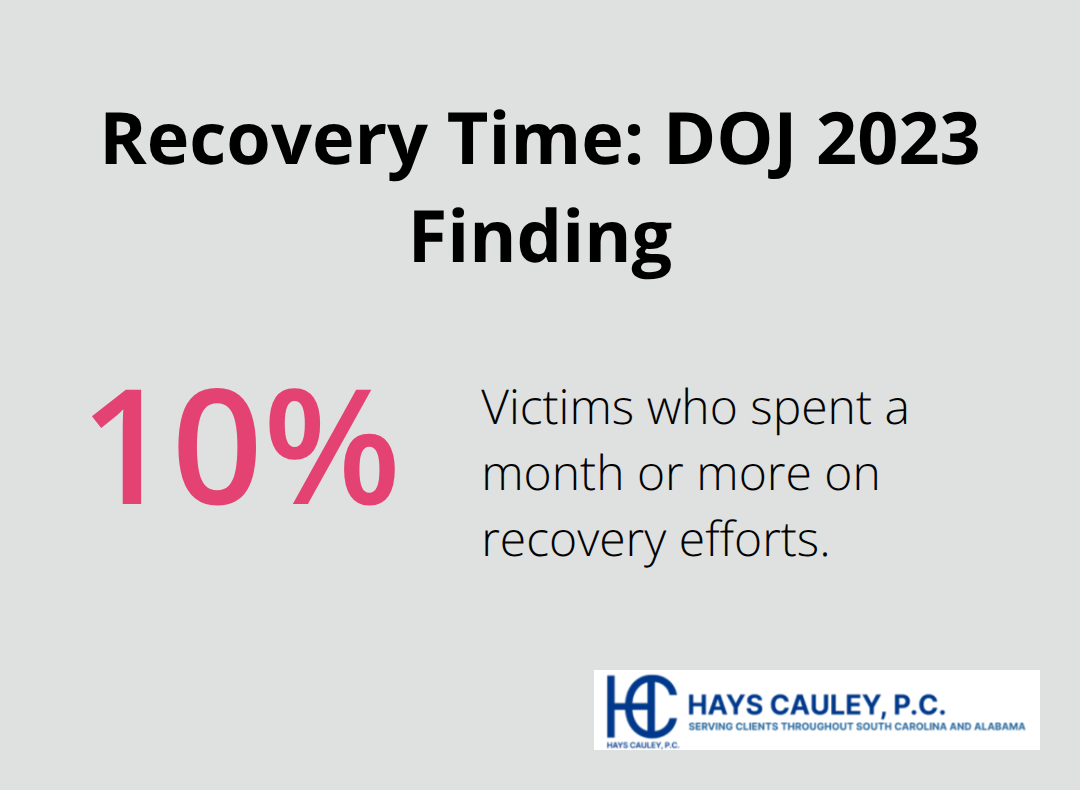

Identity theft insurance reimburses specific out-of-pocket expenses you incur while recovering your identity after fraud occurs. This is fundamentally different from what many people assume. The policy covers costs like notary fees, copies of your credit report, bank fees, lost wages during recovery, childcare expenses for court appearances, and legal fees. Some policies extend to case manager fees and document replacement costs. Coverage limits typically range from $25,000 to $1 million, though you should verify the exact amount before purchasing. A 2023 Department of Justice study found that most victims resolved financial and credit problems within a week, but about 10 percent spent a month or more on recovery-meaning those legal and administrative costs add up quickly.

What Identity Theft Insurance Does Not Cover

Most identity theft insurance policies do not reimburse stolen funds directly. If a thief drains your bank account or runs up charges on your credit card, standard coverage won’t repay that money. Banks and credit card companies typically won’t hold you responsible for unauthorized charges if you report them quickly, so stolen funds reimbursement is less common than recovery cost coverage. Some providers offer stolen funds reimbursement on all plans, but they cap identity theft insurance coverage at $25,000-a trade-off worth considering. You need to read the policy terms carefully because coverage varies dramatically between providers. Policies also exclude expenses you could have prevented with basic security practices, and they don’t cover ongoing financial losses from poor credit decisions made after the theft.

How This Differs from Credit Monitoring

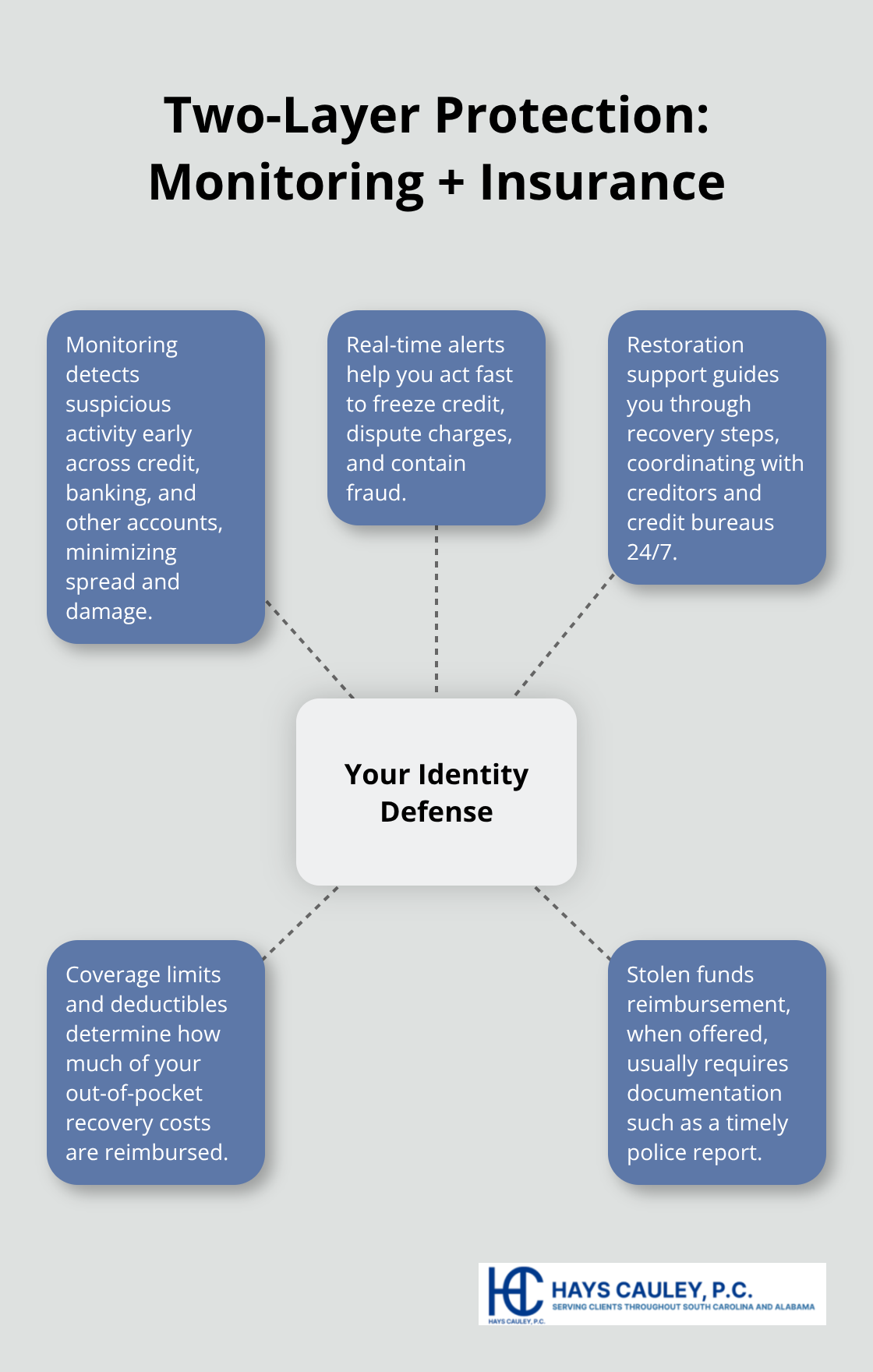

Credit monitoring services and identity theft insurance serve different purposes and shouldn’t be confused. Monitoring services watch your credit reports, bank accounts, investment accounts, and sometimes the dark web for suspicious activity, alerting you to potential fraud in real time. These services catch theft early before damage spreads. Identity theft insurance, by contrast, activates after fraud has occurred and helps you pay for recovery. Many providers bundle both together, offering credit monitoring from all three major bureaus (Experian, TransUnion, Equifax) alongside insurance coverage. The Federal Trade Commission provides IdentityTheft.gov for reporting identity theft and creating personalized recovery plans at no cost. Having both monitoring and insurance creates a two-layer defense: monitoring detects the problem quickly, and insurance covers your recovery costs. If you already have free credit monitoring through a data breach or your credit card issuer, you may only need the insurance component.

What Comes Next in Your Selection Process

Now that you understand what these policies actually cover and how they differ from monitoring services, you’re ready to compare specific plans. The next chapter walks you through the key features that matter most and how to evaluate whether a plan’s cost justifies its benefits.

Comparing Identity Theft Insurance Plans: Serving South Carolina, including Greenville, Columbia and Charleston

The market for identity theft insurance has fragmented into dozens of providers, each claiming superior protection. Your job is to cut through the noise and match a plan to what you actually need.

What Gets Monitored Matters Most

Start by looking at what each plan monitors. The stronger plans monitor all three credit bureaus weekly and pull full credit reports monthly, but many also track bank accounts, credit cards, investment accounts, and tax returns for unauthorized activity. Some extend monitoring to the dark web, USPS address changes, and criminal records. This matters because synthetic identity fraud is rising year over year, and victims often face at least around $1,000 out-of-pocket to recover. If you carry investments or have multiple financial accounts, you need a plan that covers those. IdentityIQ offers $1 million in stolen funds reimbursement on all plans, which is rare and valuable if that coverage aligns with your concerns.

Restoration Support Makes the Difference

Next, evaluate the restoration support structure. You want a dedicated identity restoration specialist available 24/7 who will guide you through freezing credit, disputing fraudulent charges, and replacing documents. This is not a generic helpline; it should be someone who understands the process and can coordinate with creditors and bureaus on your behalf. The difference between a plan that provides this and one that doesn’t is the difference between spending 100 to 200 hours recovering your identity and spending significantly less. South Carolina residents should note that security freezes are free under state law, and removal or lifting takes three business days, so your plan’s restoration team should know these timelines and use them effectively.

Cost Varies Dramatically Across Providers

Cost ranges widely by provider and plan tier. Individual plans run from about $8 to $50 per month, while family plans typically cost around $15 per month. Aura ranges from $12 to $32 monthly, LifeLock from $7.50 to $38.99, Identity Guard from $6.67 to $23.99, and IdentityForce from $16.66 to $33.33.

Before you choose based on price alone, check what you already have. Many credit card issuers, employers, and homeowners or renters policies include some identity theft coverage or free credit monitoring. If you already have monitoring through your credit card, adding another monitoring service wastes money. In that case, a standalone identity theft insurance policy with strong restoration support makes more sense.

Security Features and Customer Support Quality

Look for providers with AES-256 encryption, two-factor or multi-factor authentication including biometrics on mobile apps, and clear privacy policies that limit data sharing. Customer support quality matters enormously; test their responsiveness by contacting them before you buy. Read recent customer reviews on independent sites, not just the provider’s website. A plan with 31 alerts in the first week of monitoring, as Aura’s testing showed, demonstrates active real-time detection. Finally, check coverage limits and deductibles carefully. Most plans cap identity theft insurance coverage between $25,000 and $1 million, and some charge deductibles. Stolen funds reimbursement, when available, typically requires you to have filed a police report and documented the theft through proper channels.

Moving Forward With Your Selection

The annual cost of quality coverage-$20 to $60 per year for basic plans-is reasonable given that recovery can consume months of your time and thousands of dollars in expenses. With this understanding of what to monitor, how restoration support works, and what price ranges look like, you’re ready to assess your personal risk factors and identify coverage gaps specific to your situation.

Steps to Select the Right Identity Theft Insurance for Your Needs: Serving South Carolina, including Greenville, Columbia and Charleston

Calculate Your Real Exposure to Identity Theft

Start with your actual risk profile. South Carolina ranks 13th in identity theft reports per 100,000 citizens, which means your risk exceeds the national average. Assess what you own and what a thief could access. If you hold investment accounts, multiple bank accounts, or significant assets, you need a plan that monitors all three credit bureaus plus bank and investment accounts. If tax fraud concerns you most, you need monitoring of tax returns and the ability to file with MyDORWAY safely. The Federal Trade Commission data shows 15 million Americans faced identity theft in 2023, with victims spending 100 to 200 hours on recovery. Your time carries monetary value, so factor that into your decision. A plan costing $25 per month ($300 annually) becomes cost-effective if it saves you even 12 hours of recovery work at a reasonable hourly rate.

Audit Your Current Coverage and Protections

Next, examine what you already have in place. Check whether your employer offers identity theft coverage or monitoring as a benefit-many do, and employees never use it. Review your homeowners or renters policy, as some insurers include limited identity theft coverage. Call your credit card issuer and ask explicitly what fraud protections they provide; most cover unauthorized charges within a few days of reporting. If you experienced a data breach, you may have free credit monitoring for a year or more through that company. South Carolina law requires security freezes to be placed within five business days at no cost, and removal takes three business days, so you already have one powerful tool available. If you find you have free monitoring through your employer or credit card, skip paying for duplicate monitoring and instead purchase standalone identity theft insurance with strong restoration support. That combination covers both detection and recovery without waste. If you have neither monitoring nor insurance, a bundled plan makes sense economically. Plans running $15 to $25 monthly provide both, which beats paying separately.

Match Plan Features to Your Specific Gaps

Align the plan’s features with your specific needs. If you own a small business or have employees, check whether the plan covers business identity theft or employee data breaches. If you have children, some plans extend monitoring to minors at no extra cost-this matters because child identity theft often goes undetected for years. If you manage aging parents’ finances, look for plans covering multiple family members; most family plans cap coverage at $1 million across all members, which remains substantial. Evaluate restoration support capacity by asking the provider how many cases their specialists handle monthly and what their average resolution time is. A specialist handling 50 cases monthly has more bandwidth than one handling 200. Read the fine print on stolen funds reimbursement-if included, it typically requires a police report filed within 30 days of discovery. South Carolina allows victims to petition for expedited judicial determination of factual innocence if their identity was used to commit crimes, and your plan’s restoration team should know this process.

Test Customer Service Before You Commit

Contact the provider’s support line with a question and time how long it takes to receive a meaningful response. A plan with excellent coverage but mediocre support becomes frustrating when you actually need help during a crisis. Read recent customer reviews on independent sites, not just the provider’s website. Ask the provider how many cases their specialists handle monthly and what their average resolution time is. Verify that the plan includes 24/7 restoration support and that specialists can coordinate with creditors and bureaus on your behalf. Check coverage limits and deductibles carefully. Most plans cap identity theft insurance coverage between $25,000 and $1 million, and some charge deductibles. Stolen funds reimbursement, when available, typically requires you to have filed a police report and documented the theft through proper channels. A plan with active real-time detection (demonstrated by multiple alerts within the first week of monitoring) shows genuine monitoring capability rather than passive coverage.

Final Thoughts

Identity theft insurance coverage protects your finances and time during recovery, but only if you select a plan matching your actual situation. The policies that work best combine three elements: monitoring across all three credit bureaus plus your financial accounts, restoration support available 24/7, and coverage limits aligned with your potential losses. South Carolina residents benefit from state law-security freezes cost nothing and removal takes three business days-so your plan’s restoration team should activate these tools immediately if theft occurs.

List what you currently have: free monitoring through your employer or credit card issuer, coverage under your homeowners or renters policy, and any existing protections. Then identify your gaps and request quotes from at least two providers, asking each one the same questions about coverage limits, stolen funds reimbursement, restoration specialist availability, and average resolution time. Most quality plans cost $20 to $60 annually, making the financial commitment minimal compared to recovery expenses (which can reach thousands of dollars and consume 100 to 200 hours of your time).

If identity theft occurs, contact your insurer immediately, file a police report with local law enforcement, and place fraud alerts with all three credit bureaus. South Carolina residents can file Form I-381 Identity Theft Affidavit with the Department of Revenue and call the dedicated identity theft line at 803-898-7638 for tax-related fraud. Contact Hays Cauley, P.C. for guidance on your rights and options when identity theft strikes.