Identity theft and credit errors can wreck your financial life for years. At Hays Cauley, P.C., we help South Carolina residents rebuild their credit and fight back against fraud.

This guide walks you through South Carolina credit repair step-by-step, from filing reports to disputing errors with the three major credit bureaus.

How Identity Theft and Credit Damage Works

Identity Theft Strikes Hard in South Carolina

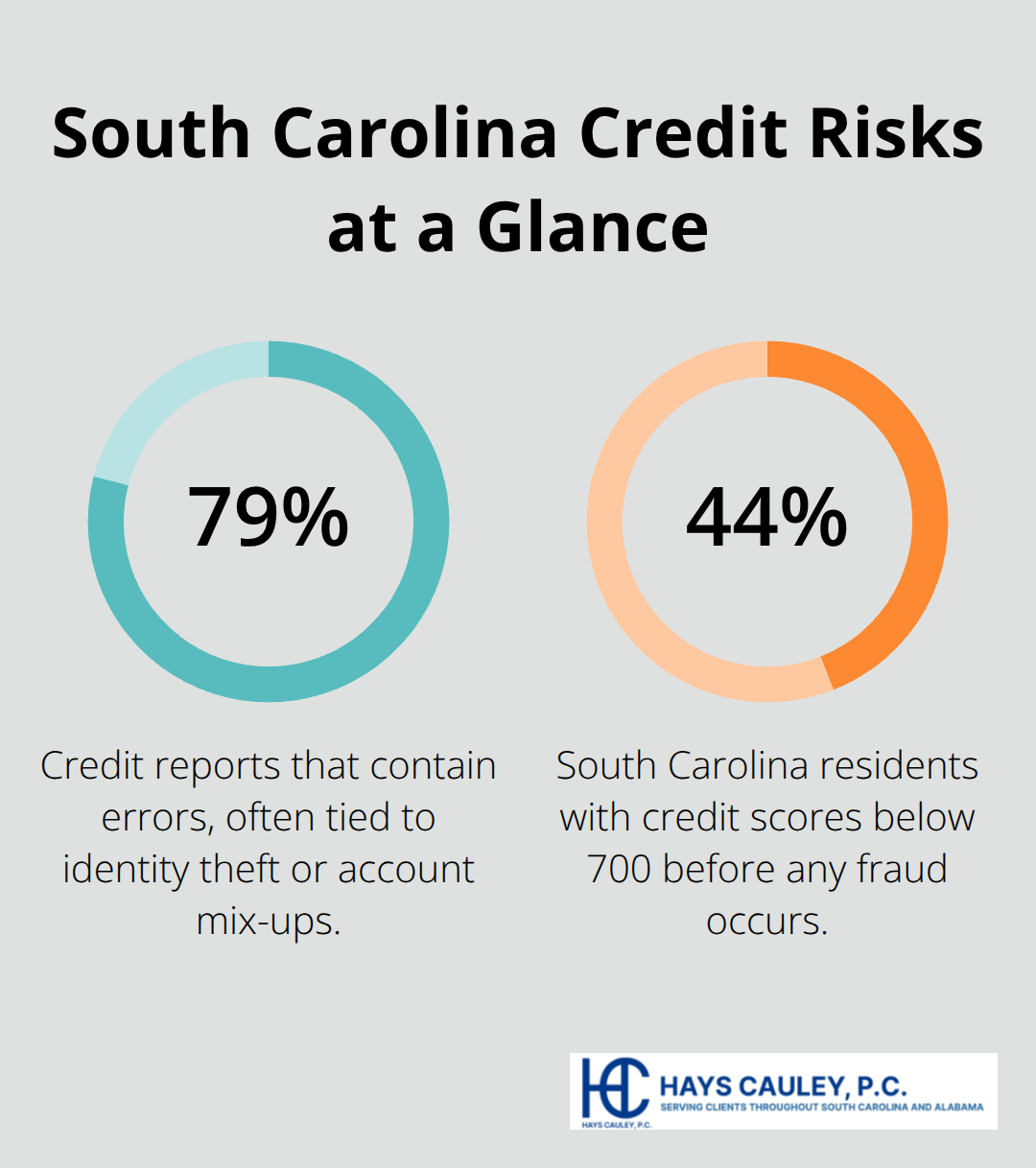

Identity theft costs South Carolina residents thousands of dollars every year, and the damage extends far beyond the initial fraud. About 79% of credit reports contain errors, and many of those errors stem from identity theft or account mix-ups. When a criminal opens accounts in your name or makes unauthorized charges, those fraudulent activities get reported to Equifax, Experian, and TransUnion just like legitimate transactions. Your credit score drops immediately because the bureaus see new accounts, missed payments, or high balances that aren’t actually yours.

How Fraudulent Accounts Tank Your Score

A single fraudulent account can lower your score by 50 to 100 points or more, depending on the account type and payment history. Medical identity theft, where someone uses your information to receive healthcare services, ranks among the most common fraud types in South Carolina. Credit card fraud and account takeovers also damage scores rapidly because they create the appearance of irresponsible borrowing behavior. The bureaus treat fraudulent entries the same way they treat legitimate ones-they report what they receive from creditors and lenders.

The Compounding Financial Damage

The financial impact compounds over time. With 44.3% of South Carolina residents already carrying credit scores below 700, identity theft can push borderline scores into the poor range, making it harder to qualify for loans, mortgages, or even jobs. Lenders view your credit report as proof of your reliability, and fraudulent entries make you look unreliable even though you’re the victim. Higher interest rates follow lower scores, meaning you’ll pay more for credit you actually need.

Some residents in South Carolina spend months or years fighting fraudulent accounts that remain on their reports while legitimate credit opportunities slip away. The longer fraud sits on your report, the more financial damage accumulates. Speed matters when you address identity theft or credit errors-the sooner you report fraud and file disputes, the sooner you can start restoring your financial standing. The next section walks you through the specific steps to take action against fraud and errors on your credit reports.

Start Your Credit Repair in South Carolina, Including Greenville, Columbia and Charleston

File Reports with the FTC and Local Authorities

The moment you discover identity theft or spot errors on your credit report, your instinct might be to panic and call every creditor at once. That approach wastes time and often gets you transferred between departments without resolution. A structured three-step process produces measurable results instead. First, file a report with the Federal Trade Commission at IdentityTheft.gov, which generates a personalized recovery plan and an Identity Theft Report that creditors and bureaus must respect. This report carries legal weight that phone calls alone cannot match.

If you suspect criminal activity beyond fraud, also file a report with local law enforcement in your county. South Carolina residents can contact the South Carolina Identity Theft Unit at IDTheftHelp@scconsumer.gov or call 1-800-922-1594 for guidance specific to your situation. The unit provides step-by-step checklists for common fraud scenarios including medical identity theft, unauthorized credit cards, and compromised government identification. Having both the FTC report and local documentation creates a paper trail that strengthens your position when you dispute accounts.

Dispute Fraudulent Entries with the Three Major Credit Bureaus

Contact Equifax, Experian, and TransUnion directly to dispute fraudulent entries and errors. The Consumer Financial Protection Bureau provides dispute letter templates, but you can also dispute online through each bureau’s website or by phone. When you dispute in writing, include your full contact information, the account number of the disputed item, a clear explanation of what is wrong, copies of supporting documents, and request certified mail with return receipt.

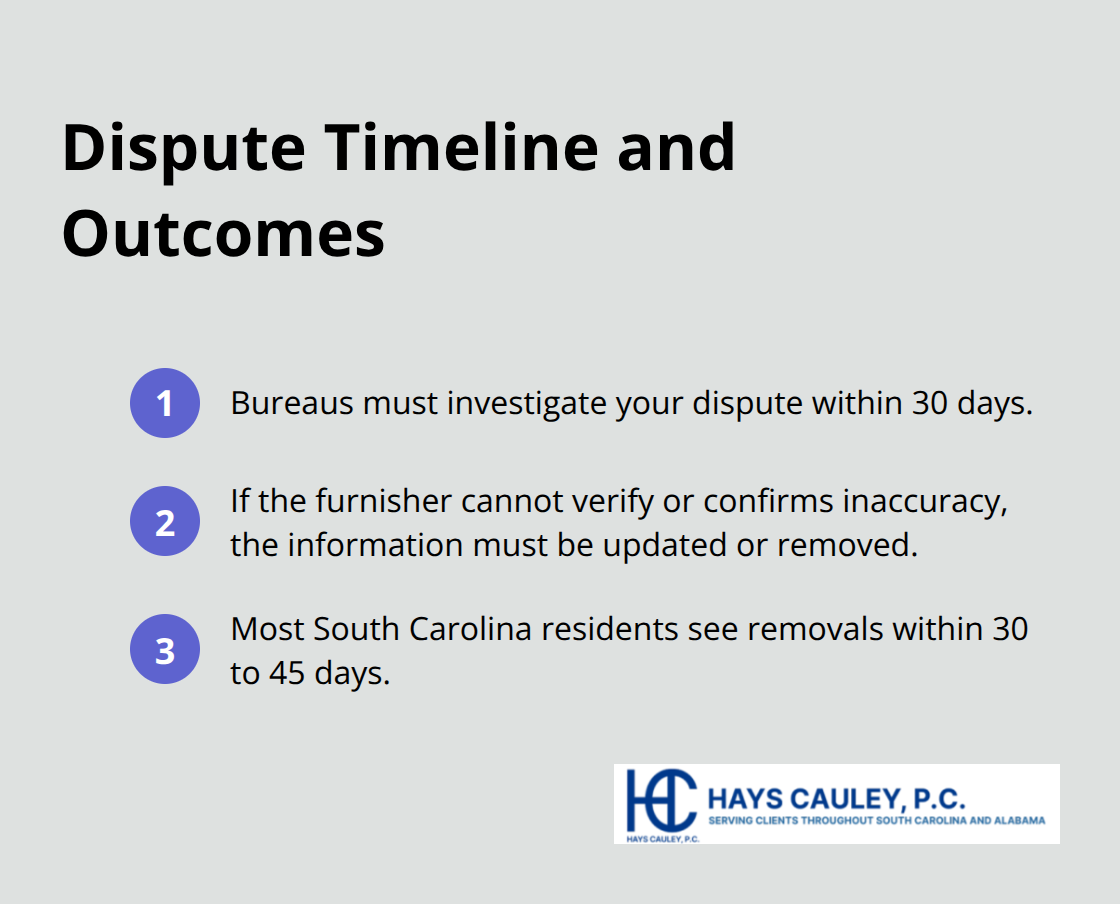

The credit reporting company must investigate within 30 days and forward your dispute to the furnisher-the company that reported the information. If the furnisher cannot verify the account or confirms it is inaccurate, they must update or remove the information across all three bureaus. Most South Carolina residents see disputed fraudulent accounts removed within 30 to 45 days of filing, though complex cases involving identity theft may take longer.

Track Your Progress Across All Three Bureaus

Monitor your progress by checking your credit reports weekly at AnnualCreditReport.com, which provides free weekly access through 2026. Since each bureau maintains different information from different data sources, checking all three reveals which disputes succeeded and where inaccuracies persist. This ongoing monitoring prevents new fraudulent accounts from slipping past your attention and allows you to catch errors that the bureaus may have missed during their initial investigation.

Once you have filed your reports and initiated disputes, the next phase involves understanding what tools and resources can accelerate your recovery and protect you from future fraud.

Recover Your Credit Faster With These Tools and Timeline Expectations

Access Free Credit Monitoring Throughout Your Recovery

Free credit monitoring through Equifax, Experian, and TransUnion accelerates your recovery significantly. Equifax currently offers six free credit reports annually through 2026 when you visit their site or call 1-866-349-5191, while AnnualCreditReport.com provides weekly access to all three bureaus at no cost. This frequency matters because fraudulent accounts sometimes reappear after removal or new fraud activity emerges weeks into your recovery. South Carolina residents should stagger their bureau checks throughout the year rather than pulling all three reports simultaneously, which allows you to catch discrepancies and monitor whether disputed items actually disappeared.

Use Targeted Checklists for Specific Fraud Scenarios

The South Carolina Identity Theft Unit provides free step-by-step checklists for specific fraud scenarios like medical identity theft, unauthorized government identification, and compromised student loan accounts. These targeted checklists guide you through each dispute more efficiently than generic templates. You can access materials tailored to your situation rather than wading through broad recovery instructions that don’t address your particular fraud type.

Understand Your Credit Repair Timeline

Most South Carolina residents see fraudulent accounts removed within 30 to 45 days after filing disputes, though medical identity theft and government document fraud occasionally extend to 60 to 90 days because furnishers require additional verification steps. Identity theft recovery takes time, and complex cases involving multiple fraudulent accounts or identity theft that spans several years may take longer, particularly when the furnisher disputes your claim or requests documentation multiple times. Knowing this timeline helps you set realistic expectations and identify when a dispute has stalled beyond normal processing periods.

Pursue Legal Action When Disputes Fail

Legal support becomes necessary when disputes stall, when bureaus refuse to remove fraudulent entries despite clear evidence, or when identity theft has caused severe financial consequences like denied mortgage applications or job rejections. If you face repeated fraud, ongoing account takeovers, or furnishers that consistently fail to investigate your disputes within 30 days, contact Hays Cauley, P.C. to review whether you have grounds for a complaint with the Consumer Financial Protection Bureau or potential legal action against the bureaus or furnishers themselves.

The Fair Credit Reporting Act and the Credit Repair Organizations Act provide specific protections and remedies that many South Carolina residents don’t realize they possess.

Document Everything for Legal Claims

Your case strengthens considerably when you document every dispute letter, maintain copies of all correspondence, and record dates when you contacted bureaus and furnishers (including the names of representatives you spoke with). This documentation becomes critical evidence if your case requires legal intervention or regulatory complaints.

Final Thoughts

Your credit recovery starts now, not next month or after you gather more documentation. The steps outlined in this guide-filing FTC reports, disputing with the three major credit bureaus, and monitoring your progress-work because they follow the legal framework that protects South Carolina consumers. Identity theft and credit errors won’t disappear on their own, and waiting only extends the financial damage to your score and your ability to qualify for loans, mortgages, or employment opportunities.

Many South Carolina credit repair cases resolve within 30 to 45 days when you take immediate action and follow the dispute process correctly. However, complex situations involving multiple fraudulent accounts, repeated identity theft, or furnishers that refuse to investigate your disputes require professional guidance. If disputes stall beyond 30 days, if bureaus reject your claims without valid reason, or if identity theft has caused significant financial harm like denied mortgage applications, you need legal support to protect your rights.

We at Hays Cauley, P.C. help South Carolina residents navigate credit reporting disputes and identity theft recovery when the standard dispute process fails. Contact us to discuss whether your case qualifies for legal intervention, and reach out to our team for guidance tailored to your specific circumstances.