Identity Theft Victims SC Your Legal Rights And Next Steps In South Carolina

Identity theft victims in SC face serious financial and legal consequences that demand immediate action. Your credit score can plummet, fraudulent accounts may appear in your name, and recovering from the damage takes months or years.

We at Hays Cauley, P.C. help South Carolina residents in Greenville, Columbia, and Charleston understand their rights and take control of the situation. This guide walks you through the legal protections available to you and the concrete steps to protect your future.

How Identity Theft Damages Your Finances

Thieves Act Fast With Your Stolen Information

Thieves who obtain your personal identifying information waste no time putting it to work. They open credit card accounts in your name, take out loans, drain bank accounts, or file fraudulent tax returns. The Federal Trade Commission reports that over 14 million Americans fall victim to identity theft annually, and South Carolina residents are no exception. When a criminal uses your Social Security number, driver’s license number, or banking details, the financial consequences hit fast and hard. Within days, fraudulent charges accumulate across multiple accounts, and creditors begin reporting delinquencies to the credit bureaus under your name.

Your Credit Score Takes an Immediate Hit

Your credit score drops fast and hard. A single identity theft case can lower your score by 50 to 100 points or more, depending on the type and amount of fraudulent activity. The FTC notes that acting within 24 hours of discovering theft limits average losses to about $1,200 instead of $4,800 when action is delayed. Fraudulent accounts remain on your credit report for seven years unless you dispute and remove them, which means your creditworthiness stays damaged long after the initial theft. New accounts opened in your name trigger hard inquiries that further depress your rating. Late payments on accounts you never opened appear as delinquencies, making legitimate borrowing difficult or impossible.

When you apply for a mortgage, car loan, or business credit, lenders see a profile of missed payments and maxed-out accounts that do not belong to you. Your ability to refinance existing debt, qualify for better interest rates, or access new credit becomes severely restricted.

Financial Losses Extend Beyond Credit Damage

The damage spreads far beyond your credit score. Criminals may drain your checking or savings accounts directly, costing you thousands in days. They may establish utility accounts, phone services, or medical services in your name, leaving you responsible for unpaid bills. Tax fraud represents another major threat, with thieves filing returns using your Social Security number to claim refunds. Medical identity theft can result in fraudulent charges appearing on your health insurance, affecting your coverage and leaving you liable for procedures you never received.

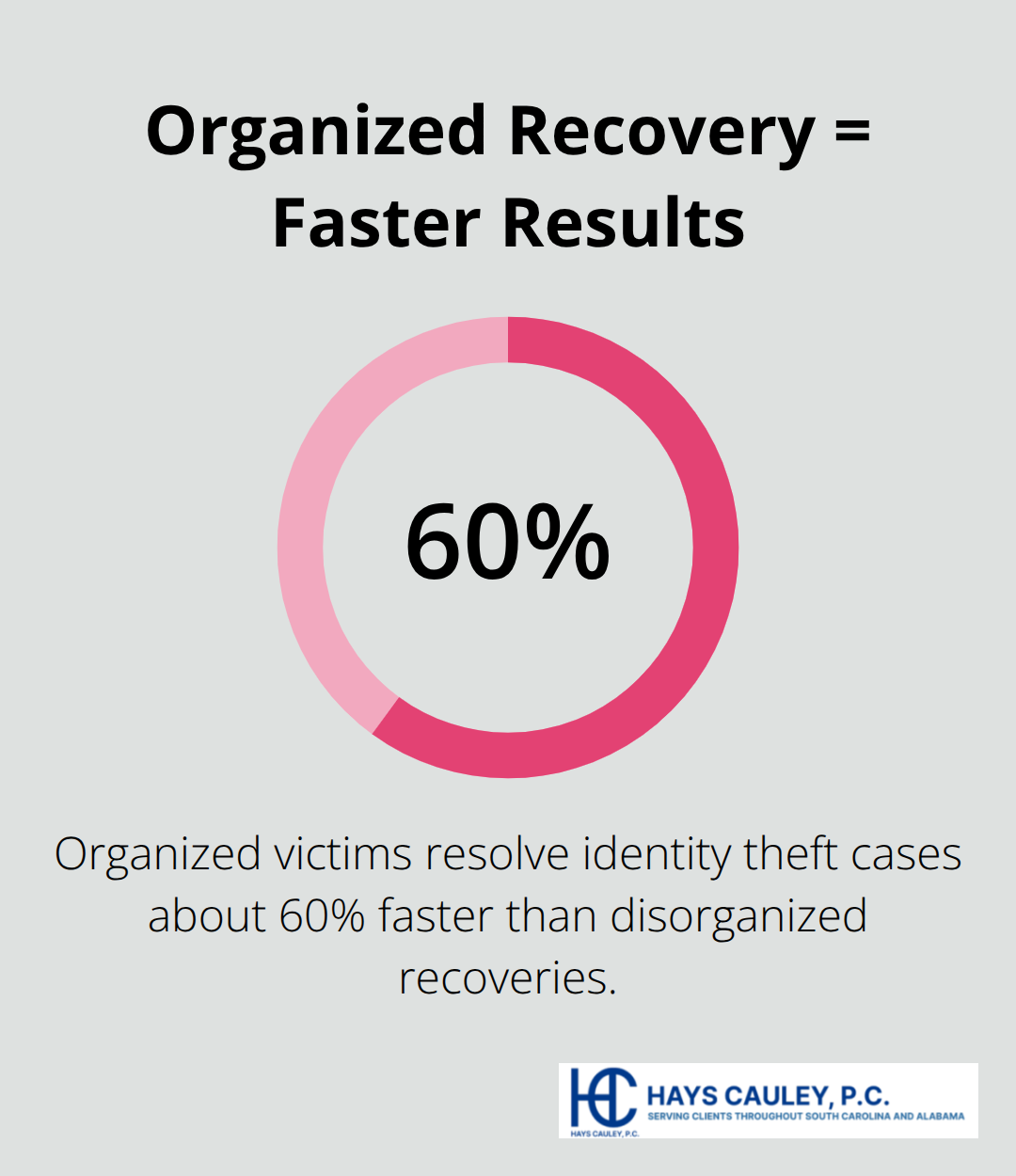

Recovery Takes Time, But Organization Matters

Recovery timelines vary significantly based on how quickly you respond and how organized your dispute process becomes. The Identity Theft Resource Center reports that organized victims resolve cases about 60 percent faster than those without a systematic approach. A disorganized recovery can stretch three to five years, while a methodical dispute process can restore your credit to pre-theft levels in 12 to 18 months if no new fraud occurs. Understanding your legal rights in South Carolina positions you to act strategically and recover faster.

What Legal Protections Do You Actually Have

Federal Law Gives You Real Remedies

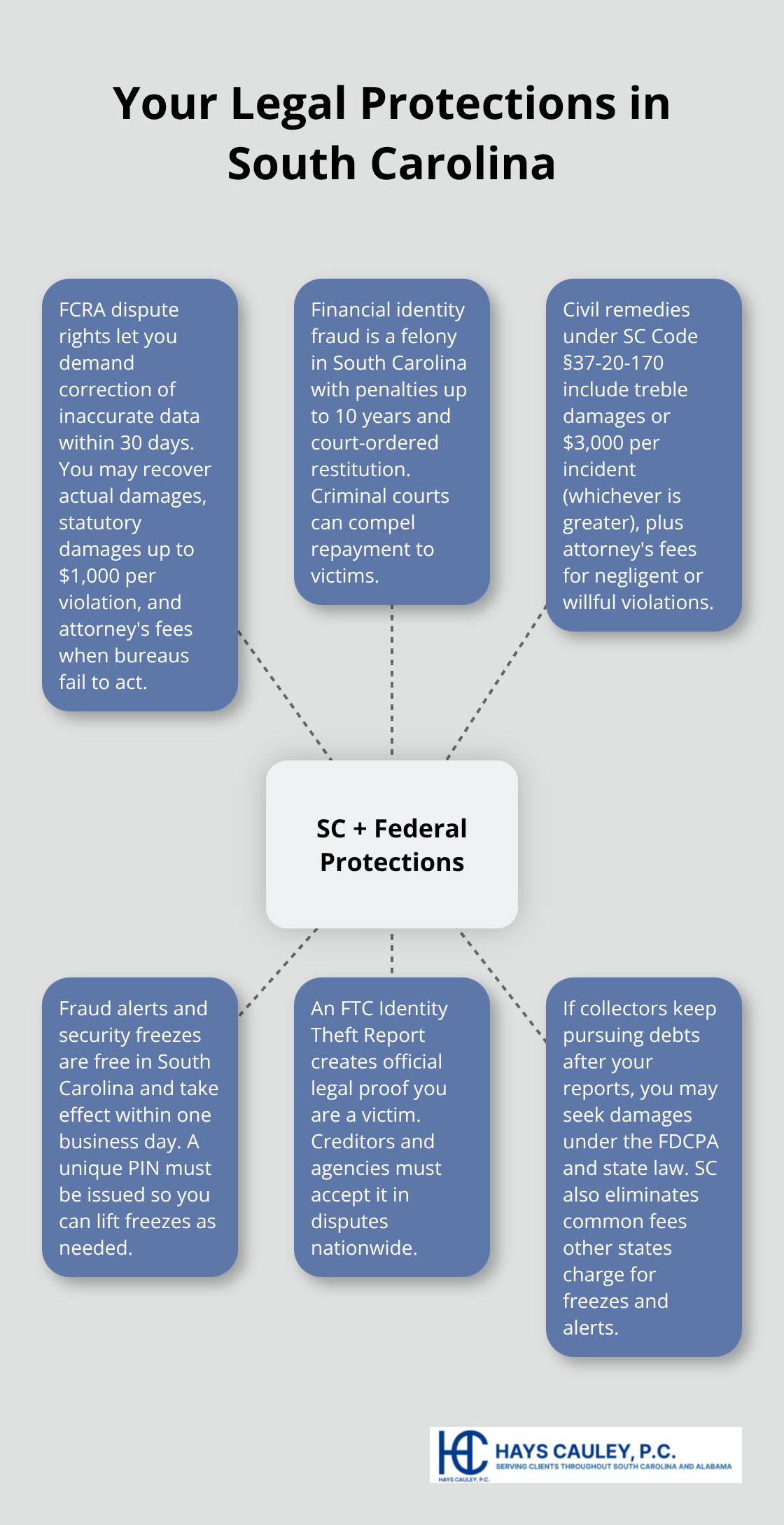

South Carolina and federal law provide concrete remedies when identity theft strikes, but most victims never use them because they do not know they exist. The Fair Credit Reporting Act allows you to dispute fraudulent accounts and demand that credit bureaus correct inaccurate information within 30 days. If a bureau ignores your dispute or refuses to remove verified fraud, you can sue for actual damages, statutory damages up to $1,000 per violation, and attorney’s fees under the FCRA. This legal framework transforms your position from victim to claimant with real leverage against creditors and bureaus that fail to act.

South Carolina State Law Protects You Aggressively

South Carolina state law goes further than most states, making financial identity fraud a felony under Section 16-13-510 with penalties up to 10 years in prison and restitution to victims. This means the criminal justice system can force the thief to repay you directly. You also have civil rights under South Carolina Code Section 37-20-170, which allows you to recover three times your actual damages or $3,000 per incident (whichever is greater), plus attorney’s fees if a creditor or bureau acts negligently or willfully.

Credit bureaus must process your fraud alert within one business day at no cost, and security freezes in South Carolina are free and take effect within one business day after your request. When you place a freeze, the bureau must issue you a unique PIN within ten business days so you can lift it whenever you choose.

Your FTC Identity Theft Report Creates Legal Proof

The FTC Identity Theft Report filed at IdentityTheft.gov creates an official legal record that creditors and agencies nationwide must accept as proof that you are a victim. This document strengthens your position in disputes significantly and signals to lenders and collectors that you have taken formal action. Filing this report within 24 to 48 hours of discovering theft establishes a documented timeline that supports your claims and protects you from liability for fraudulent accounts.

South Carolina Eliminates Costs That Other States Charge

South Carolina residents have additional protections that most states do not offer. The state eliminated all fees for credit freezes and fraud alerts, meaning you can freeze all three bureaus for free without paying the $10 to $20 per bureau that other states charge. If a creditor continues collecting a debt after you have submitted your FTC Identity Theft Report and police report, you can pursue civil damages under the Fair Debt Collection Practices Act and state law. These protections put real financial consequences on creditors who ignore your victim status.

Free Resources From South Carolina’s Consumer Affairs Department

The South Carolina Department of Consumer Affairs Identity Theft Unit provides free assistance including the ID Theft Toolkit, step-by-step checklists for specific fraud scenarios, and one-on-one support at no charge. Contact them at IDTheftHelp@scconsumer.gov or 803-734-4200. When you need to pursue damages against creditors or bureaus that refuse to correct fraud, a consumer protection attorney can evaluate your claim and represent you in court. Hays Cauley, P.C. serves South Carolina residents in Greenville, Columbia, and Charleston and offers confidential case reviews for identity theft victims exploring their legal options.

What to Do in the First 48 Hours

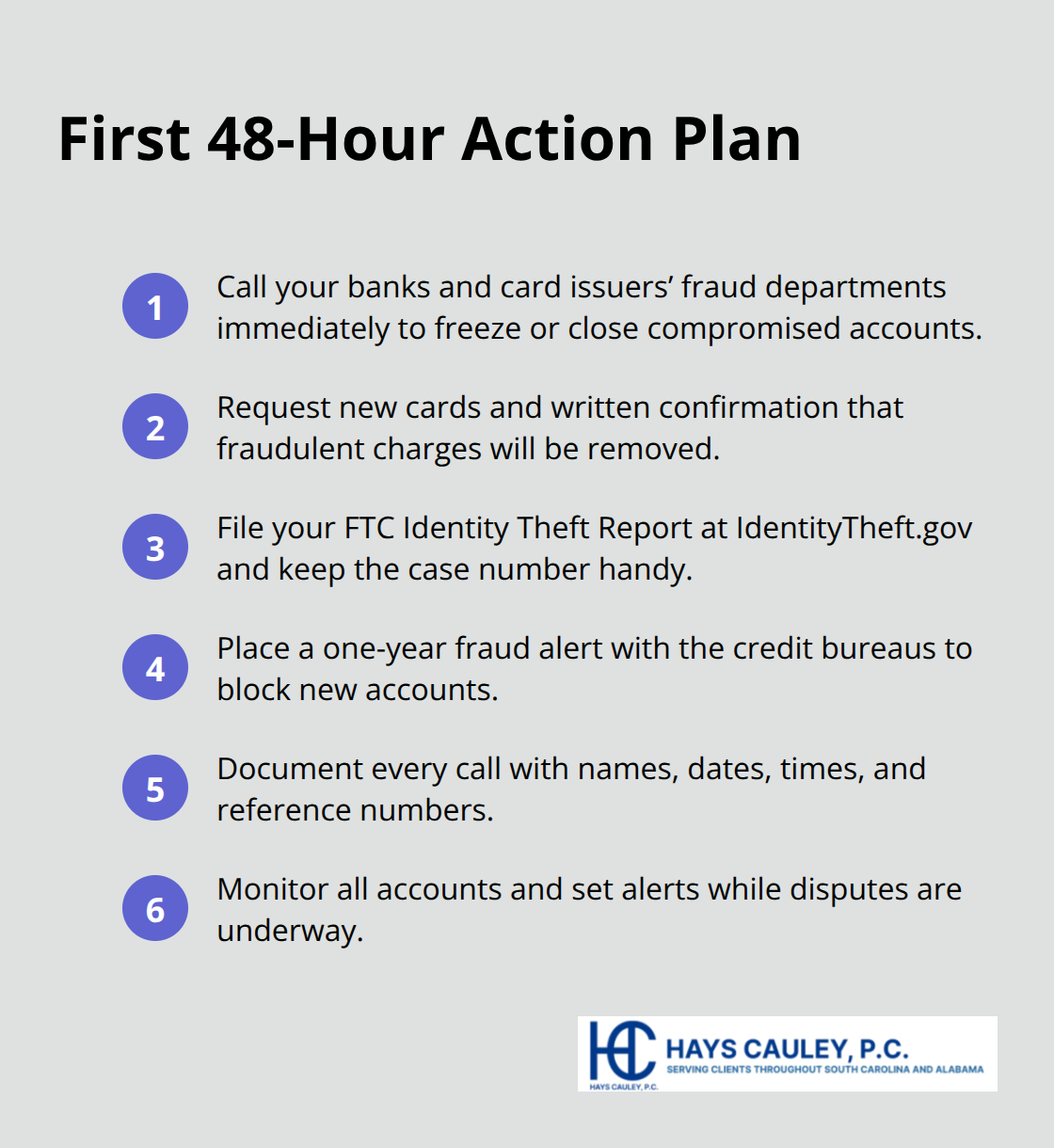

Speed matters more than anything else when identity theft strikes. The Federal Trade Commission found that victims who act within 24 hours limit their average losses to about $1,200, compared to $4,800 when action is delayed. Your first priority is stopping the bleeding by contacting financial institutions and creating an official record with the FTC. These steps take a few hours but prevent weeks of additional damage.

Contact Your Banks and Credit Card Companies Immediately

Start with your banks and credit card issuers immediately, even before filing reports or placing fraud alerts. Call the fraud departments directly using the phone numbers on the back of your cards or statements, not numbers from a Google search. Tell them your account has been compromised and request that they freeze or close the accounts. Ask them to issue new cards with different account numbers and confirm in writing that fraudulent transactions will be removed.

Many banks can reverse unauthorized charges within 24 hours if you report them before the fraud spreads across multiple accounts. Document the name, date, time, and reference number for every call you make. This documentation becomes critical later when you dispute charges or pursue legal claims.

File Your FTC Identity Theft Report Within 24 to 48 Hours

File your FTC Identity Theft Report at IdentityTheft.gov within 24 to 48 hours. This creates an official legal document that creditors and credit bureaus must accept as proof you are a victim, and it generates a case number you will use for every dispute going forward. The report takes about 15 minutes to complete and produces a personalized recovery plan that lists specific actions tailored to your situation.

Save your case number in multiple locations and include it in every written communication with creditors, bureaus, and collectors. This number strengthens your position significantly when you challenge fraudulent accounts or demand corrections from credit reporting agencies.

Place a Fraud Alert With the Credit Bureaus

Contact one of the three major credit bureaus by phone to place a fraud alert, which lasts one year at no cost and takes effect within one business day. Call Equifax at 1-800-525-6285, Experian at 1-888-397-3742, or TransUnion at 1-800-680-7289. The bureau you contact must notify the other two, but calling all three directly ensures faster processing.

The fraud alert instructs lenders to verify your identity before opening new accounts, blocking criminals from opening additional fraudulent lines of credit in your name. Once placed, the alert should prevent the majority of new fraud from occurring while you work on removing existing fraudulent accounts.

Final Thoughts

Identity theft victims in SC who monitor their credit reports every three months for the first two years after theft catch new fraud before it spreads. You can check your reports at annualcreditreport.com for free and request additional reports every 90 days if needed, watching for a 50 to 100 point score drop or accounts you do not recognize as red flags. A security freeze in South Carolina stops criminals from opening new accounts in your name without your permission, takes effect within one business day at no cost, and provides ongoing protection long after fraudulent accounts are resolved.

Pursuing damages against creditors and credit bureaus that refuse to correct fraud transforms your recovery into an offensive legal claim with real financial consequences. Under the Fair Credit Reporting Act and South Carolina law, you can recover actual damages, statutory penalties up to $1,000 per violation, and attorney’s fees when bureaus or creditors act negligently or willfully. A consumer protection attorney evaluates whether your case qualifies for damages and handles negotiations or litigation on your behalf.

We at Hays Cauley, P.C. serve South Carolina residents in Greenville, Columbia, and Charleston and help identity theft victims pursue the compensation they deserve. Contact us for a confidential case review to discuss your options and next steps.